北米の豚肉加工食品:市場シェア分析、産業動向、成長予測(2025年~2030年)

North America Processed Pork Meat - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 202 Pages

- 納期

- 2~3営業日

- 商品コード

- 1692072

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

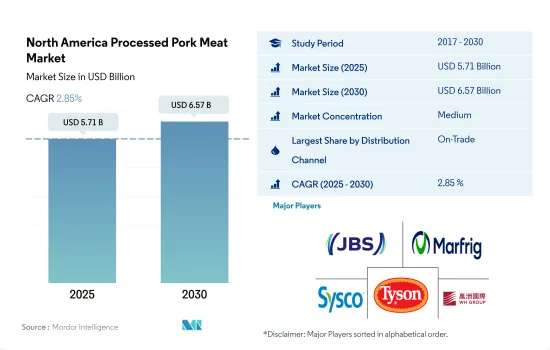

北米の豚肉加工食品市場規模は2025年に57億1,000万米ドルと推定・予測され、2030年には65億7,000万米ドルに達し、予測期間(2025年~2030年)のCAGRは2.85%で成長すると予測されます。

小売チャネルの先端技術が市場の成長を後押ししている

- 北米では2022年に豚肉加工食品のオン・トレード販売が市場を独占しました。豚肉の一人当たり消費量が多いため、豚肉加工肉の外食売上は高水準に再調整されました。2022年には、米国人はレストランなど家庭外での食事に平均で約2,994米ドルを費やしました。家庭外食品のシェアは、前年の46%から2022年には58%に増加します。これは主に、栄養価の高いメニューを求める消費者の意識の高まりと、地元産の肉への関心の高まりによるものと考えられます。

- オフ・トレード・チャネルは、予測期間中にCAGR 3.37%を記録し、最も急成長する流通チャネルになると予測されます。この増加は、スーパーマーケット、ハイパーマーケット、コンビニエンスストア、オンライン小売店で広く入手可能な豚肉加工品に対する需要の高まりに起因しています。スーパーマーケットでは、チェックアウトが無料であることや、より本格的な豚肉加工品がクリーン・ラベルで入手可能であることから、オフ・トレード・チャネル・セグメンテーションを通じた需要全体が増加すると予想されます。

- テクノロジーの進歩も、外食チャネルを通じた販売を促進しています。例えば、2022年現在、約90%のレストランが厨房自動化技術の向上に注力しており、外食の売上を押し上げています。さらに、過去3年間におけるオンライン・デリバリー・チャネルの増加やソーシャルメディアの急速な利用が、この地域における商品の入手可能性の露出を高めています。例えば米国では、オンライン食料品店の顧客は宅配よりもクリック・アンド・コレクトサービスを好みます。2021年には、顧客はオンライン・サイトで肉製品を含む約4.4倍の商品を閲覧し、6倍の支出を行いました。

市場参入企業による事業拡大が商品の入手可能性を高め、売上に拍車をかける

- 北米では豚肉加工品の売上が増加し、予測期間中のCAGRは金額ベースで2.59%を記録しました。各社は豚肉加工品市場の製品拡大に投資しています。例えば、Hormel Foods Corporation、Tyson Foods Inc.、Conagra Brands Incorporatedは製品を革新し、ソーセージ、ベーコン、トルコなど幅広い豚肉加工品をスーパーマーケットやオンラインショップを通じて提供しています。さらに、豚肉製品の加工により、消費者が備蓄するようになったため、製品の保存期間が延び、その結果、2022年時点で1人当たりの消費量が23.68kgに増加し、売上をさらに押し上げています。

- 北米地域では米国が豚肉加工品市場の主要シェアを占めています。2020年から2022年にかけて、豚肉加工品市場は金額ベースで7.3%の成長を記録しました。豚肉に対する旺盛な需要があり、需要の増加は2020年の貿易黒字につながりました。2020年の豚肉輸出は豚肉輸入の7倍で、15%以上増加しました。米国は世界第3位の豚肉生産国です。

- メキシコは北米の豚肉加工品市場で米国に次ぐ第2位のシェアを占めています。メキシコは予測期間中、金額ベースで約3.33%のCAGRで推移すると予想されています。同国の豚肉生産は、国内小売での需要増と中国、日本、韓国への輸出機会により拡大しています。2019年から2022年にかけて、メキシコの豚肉需要は、マクロ経済の不利な状況の深刻化と、後者が安価な動物性タンパク質であることから小売消費者が牛肉から豚肉にシフトしたことにより増加しました。

北米の豚肉加工品市場の動向

疾病の蔓延を防ぐための政府の取り組みが生産を促進する

- 北米の豚肉生産量は米国がトップで、2022年の同地域の豚肉生産量の73%を占めました。アイオワ州は2021年に米国で約2,380万頭の豚を飼養していました。米国では2021年におよそ7,477万頭の豚と豚が生産され、そのうち繁殖用の豚はかなり少なく(618万頭)、6,800万頭が市場豚でした。人気のある豚の品種には、バークシャー、チェスター・ホワイト、デュロック、ハンプシャー、ランドレース、ポーランド・チャイナ、スポッテッド・ピッグなどがあります。米国農務省動植物検疫局(APHIS)は、米国におけるアフリカ豚熱の蔓延を阻止するため、さらなる対策を講じています。Protect Our Pigs(豚を守ろう)」キャンペーンは、米国内の豚の個体数を守るため、商業養豚業者に情報とツールを提供するものです。

- メキシコは豚肉の主要生産国でもあり、この地域の豚肉の10.36%を生産しています。2022年の生産量は前年比2.19%増となったが、これは2022年を通じて豚肉の消費者価格が牛肉や鶏肉に比べて非常に競合しているため、高インフレ時に家計の購買決定に影響を与えるなどの要因によるものです。加えて、ますます多くの豚肉を必要とする豚肉加工品の成長や、輸入カット肉と競合する特殊な国産カット肉の生産が、生産量の増加に寄与しました。

- 豚肉産業はカナダで4番目に大きな農業です。2021年には約7,330の農場で1,417万頭の豚が生産され、ケベック州(31%)、オンタリオ州(26%)、マニトバ州(24%)がカナダの在庫の81%を占めています。2021年にカナダで食肉処理された豚は約2,165万6,185頭。

供給不足につながる生産量の減少が価格高騰につながる

- 2022年の豚肉価格は2017年から8.80%上昇しました。2023年第2四半期には豚肉100重量(cwt)当たり1米ドルから57米ドルまでの価格上昇が見られ、米国の2022年同時期の価格より25%近く低くなりました。6月と7月の価格は通常、平均より8~10%高いです。この季節のピークは、消費者がブラートヴルストやグリル用のポークチョップのような食品を購入しやすい米国の夏を通して発生します。ファーム・クレジット・カナダによれば、東部地域のマージンは、西部地域と比較して価格が軟化し、飼料コストが相対的に高いため、2年目も低下します。西部の分娩からフィニッシュまでのマージンはプラスを維持すると思われます。

- 豚不足とインフレが豚肉価格を記録的高値に押し上げています。しかし、インフレは豚肉価格に追いついていないです。2021年4月から2022年4月にかけて、インフレ率は8.5%上昇したが、豚肉価格は16.1%上昇しました。ベーコンの需要増が小売における豚肉価格上昇の主な要因です。スライスベーコンの平均小売価格は2022年3月に23.1%上昇したが、ボンレスポークチョップとボンレスハムはそれぞれ4.5%と7.5%の上昇にとどまりました。これら最後の2つのカットはインフレ率よりも低い伸び率を記録しました。

- この地域の豚肉価格は、予想を下回る豚肉生産の伸びにより、引き続き上昇する可能性があります。2021年のと殺豚頭数は2020年から1.96%減少しました。小売価格の高止まりは、すべてのタンパク質の消費を制限します。消費者は、日常的な購入をより低価値のタンパク質オプションにシフトしたり、販売チャネルを切り替えたり、より小さなパックサイズに移行したりすることで、所得を節約し続けています。

北米の豚肉加工食品産業の概要

北米の豚肉加工食品市場は適度に統合されており、上位5社で53.16%を占めています。この市場の主要企業は以下の通り。 JBS SA, Marfrig Global Foods S.A., Sysco Corporation, Tyson Foods Inc. and WH Group Limited(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- 価格動向

- 豚肉

- 生産動向

- 豚肉

- 規制の枠組み

- カナダ

- メキシコ

- 米国

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- 流通チャネル

- オフ・トレード

- コンビニエンスストア

- オンライン・チャネル

- スーパーマーケットとハイパーマーケット

- その他

- オン・トレード

- オフ・トレード

- 国名

- カナダ

- メキシコ

- 米国

- その他の北米

第5章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Conagra Brands Inc.

- Hormel Foods Corporation

- Industrias Bachoco SA de CV

- JBS SA

- Maple Leaf Foods

- Marfrig Global Foods S.A.

- OSI Group

- Seaboard Corporation

- Sysco Corporation

- The Kraft Heinz Company

- Tyson Foods Inc.

- WH Group Limited

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The North America Processed Pork Meat Market size is estimated at 5.71 billion USD in 2025, and is expected to reach 6.57 billion USD by 2030, growing at a CAGR of 2.85% during the forecast period (2025-2030).

Advanced technologies in retail channels are propelling the market's growth

- On-trade sales of processed pork meat dominated the market in North America in 2022. Foodservice sales for processed pork meat recalibrated to higher levels due to pork's high per capita consumption. On average, Americans spent around USD 2,994 on food away from home, such as at restaurants, in 2022. The share of food away from home increased to 58% in 2022 compared to 46% compared to the previous year. This could be primarily attributed to the increased awareness among consumers looking for nutritional menus and the growing interest in locally sourced meat.

- The off-trade channel is projected to be the fastest-growing distribution channel, registering a CAGR of 3.37% during the forecast period. This increase can be attributed to the rising demand for processed pork products, which are widely accessible in supermarkets, hypermarkets, convenience stores, and online retailers. Free checkout and the availability of more authentic processed pork meat products with clean labels in supermarkets are expected to increase the overall demand through the off-trade channel segment.

- The advancements in technology are also driving sales through restaurant channels. For instance, as of 2022, around 90% of restaurants were focused on increasing kitchen automation technology, boosting the sales of food away from home. Moreover, the rise in online delivery channels over the past three years and the rapid usage of social media have boosted the exposure of product availability in the region. For instance, in the United States, online grocery customers prefer click-and-collect services over home delivery. In 2021, customers viewed around 4.4 times more products, including meat products, and spent six times more on online sites.

Expansions by the market players increase the availability of products, thus fueling the sales

- Processed pork sales increased in North America, registering a CAGR of 2.59% by value during the forecast period. Companies are investing in product expansions within the processed pork meat market. For instance, Hormel Foods Corporation, Tyson Foods Inc., and Conagra Brands Incorporated are innovating products and offering a wide range of processed pork like sausages, bacon, and turkey through supermarkets and online stores. Furthermore, the processing of pork products has extended the product's shelf life as consumers have adopted a stockpiling nature, which, in turn, increased the per capita consumption to 23.68 kg per capita as of 2022, further boosting the sales.

- The United States holds the major share of the processed pork meat market in the North American region. During 2020-2022, the processed pork meat market registered a growth of 7.3% by value. There was robust demand for pork, and the increase in demand led to a trade surplus in 2020. Pork exports in 2020 were sevenfold higher than pork imports, increasing by more than 15%. The United States is the third-largest pork producer in the world.

- Mexico holds the second-largest share in the North American processed pork meat market after the United States. It is anticipated to register a CAGR of about 3.33% by value during the forecast period. Pork production in the country is growing due to the increased demand in domestic retail and export opportunities to China, Japan, and South Korea. From 2019 to 2022, demand for pork meat in Mexico increased due to the escalation of adverse macroeconomic conditions and the shift of retail consumers from beef to pork since the latter is a cheaper animal protein.

North America Processed Pork Meat Market Trends

Initiatives taken by the government to prevent the spread of diseases will propel the production

- The United States was the top pork producer in North America, with a 73% share in the region's pork production in 2022. Iowa accounted for about 23.8 million pigs in the United States in 2021. The United States produced roughly 74.77 million pigs and hogs in 2021, of which a significantly smaller number of pigs (6.18 million) in the country were used for breeding, and 68 million were market hogs. Some popular swine breeds include Berkshires, Chester Whites, Durocs, Hampshire, Landraces, Poland Chinas, and Spotted Pigs. The USDA's Animal and Plant Health Inspection Service (APHIS) is taking additional measures to stop the spread of African swine fever in the United States. The "Protect Our Pigs" campaign will provide information and tools to commercial pig producers in order to protect the swine population in the United States.

- Mexico is also a major pork producer, producing 10.36% of the region's pork. The production increased by 2.19% in 2022 compared to the previous year, owing to factors such as the highly competitive consumer prices of pork throughout 2022 compared to those of beef and chicken, thus influencing household purchasing decisions during high inflation. In addition, the growth of processed pork, which requires increasingly more pork, and the production of specialized domestic cuts that compete with imported cuts contributed to the growth in production.

- The pork industry is the 4th largest farming industry in Canada. In 2021, the country had around 7,330 farms producing 14.17 million hogs, with Quebec (31%), Ontario (26%), and Manitoba (24%) accounting for 81% of Canada's inventory. Around 21,656,185 hogs were slaughtered in federally and provincially inspected establishments in Canada in 2021.

Lower rate of production leading to supply shortage is leading to price spikes

- The price of pork grew 8.80% in 2022 from 2017. The second quarter of 2023 saw a price hike ranging from USD 1 per hundredweight (cwt) to USD 57 per cwt of pork, which was almost 25% lower than the price at the same time in 2022 in the US. Prices in June and July are typically 8-10% higher than average. This seasonal peak occurs throughout the US summer when consumers are more likely to purchase foods like bratwursts and pork chops for grilling. As per Farm Credit Canada, margins in the eastern region will drop for the second year due to softening prices and relatively higher feed costs compared to the western region. The margins of western farrow-to-finish will stay positive.

- A shortage of pigs and inflation are driving record-high pork prices. However, inflation is not catching up with the price of pork. Between April 2021 and 2022, inflation increased by 8.5%, while pork prices increased by 16.1%. The increased demand for bacon is a major factor responsible for increased pork prices in retail. Sliced bacon's average retail cost increased by 23.1% in March 2022, whereas the prices for boneless pork chops and boneless ham increased by just 4.5% and 7.5%, respectively. These last two cuts recorded growth at a slower rate than inflation.

- Pork prices in the region may continue to rise due to the lower-than-expected growth in pork production. The number of pigs slaughtered in 2021 decreased by 1.96% from 2020. Persistently high retail prices limit the consumption of all proteins. Consumers continue to conserve income by shifting everyday purchases to lower-value protein options, switching channels, and moving to smaller pack sizes.

North America Processed Pork Meat Industry Overview

The North America Processed Pork Meat Market is moderately consolidated, with the top five companies occupying 53.16%. The major players in this market are JBS SA, Marfrig Global Foods S.A., Sysco Corporation, Tyson Foods Inc. and WH Group Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Price Trends

- 3.1.1 Pork

- 3.2 Production Trends

- 3.2.1 Pork

- 3.3 Regulatory Framework

- 3.3.1 Canada

- 3.3.2 Mexico

- 3.3.3 United States

- 3.4 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Distribution Channel

- 4.1.1 Off-Trade

- 4.1.1.1 Convenience Stores

- 4.1.1.2 Online Channel

- 4.1.1.3 Supermarkets and Hypermarkets

- 4.1.1.4 Others

- 4.1.2 On-Trade

- 4.1.1 Off-Trade

- 4.2 Country

- 4.2.1 Canada

- 4.2.2 Mexico

- 4.2.3 United States

- 4.2.4 Rest of North America

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 5.4.1 Conagra Brands Inc.

- 5.4.2 Hormel Foods Corporation

- 5.4.3 Industrias Bachoco SA de CV

- 5.4.4 JBS SA

- 5.4.5 Maple Leaf Foods

- 5.4.6 Marfrig Global Foods S.A.

- 5.4.7 OSI Group

- 5.4.8 Seaboard Corporation

- 5.4.9 Sysco Corporation

- 5.4.10 The Kraft Heinz Company

- 5.4.11 Tyson Foods Inc.

- 5.4.12 WH Group Limited

6 KEY STRATEGIC QUESTIONS FOR MEAT INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 202 Pages

- 納期

- 2~3営業日