豚肉加工品-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Processed Pork Meat - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 340 Pages

- 納期

- 2~3営業日

- 商品コード

- 1692570

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

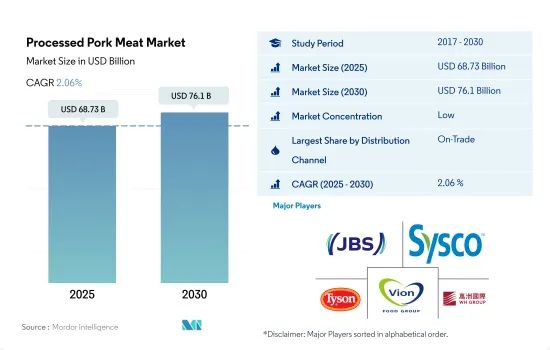

豚肉加工肉の市場規模は2025年に687億3,000万米ドルと推定・予測され、2030年には761億米ドルに達し、予測期間中(2025~2030年)のCAGRは2.06%で成長すると予測されます。

製品の革新とスーパーマーケットを通じた拡大が市場成長を後押ししている

- 豚肉加工食品の販売は、主にオンチャネルを通じて行われます。2020~2022年にかけて、金額ベースで8.16%の成長を記録しました。豚肉は外食産業で特に人気があり、ベーコンバーガーやファストフードの朝食に使われています。レストランでは、豚バラ、豚肩ロース、プルドポーク、より良いチョップカットを使った料理も増えています。豚肉に対する外国からの需要も、特にメキシコ、中国、米国、日本などの市場で増加しています。これらの地域では豚肉産業が確立しており、ソーセージ、ハム、ベーコンなどの豚肉加工品を大量に消費しています。

- オフトレードは豚肉加工品市場で最も急成長しているチャネルであり、予測期間中にCAGR値2.49%を記録すると予測されています。JBS SA、Tyson Foods、Conagra Brands Incorporated、WH Group Limited、Hormel Foods Corporationなどの主要企業は、製品のイノベーションとスーパーマーケットやオンラインストアなど様々な小売チャネルを通じた拡大に注力しています。労働人口の増加は消費者の食習慣と消費パターンを変えつつあり、一方、多忙なライフスタイルは豚肉加工品への需要を高めています。

- オンラインは豚肉加工品市場で最も急成長している流通チャネルです。予測期間中、金額ベースで7.63%の成長が見込まれます。食料品のオンライン購入は世界的に人気が高いです。Walmart、Kroger、Amazon Fresh、Grofersなどの国際的な大手企業は、現在の顧客基盤を拡大することに注力しています。彼らは、オンライン食料品市場の成長を後押しするプロモーション活動に広く従事しています。彼らはまた、調達、認証、加工、製造手順などの具体的な製品情報を提供しています。

アジア太平洋が大きな市場シェアを占める

- 世界の豚肉加工食品の売上は緩やかに伸びています。2022年には世界全体で前年比0.83%増となる人口の増加と、健康志向の高まりによるタンパク質需要の急増が、世界全体の豚肉加工品需要を促進しています。レディトゥイート食品オプションへの需要が、豚肉加工品の販売と消費に貢献しています。豚肉加工品は、持ち運びに便利な食事の選択肢としてコンビニエンスストアの棚に並ぶことが多いです。

- 2022年の豚肉加工品販売では、アジア太平洋が大きな市場シェアを占めています。豚肉加工品の大半は中国で消費されており、2022年には1人当たり年間24.29kgの消費が記録されました。同国はまた、2022年時点で14億3,000万人という世界最大級の人口を有し、世界の豚肉と豚肉加工品消費の50%を占めています。その他のアジア太平洋諸国も、廃棄所得の増加と都市人口の増加により、豚肉消費を伸ばしています。アジア諸国では飼料の入手可能性が高まっているため、新しい養鶏場が誘致され、その養鶏場が豚肉加工産業を誘致しています。

- 欧州は豚肉消費において世界第2位の地域です。同地域の2022年の豚肉生産量は2,210万トンです。ドイツ、ポーランド、スペインがこの地域の主要な豚肉生産国です。欧州の料理は多様性に富み、豚肉を使った伝統的レシピが豊富で、ドイツのブラートヴルスト、フランスのシャルキュトリー、イタリアのプロシュート、スペインのチョリソ、英国のベーコンといった代表的な料理の主要食材となっています。中東地域では豚肉は禁止されています。アラブ首長国連邦とオマーンでは、数少ない公認スーパーマーケットとレストランだけが豚肉の販売を許可されています。

世界の豚肉加工品市場の動向

豚の個体数における様々な感染症の流行が生産に影響

- 世界の豚肉生産量は調査期間中に様々な伸びを示し、2022年には前年比1.55%増となりました。アジア太平洋は最大の豚肉生産地域で、2022年の世界総生産量の51.45%を占めます。アジア太平洋では、中国が最も多くの豚肉を生産しており、i.2021年には5,295万トンで、世界の豚肉総生産量の41.78%以上を占めています。2021年の中国の豚と畜頭数は6億900万頭に達し、2020年の4億6,900万頭から急増しました。同様に、ベトナムは2021年に259万トンの豚肉を生産しました。その他の主要生産国は米国(1,231万トン)、その他のアジア太平洋(696万トン)、ドイツ(520万トン)です。

- 数量は2018~2019年にかけて8.63%減少したが、これは主にASFの影響によるもので、世界の豚肉生産に影響を与えました。ASFは伝染性が高く致死的な豚病で、農場飼育豚や野豚(野生豚)が罹患する可能性があり、死亡率も高い(95~100%)。2019年には中国で約2億2,500万頭の豚が死亡するか、発生により淘汰され、2018~2019年にかけて世界の豚のほぼ25%がASFにより死亡しました。ASFウイルスは約1世紀前に発見されたもの、市販の予防接種や治療法はまだないです。ASFは欧州、アジア、オセアニアでも家畜の死亡につながりました。

- 欧州は世界第2位の豚肉生産地域で、2022年の世界の豚肉生産量の23.05%以上を占めています。その他の欧州は2021年の豚肉生産量が1,011万トンで同地域最大の豚肉生産国であり、スペイン(518万トン)、ドイツ(497万トン)、ロシア(434万トン)、フランス(220万トン)、オランダ(171万トン)がこれに続きます。

投入コストの上昇とインフレが価格高騰を招く

- 2017~2022年にかけて、世界の豚肉価格は8.50%上昇しました。食品の値ごろ感と安全性に対する懸念、COVID-19パンデミック後の不安定な豚肉価格の上昇が、豚肉小売価格上昇の主要因です。2020~2022年にかけてのトウモロコシ価格の79%高騰と大豆粕価格の42%上昇に伴う飼料コストの大幅上昇が、燃料費、輸送費、包装費、小売コストの上昇とともに、コスト増の要因となっています。こうした限界コストの多くは、農場、卸売、小売の豚肉価格の変動につながります。

- 米国の豚肉小売価格は2021年後半に上昇し、2022年まで高止まりしました。労働局の消費者物価指数によると、豚肉価格は前年同期比15%上昇し、米国のインフレ率の2倍に達しました。これは過去20年間で大幅な上昇です。平均すると、豚肉価格は毎年2%上昇し、牛肉価格は18.6%、鶏肉価格は10.4%上昇しました。2022年の米国における各種豚肉製品の価格は、ベーコンが6,224米ドル/ポンド、ポークチョップが4.24米ドル/ポンド、ハムが4.44米ドル/ポンドでした。ウクライナ紛争や物流関連の問題による生産、輸送、エネルギー、飼料のコスト上昇により、豚肉価格は今後も上昇する可能性があります。また、豚の頭数の流動化や家畜の供給量の少なさも、欧州での採算割れにつながっています。したがって、豚の供給が少ないことは、予測期間中、同地域での買い取り価格の上昇に有利に働く可能性があります。2023年第1四半期の豚肉生産量は、2022年第1四半期と比較して、英国では前年同期比11%減、EUでは同8%減となりました。その結果、価格は高止まりしており、年初から英国と欧州の両市場で大幅な上昇が見られました。

豚肉加工品産業概要

豚肉加工品市場は細分化されており、上位5社で19.47%を占めています。この市場の主要企業は、 JBS SA、Sysco Corporation、Tyson Foods Inc.、Vion Group、WH Group Limitedなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- 価格動向

- 豚肉

- 生産動向

- 豚肉

- 規制の枠組み

- カナダ

- フランス

- ドイツ

- イタリア

- メキシコ

- 英国

- 米国

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- 流通チャネル

- オフトレード

- コンビニエンスストア

- オンラインチャネル

- スーパーマーケットとハイパーマーケット

- その他

- オントレード

- オフトレード

- 地域

- アフリカ

- 流通チャネル別

- 国別

- エジプト

- ナイジェリア

- 南アフリカ

- その他のアフリカ

- アジア太平洋

- 流通チャネル別

- 国別

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- 韓国

- その他のアジア太平洋

- 欧州

- 流通チャネル別

- 国別

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- 英国

- その他の欧州

- 中東

- 流通チャネル別

- 国別

- その他の中東

- 北米

- 流通チャネル別

- 国別

- カナダ

- メキシコ

- 米国

- その他の北米

- 南米

- 流通チャネル別

- 国別

- アルゼンチン

- ブラジル

- その他の南米地域

- アフリカ

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- COFCO Corporation

- Danish Crown AmbA

- Hormel Foods Corporation

- JBS SA

- Muyuan Foods Co., Ltd.

- Seaboard Corporation

- Sysco Corporation

- The Clemens Family Corporation

- Tyson Foods Inc.

- Tonnies Holding ApS & Co. KG

- Vion Group

- WH Group Limited

第6章 CEOへの主要戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92397

The Processed Pork Meat Market size is estimated at 68.73 billion USD in 2025, and is expected to reach 76.1 billion USD by 2030, growing at a CAGR of 2.06% during the forecast period (2025-2030).

Product innovation and expansion through supermarkets are propelling the market growth

- Sales of processed pork meat are primarily made through the on-trade channel, which is the primary market segment. It registered a growth of 8.16% by value from 2020 to 2022. Pork is particularly popular in the foodservice sector, used in bacon burgers and fast-food breakfasts. Restaurants are also introducing more dishes featuring pork belly, pork shoulder, pulled pork, and better chop cuts. Foreign demand for pork is also increasing, especially in markets such as Mexico, China, the United States, and Japan. These regions have well-established pork industries and consume a substantial amount of processed pork products like sausages, ham, and bacon.

- Off-trade is the fastest-growing channel in the processed pork market, which is projected to record a CAGR value of 2.49% during the forecast period. Key players such as JBS SA, Tyson Foods, Conagra Brands Incorporated, WH Group Limited, and Hormel Foods Corporation focus on product innovation and expansion through various retail channels, such as supermarkets and online stores. The growing working population is changing consumer food habits and spending patterns, whereas busy lifestyles are increasing the demand for processed pork.

- Online is the fastest-growing distribution channel in the processed pork market. It is projected to register a growth of 7.63% by value during the forecast period. Online grocery purchasing is highly sought after worldwide. The major international companies, including Walmart, Kroger, Amazon Fresh, and Grofers, focus on growing their current customer bases. They are extensively engaging in promotional efforts, boosting the growth of the online grocery market. They also provide specific product information, such as sourcing, certifications, processing, and manufacturing procedures.

Asia-Pacific region occupies a significant market share

- The sales of processed pork meat worldwide are growing moderately. The increase in the population, growing at 0.83% across the world in 2022 compared to the previous year, and the spike in protein demand due to increased health consciousness are fueling processed pork demand across the world. The demand for ready-to-eat food options has contributed to the sales and consumption of processed pork. Processed pork products are often found on convenience store shelves as convenient, on-the-go meal options.

- The Asia-Pacific region occupied a significant market share of processed pork sales in 2022. Most processed pork is consumed in China, with the highest per capita consumption of 24.29 kg per annum recorded in 2022. The country also has one of the world's largest populations, at 1.43 billion as of 2022, accounting for 50% of pork and processed pork meat consumption in the world. The rest of the countries in the Asia-Pacific are also increasing pork consumption due to higher disposal incomes and the increasing urban population. An increase in feed availability in Asian countries is attracting new poultry farms, which are, in turn, attracting pork processing industries.

- Europe is the second-leading region in the consumption of pork globally. The region produced 22.1 million tons of pork in 2022. Germany, Poland, and Spain are the major pork-producing countries in the region. European cuisines are diverse and rich in pork-based traditional recipes and are key ingredients in iconic dishes like German bratwurst, French charcuterie, Italian prosciutto, Spanish chorizo, and British bacon. Pork is prohibited in the Middle East region. Only a few authorized supermarkets and restaurants in the UAE and Oman are licensed to sell pork in the region.

Global Processed Pork Meat Market Trends

The prevalence of a variety of infectious diseases in the pig population affects production

- Global pork production saw varied growth during the study period, which grew by 1.55% in 2022 compared to the previous year. Asia-Pacific is the largest pork-producing region, representing 51.45% of the total global production volume in 2022. In Asia-Pacific, China produced the most pork, i.e., 52.95 million tons in 2021, accounting for over 41.78% of the total global pork production. In 2021, China's pig slaughter volume reached 609 million heads, a steep rise from the slaughter volume in 2020, which was only 469 million heads. Similarly, Vietnam produced 2.59 million tons of pork in 2021. Other leading producers are the United States (12.31 million tons), the Rest of Asia-Pacific (6.96 million tons), and Germany (5.20 million tons).

- The volume declined by 8.63% from 2018 to 2019, primarily due to the effects of ASF, which impacted global pork production. ASF is a highly contagious and deadly swine disease that can affect farm-raised and feral (wild) pigs and has high mortality rates (95-100%). In 2019, about 225 million pigs in China either died or were culled due to the outbreak, and almost 25% of the global pig population died from ASF during 2018-2019. Although the ASF virus was discovered about a century ago, no commercial vaccinations or treatments are still available. ASF also led to livestock deaths in Europe, Asia, and Oceania.

- Europe is the second-largest pork-producing region globally, contributing over 23.05% of the total global pork production in 2022. The rest of Europe was the largest pork producer in the region in 2021, with a pork volume of 10.11 million tons, followed by Spain (5.18 million tons), Germany (4.97 million tons), Russia (4.34 million tons), France (2.20 million tons), and the Netherlands (1.71 million tons).

Rising input costs and inflation are leading to a spike in prices

- From 2017 to 2022, global pork prices grew by 8.50%. Concerns about food affordability and safety, as well as volatile and rising post-COVID-19 pandemic pork prices, are the main drivers behind the rise in retail pork prices. Significantly higher feed costs, accompanied by a 79% surge in corn prices and a 42% increase in soybean meal prices from 2020 to 2022, along with increasing fuel, transportation, packing, and retail costs, have contributed to incremental cost rises. Many of these marginal costs result in changes in farm, wholesale, and retail pork prices.

- In US retail, pork prices increased in the second half of 2021 and remained elevated until 2022. The Bureau of Labor's consumer price index showed pork prices rising 15% Y-o-Y, twice the rate of US inflation. This has been a significant leap in the last 20 years. On average, pork prices rose by 2% annually, while beef prices rose by 18.6% and chicken prices rose by 10.4%. Prices of various pork products in the United States in 2022 were USD 6,224/lb for bacon, USD 4.24/lb for pork chops, and USD 4.44/lb for ham. The hog prices may continue to grow due to the rising costs of production, transport, energy, and feed caused by the conflict in Ukraine and logistics-related issues. The liquidation of the swine population and the low supply of livestock are also leading to a lack of profitability in Europe. Therefore, a low supply of pigs may favor the higher purchase prices in the region during the forecast period. In Q1 2023, pig meat production witnessed an 11% Y-o-Y decline in the United Kingdom and an 8% drop in EU production compared to Q1 2022. Consequently, prices have remained elevated, with substantial increases observed in both the UK and European markets since the start of the year.

Processed Pork Meat Industry Overview

The Processed Pork Meat Market is fragmented, with the top five companies occupying 19.47%. The major players in this market are JBS SA, Sysco Corporation, Tyson Foods Inc., Vion Group and WH Group Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Price Trends

- 3.1.1 Pork

- 3.2 Production Trends

- 3.2.1 Pork

- 3.3 Regulatory Framework

- 3.3.1 Canada

- 3.3.2 France

- 3.3.3 Germany

- 3.3.4 Italy

- 3.3.5 Mexico

- 3.3.6 United Kingdom

- 3.3.7 United States

- 3.4 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Distribution Channel

- 4.1.1 Off-Trade

- 4.1.1.1 Convenience Stores

- 4.1.1.2 Online Channel

- 4.1.1.3 Supermarkets and Hypermarkets

- 4.1.1.4 Others

- 4.1.2 On-Trade

- 4.1.1 Off-Trade

- 4.2 Region

- 4.2.1 Africa

- 4.2.1.1 By Distribution Channel

- 4.2.1.2 By Country

- 4.2.1.2.1 Egypt

- 4.2.1.2.2 Nigeria

- 4.2.1.2.3 South Africa

- 4.2.1.2.4 Rest of Africa

- 4.2.2 Asia-Pacific

- 4.2.2.1 By Distribution Channel

- 4.2.2.2 By Country

- 4.2.2.2.1 Australia

- 4.2.2.2.2 China

- 4.2.2.2.3 India

- 4.2.2.2.4 Indonesia

- 4.2.2.2.5 Japan

- 4.2.2.2.6 Malaysia

- 4.2.2.2.7 South Korea

- 4.2.2.2.8 Rest of Asia-Pacific

- 4.2.3 Europe

- 4.2.3.1 By Distribution Channel

- 4.2.3.2 By Country

- 4.2.3.2.1 France

- 4.2.3.2.2 Germany

- 4.2.3.2.3 Italy

- 4.2.3.2.4 Netherlands

- 4.2.3.2.5 Russia

- 4.2.3.2.6 Spain

- 4.2.3.2.7 United Kingdom

- 4.2.3.2.8 Rest of Europe

- 4.2.4 Middle East

- 4.2.4.1 By Distribution Channel

- 4.2.4.2 By Country

- 4.2.4.2.1 Rest of Middle East

- 4.2.5 North America

- 4.2.5.1 By Distribution Channel

- 4.2.5.2 By Country

- 4.2.5.2.1 Canada

- 4.2.5.2.2 Mexico

- 4.2.5.2.3 United States

- 4.2.5.2.4 Rest of North America

- 4.2.6 South America

- 4.2.6.1 By Distribution Channel

- 4.2.6.2 By Country

- 4.2.6.2.1 Argentina

- 4.2.6.2.2 Brazil

- 4.2.6.2.3 Rest of South America

- 4.2.1 Africa

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 5.4.1 COFCO Corporation

- 5.4.2 Danish Crown AmbA

- 5.4.3 Hormel Foods Corporation

- 5.4.4 JBS SA

- 5.4.5 Muyuan Foods Co., Ltd.

- 5.4.6 Seaboard Corporation

- 5.4.7 Sysco Corporation

- 5.4.8 The Clemens Family Corporation

- 5.4.9 Tyson Foods Inc.

- 5.4.10 Tonnies Holding ApS & Co. KG

- 5.4.11 Vion Group

- 5.4.12 WH Group Limited

6 KEY STRATEGIC QUESTIONS FOR MEAT INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

豚肉加工品-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 340 Pages

- 納期

- 2~3営業日