アフリカの植物性タンパク質成分:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Africa Plant Protein Ingredients - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 218 Pages

- 納期

- 2~3営業日

- 商品コード

- 1692027

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

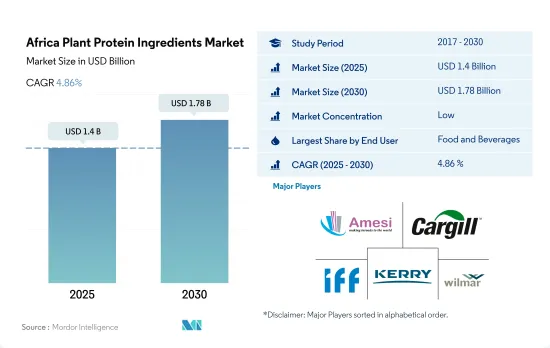

アフリカの植物性タンパク質成分市場規模は2025年に14億米ドルと推定され、2030年には17億8,000万米ドルに達し、予測期間中(2025年~2030年)のCAGRは4.86%で成長すると予測されています。

F&B産業が支配的で、食肉代替セグメントからの植物性タンパク質への需要が旺盛

- F&B産業がアフリカの植物性タンパク質市場を牽引しています。2023年には最大のシェアを占め、2021年から2023年にかけて金額ベースで6.27%の成長を示しています。代替肉における植物性タンパク質の用途は、主要なF&Bサブセグメントの1つであり、2024年から2029年の間にCAGR 4.23%を記録すると予測されています。植物性タンパク質成分の用途は、特に食肉および食肉代替品セグメントにおいて、その膨大な機能性により拡大しています。製品メーカーはまた、消費者の認識の変化により、提供する地域を拡大しています。例えば、植物ベースの肉代替ブランドFuture Farmは2021年に南アフリカで発売されました。

- パーソナルケア・化粧品分野もまた、パーソナルケア製品については特にeコマースにおける拡大的なマーケティングキャンペーンと流通チャネルの増加により、4.35%という高いCAGRで推移すると予測されています。美容・化粧品業界の国際的な大手企業は、業界の「次なるフロンティア」と見なされているサハラ以南のアフリカで予想されるブームを最大限に活用しています。植物性タンパク質は、皮膚の角質層やその付属物と水分を結合させる能力があるため、健康な皮膚や毛髪に適した環境を育むのに有益な成分と考えられています。

- 動物飼料セグメントは、2021年から2023年にかけて金額ベースで4.79%成長しました。動物飼料セグメントにおけるタンパク質用途は、使用コストが低く、消化性に優れ、風味がニュートラルであることから、主に大豆タンパク質と小麦タンパク質を中心とする植物性タンパク質が牽引しています。また、植物性タンパク質は食物繊維が豊富で、動物にとって良質な飼料源となります。

アフリカ諸国における植物性製品に対する需要の高まりと植物性タンパク質成分の注目すべき急増

- アフリカの植物性タンパク質市場はナイジェリアが牽引しており、予測期間中に金額ベースで最速のCAGR 5.97%を記録すると予測されています。同国はベジタリアンの人口が少ないにもかかわらず、菜食主義やベジタリアニズムの受け入れが進んでいるため、業界は拡大すると予測されます。ナイジェリアでは、Z世代とミレニアル世代の5人に4人が植物性タンパク質を試す可能性が高いです。アフリカは歴史的に食糧安全保障の混乱と栄養不良の影響を受けやすく、植物性タンパク質ソリューションは食糧安全保障を向上させる可能性があります。

- 南アフリカはもう一つの主要市場であり、主に動物飼料への大豆タンパク質の応用が牽引しています。同国の動物飼料分野は比較的大きく、アフリカの動物飼料産業全体の33.04%を占めており、南アフリカ市場の成長をさらに後押ししています。大豆タンパク質は、その低コストと高タンパク質含有量により、動物飼料分野で一般的に使用されています。様々な年齢の離乳早期の子豚に給与するために、分離大豆タンパク質をホエイパウダーのような高品質の炭水化物飼料と組み合わせて使用することで、脱脂粉乳と同様の成長成績を達成しています。

- アフリカ全土、特にケニア、ナイジェリア、南アフリカでは、植物性食肉に対する消費者の受容性が広まり、大きな需要があります。ケニア、ナイジェリア、南アフリカでは、それぞれ約182万人、1,700万人、150万人が深刻な栄養不良に苦しんでいます。栄養失調の蔓延が著しいため、植物性タンパク質市場は今後、この地域全体で成長する可能性が高いです。したがって、アフリカの植物性タンパク質市場は、2024年から2029年の間に金額ベースで4.58%のCAGRで推移すると予測されます。

アフリカの植物性タンパク質成分市場動向

ケニアやナイジェリアのような国々では植物性食品への関心が高まっており、植物性タンパク質の消費は着実に成長します。

- グラフはアフリカ全体の一人当たりの植物性タンパク質消費量を示しています。この地域のメーカーは、コスト・リーダーシップを獲得するために常にオープン・イノベーションを採用し、開発初期段階でサプライヤーを固定しています。スポーツ栄養製品に含まれる植物原料が用途別市場の主要シェアを占め、次いで動物飼料が続きます。消費者のライフスタイルの変化とヘルスケアコストの上昇が、植物性タンパク質市場の成長に重要な役割を果たしています。サハラ以南のアフリカにおける医療費は2019年に29.98%上昇しました。小売業界の盛況により市場は加速度的に拡大しています。明確な表示に対する消費者の要求の高まりは、消化のしやすさ、アレルゲンのなさ、持続可能性も提供する植物性タンパク質へのニーズを後押ししています。

- 同国における植物性蛋白質に対する需要の高まりは、主要な市場関係者に需要の高まりに対応する原料を提供するよう促しています。ケニアのような国では、ミレニアル世代の消費者の80%近くが植物性タンパク質を試す可能性があります。ナイジェリアでは、76%の消費者が植物性食品を好んでいます。植物性食品が高いレベルで受け入れられていることは、伝統的な食肉への依存を最小限に抑え、公衆衛生、環境、動物福祉の成果を高める機会を提供します。

- 肥満のような予防可能な病態と闘うために、消費者の健康意識はより広まりつつあり、人々はますます植物に目を向けるようになっています。この地域では、植物性食品を摂取することの健康上の利点に対する消費者の意識の高まりから、ビーガンおよびベジタリアン食品に対する需要が増加しており、ビーガンオプションを特徴とする外食店の設立につながっています。2020年には、南アフリカで菜食主義者の持ち帰り注文が71%急増し、大陸でトップの売上を記録しました。

大豆、小麦、エンドウ豆の生産は、植物性タンパク質成分メーカーの原料として大きく貢献しています。

- グラフはアフリカ全体の乾燥豆、米、大豆、小麦の生産量を表しています。アフリカの生産者が供給する大豆は、世界の大豆の1%にも満たないです。南アフリカ、ナイジェリア、ザンビアがアフリカの大豆生産量トップ3です。南アフリカの大豆生産量は、2016年の74万2,000トンから2020年には124万5,500トンに増加します。大規模農場での商業的大豆生産は、ザンビア、ジンバブエ、南アフリカで行われています。しかし、アフリカの他の地域では、小規模農家による栽培がほとんどで、ソルガム、トウモロコシ、キャッサバの中のマイナーな食用作物として植えられています。

- ナイジェリアの6年間(2016~2021年)の平均大豆生産量は45万4,600トンで、これはアフリカ大陸の生産量の25%です。ザンビアの3年平均生産量は1,040万ブッシェルで、これは大陸の生産量の約10%でした。データが入手可能な他の21カ国の大豆生産量は、アフリカ全体の25%でした。国別平均生産量は402万6,969ブッシェルで、最も生産量が少なかったのはマダガスカルで、3年間の平均生産量は1,470ブッシェルでした。

- 伝統的に、小麦はアフリカの主要な主食作物ではありません。パンのような手軽で速い食べ物への嗜好の変化に伴う急速な人口増加により、重要な食料作物となりつつあります。アフリカの小麦生産量は、2017年の2,660万トンに対し、2021年は約3,040万トンです。2013年、サハラ以南のアフリカにおける小麦の総消費量は2,500万トンに達し、輸入量は1,750万トン、60億米ドルに達しました。同期間、この地域の総面積は290万ヘクタールで、生産量はわずか730万トンに過ぎませんでした。同地域の生産性が低い(2t/ha)のは、主に生物的・生物的ストレスによるものです。

アフリカの植物性タンパク質成分産業概要

アフリカの植物性タンパク質成分市場は断片化されており、上位5社で5.37%を占めています。この市場の主要企業は以下の通りです。 Amesi Group, Cargill Incorporated, International Flavors & Fragrances Inc., Kerry Group PLC and Wilmar International Ltd(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- エンドユーザー市場規模

- ベビーフードおよび乳児用調製粉乳

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品および乳製品代替製品

- 高齢者栄養・医療栄養

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- スポーツ/パフォーマンス栄養

- 動物飼料

- パーソナルケアと化粧品

- タンパク質消費動向

- 植物

- 生産動向

- 植物

- 規制の枠組み

- 南アフリカ

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- タンパク質タイプ

- ヘンプ・プロテイン

- エンドウ豆プロテイン

- ジャガイモ・プロテイン

- 米プロテイン

- 大豆プロテイン

- 小麦プロテイン

- その他の植物性タンパク質

- エンドユーザー

- 動物飼料

- 食品・飲料

- サブエンドユーザー別

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品・乳製品代替品

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- パーソナルケアと化粧品

- サプリメント

- サブエンドユーザー別

- ベビーフードおよび乳児用調製粉乳

- 高齢者栄養と医療栄養

- スポーツ/パフォーマンス栄養

- 国別

- ナイジェリア

- 南アフリカ

- その他のアフリカ

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- A. Costantino & C. SpA

- Amesi Group

- Axiom Foods Inc.

- Cargill Incorporated

- International Flavors & Fragrances Inc.

- Kerry Group PLC

- Wilmar International Ltd

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The Africa Plant Protein Ingredients Market size is estimated at 1.4 billion USD in 2025, and is expected to reach 1.78 billion USD by 2030, growing at a CAGR of 4.86% during the forecast period (2025-2030).

The F&B industry dominates, with strong demand for plant proteins from the meat alternative segment

- The F&B industry drives the African plant protein market. It accounted for the largest share in 2023, witnessing a growth of 6.27% by value from 2021 to 2023. The applications of plant proteins in meat alternatives are one of the primary F&B sub-segments, projected to register a CAGR of 4.23% between 2024 and 2029. Applications of plant protein ingredients are growing due to their immense functionalities, especially in the meat and meat alternatives segment. Product manufacturers are also expanding their regional offerings due to the changing consumer perceptions. For instance, the plant-based meat alternative brand Future Farm was launched in South Africa in 2021.

- The personal care and cosmetics segment is also projected to register a high CAGR of 4.35%, owing to expansive marketing campaigns and increasing distribution channels, especially in e-commerce for personal care products. Major international players in the beauty and cosmetics industry are maximizing the boom anticipated for Sub-Saharan Africa, which is viewed as the industry's "next frontier." Because of their capacity to bind water with the horny layer of skin and its annexes, plant proteins are considered beneficial components for fostering an environment favorable for healthy skin and hair.

- The animal feed segment grew by 4.79% in value terms from 2021 to 2023. Protein applications in the animal feed segment are driven by plant proteins, mainly soy and wheat proteins, due to their low cost-in-use, excellent digestibility, and neutral flavor profile. Plant proteins are also considered high in dietary fiber, which acts as a good source of diet for animals.

Rising demand for plant-based products and notable surge in the adoption of plant protein ingredients in Rest of Africa

- The African plant protein market is led by Nigeria, which is also projected to record the fastest CAGR of 5.97% by value during the forecast period. Despite the country's small vegetarian population, the industry is projected to expand due to the growing acceptance of veganism or vegetarianism. Four out of five Gen Z and millennials in Nigeria are highly likely to try plant-based proteins. Africa has historically been susceptible to food security disruptions and malnutrition, with plant-based protein solutions a potential source of increased food security.

- South Africa is another leading market, largely led by soy protein applications in animal feed. The comparatively bigger animal feed segment of the country, accounting for a 33.04% share of the overall African animal feed industry, has further catered to the growth of the South African market. Soy protein is commonly used in the animal feed segment due to its low cost and high protein content. The use of soy protein isolates in combination with high-quality carbohydrate feed such as whey powder to feed early-weaned piglets of different ages has achieved similar growth performance to skimmed milk powder.

- There is widespread consumer acceptability and significant demand for plant-based meat throughout Africa, especially in Kenya, Nigeria, and South Africa. About 1.82 million, 17 million, and 1.5 million people in Kenya, Nigeria, and South Africa suffer from severe malnutrition, respectively. Due to the significant prevalence of malnutrition, the plant-based protein market is likely to grow across the region in the future. Thus, the African market for plant proteins is anticipated to register a CAGR of 4.58% by value between 2024 and 2029.

Africa Plant Protein Ingredients Market Trends

Plant protein consumption to grow steadily, with countries like Kenya and Nigeria seeing more inclination toward plant-based food

- The graph depicts the per capita consumption of plant protein for the whole of Africa. Manufacturers in the region constantly embrace open innovation to gain cost leadership and fixed suppliers in the early development stage. Plant ingredients in sports nutrition products constitute the major share of the market by application, followed by animal feed. Changing consumer lifestyles and rising healthcare costs are playing a vital role in the growth of the plant protein market. Health expenditure in Sub-Saharan Africa rose by 29.98% in 2019. The market is expanding at an accelerated rate due to the retail industry's thriving growth. Increased consumer demand for clear labeling drives the need for plant proteins, which also offer ease of digestion, no allergens, and sustainability.

- The rising demand for plant-based proteins in the country has urged key market players to provide ingredients to cater to the rising demand. In countries like Kenya, nearly 80% of millennial consumers are likely to try a plant-based protein. In Nigeria, 76% of consumers lean toward plant-based food. The high level of acceptance of plant-based products provides an opportunity to minimize dependence on traditional meat, enhancing outcomes for public health, the environment, and animal welfare.

- To combat preventable conditions such as obesity, health awareness among consumers is becoming more widespread, and people are increasingly turning to plants. The region's demand for vegan and vegetarian food has increased due to consumers' growing awareness about the health benefits of consuming plant-based foods, leading to the establishment of food service outlets featuring vegan options. In 2020, South Africa saw a 71% spike in vegan takeaway orders, making it the continent's top seller.

Soy, wheat, and pea production contributes majorly as raw material for plant protein ingredients manufacturers

- The graph depicts the production of dry peas, rice, soybeans, and wheat for the whole of Africa. African producers supply less than 1% of the world's soybeans. South Africa, Nigeria, and Zambia are the top three soybean producers in Africa. Soybean production in South Africa increased from 742,000 tons in 2016 to 1,245,500 tons in 2020. Commercial soybean production on large farms takes place in Zambia, Zimbabwe, and South Africa. However, it is mostly cultivated by small-scale farmers in other parts of Africa, where it is planted as a minor food crop among sorghum, maize, or cassava.

- Nigeria's six-year production (2016-2021) of soybean average was 454,600 tons, which was 25% of the continent's production. Zambia's three-year average was 10.4 million bushels, which was around 10% of the continent's production. The other 21 countries, where data are available, produced 25% of Africa's total soybean production. The average national production was 4,026,969 bushels, and the smallest producer was Madagascar, whose three-year production average was 1,470 bushels.

- Traditionally, wheat was not the leading staple crop in Africa. It is becoming an important food crop because of rapid population growth associated with changes in food preference for easy and fast food, such as bread. Africa produced around 30.4 million metric tons of wheat in the trading year 2021, compared to 26.6 million metric tons in 2017. In 2013, total wheat consumption in Sub-Saharan Africa reached 25 million tons, with imports amounting to 17.5 million tons at USD 6 billion. During the same period, the region produced only 7.3 million tons on a total area of 2.9 million ha. The region's low productivity (2t/ha) is principally because of abiotic and biotic stresses.

Africa Plant Protein Ingredients Industry Overview

The Africa Plant Protein Ingredients Market is fragmented, with the top five companies occupying 5.37%. The major players in this market are Amesi Group, Cargill Incorporated, International Flavors & Fragrances Inc., Kerry Group PLC and Wilmar International Ltd (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Plant

- 3.3 Production Trends

- 3.3.1 Plant

- 3.4 Regulatory Framework

- 3.4.1 South Africa

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Protein Type

- 4.1.1 Hemp Protein

- 4.1.2 Pea Protein

- 4.1.3 Potato Protein

- 4.1.4 Rice Protein

- 4.1.5 Soy Protein

- 4.1.6 Wheat Protein

- 4.1.7 Other Plant Protein

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Confectionery

- 4.2.2.1.6 Dairy and Dairy Alternative Products

- 4.2.2.1.7 Meat/Poultry/Seafood and Meat Alternative Products

- 4.2.2.1.8 RTE/RTC Food Products

- 4.2.2.1.9 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

- 4.3 Country

- 4.3.1 Nigeria

- 4.3.2 South Africa

- 4.3.3 Rest of Africa

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 A. Costantino & C. SpA

- 5.4.2 Amesi Group

- 5.4.3 Axiom Foods Inc.

- 5.4.4 Cargill Incorporated

- 5.4.5 International Flavors & Fragrances Inc.

- 5.4.6 Kerry Group PLC

- 5.4.7 Wilmar International Ltd

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 218 Pages

- 納期

- 2~3営業日