|

市場調査レポート

商品コード

1693391

ドイツのシーラント:市場シェア分析、産業動向、成長予測(2025~2030年)Germany Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ドイツのシーラント:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 159 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

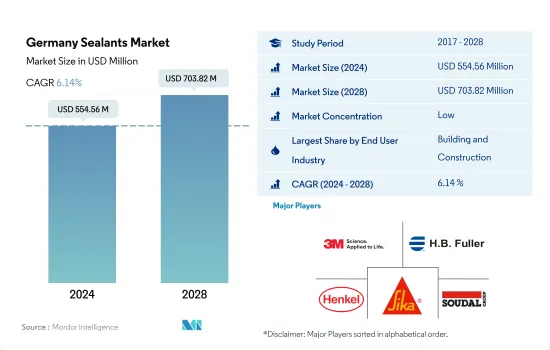

ドイツのシーラント市場規模は、2024年に5億5,456万米ドルと推定され、2028年には7億382万米ドルに達すると予測され、予測期間中(2024~2028年)のCAGRは6.14%で成長します。

ドイツにおけるEV生産の拡大がシーラントの使用を拡大

- ドイツのシーラント市場は、防水、耐候性シーリング、ひび割れシーリング、目地シーリングなど、建築におけるシーラントの多様な用途により、建設産業が牽引し、他のエンドユーザー産業がそれに続きます。ドイツの建設産業はGDPの5.9%近くを占めており、今後数年間のシーラント需要を押し上げる要因となっています。住宅施設の不足と進行中の改修工事による住宅建設プロジェクトの増加は、予測期間中にドイツのシーラント需要を増強します。

- 様々なシーラントが、電子機器や電気機器の製造において、ポッティングや材料保護に広く使用されています。これらはセンサやケーブルなどのシールに使用されます。ドイツのエレクトロニクス市場は世界第6位で、収益シェアは2.6%(2021年)を占めており、今後数年間で成長する可能性が高いです。このことは、他のエンドユーザーセグメントでのシーラント需要を促進することになります。

- ドイツは数十年にわたり、医療産業と自動車産業で大きな発展を遂げてきました。シーラントは、医療機器部品の組み立てやシールなど、医療における用途に使用されています。自動車産業では、ガラス、金属、プラスチック、塗装面など様々な基材にシーラントが使用されています。これらは主にエンジンや自動車のガスケットに使用されています。2021年のプレミアムカーの生産台数において、ドイツは市場シェアの約23%を占めています。ドイツの自動車とOEMは、二酸化炭素排出量を削減するために電気自動車の製造に注力し、産業標準を満たすために車両重量を維持しています。これらの要因は、近い将来、自動車とOEMの生産を増強し、需要に徐々に影響を与えます。

ドイツのシーラント市場動向

デジタルパークや病院などのインフラ整備に向けた政府の取り組みが建設産業を後押し

- 建設業は工業生産高全体の11%を占めます。ドイツの建設産業は、主に住宅建設の増加に牽引され、緩やかなペースで成長しています。ドイツの建設会社は、不動産需要の高騰、建物への投資の増加、インフラに対する国家支出の増加から利益を得ています。過去5年間の欧州中央銀行の超低金利、都市人口の増加、移民の増加が、建設業の好況を後押ししてきました。また、このセグメントは経済成長全体の推進力にもなっています。

- 2021年、ドイツの建設市場は前年比1.99%の成長率を記録しました。ドイツ政府は、ドイツ・ヘッセン州フランクフルト・フェッヘンハイムの10.7ヘクタール、延べ床面積10万平方メートルのデジタルパーク・フェッヘンハイムの建設に着手し、11億7,900万米ドルを投資しました。建設工事は2021年第3四半期に開始され、2028年第4四半期に完成する予定です。2021年第3四半期には、バーデン=ヴュルテンベルク州ロラッハに4億1,800万米ドルを投じて中央病院の建設を開始し、2025年までに完成する予定です。このプロジェクトは、精神保健センターと駐車場を備えた医療デパートの建設を目指しています。

- 低金利、実質可処分所得の増加、欧州連合(EU)やドイツ政府による数多くの投資などが成長を支えるものと考えられます。このため、同国の非住宅と業務用建築物は大きな成長が見込まれ、予測期間中、同国の建設産業は増加する可能性が高いです。

自動車メーカーに対する政府の規制にもかかわらず、電気自動車の需要は自動車産業を推進すると考えられます。

- 自動車製造業はドイツで最も重要な産業であり、国内産業収益の24%はこの産業から生み出されています。ドイツの自動車生産台数は2018年第3四半期に9.4%減少したが、これは同国が2018年後半に景気減速に見舞われたことに加え、新しい世界調和小型車検査方法(WLTP)の実施における問題が重なったためです。

- ドイツで生産される自動車ユニットの75%以上は国際市場向けであり、主に米国、中国、その他のEU諸国です。米国と中国の貿易摩擦は2019年の世界需要を減退させました。これに加え、新たに販売される自動車の平均CO2排出量を1キロメートル当たり95グラムにすることを自動車メーカーに義務付けるEU-28のCO2排出量の新基準が加わり、国内での自動車生産は一時的に制限されました。

- 2020年、COVID-19の大流行は、すでに減少していた自動車生産に大きな打撃を与えました。2020年の自動車生産台数は前年比24.5%減少し、その直後に発生したサプライチェーンの制約と2021年の半導体チップ不足が相まって、自動車生産台数は2020年の水準に比べてさらに10.8%減少しました。チップ不足とサプライチェーン制約の長期的な影響により、予測期間中のドイツの自動車生産は制限されると予想されます。ドイツ政府のeモビリティ計画では、2030年までに1,500万台のEVの普及を目指しています。これにより、同国の自動車生産は増加すると予想されます。これらの要因から、ドイツの自動車生産は予測期間中に増加すると予想されます。

ドイツのシーラント産業概要

ドイツのシーラント市場は細分化されており、上位5社で37.69%を占めています。この市場の主要企業は、3M、H.B. Fuller Company、Henkel AG & Co. KGaA、Sika AG、Soudal Holding N.V.などです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 規制の枠組み

- ドイツ

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- 医療

- その他

- 樹脂

- アクリル

- エポキシ

- ポリウレタン

- シリコーン

- その他

第6章 競合情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- 3M

- Arkema Group

- Dow

- EGO Dichtstoffwerke GmbH & Co. Betriebs KG

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- MAPEI S.p.A.

- Sika AG

- Soudal Holding N.V.

- Wacker Chemie AG

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界の接着剤・シーラント産業概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、抑制要因、機会

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92447

The Germany Sealants Market size is estimated at 554.56 million USD in 2024, and is expected to reach 703.82 million USD by 2028, growing at a CAGR of 6.14% during the forecast period (2024-2028).

Growing EV production in Germany to augment the use of sealants

- The German sealants market is driven by the construction industry, followed by other end-user industries due to the diverse application of sealants in building construction, such as waterproofing, weather-sealing, cracks-sealing, and joint-sealing. The German construction industry obtained nearly 5.9% of the country's GDP, propelling the demand for sealants in the coming years. The increasing growth of residential construction projects due to the shortage in housing facilities and ongoing renovation works will augment the sealants demand in Germany during the forecast period.

- A variety of sealants are widely used in electronics and electrical equipment manufacturing for potting and protecting materials. They are used for sealing sensors and cables, etc. The German electronics market is the sixth largest in the world, generating 2.6% (2021) of revenue share, which is likely to grow in the upcoming years. This, in terms, will foster the demand for sealants in the other end-user segment.

- Germany has achieved significant development in the healthcare and automotive industries over the decades. Sealants are used in applications in healthcare, such as assembling and sealing medical device parts. The automotive industry exhibits significant applicability of sealants to various substrates, such as glass, metal, plastic, and painted surfaces. These are mostly used in engines and car gaskets. Germany has registered about 23% of the market share in terms of the production of premium cars in 2021. German automotive and OEMs focus on manufacturing electric vehicles to reduce carbon emissions and maintain vehicle weight to meet the industry standard. These factors will augment automotive and OEM production in the near future, which gradually influences demand.

Germany Sealants Market Trends

The government initiatives towards infrastructure including digital parks and hospitals to boost the construction industry

- Construction accounts for 11% of total industrial production output. The construction industry in the country is growing at a slow pace, majorly driven by increasing new residential construction activities. German construction companies are benefiting from soaring demand for real estate, increased investments in buildings, and higher state spending on infrastructure. The upswing in construction has been encouraged by the European Central Bank's ultra-low interest rates, a growing urban population, and high immigration over the past five years. The sector is also helping to propel overall economic growth.

- In 2021, the construction market in the country registered a 1.99% growth rate compared to the previous year. The German government has initiated the construction of the Digital Park Fechenheim on 10.7 hectares of area, with a gross floor area of 100,000 m2 in Frankfurt-Fechenheim, Hesse, Germany, with an investment of USD 1,179 million. The construction work started in Q3 2021 and is expected to be completed in Q4 2028. In the third quarter of 2021, the country started the construction of the Central Hospital in Lorrach, Baden-Wuerttemberg, with an investment of USD 418 million, and it is expected to be completed by 2025. The project aims to build a center for mental health and a medical department store with a parking garage.

- The growth is likely to be supported by lower interest rates, increased real disposable incomes, and numerous investments by the European Union and the German government. Therefore, with the non-residential and commercial buildings in the country expected to witness significant growth prospects, the construction industry in the country is likely to increase during the forecast period.

Despite the government regulations on carmakers, electrical vehicles demand is likely to propel the automotive industry

- The automotive manufacturing industry is the most important industry in Germany, and 24% of the domestic industry revenue is generated from this industry. Automotive production in Germany declined by 9.4% in the third quarter of 2018, as the country experienced an economic slowdown in the second half of 2018, coupled with the problems in the implementation of the new Worldwide Harmonized Light-Duty Vehicles Test Procedure (WLTP).

- Over 75% of the automotive units manufactured in Germany are destined for international markets, which are mainly the United States, China, and other EU countries. The trade conflicts between the United States and China sapped away the global demand in 2019. This, coupled with the new EU-28 standard of CO2 emissions, which mandates carmakers to achieve average CO2 emissions of 95 grams per kilometer across newly-sold vehicles, has briefly restricted automotive production in the country.

- In 2020, the COVID-19 pandemic hit hard on the already declining automotive production. In 2020, automotive production fell by 24.5% Y-o-Y, and the supply chain constraints that quickly followed, coupled with the semiconductor chip shortage in 2021, have further declined automotive production by 10.8% compared to 2020 levels. The long-lasting effects of chip shortages and supply chain restrictions are expected to restrict automotive production in Germany in the forecast period. The German government's e-mobility plan aims to achieve 15 million EVs on the road by 2030. This is expected to drive up automotive production in the country. Due to all these factors, Germany's automotive production is expected to increase during the forecast period.

Germany Sealants Industry Overview

The Germany Sealants Market is fragmented, with the top five companies occupying 37.69%. The major players in this market are 3M, H.B. Fuller Company, Henkel AG & Co. KGaA, Sika AG and Soudal Holding N.V. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.2 Regulatory Framework

- 4.2.1 Germany

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Healthcare

- 5.1.5 Other End-user Industries

- 5.2 Resin

- 5.2.1 Acrylic

- 5.2.2 Epoxy

- 5.2.3 Polyurethane

- 5.2.4 Silicone

- 5.2.5 Other Resins

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 Dow

- 6.4.4 EGO Dichtstoffwerke GmbH & Co. Betriebs KG

- 6.4.5 H.B. Fuller Company

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 MAPEI S.p.A.

- 6.4.8 Sika AG

- 6.4.9 Soudal Holding N.V.

- 6.4.10 Wacker Chemie AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms