ヘルスケア規制関連業務アウトソーシングの世界市場:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Global Healthcare Regulatory Affairs Outsourcing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 115 Pages

- 納期

- 2~3営業日

- 商品コード

- 1692093

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

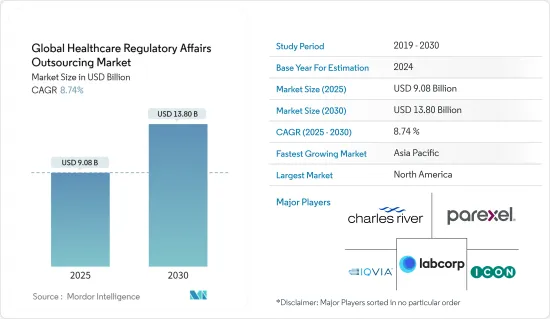

世界のヘルスケア規制関連業務アウトソーシング市場規模は、2025年に90億8,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは8.74%で、2030年には138億米ドルに達すると予測されます。

パンデミックの期間中、COVID-19患者が大量に流入した結果、大量のロックダウンが発生し、がんなどさまざまな慢性疾患の臨床研究が中断されました。パンデミックの中で臨床試験数が減少した結果、ヘルスケア規制関連業務アウトソーシングサービスの需要が減少しました。例えば、2021年12月にFrontiers in Medicine1誌に掲載された研究では、パンデミック中にCOVID-19患者数が増加したため、臨床試験活動が減少したことが強調されています。この情報源はまた、パンデミックの中、COVID-19以外の臨床開発では新薬の申請が減少したとも述べています。

したがって、世界サプライチェーンの混乱は、パンデミックの初期段階における医薬品の製造と流通に影響を与え、市場の成長に大きな影響を与えました。薬事チームは、必要不可欠な医薬品の入手可能性と安全性の確保に関する課題を克服しなければならず、規制の適応が必要となりました。

さらに、研究開発費の増加、臨床試験件数の増加、アウトソーシングの費用対効果が市場成長の原動力になると予想されます。例えば、2022年2月に発表されたGlobal Observatory on Health R&D analysisによると、WHOのほとんどの地域でWHO International Clinical Trials Registry Platform(ICTRP)に登録された新規募集の臨床試験数はコンスタントに増加しています。さらに、WHOの欧州、南北アメリカ、西太平洋地域の登録試験数は、他の地域よりも高い割合で増加しています。例えば、2021年に西太平洋地域で登録された臨床試験数は16,860件で、851件であったアフリカ地域の約20倍でした。このように、臨床試験数の増加により、予測期間中に薬事業務のアウトソーシングが増加すると予想されます。

さらに、製薬企業やバイオテクノロジー企業による研究開発投資の増加が市場成長の原動力になると予想されます。PhRMAの発表によると、PhRMA加盟企業は2021年に約1,023億米ドルを研究開発活動に投資しました。欧州製薬団体連合会(European Federation of Pharmaceutical Industries and Associations)が2022年に発表したデータによると、研究開発ベースの欧州製薬業界は過去数年よりも増加しており、2021年には3,000億ユーロ(3,237億米ドル)に達しました。また同じ情報源は、この産業が2021年に415億ユーロ(447億7,000万米ドル)という多額の研究開発投資を受けたと述べています。

さらに、M&Aなど主要市場プレーヤーによる様々な戦略的活動が市場成長を促進すると予想されています。例えば、2021年7月、Covance社は、患者中心の分散型臨床試験(DCT)の世界的リーダーであるGlobalCare社を買収し、Covance社のDCTサービスを国際市場に拡大し、患者中心の試験デザインに対する需要の高まりに対応します。

このように、上記の要因により、ヘルスケア規制サービス業界における需要が増加し、予測期間中の市場成長が促進されると予想されます。しかし、データセキュリティに関連するリスクと標準化の欠如が、調査対象市場の主な抑制要因となっています。

ヘルスケア規制関連業務アウトソーシング市場動向

予測期間中、製品登録および臨床試験アプリケーション分野が大きな市場シェアを占める見込み

製品登録とは、製品をその国や地域で販売、流通、販売、輸入することを許可するために、その国や地域で適用される当局が承認する規制当局への承認申請を指します。治験薬登録申請書(Clinical Trial Application)治験薬登録申請書(Clinical Trial Application)とは、当該国において臨床試験を実施するための許可を得るために、所轄の国内規制当局に提出する書類をいう。治験申請書には治験薬と計画中の臨床試験に関する詳細な情報が記載され、規制当局は試験の実施可能性を評価することができます。

先進国と新興諸国の両方で臨床試験申請と製品登録のアウトソーシングが増加していることが、予測期間にわたって製品登録と臨床試験申請セグメントを牽引しています。製品登録プロセスの複雑さ、業界の専門家の不足、社内の能力不足のため、ほとんどの製薬会社および医療機器会社は、製品登録業務を第三者のサービスプロバイダーにアウトソーシングしています。さらに、薬事規制の絶え間ない変更と更新も、こうしたサービスのアウトソーシングを後押ししています。例えば、2022年1月31日、欧州医薬品庁はEUにおける臨床試験の規制調和を発表しました。また、新たな臨床試験情報システム(CTIS)を立ち上げました。このことは、予測期間中の同分野の成長を促進すると予想されます。

このように、上記のすべての要因が予測期間中のセグメント成長を促進すると予想されます。

予測期間中、北米が主要市場シェアを占める見込み

償還シナリオの変化とジェネリック医薬品の競合による価格圧力が、大手製薬会社の規制関連業務アウトソーシングを引き起こしており、北米における薬事アウトソーシングサービスの成長を牽引すると予想されます。さらに、研究開発活動の活発化と臨床試験の増加が、同地域の市場成長を促進すると予想されます。例えば、Global Observatory on Health R&Dによると、米国は2021年に10,870件の臨床試験を登録し、全体の18.1%を占めました。同出典によると、カナダでは2021年に2,099件の臨床試験が登録され、全体の3.5%を占める。このように、同地域では多くの臨床試験が実施されており、薬事アウトソーシング市場を牽引する可能性が高いです。

さらに、地域の主要プレイヤーの存在と業界における戦略的提携が市場の成長を後押ししています。例えば、2021年4月、ParexelとVeeva Systemsは、テクノロジーとプロセスイノベーションを活用して臨床試験を迅速化するための戦略的提携を発表しました。両社は互いの薬事コンサルティングサービスから利益を得ることになります。

したがって、上記のすべての要因は、予測期間にわたって北米地域の市場成長を促進すると予想されます。

ヘルスケア規制関連業務アウトソーシング業界の概要

ヘルスケア規制関連業務アウトソーシング市場は、様々な市場プレーヤーの存在により、やや断片化された市場となっています。競合情勢には、Charles River Laboratories、Syneos Health、Laboratory Corporation of America Holdings、ICON Plc、IQVIA、PAREXEL International Corporation、Thermo Fisher Scientific Inc.(PPD)など、大きな市場シェアを持つ数社の分析が含まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 臨床試験数の増加

- ライフサイエンス企業のコアコンピテンシーへの注力

- 市場抑制要因

- データセキュリティに関するリスク

- 標準化の欠如

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- サービス別

- 規制コンサルティング

- 法的代理

- 薬事関連の執筆と出版

- 製品登録および臨床試験申請

- その他のサービス

- エンドユーザー別

- 製薬およびバイオテクノロジー企業

- 医療機器企業

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Accell Clinical Research, LLC

- Charles River Laboratories

- Syneos Health

- Laboratory Corporation of America Holdings

- ICON PLc.

- IQVIA

- Medpace, Inc.

- PAREXEL International Corporation

- Thermo Fisher Scientific Inc.(PPD)

- Promedica International

- WuXi App Tec

- CTI Clinical Trial & Consulting

第7章 市場機会と今後の動向

目次

The Global Healthcare Regulatory Affairs Outsourcing Market size is estimated at USD 9.08 billion in 2025, and is expected to reach USD 13.80 billion by 2030, at a CAGR of 8.74% during the forecast period (2025-2030).

During the pandemic, the massive influx of COVID-19 patients resulted in mass lockdowns, which disrupted clinical studies of various chronic diseases such as cancer. The reduction in the number of clinical trials amid the pandemic resulted in a decrease in the demand for healthcare regulatory affairs outsourcing services. For instance, a study published in the Frontiers in Medicine1 in December 2021 highlighted that clinical trial activities decreased during the pandemic as the number of COVID-19 patients increased. The source also stated that new drug submissions dropped in non-COVID-19 clinical developments amid the pandemic.

Therefore, disruptions in the global supply chain affected the manufacturing and distribution of pharmaceutical products during the pandemic's initial phase, significantly impacting the market growth. Regulatory affairs teams had to navigate challenges related to ensuring the availability and safety of essential drugs, necessitating regulatory adaptations.

Moreover, growing R&D expenditure, the increasing number of clinical trials, and the cost-effectiveness of outsourcing are expected to drive market growth. For instance, according to Global Observatory on Health R&D analysis published on February 2022, there was a constant rise in the number of newly recruiting trials registered on the WHO International Clinical Trials Registry Platform (ICTRP) for most WHO regions. Moreover, the number of trials registered in WHO's Europe, Americas, and Western Pacific regions increased at a higher rate than in other regions. For instance, in 2021, Western Pacific registered 16,860 clinical trials, around 20 times higher than that in Africa, which accounted for 851 clinical trials. Thus, an increasing number of clinical trial studies are expected to increase regulatory affairs outsourcing over the forecast period.

Furthermore, increasing research and development investment by pharmaceutical and biotechnology firms is anticipated to drive market growth. As per the PhRMA, the members of PhRMA invested about USD 102.3 billion in R&D activities in 2021. As per the data published by the European Federation of Pharmaceutical Industries and Associations in 2022, the research-based European pharmaceutical industry has increased from the past years and reached the value of EUR 300 billion (USD 323.7 billion) in 2021. The same source also stated that this industry received a significant R&D investment of EUR 41.5 billion (USD 44.77 billion) in 2021.

Additionally, various strategic activities by key market players, such as mergers and acquisitions, are anticipated to drive market growth. For instance, in July 2021, Covance acquired GlobalCare, a global leader in patient-centric decentralized clinical trials (DCTs), to expand Covance's DCT offerings into international markets and meet the growing demand for patient-centric trial designs.

Thus, the factors mentioned above are expected to increase the demand for healthcare regulatory services in the industry, thereby driving market growth over the forecast period. However, the risk associated with data security and lack of standardization is the major restraining factor for the studied market.

Healthcare Regulatory Affairs Outsourcing Market Trends

Product Registration & Clinical Trial Application Segment is Expected to Hold Significant Market Share Over the Forecast Period

Product Registration refers to the application for regulatory approval granted by the applicable authority in a given country or territory to allow a product to be marketed, distributed, sold, or imported into the country or region. The Clinical Trial Application refers to submission to the competent national regulatory authorities for getting authorization to conduct a clinical trial in the country. The clinical trial application contains detailed information about the investigational medicinal product and planned trial, allowing regulatory authorities to assess the study's feasibility.

The increase in outsourcing of clinical trial applications and product registrations in both developed and developing countries is driving the product registration and clinical trial application segment over the forecast period. Due to the complexity of the product registration process, lack of professionals in the industry, and lack of internal capability, most pharmaceutical and medical device companies outsource their product registration activities to third-party service providers. Furthermore, constant changes and updation in regulatory affairs also drive the outsourcing of such services. For instance, on 31 January 2022, the European Medicines Agency announced the regulatory harmonization of clinical trials in the EU. It also launched a new Clinical Trials Information System (CTIS). This is anticipated to propel the segment growth over the forecast period.

Thus, all factors mentioned above are expected to boost segment growth over the forecast period.

North America is Expected to Hold Major Market Share Over the Forecast Period

Pricing pressure due to the changing reimbursement scenario and generic competition is causing major pharmaceutical firms to outsource regulatory affairs activities expected to drive the growth of healthcare regulatory outsourcing services in North America. Additionally, growing research and development activity and rising clinical trials are anticipated to drive regional market growth. For instance, according to the Global Observatory on Health R&D, the United States registered 10,870 clinical trials in 2021, accounting for 18.1% of the total. According to the same source, Canada registered 2,099 clinical trials in 2021, accounting for 3.5% of the total. Thus, many clinical trials in the region are likely to drive the regulatory affairs outsourcing market.

Moreover, the presence of key regional players and strategic collaborations in the industry are driving the market's growth. For instance, in April 2021, Parexel and Veeva Systems announced a strategic partnership to speed up clinical trials by leveraging technology and process innovation. Both businesses will benefit from each other's regulatory consulting services.

Thus, all factors above are expected to boost the market growth in the North America region over the forecast period.

Healthcare Regulatory Affairs Outsourcing Industry Overview

The Healthcare Regulatory Affairs Outsourcing Market is a slightly fragmented market owing to the presence of various market players. The competitive landscape includes an analysis of a few companies which hold significant market shares, including Charles River Laboratories, Syneos Health, Laboratory Corporation of America Holdings, ICON Plc., IQVIA, PAREXEL International Corporation, and Thermo Fisher Scientific Inc. (PPD), among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Number of Clinical Trials

- 4.2.2 Life Science Companies Focusing on Their Core Competencies

- 4.3 Market Restraints

- 4.3.1 Risk Associated with the Data Security

- 4.3.2 Lack of Standardization

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Services

- 5.1.1 Regulatory Consulting

- 5.1.2 Legal Representation

- 5.1.3 Regulatory Writing & Publishing

- 5.1.4 Product Registration & Clinical Trial Application

- 5.1.5 Other Services

- 5.2 By End User

- 5.2.1 Pharmaceutical and Biotechnology Companies

- 5.2.2 Medical Device Companies

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle-East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle-East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Accell Clinical Research, LLC

- 6.1.2 Charles River Laboratories

- 6.1.3 Syneos Health

- 6.1.4 Laboratory Corporation of America Holdings

- 6.1.5 ICON PLc.

- 6.1.6 IQVIA

- 6.1.7 Medpace, Inc.

- 6.1.8 PAREXEL International Corporation

- 6.1.9 Thermo Fisher Scientific Inc. (PPD)

- 6.1.10 Promedica International

- 6.1.11 WuXi App Tec

- 6.1.12 CTI Clinical Trial & Consulting

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 115 Pages

- 納期

- 2~3営業日