|

市場調査レポート

商品コード

1693402

タイのシーラント:市場シェア分析、産業動向、成長予測(2025~2030年)Thailand Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| タイのシーラント:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 158 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

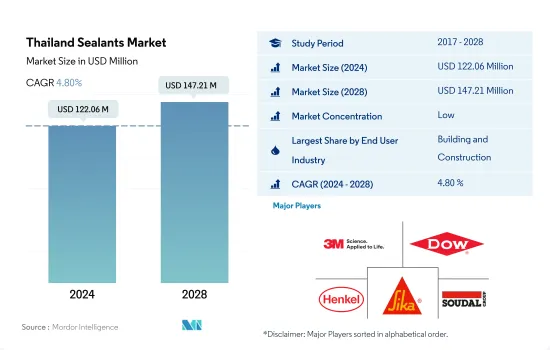

タイのシーラント市場規模は2024年に1億2,206万米ドルと推定され、2028年には1億4,721万米ドルに達すると予測され、予測期間(2024~2028年)のCAGRは4.80%で成長すると予測されます。

自動車産業の勃興と高度医療機器需要の高まりがタイのシーラント消費を押し上げると予測

- 建設産業はタイのシーラント市場で主要なシェアを占めており、建築・建設におけるシーラントの多様な用途により、他のエンドユーザー産業がそれに続いています。さらに、建設用シーラントは、耐用年数が長く、さまざまな基材に簡単に塗布できるように設計されています。建設セクタは、2021年に4,391億3,000万バーツで国のGDPに貢献し、住宅建設への投資の増加により大きな成長を記録する可能性が高く、今後数年間でシーラントの需要を押し上げると予想されます。

- その他のエンドユーザー産業セグメントは、タイのシーラント市場において金額と数量で2番目に高いシェアを占めると予想されており、そのうち電子機器と電気機器が主要な部分を占めると見られています。電気機器製造では、ポッティングや保護用途に様々なシーラントが使用されています。センサやケーブルなどのシールに使用されます。タイのエレクトロニクス産業は、国内に大手メーカーが存在することから、今後数年間で成長する可能性が高いです。これは、他のエンドユーザー産業セグメントにおけるシーラントの生産能力と需要を促進します。

- シーリング材は、自動車産業における様々な用途に使用されており、主にエンジンや自動車のガスケットに使用されています。タイは、生産設備が整備され、主要企業が進出していることから、ここ数年、自動車メーカーの主要拠点となっており、今後数年間、シーラントの需要を生み出す可能性が高いです。シーリング材は、医療機器部品の組み立てやシールといった医療用途にも使用されているため、エンドユーザー産業の中でもタイのシーリング材市場で一定のシェアを占めています。

タイのシーリング材市場の動向

公共インフラプロジェクトへの支出増加が建設セクタの成長を促進しそう

- タイの建設産業は、予測期間2022~2028年にかけて約2.59%のCAGRで推移すると予測されています。タイは、建設業者にとって東南アジアで最もエキサイティングなハブのひとつであり、巨大な建設セクタへの投資が可能です。交通路線や地下鉄インフラの建設など公共事業の増加に伴い、住宅建設の需要は一貫して伸びています。住宅建設は、2014~2019年にかけてタイの建設産業で最大のセグメントであり、2019年にはその総額の40%以上を占めています。建設産業は2023年までに回復すると予想されており、建設支出総額は2021年に4.5~5%、2022~2023年に5~5.5%増加すると予測されています。

- 特に東部経済回廊(Eastern Economic Corridor)では、政府が支援するプロジェクトへの投資が民間投資(工業団地など)のクラウディングインを促すと考えられます。また、近隣諸国でも、経済成長と都市化の継続に対応して政府が国家インフラを整備するため、新たな機会が生まれると考えられます。

- 2021年には、いくつかの住宅プロジェクトが着工し、このセグメントの成長はさらに促進されました。このプロジェクトには、5億700万米ドルのSkyrise Avenue Sukhumvit 64 Mixed-Use Developmentや1億1,700万米ドルのArom Wongamat Condominium Towerなどが含まれます。これらのプロジェクトの完成予定は2024~2025年頃です。同国ではインフラ整備が進んでおり、予測期間中に接着剤需要が高まると予想されます。

ASEAN諸国の中で自動車生産台数全体の50.1%近くを占めるタイが、同産業を牽引するとみられる

- タイの自動車産業は、過去50年間で驚異的な成長を遂げてきました。同国は、より付加価値の高い生産でS字カーブを描く次世代自動車産業を常に進めており、自動車産業施策も環境保護施策との整合を目指しています。タイはASEAN地域最大の自動車生産国です。2020年の生産台数は142万7,074台で、ASEAN全体の50.1%を占めています。これにインドネシア(69万150台、約24.2%)、マレーシア(48万5,186台、約17.0%)が続きます。

- 2019年の自動車生産台数は約201万3,710台を記録したが、2020年には142万7,074台に激減し、COVID-19の流行により約29%の減少を記録しました。その結果、2019~2021年にかけての自動車生産台数の変動は約-16%であったが、2020~2021年にかけての変動は約-1%を記録しました。

- タイは世界第11位、ASEANでは第1位の自動車生産国であり、バリューチェーンが確立されていることから、ASEANのEVセンターとなる準備が整っています。タイのEV在庫は、地元の需要に応えて着実に増加しています。さらに重要なのは、タイの有名企業数社が国内のEV充電インフラに積極的に投資していることで、将来の需要増加に対する確信が高まっていることを示しています。充電ステーションなどのEVインフラを増やす政府機関や民間機関の取り組みは、タイのEVエコシステムが急速に発展していることを示唆しています。

タイのシーラント産業概要

タイのシーラント市場は細分化されており、上位5社で22.73%を占めています。同市場の主要企業は以下の通りです。3M、Dow、Henkel AG & Co. KGaA、Sika AG、Soudal Holding N.V.などです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 規制の枠組み

- タイ

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- 医療

- その他

- 樹脂

- アクリル

- エポキシ

- ポリウレタン

- シリコーン

- その他

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- 3M

- Arkema Group

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Plic Firston(タイ)Co., Ltd

- Shin-Etsu Chemical Co., Ltd.

- Sika AG

- Soudal Holding N.V.

- THE YOKOHAMA RUBBER CO., LTD.

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界の接着剤・シーラント産業概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、抑制要因、機会

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92458

The Thailand Sealants Market size is estimated at 122.06 million USD in 2024, and is expected to reach 147.21 million USD by 2028, growing at a CAGR of 4.80% during the forecast period (2024-2028).

The emerging automotive industry and rising demand for advanced medical equipment are expected to boost the consumption of sealants in Thailand

- The construction industry holds a major share of the Thai sealants market, followed by other end-user industries due to the diverse applications of sealants in building and construction. Moreover, construction sealants are designed for longevity and ease of application on different substrates. The construction sector contributed THB 439.13 billion to the nation's GDP in 2021 and is likely to register significant growth owing to increasing investment in residential construction, which is expected to boost the demand for sealants in the upcoming years.

- The other end-user industries segment is anticipated to hold the second-highest share in value and volume in the Thai sealants market, of which electronics and electrical equipment will account for the major portion. Various sealants are used in electrical equipment manufacturing for potting and protecting applications. They are used for sealing sensors and cables, etc. The Thai electronics industry is likely to grow over the coming years, owing to the presence of major manufacturers in the country. This will foster the production capacity and demand for sealants in the other end-user industries segment.

- Sealants are used in diverse applications in the automotive industry, mostly for engines and car gaskets, and exhibit extensive bonding to various substrates. Thailand has been a major hub for automakers over the last few years due to well-organized production facilities and the presence of leading companies, which is likely to create demand for sealants over the coming years. Sealants are also used for healthcare applications, such as assembling and sealing medical device parts, thus, accounting for a decent share of the Thai sealants market among end-user industries.

Thailand Sealants Market Trends

Increasing spending on public infrastructure projects is likely to facilitate the growth of construction sector

- The Thai construction industry is projected to record a CAGR of about 2.59% during the forecast period 2022-2028. Thailand is one of Southeast Asia's most exciting hubs for contractors, with a huge construction sector to invest in. With increasing public works, such as the construction of transit lines and subway infrastructure, the demand for residential construction has been consistently growing. Residential construction was the largest segment in the Thai construction industry between 2014 and 2019, accounting for more than 40% of its total value in 2019. The construction industry is expected to recover by 2023, with total construction spending having been forecast to rise by 4.5-5% in 2021 and then by 5-5.5% in 2022-2023.

- The major driver in the country for increasing construction will be public-sector spending on infrastructure megaprojects, especially in the Eastern Economic Corridor, where investment in government-backed projects will encourage crowding-in of private-sector investment (e.g., industrial estates). There will also be new opportunities in neighbouring countries as their governments improve national infrastructure in response to continued economic growth and urbanization.

- The segment's growth was further propelled in 2021 as a few residential projects started construction. The projects include the Skyrise Avenue Sukhumvit 64 Mixed-Use Development of USD 507 million and the Arom Wongamat Condominium Tower of USD 117 million, among others. The timelines for completing these projects range from around 2024 to 2025. The growing infrastructure development in the country is expected to generate demand for adhesives over the forecast period.

Nearly 50.1% share of the overall automotive production among the ASEAN countries is likely to drive the industry in Thailand

- The Thai automobile sector has grown tremendously over the last 50 years. The country is constantly advancing its next-generation automotive industry to follow the S-Curve promotion with better value-added production, and it also aims for the automotive industrial policy to be aligned with the environmental protection policy. Thailand is the largest auto producer in the ASEAN region. In 2020, production totaled 1,427,074 units, accounting for 50.1% of total ASEAN production. This was followed by Indonesia (690,150 units, or approximately 24.2%) and Malaysia (485,186 units, or approximately 17.0%).

- In 2019, the country recorded about 20.13,710 units of vehicles produced, which drastically reduced to 14,27,074 units in 2020, accounting for a decline of about 29% owing to the COVID-19 pandemic. As a result, the variation in automotive production between 2019 and 2021 amounted to about -16%, whereas between 2020 and 2021, the variation was recorded at about -1%.

- Thailand, ranked as the 11th largest automotive producer in the world and the first in ASEAN, is poised to become ASEAN's EV center, owing to its well-established value chain, which provides the industry with top-notch quality products at a competitive price. Thailand's EV stock has been steadily increasing in response to local demand. More importantly, several well-known Thai corporations have been actively investing in EV charging infrastructure around the country, indicating rising confidence in future demand increases. Efforts by governmental and private sector institutions to increase EV infrastructure, such as charging stations, suggest that Thailand's EV ecosystem is developing rapidly.

Thailand Sealants Industry Overview

The Thailand Sealants Market is fragmented, with the top five companies occupying 22.73%. The major players in this market are 3M, Dow, Henkel AG & Co. KGaA, Sika AG and Soudal Holding N.V. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.2 Regulatory Framework

- 4.2.1 Thailand

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Healthcare

- 5.1.5 Other End-user Industries

- 5.2 Resin

- 5.2.1 Acrylic

- 5.2.2 Epoxy

- 5.2.3 Polyurethane

- 5.2.4 Silicone

- 5.2.5 Other Resins

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 Dow

- 6.4.4 H.B. Fuller Company

- 6.4.5 Henkel AG & Co. KGaA

- 6.4.6 Plic Firston (Thailand) Co., Ltd

- 6.4.7 Shin-Etsu Chemical Co., Ltd.

- 6.4.8 Sika AG

- 6.4.9 Soudal Holding N.V.

- 6.4.10 THE YOKOHAMA RUBBER CO., LTD.

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms