|

市場調査レポート

商品コード

1692583

欧州の自動車用接着剤・シーラント:市場シェア分析、産業動向、成長予測(2025~2030年)Europe Automotive Adhesives & Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の自動車用接着剤・シーラント:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 197 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

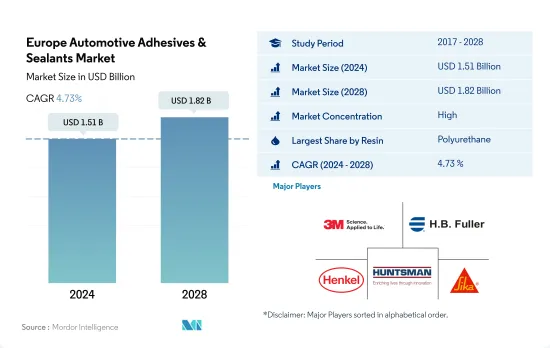

欧州の自動車用接着剤・シーラント市場規模は2024年に15億1,000万米ドルと推定・予測され、2028年には18億2,000万米ドルに達し、予測期間(2024~2028年)のCAGRは4.73%で成長すると予測されます。

自動車メーカーによる自動車の電動化へのシフトが市場成長を促進

- 欧州の自動車用接着剤・シーラント市場では、ポリウレタン樹脂、エポキシ樹脂、アクリル樹脂が大きなシェアを占めています。ポリウレタン樹脂のシェアが高いのは、自動車産業で小型商用車、自動車、電気自動車の高反発フォームシート、硬質フォーム断熱パネル、Bピラー、ヘッドライナー、サスペンションインシュレーター、バンパー、その他の内装部品の製造に最も一般的に使用されているからです。

- 欧州では、ドイツ、ロシア、ポーランド、フランス、英国、ベルギー、イタリアなどの国々でエポキシ樹脂の使用が増加しています。これらの国々では、自動車生産能力とともに、自動車部品における軽量樹脂の使用が増加しています。2021年の小型商用車の生産台数は210万台に増加し、2020年比で1%増加しました。そのため、アクリル、シリコーン、その他の樹脂ベースの接着剤とシーラントの使用量がこの地域で増加しました。

- 同地域の政府が実施する厳しい排ガス規制と、自動車メーカーによる自動車の電動化へのシフトが、予測期間中の欧州自動車用接着剤市場の成長を押し上げると予想されます。市場は、従来の金属溶接よりも自動車用接着剤が提供する利点により、大きな成長が見込まれています。自動車用接着剤はまた、自動車の騒音、過酷さ、振動を低減し、快適な運転を記載しています。したがって、このような要因により、市場は予測期間(2022-028)中に4.57%のCAGRで推移すると推定されます。

CO2排出量削減のための政府規制が電気自動車製造を後押しし、市場需要を押し上げる

- 2018年と2019年の欧州の自動車用接着剤・シーラント需要は、世界の自動車規格の変更と西欧での需要減退、国際貿易摩擦により若干減少しました。2020年、欧州の自動車用接着剤・シーラント需要は、COVID-19パンデミックによる操業とサプライチェーンの制限により、自動車生産台数が2019年の2,156万台から2020年には1,690万台に減少し、20%減少します。

- ドイツは、同国の統合されたバリューチェーンと研究開発インフラに支えられた大規模な製造能力により、欧州諸国の中で自動車用接着剤・シーラントの需要で最大のシェアを占めています。2021年にドイツが製造した自動車は330万台で、欧州で製造される自動車全体の20%を占めています。

- ポリウレタンとエポキシベースの接着剤とシーラントは、自動車の耐荷重性を高める構造用接着剤として使用できるため、この地域で最も一般的に使用されています。また、電気絶縁性とともに耐熱性や耐薬品性も備えているため、PCB(プリント基板)用途にも最適です。2021年には8,500万キログラムのポリウレタン系製品が消費され、2028年にはCAGR 3.16%で1億560万キログラムに達すると予想されています。

- 2030年までに温室効果ガスの排出量を少なくとも55%削減するという欧州委員会の気候変動目標の一環として、「Fit for 55」という法律が制定されました。Fit for 55 "法では、2030年までに自動車のCO2排出量を55%、バンのCO2排出量を50%削減する目標を設定しています。この規制は電気自動車の需要を押し上げ、自動車用電子機器にも使用できるPU、アクリル、シリコーン系製品の需要を予測期間中に押し上げると予想されます。

欧州の自動車用接着剤・シーラント市場動向

電気自動車普及に向けた政府の支援策が産業規模を拡大

- 欧州の一人当たりGDPは3万4,230米ドルで、2022年の成長率は前年比1.6%です。自動車産業部門がGDP全体に占める割合は約2%です。2021年の欧州の自動車生産台数は、乗用車81%、商用車17%、その他2%です。

- 2020年には、ドイツ、イタリア、スペイン、ロシア、英国など多くの欧州諸国がCOVID-19パンデミックの影響を受けました。パンデミックはサプライチェーンの混乱、各国での操業停止、チップ不足をもたらし、欧州の自動車生産に影響を与えました。自動車の生産台数は2019年比で22%も激減しました。

- 米国は欧州から25.3%相当の自動車を輸入しており、2021年にはドイツが10.3%、英国が4.7%を占める主要輸入国のひとつとなりました。2022年初頭、ロシアによるウクライナ侵攻により新車販売が20.5%減少し、それが自動車生産にも反映されました。2022年第1四半期の欧州自動車市場は、前年同期比で10.6%減少しました。

- 自動車生産台数は、多くの欧州諸国が電気自動車に新たな投資を行っているため、期間中(2022~2027年)にCAGR 2.25%で成長する可能性が高いです。例えば、スペインは電気自動車生産に51億米ドルを投資する予定です。

欧州の自動車用接着剤・シーラント産業概要

欧州の自動車用接着剤・シーラント市場はかなり統合されており、上位5社で66.71%を占めています。この市場の主要企業は、3M、H.B. Fuller Company、Henkel AG & Co. KGaA、Huntsman International LLC、Sika AGなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 自動車

- 規制の枠組み

- EU

- ロシア

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 樹脂

- アクリル

- シアノアクリレート

- エポキシ

- ポリウレタン

- シリコーン

- VAE・EVA

- その他

- 技術

- ホットメルト

- 反応性

- シーラント

- 溶剤系

- UV硬化型接着剤

- 水性

- 国名

- フランス

- ドイツ

- イタリア

- ロシア

- スペイン

- 英国

- その他の欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- 3M

- Arkema Group

- AVERY DENNISON CORPORATION

- DELO Industrie Klebstoffe GmbH & Co. KGaA

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Illinois Tool Works Inc.

- Sika AG

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界の接着剤・シーラント産業概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、抑制要因、機会

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92420

The Europe Automotive Adhesives & Sealants Market size is estimated at 1.51 billion USD in 2024, and is expected to reach 1.82 billion USD by 2028, growing at a CAGR of 4.73% during the forecast period (2024-2028).

Increasing shift toward vehicle electrification by automobile players to propel market growth

- Polyurethane, epoxy, and acrylic resins account for a large share of the European automotive adhesives and sealants market. The share of polyurethane resins is higher as they are most commonly used in the automotive industry to manufacture high-resilience foam seating, rigid foam insulation panels, B-pillars, headliners, suspension insulators, bumpers and other interior parts of light commercial vehicles, cars, and electric vehicles.

- In Europe, the usage of epoxy resins is increasing in countries like Germany, Russia, Poland, France, the United Kingdom, Belgium, and Italy. The use of lightweight resins in automotive vehicle parts increased along with automotive vehicle production capacities in these countries. In 2021, the production of light commercial vehicles increased to 2.1 million units, an increase of 1% over 2020. Thus, the usage of acrylic, silicone, and other resin-based adhesives and sealants increased in the region.

- The stringent emission norms implemented by governments in the region and the shift toward vehicle electrification by players are expected to boost the growth of the European automotive adhesives market over the forecast period. The market is expected to witness significant growth owing to the benefits offered by automotive adhesives over traditional metal welding. Automotive adhesives also reduce the noise, harshness, and vibration of the vehicle and provide comfortable driving. Hence, owing to such factors, the market is estimated to register a CAGR of 4.57% during the forecast period (2022-028).

Government legislations to reduce Co2 emissions to boost electric vehicle manufacturing in turn boosting market demand

- Europe's automotive adhesives and sealants demand declined slightly in 2018 and 2019 due to changes in global vehicle standards and demand falls in western Europe and international trade conflicts. In 2020, Europe's automotive adhesives and sealants demand decreased by 20% as vehicle production fell from 21.56 million units in 2019 to 16.9 million units in 2020 due to operational and supply chain restrictions caused by the COVID-19 pandemic.

- Germany has the largest share of the demand for automotive adhesives and sealants among European countries due to its large manufacturing capacity, which is supported by the integrated value chain and R&D infrastructure of the country. In 2021, Germany manufactured 3.3 million units which constitute up to 20% of the total vehicles manufactured in Europe.

- Polyurethane and epoxy-based adhesives and sealants are most commonly used in the region because they can be used as structural adhesives to enhance the load-bearing capacity of the vehicle. They also offer heat and chemical resistance along with electric insulation, which makes them ideal for PCB (Printed Circuit Board) applications. In 2021, 85 million kilograms of polyurethane-based products were consumed, and by 2028 this is expected to reach 105.6 million kilograms with a CAGR of 3.16%.

- As part of the European commission's climate goals to reduce greenhouse house emissions by at least 55% by 2030. The legislation 'Fit for 55' sets targets to reduce CO2 emissions from cars by 55% and vans by 50% by 2030. This regulation has boosted the demand for electric vehicles, which in turn is expected to boost the demand for PU, acrylic, and silicone-based products in the forecast period, as they can also be used in automotive electronics.

Europe Automotive Adhesives & Sealants Market Trends

Supportive government initiatives to promote electric vehicles will raise the industry size

- Europe has a GDP of 34,230 USD per capita with a growth rate of 1.6% y-o-y in 2022. The automotive industry sector contributes a percentage of around 2% of the total GDP. The European vehicle production comprises 81% passenger vehicles, 17% commercial vehicles, and 2% other vehicles in 2021.

- In 2020, many European countries were affected by the COVID-19 pandemic, including Germany, Italy, Spain, Russia, and the United Kingdom. The pandemic resulted in supply chain disruptions, lockdowns in the countries, and chip shortages which affected automotive production in Europe. The production of vehicles sharply declined by 22% compared to 2019.

- The United States imports 25.3% worth of cars from Europe and became one of the leading importers of the United States, where Germany accounted for 10.3% and the United Kingdom for 4.7% of total imports of vehicles in the country in 2021. At the beginning of 2022, the sale of the new vehicle dropped by 20.5% due to the invasion of Ukraine by Russia, which reflected in vehicle production as well. In the first quarter of 2022, the European automotive market was down by 10.6% compared to the same period last year.

- Vehicle production is likely to grow with a CAGR of 2.25% during the period (2022 to 2027) due to the new investments being made in electric vehicles by many European countries. For instance, Spain is going to invest USD 5.1 billion in electric vehicle production.

Europe Automotive Adhesives & Sealants Industry Overview

The Europe Automotive Adhesives & Sealants Market is fairly consolidated, with the top five companies occupying 66.71%. The major players in this market are 3M, H.B. Fuller Company, Henkel AG & Co. KGaA, Huntsman International LLC and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Automotive

- 4.2 Regulatory Framework

- 4.2.1 EU

- 4.2.2 Russia

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Sealants

- 5.2.4 Solvent-borne

- 5.2.5 UV Cured Adhesives

- 5.2.6 Water-borne

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Russia

- 5.3.5 Spain

- 5.3.6 United Kingdom

- 5.3.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 AVERY DENNISON CORPORATION

- 6.4.4 DELO Industrie Klebstoffe GmbH & Co. KGaA

- 6.4.5 Dow

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 Huntsman International LLC

- 6.4.9 Illinois Tool Works Inc.

- 6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms