|

市場調査レポート

商品コード

1692584

北米の自動車用接着剤とシーラント:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)North America Automotive Adhesives & Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の自動車用接着剤とシーラント:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 189 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

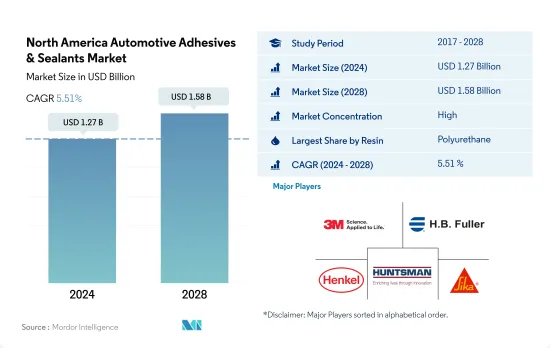

北米の自動車用接着剤とシーラント市場規模は2024年に12億7,000万米ドルと推定・予測され、2028年には15億8,000万米ドルに達し、予測期間(2024-2028年)のCAGRは5.51%で成長すると予測されます。

自動車産業における持続可能性の採用が市場成長の追い風に

- 北米の自動車用接着剤とシーラント市場では、ポリウレタン樹脂が最大のシェアを占めています。北米におけるポリウレタン接着剤の使用量は、他の樹脂よりも高いです。この要因の主な理由は、この地域に生産設備が多く含まれていることです。2017年から2019年にかけて、消費成長率は着実に減少し、約-3%を記録したが、これは自動車生産の減少によるものです。パンデミック後、消費は3%の成長につながります。ポリウレタン接着剤は、2022年から2028年にかけてCAGR 3.1%を記録しています。

- 一方、エポキシ接着剤とアクリル接着剤も自動車用接着剤市場で大きな存在感を示しています。しかし、エポキシ接着剤を製造するために使用される原材料は本質的に有害であり、したがって、米国政府によって規制されているため、エポキシについては、来年は大きな課題となる可能性があります。エポキシ接着剤は、2022年から2028年までのCAGRが約3.14%で、2番目に大きな消費材料です。エポキシ接着剤に続くのはアクリル接着剤で、2022~2028年のCAGRは約3.01%です。

- シアノアクリレートやシリコーンシーラントなどの接着剤は、活況を呈しています。自動車産業における持続可能性の採用は広く拡大しており、EVの生産は大幅に増加しています。このため、電子部品の組み立てにこれらの接着剤の使用が増加しており、その結果、今後数年間で需要が増加する可能性があります。シアノアクリレート系およびシリコーン系接着剤は、予測期間(2022~2028年)に数量ベースで2.5%を超えるCAGRを記録しました。

溶接の代わりに接着する」動向の高まりが自動車用接着剤の需要に大きく貢献

- 北米の自動車用接着剤とシーラント市場は、同国の巨大な自動車生産能力により米国が支配的です。米国は2021年の自動車生産台数が917万台で世界第2位であるのに対し、メキシコは310万台、カナダは110万台です。

- 溶接の代わりに接着する」という動向の高まりが、この地域における自動車用接着剤とシーラントの需要創出に大きく貢献しています。自動車メーカーは、燃料を節約しCO2排出量を削減するために、自動車を軽量化するための技術革新を常に行っているため、プラスチックルーフ、バンパー、または衝突に関連する部品に接着剤を使用し、接合することが、ネジ、リベット、溶接などの従来の接合方法に代わる効果的な方法となりました。

- ポリウレタンをベースとする接着剤とシーラントは、広い使用温度範囲、熱硬化と湿気硬化、塗装性などの柔軟性により、北米地域の自動車産業で最も一般的に使用され、2021年には26.3%のシェアを占める。エポキシ接着剤とシーラントは、他の樹脂タイプの中で2番目に多く使用されており、2021年には21.5%のシェアを占めています。

- 2028年には、北米地域におけるアクリル系接着剤のシェアは2021年の16%から20%に拡大すると予想されます。これは、プラスチックや複合材料と結合して自動車の重量を軽くする能力があり、バッテリーの組み立て作業にも適用できるためです。

北米の自動車用接着剤とシーラント市場の動向

自動車生産を支える電気自動車に対する政府の取り組み

- 北米の自動車産業は、その経済の3%以上を生み出すのに役立っている著名なセクターの一つです。3カ国の中では米国が最大の自動車生産国で65%以上のシェアを占め、メキシコが23%、カナダが8%で続きます。

- 同地域の自動車販売台数は全体の生産台数を大きく減少させており、そのために接着剤の利用が影響を受けています。2017-18年と2018-19年の変動幅は-0.2%から-3.7%でした。さらに2019-20年には、COVID-19パンデミックのため、地域の生産に大きな影響が出ています。製造施設の操業停止やサプライチェーンの混乱による自動車部品の不足は、生産水準を制約する傾向にあります。変動という点では、この地域は約20%の減少を記録しています。しかし、2021年には自動車需要が高まるため、逆にこの地域全体で接着剤の利用が増加する可能性があります。

- 北米のEV市場も接着剤の成長機会です。EVとハイブリッド車の生産と採用の増加は、車両の電子部品アセンブリのための接着剤の使用量を高める傾向があります。米国は、地域全体だけでなく、世界のEVの最大の生産者の一つです。米国連邦政府の目標は、2030年までに乗用車と小型トラックの新車販売台数の50%をEVが占めるようにすることです。同時に、多くの州がより積極的な目標を発表しています。これらの要因は接着剤の需要を増加させる傾向にあり、予測期間中のより良い成長をもたらすと思われます。

北米の自動車用接着剤とシーラント産業の概要

北米の自動車用接着剤とシーラント市場はかなり統合されており、上位5社で66.62%を占めています。この市場の主要企業は以下の通りです。 3M, H.B. Fuller Company, Henkel AG & Co. KGaA, Huntsman International LLC and Sika AG(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 自動車

- 規制の枠組み

- カナダ

- メキシコ

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 樹脂

- アクリル

- シアノアクリレート

- エポキシ

- ポリウレタン

- シリコーン

- VAE・EVA

- その他の樹脂

- テクノロジー

- ホットメルト

- 反応性

- シーラント

- 溶剤系

- UV硬化型接着剤

- 水性

- 国名

- カナダ

- メキシコ

- 米国

- その他北米地域

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- 3M

- Arkema Group

- AVERY DENNISON CORPORATION

- Dow

- DuPont

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Illinois Tool Works Inc.

- Sika AG

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の接着剤とシーラント産業の概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、阻害要因、機会

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The North America Automotive Adhesives & Sealants Market size is estimated at 1.27 billion USD in 2024, and is expected to reach 1.58 billion USD by 2028, growing at a CAGR of 5.51% during the forecast period (2024-2028).

Adoption of sustainability in the automotive industry to create upswings for the market growth

- In the North American automotive adhesives and sealants market, polyurethane resins cover the largest share. The usage of polyurethane adhesive in North America is higher than other resins. The main reason behind this factor is that the region includes production facilities to a large extent. From 2017 to 2019, the consumption growth rate reduced steadily and recorded about -3%, and this is due to the reduction in automotive production. After the pandemic, consumption leads to a growth of 3%. Polyurethane adhesives are registering a CAGR of 3.1% between 2022 to 2028.

- On the other hand, epoxy and acrylic adhesives also show their great presence in the automotive adhesives market. However, for epoxy, the upcoming year could be a great challenge as the raw materials used to produce epoxy adhesives are hazardous in nature and, thus, are getting regulated by the US government. Epoxy adhesive is the second largest consumed material, with a CAGR of about 3.14% from 2022 to 2028. Epoxy adhesives are followed by acrylic adhesives, which register a CAGR of about 3.01% between 2022 to 2028.

- Adhesives, such as cyanoacrylate and silicone sealants, are on a booming trend. The adoption of sustainability in the automotive industry is getting increased widely, and EV production is increasing to a large extent. Owing to this, the usage of these adhesives for electronic component assembly is increasing, which, as a result, may lead to increased demand in the coming years. Cyanoacrylate and silicone adhesives recorded a CAGR of above 2.5% in terms of volume during the forecast period (2022-2028).

Growing trend of 'bonding instead of welding' to significantly contribute to the demand for automotive adhesives

- The North American automotive adhesives and sealants market is dominated by the United States due to the huge automotive production capacity of the country. The United States ranks 2nd globally in automotive production, with 9.17 million produced in 2021, whereas Mexico produced 3.1 million units and Canada produced 1.1 million units.

- The growing trend of 'bonding instead of welding' has significantly contributed to the demand generated for automotive adhesives and sealants in the region. As automakers are always innovating to make vehicles lighter to save fuel and reduce CO2 emissions, usage of adhesives for plastic roofs, bumpers, or crash-relevant parts - bonded joints became an effective alternative to traditional joining procedures, such as screws, rivets, or welding.

- Polyurethane-based adhesives and sealants are most commonly used in the automotive industry in the North American region occupying a share of 26.3% in 2021 due to their flexibility, like wide operating temperature range, heat cured and moisture cured, and paintability. Epoxy adhesives and sealants are the second most commonly used among other resin types, with a share of 21.5% in 2021 because of the stronger metal-to-metal bonding property.

- In 2028, the share of acrylic adhesives in the North American region is expected to grow up to 20% from 16% in 2021 due to their ability to bind to plastic and composite materials to lighten the weight of vehicles and applicability in battery assembly operations.

North America Automotive Adhesives & Sealants Market Trends

Government initiatives for electric vehicles to support the automotive production

- North American automotive is one of the prominent sectors which helps to generate above 3% of its economy. Among all the 3 countries, the United States is the largest automotive producer, covering more than 65% of shares, followed by Mexico with 23% of shares and Canada with 8% of shares.

- Vehicle sales in the region have majorly declined its overall production, owing to which the utilization of adhesives is impacted. In 2017-18 and 2018-19, the variation change has been recorded from -0.2% to -3.7%. Moreover, in 2019-20, due to the COVID-19 pandemic, regional production has been largely impacted. The shutdown of manufacturing facilities and the shortage of vehicle components due to disruption in the supply chain tend to constrain the production level. In terms of variation, the region has recorded about a 20% decline. However, in 2021, the demand for automotive is rising, which, on the other hand, may increase the utilization of adhesives across the region.

- The EV market in North America is another opportunity for adhesives to grow. The rising production and adoption of EVs and Hybrid vehicles tend to raise the usage of adhesives for electronic component assembly in the vehicles. The United States is one of the largest producers of EVs globally as well as across the region. The federal government's goal in the United States is for EVs to account for 50% of new passenger vehicles and light truck sales by 2030. Simultaneously, a number of particular states have announced more aggressive targets. These factors tend to increase the demand for adhesives and will result in better growth in the forecast period.

North America Automotive Adhesives & Sealants Industry Overview

The North America Automotive Adhesives & Sealants Market is fairly consolidated, with the top five companies occupying 66.62%. The major players in this market are 3M, H.B. Fuller Company, Henkel AG & Co. KGaA, Huntsman International LLC and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Automotive

- 4.2 Regulatory Framework

- 4.2.1 Canada

- 4.2.2 Mexico

- 4.2.3 United States

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Sealants

- 5.2.4 Solvent-borne

- 5.2.5 UV Cured Adhesives

- 5.2.6 Water-borne

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 AVERY DENNISON CORPORATION

- 6.4.4 Dow

- 6.4.5 DuPont

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 Huntsman International LLC

- 6.4.9 Illinois Tool Works Inc.

- 6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms