|

市場調査レポート

商品コード

1693384

タイの接着剤:市場シェア分析、産業動向、成長予測(2025~2030年)Thailand Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| タイの接着剤:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

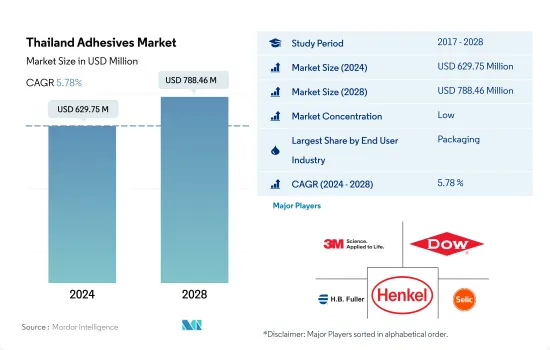

タイの接着剤市場規模は2024年に6億2,975万米ドルと推定され、2028年には7億8,846万米ドルに達すると予測され、予測期間中(2024~2028年)のCAGRは5.78%で成長する見込みです。

タイの自動車産業は、同国における接着剤需要の全体的な成長において重要な役割を担っています。

- 2020年の接着剤消費量は、COVID-19の大流行により2019年比で約11.6%減少しました。この大流行は、製造拠点の閉鎖や需要の減少により、タイの接着剤消費量に深刻な影響を与えました。タイでは3ヵ月近く閉鎖が続き、サプライチェーンの混乱と労働力不足が生じた。しかし、2021年の消費は、製造部門からの安定した需要により、約10%のプラス成長率を記録しました。

- 接着剤は、プラスチック、金属、紙や段ボールの包装用途の接着に重要な役割を果たすため、国内の包装産業で主に消費されています。水性接着剤は、コストが安く、接着強度が高いため、これらの用途で必要とされ、同産業で大量に消費されています。タイの包装産業では、2021年に約2万6,000トンの水性接着剤が消費されました。溶剤系接着剤は包装産業で最も急成長している技術であり、このセグメントは2022~2028年にかけてCAGR 2.37%を記録すると予想されています。

- 自動車産業は、タイにおける接着剤の第2位の消費者です。同国の自動車生産能力は168万台に達し、前年比18%増となったことから、自動車用接着剤市場は2021年に16.62%成長しました。国際市場におけるタイの自動車輸出需要の高まりが、今後数年間の自動車用接着剤需要を牽引すると予想されます。自動車輸出額は2021年に414億3,000万米ドルに達します。

タイの接着剤市場動向

食品、化粧品、その他産業におけるプラスチック包装の需要拡大が包装産業を牽引

- タイは2022年に1人当たり7,450米ドルのGDPを記録し、前年比成長率は3.3%でした。包装産業は同国のGDPの約1.91%を占めています。貿易為替、雇用、人件費、政府の施策支援などがタイの包装産業に影響を与えます。

- 2020年、COVID-19パンデミックのため、タイの経済は減速しました。同年の生産量は2019年と比較して4.74%減少しました。これは、サプライチェーンの混乱、労働力不足、3ヶ月近くにわたる国内封鎖のために起こりました。しかし、2021年に国際国境が開放されたことに伴う国内の景気回復により、生産に必要な原料の定期的な供給が始まり、2021年には7,900トン増加しました。

- タイは世界のプラスチック包装市場の主要製造国のひとつです。プラスチック包装産業は年間50億米ドルに達し、他タイプの包装の中で最も高いです。同国のプラスチック生産量の約28%がプラスチック包装製品に使用されています。この包装は主に食品、医療、化粧品、その他多くの製品タイプに使用されています。

- タイの包装産業におけるバイオプラスチックの使用量は増加しています。政府もプラスチック廃棄物管理ロードマップ(2018~2030年)などの施策を通じて、バイオプラスチック産業の開発を優先しています。GCとカーギルは、タイにバイオプラスチック工場を新設するために200億米ドルを投資する計画を発表している多国籍バイオポリマー企業です。

ASEAN諸国の自動車生産台数の50.1%近くがタイの自動車産業を牽引すると思われる

- タイの自動車産業は過去50年間に目覚しい成長を遂げました。同国は、より付加価値の高い生産でS字カーブを描く次世代自動車産業を常に進めており、自動車産業施策が環境保護施策と整合することも目指しています。タイはASEAN地域最大の自動車生産国です。2020年の生産台数は142万7,074台で、ASEAN全体の50.1%を占めています。これにインドネシア(69万150台、約24.2%)、マレーシア(48万5,186台、約17.0%)が続きます。

- 2019年の自動車生産台数は約201万3,710台を記録したが、2020年には142万7,074台に激減し、COVID-19の流行により約29%の減少を記録しました。その結果、2019~2021年にかけての自動車生産台数の変動は約-16%であったが、2020~2021年にかけての変動は約-1%を記録しました。

- タイは世界第11位、ASEANでは第1位の自動車生産国であり、バリューチェーンが確立されていることから、ASEANのEVセンターとなる準備が整っています。タイのEV在庫は、地元の需要に応えて着実に増加しています。さらに重要なのは、タイの有名企業数社が国内のEV充電インフラに積極的に投資していることで、将来の需要増加に対する確信が高まっていることを示しています。充電ステーションなどのEVインフラを増やす政府機関や民間機関の取り組みは、タイのEVエコシステムが急速に発展していることを示唆しています。

タイの接着剤産業概要

タイの接着剤市場は細分化されており、上位5社で29.77%を占めています。この市場の主要企業は、3M、Dow、H.B. Fuller Company、Henkel AG & Co. KGaA、Selic Corp Public Company Limited.などです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- フットウェア皮革

- 包装

- 木工・建具

- 規制の枠組み

- タイ

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- フットウェアと皮革

- 医療

- 包装

- 木工・建具

- その他

- 技術

- ホットメルト

- 反応性

- 溶剤系

- UV硬化型接着剤

- 水性

- 樹脂

- アクリル系

- シアノアクリレート

- エポキシ

- ポリウレタン

- シリコーン

- VAE・EVA

- その他

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- 3M

- Arkema Group

- Dow

- DUNLOP ADHESIVES(THAILAND)CO., LTD.

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Selic Corp Public Company Limited.

- Sika AG

- Star Bond (Thailand) Company Limited

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界の接着剤・シーラント産業概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、抑制要因、機会

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92439

The Thailand Adhesives Market size is estimated at 629.75 million USD in 2024, and is expected to reach 788.46 million USD by 2028, growing at a CAGR of 5.78% during the forecast period (2024-2028).

Thailand's Automotive industry having a significant role in the overall growth of adhesive's demand in the country

- The consumption of adhesives declined in 2020 by about 11.6% compared to 2019 due to the COVID-19 pandemic, which severely affected the consumption of adhesives in Thailand owing to the closedown of the manufacturing sites and reduction in demand. The lockdown in the country for nearly three months resulted in supply chain disruptions and labor shortages. However, consumption registered growth in 2021 with a positive growth rate of about 10% due to steady demand from the manufacturing sector.

- Adhesives are majorly consumed in the packaging industry in the country owing to their importance in bonding plastics, metals, and paper and cardboard packaging applications. Water-borne adhesives are highly consumed in the industry because of their cheaper cost and high bonding strength, which is required in these applications. Nearly 26 thousand tons of water-borne adhesives were consumed in the Thai packaging industry in 2021. Solvent-borne adhesives are the fastest-growing technology in the packaging industry, and the segment is expected to register a CAGR of 2.37% from 2022 to 2028.

- The automotive industry is the second-largest consumer of adhesives in Thailand. The automotive adhesives market grew by 16.62% in 2021, as the country's total vehicle manufacturing capacity reached 1.68 million units, up by 18% from the previous year. The rising demand for Thailand's automotive exports in the international market is expected to drive the demand for automotive adhesives over the coming years. The automotive export value reached USD 41.43 billion in 2021.

Thailand Adhesives Market Trends

Growing demand for plastic packaging in food, cosmetics, and other industries will propel the packaging industry

- Thailand registered a GDP of USD 7,450 per capita with a growth rate of 3.3% Y-O-Y in 2022. The packaging industry contributes a share of around 1.91 of the country's GDP. Trade exchange, employment, labor charges, government policy support, etc., affect the Thai packaging industry.

- The country observed an economic slowdown in 2020 because of the COVID-19 pandemic. Production volume declined by 4.74% in the same year compared to 2019. This happened due to supply chain disruptions, labor shortages, and a lockdown in the country for nearly three months. However, because of economic recovery in the country in line with international borders being opened in 2021, the regular supply of raw materials began for production, which increased by 7,900 ton in 2021.

- Thailand is one of the major manufacturing countries in the global plastic packaging market. The plastic packaging industry reaches USD 5 billion annually, the highest among other types of packaging. Around 28% of the country's plastic production is used in plastic packaging products. This packaging is majorly used in food, healthcare, cosmetics, and many other types of products in Thailand.

- The usage of bioplastics in the packaging industry of Thailand is increasing. The government has also prioritized the bioplastic industry's development through policies such as the Plastic Waste Management Roadmap (2018-2030). GC and Cargill are two multinational biopolymer companies that have announced plans to invest USD 20 billion in establishing new bioplastic plants in Thailand.

Nearly 50.1% share of the overall automotive production among the ASEAN countries is likely to drive the industry in Thailand

- The Thai automobile sector has grown tremendously over the last 50 years. The country is constantly advancing its next-generation automotive industry to follow the S-Curve promotion with better value-added production, and it also aims for the automotive industrial policy to be aligned with the environmental protection policy. Thailand is the largest auto producer in the ASEAN region. In 2020, production totaled 1,427,074 units, accounting for 50.1% of total ASEAN production. This was followed by Indonesia (690,150 units, or approximately 24.2%) and Malaysia (485,186 units, or approximately 17.0%).

- In 2019, the country recorded about 20.13,710 units of vehicles produced, which drastically reduced to 14,27,074 units in 2020, accounting for a decline of about 29% owing to the COVID-19 pandemic. As a result, the variation in automotive production between 2019 and 2021 amounted to about -16%, whereas between 2020 and 2021, the variation was recorded at about -1%.

- Thailand, ranked as the 11th largest automotive producer in the world and the first in ASEAN, is poised to become ASEAN's EV center, owing to its well-established value chain, which provides the industry with top-notch quality products at a competitive price. Thailand's EV stock has been steadily increasing in response to local demand. More importantly, several well-known Thai corporations have been actively investing in EV charging infrastructure around the country, indicating rising confidence in future demand increases. Efforts by governmental and private sector institutions to increase EV infrastructure, such as charging stations, suggest that Thailand's EV ecosystem is developing rapidly.

Thailand Adhesives Industry Overview

The Thailand Adhesives Market is fragmented, with the top five companies occupying 29.77%. The major players in this market are 3M, Dow, H.B. Fuller Company, Henkel AG & Co. KGaA and Selic Corp Public Company Limited. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Footwear and Leather

- 4.1.5 Packaging

- 4.1.6 Woodworking and Joinery

- 4.2 Regulatory Framework

- 4.2.1 Thailand

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Packaging

- 5.1.7 Woodworking and Joinery

- 5.1.8 Other End-user Industries

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Solvent-borne

- 5.2.4 UV Cured Adhesives

- 5.2.5 Water-borne

- 5.3 Resin

- 5.3.1 Acrylic

- 5.3.2 Cyanoacrylate

- 5.3.3 Epoxy

- 5.3.4 Polyurethane

- 5.3.5 Silicone

- 5.3.6 VAE/EVA

- 5.3.7 Other Resins

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 Dow

- 6.4.4 DUNLOP ADHESIVES (THAILAND) CO., LTD.

- 6.4.5 H.B. Fuller Company

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 Huntsman International LLC

- 6.4.8 Selic Corp Public Company Limited.

- 6.4.9 Sika AG

- 6.4.10 Star Bond (Thailand) Company Limited

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms