|

市場調査レポート

商品コード

1692062

アジア太平洋地域のエビ:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Asia-Pacific Shrimp - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域のエビ:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 208 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

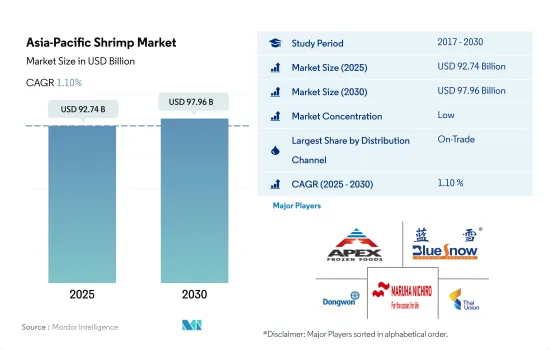

アジア太平洋地域のエビ市場規模は2025年に927億4,000万米ドルと推定され、2030年には979億6,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは1.10%で成長する見込みです。

外食産業からの需要とeコマースの台頭がエビの販売を促進

- オントレードチャネルがエビ加工品市場を独占しており、金額ベースでは2019年から2022年にかけてオントレードチャネルを通じて4.59%の成長を記録しました。外食産業は主にその品質の高さから加工エビを購入しています。エビは人に健康上の悪影響を及ぼす病気に感染している可能性があります。病害のトランスミッションは、安全上の注意を払って加工・包装することで回避されます。しかし、この地域の養殖セクターは急速に拡大しているため、価格はエビ養殖業者に大きく依存しています。ほとんどの養殖動物の死亡率は月1%程度です。

- オフトレードチャネルはエビ市場で最も急成長しているチャネルであり、予測期間中のCAGRは1.17%と予測されています。Thai Union Group PCL、Wynntech Star Sdn Bhd、Apex Frozen Foods Ltd、Blue Snow Foodなどの主要企業は、製品のイノベーションとスーパーマーケットやオンラインストアなど様々な小売チャネルを通じた事業拡大に注力しています。食習慣や消費パターンの変化、労働人口の増加に伴う多忙なライフスタイルにより、食生活に合わせたエビ加工品の需要が高まっています。

- eコマースは歴史的期間(2017~2022年)に急成長しました。パンデミックがこの地域におけるエビのオンライン販売の成長を後押ししました。モバイルアクセシビリティの向上とブロードバンドの普及は、従来の食料品購入のビジネスモデルを破壊しています。オンライン・チャネルにより、消費者はいつでもどこでも食料品を購入できるようになっています。2022年、中国における食料品オンライン・ショッピングの普及率は10.28%に達しました。予測期間中、同国ではオンライン・チャネルがさらに成長すると予想されます。

水産物に対する国内需要の増加により域内の生産と輸入が拡大

- エビ生産は中国が市場をリードし、インドネシア、インドがこれに続きます。中国は世界人口の5分の1を擁し、エビを含む世界の水産物生産量の3分の1を占めています。中国は世界最大の養殖エビ生産国になると考えられており、エビの生産量は2020年から2022年にかけて190万トンから200万トンに増加します。中国市場におけるエビの消費者需要は小売業やケータリング業で旺盛である一方、供給不足はますます輸入によって満たされています。2022年の輸入量は25.8%増の37万1,123トンで、品目別ではエクアドル産エビがトップシェア(60%)、次いでインド(12.5%)、ベトナム(6%)、カナダ(3.6%)、グリーンランド(3%)となっています。

- インドネシアはアジア太平洋で2番目に大きなエビ消費国で、販売額は2017年から2022年にかけて1.20%のCAGRを記録しています。エビの国内需要は他の水産物品種に比べ相対的に低く、ほとんどの家庭にとってエビは依然として高価な蛋白源と考えられているため、生産量の95%は輸出されています。しかし、消費者の所得が増加していることがエビの消費を後押ししており、2022年にはオントレードセグメントが58.61%のシェアを占めて市場を独占しています。

- オーストラリアは予測期間中に最も速い成長を記録すると予想され、現在の販売額は7.16%拡大しています。オーストラリアのエビは養殖コストが高いため、高価になりがちです。それにもかかわらず、養殖は国内で拡大し、政府機関によって設定された環境と衛生の制限のもとで開発されているため、現在発展途上にある同国のエビ市場をさらに拡大させる規模になる可能性があります。

アジア太平洋地域のエビ市場動向

世界中で高まるアジア産エビの需要が生産を後押しする

- アジアは世界のエビ生産量の3分の2を占め、今後も安定成長または減少が予想されます。生産コストの上昇や病気の蔓延により、この地域の多くの養殖業者は撤退するか播種率を下げています。この地域では中国が主要な生産シェアを占め、2022年には地域全体の生産量の約60%を占め、日本、インドがこれに続きます。

- 2022年初頭、中国とインドでは天候問題、疾病、飼料コストの上昇が全体の成長にマイナスの影響を与えました。この地域で発生している疾病は、腸虫性肝炎(EHP)や早期死亡症候群(EMS)といった一貫して発生している問題の組み合わせです。これらの問題は生産量の減少と生産コストの上昇につながります。インドにおけるエビの生産を増加させるため、畜産酪農省は内陸漁業と養殖業のための開発プログラムを立ち上げ、資金援助と質の高い種子を提供し、全国的な生産の質の向上に貢献しました。政府は、2020-2021年から2024-2025年までの5年間、プラダン・マントリ・マツヤ・サンパダ・ヨジャナ(PMMSY)を立ち上げ、エビの生産を強化し、2024年までに140万トンを生産するという野心的な目標を達成することを目指しました。

- アジア諸国のエビ養殖は、2017年から2022年にかけて2.68%増加しました。主要生産国のひとつであるベトナムは横ばいの成長です。ベトナムのエビ生産量は2023年に初めて100万トンに達することを目指しました。エビ生産量の増加は、ベトナムのエビ産業がエクアドル、インド、インドネシア、タイ、中国といった主要輸出国との競合を維持するのに役立つと思われます。

地域の平均価格は安定的に推移し、主要生産国で上下する見込み

- 2022年の同地域のエビ価格は2021年から0.96%上昇しました。2023年のアジアのエビ生産量はわずかながら増加すると予想されます。価格が現在の水準から大きく回復する可能性は低いです。世界の景気後退と市場におけるエビの供給過剰が重なり、2022年後半には価格が下落し、上半期末の予想とほぼ一致しました。飼料コストはピークに達するにつれて多少改善すると予想されるが、アジアの生産者が拡大できるほどではないです。

- ベトナムでは、2022年5月上旬に集約型養殖場の白足エビの価格が0.08~1.6米ドル/kgわずかに上昇しました。同国では同期間、ホワイトレッグシュリンプ(100尾/kg)は4.10~4.19米ドル/kgで販売されました。ブラックタイガーシュリンプの価格は20尾/kgで9.73~10.16米ドル/kgと2021年より0.04米ドル/kg上昇、30尾/kgで8.00~8.45米ドル/kgと2021年より0.21米ドル/kg上昇、40尾/kgで6.91~7.35米ドル/kgでした。

- 中国のエビ価格は2017年から2022年にかけて5.77%上昇しました。中国では、商業用エビの国内価格が低水準に達したが、これは農家がより厳しくなった雨季に向けた仕入れに興味を示さなくなったことを暗示しています。したがって、中国における商業エビの低価格は、消費と輸出を増加させる基盤となり得る。ベトナムがエビの輸出安全証明書を完全に実施すれば、ベトナムのエビ製品の価格は上昇する可能性が高いです。インド、タイ、中国から輸出されるエビの価格は、WTO加盟国であることのメリットとベトナムのエビの病気のデメリットを反映しており、ベトナムのエビの輸出価格に大きな影響を与えました。

アジア太平洋地域のエビ産業の概要

アジア太平洋地域のエビ市場は断片化されており、上位5社で1.19%を占めています。この市場の主要企業は以下の通りです。 Apex Frozen Foods Ltd, Blue Snow Food, Dongwon Industries Ltd, Maruha Nichiro Corporation and Thai Union Group PCL(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- 価格動向

- エビ

- 生産動向

- エビ

- 規制の枠組み

- オーストラリア

- 中国

- インド

- 日本

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- 形態

- 缶詰

- 生鮮・冷蔵

- 冷凍

- 加工

- 流通チャネル

- オフトレード

- コンビニエンスストア

- オンラインチャネル

- スーパーマーケットとハイパーマーケット

- その他

- オントレード

- オフトレード

- 国

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- 韓国

- その他アジア太平洋地域

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Apex Frozen Foods Ltd

- Blue Snow Food Co. Ltd

- De Oro Resources Inc.

- Dongwon Industries Ltd

- Maruha Nichiro Corporation

- Millennium Ocean Star Corporation

- Roda Internacional Canarias SL

- Thai Union Group PCL

- Wynntech Star Sdn Bhd

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Asia-Pacific Shrimp Market size is estimated at 92.74 billion USD in 2025, and is expected to reach 97.96 billion USD by 2030, growing at a CAGR of 1.10% during the forecast period (2025-2030).

Demand from the foodservice industry and a rise in e-commerce are driving the sales of shrimp

- The on-trade channel dominates the processed shrimp market; by value, it registered a growth of 4.59% through the on-trade channel between 2019 and 2022. The foodservice industry primarily acquires processed shrimp due to its high quality. Shrimps may be infected with diseases that have negative health effects on people. Disease transmission is avoided by processing and packaging with safety precautions. However, prices are extremely dependent on shrimp farmers, as the aquaculture sector in the region has been expanding rapidly. Most farmed animals have a mortality rate of around 1% per month.

- The off-trade channel is the fastest-growing channel in the shrimp market, and it is projected to witness a CAGR of 1.17% during the forecast period. Key players such as Thai Union Group PCL, Wynntech Star Sdn Bhd, Apex Frozen Foods Ltd, and Blue Snow Food Co. Ltd focus on product innovation and expansion through various retail channels such as supermarkets and online stores. The changing food habits and spending patterns and busy lifestyles of the growing working population are increasing the demand for processed shrimp to meet dietary habits.

- E-commerce grew rapidly during the historical period (2017-2022). The pandemic boosted the growth of online sales of shrimp in the region. Increased mobile accessibility and broadband penetration are disrupting the traditional grocery-buying business model. Online channels are enabling consumers to purchase groceries anywhere, at any time. In 2022, the penetration rate of online grocery shopping in China reached 10.28%. Online channels are further anticipated to grow in the country during the forecast period.

Production and imports in the region are expanding owing to an increase in domestic demand for seafood

- China is the market leader in shrimp production, followed by Indonesia and India. China has one-fifth of the world's population and accounts for one-third of the world's seafood production, including shrimp. China is deemed to be the largest aquaculture shrimp producer globally, with the production of shrimp rising from 1.9 million metric ton to 2 million metric ton over 2020-2022. Consumer demand for shrimp has been strong in the retail and catering trade in the Chinese market, while supply gaps are increasingly met through imports. In 2022, imports increased by 25.8% at 370,123 ton with Ecuadorean shrimp, the top product group, having lion's share (60%), followed by India (12.5%), Vietnam (6%), Canada (3.6%), and Greenland (3%).

- Indonesia is the second largest shrimp consumer in the Asia-Pacific, with sales value registering a CAGR of 1.20% over 2017-2022. The domestic demand for shrimp is relatively lower than other seafood varieties as shrimp is still considered a costly source of protein for most households, owing to which 95% of the production is exported by the country. However, the rising income of the consumers is boosting shrimp consumption, with the on-trade segment dominating the market with a share of 58.61% in 2022.

- Australia is expected to register the fastest growth during the forecast period, with the current sales value expanding by 7.16%. Due to the higher farming costs of Australian shrimp, they are often more expensive. Nonetheless, aquaculture is expanding domestically and developed with environmental and sanitation restrictions set by government agencies, which may scale further to expand the market for shrimp in the country, which is currently in a nascent state.

Asia-Pacific Shrimp Market Trends

Growing demand for Asian shrimp across the globe will propel the production

- Asia accounts for two-thirds of world shrimp production, which is anticipated to grow at a steady or declining pace. With the rising production costs and diseases, many individual farmers in the region are either exiting or reducing their seeding rates. China accounted for the major production share in the region, accounting for around 60% of the total regional production in 2022, followed by Japan and India.

- Early in 2022, weather issues, diseases, and increasing feed costs in China and India had a negative impact on the overall growth. Diseases occurring in the region are a combination of consistently occurring issues such as Enterocytozoon hepatopenaeic (EHP) and early mortality syndrome (EMS). These issues lead to a decline in production and an inclination in production costs. To increase shrimp production in India, the Department of Animal Husbandry and Dairying launched a development program for inland fisheries and aquaculture, which helped provide financial aid and quality seeds to increase production quality across the country. The government launched the Pradhan Mantri Matsya Sampada Yojana (PMMSY) for five years, i.e., 2020-2021 to 2024-2025, which aims to enhance shrimp production and achieve an ambitious target of producing 1.4 million metric tons by 2024.

- Shrimp farming in Asian countries grew by 2.68% from 2017 to 2022. Vietnam, one of the major producers, is experiencing flat growth. Vietnam's shrimp production aimed to reach 1 million tons for the first time in 2023. The increase in shrimp production will help Vietnam's shrimp industry maintain its competitiveness with leading exporting countries such as Ecuador, India, Indonesia, Thailand, and China.

Average regional prices are expected to remain stable, with ups and downs happening in major producer nations

- The shrimp prices in the region grew by 0.96% in 2022 from 2021. Shrimp production in Asia was expected to grow marginally in 2023. The prices are unlikely to recover significantly from their current levels. The combination of a global recession and a glut of shrimp in the market led to a decline in prices in the latter half of 2022, broadly in line with what was expected at the end of the first half. Feed costs are expected to improve somewhat as they reach their peak, but not enough to enable the Asian producers to expand.

- In Vietnam, the prices of white leg shrimps from intensive farms slightly increased by USD 0.08 - 1.6/kg in early May 2022. During the same period in the country, white leg shrimps (100 pcs/kg) were sold at USD 4.10 - 4.19/kg. The price of black tiger shrimp ranged between USD 9.73 - 10.16/kg for 20 pcs/kg, up by USD 0.04/kg from 2021, USD 8.00/kg - 8.45/kg for 30 pcs/kg, up by USD 0.21/kg from 2021, and USD 6.91-USD 7.35/kg for 40 pcs/kg.

- Shrimp prices in China grew by 5.77% from 2017 to 2022. In China, the domestic prices of commercial shrimp reached a low point, implying that farmers were no longer interested in stocking up for the wet season, which had become more challenging. Therefore, the low price of commercial shrimp in China can be the basis for a rise in consumption and export. If Vietnam fully implements the export safety certificates for shrimp, the prices of Vietnamese shrimp products will likely increase. The prices of shrimp exported from India, Thailand, and China reflected the advantages of being members of the WTO and the disadvantages of the shrimp diseases in Vietnam, which significantly affected the export prices of Vietnamese shrimp.

Asia-Pacific Shrimp Industry Overview

The Asia-Pacific Shrimp Market is fragmented, with the top five companies occupying 1.19%. The major players in this market are Apex Frozen Foods Ltd, Blue Snow Food Co. Ltd, Dongwon Industries Ltd, Maruha Nichiro Corporation and Thai Union Group PCL (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Price Trends

- 3.1.1 Shrimp

- 3.2 Production Trends

- 3.2.1 Shrimp

- 3.3 Regulatory Framework

- 3.3.1 Australia

- 3.3.2 China

- 3.3.3 India

- 3.3.4 Japan

- 3.4 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Form

- 4.1.1 Canned

- 4.1.2 Fresh / Chilled

- 4.1.3 Frozen

- 4.1.4 Processed

- 4.2 Distribution Channel

- 4.2.1 Off-Trade

- 4.2.1.1 Convenience Stores

- 4.2.1.2 Online Channel

- 4.2.1.3 Supermarkets and Hypermarkets

- 4.2.1.4 Others

- 4.2.2 On-Trade

- 4.2.1 Off-Trade

- 4.3 Country

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Indonesia

- 4.3.5 Japan

- 4.3.6 Malaysia

- 4.3.7 South Korea

- 4.3.8 Rest of Asia-Pacific

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 5.4.1 Apex Frozen Foods Ltd

- 5.4.2 Blue Snow Food Co. Ltd

- 5.4.3 De Oro Resources Inc.

- 5.4.4 Dongwon Industries Ltd

- 5.4.5 Maruha Nichiro Corporation

- 5.4.6 Millennium Ocean Star Corporation

- 5.4.7 Roda Internacional Canarias SL

- 5.4.8 Thai Union Group PCL

- 5.4.9 Wynntech Star Sdn Bhd

6 KEY STRATEGIC QUESTIONS FOR SEAFOOD INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms