南米の植物性たんぱく質成分:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

South America Plant Protein Ingredients - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 222 Pages

- 納期

- 2~3営業日

- 商品コード

- 1683502

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

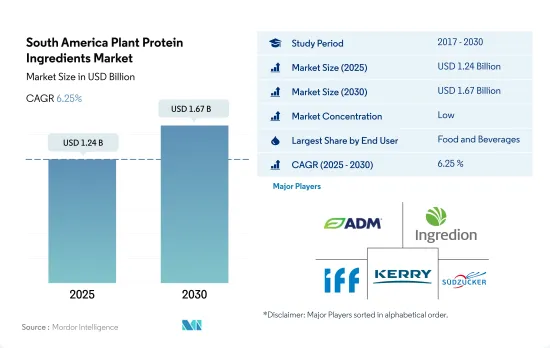

南米の植物性たんぱく質成分市場規模は2025年に12億4,000万米ドルと推計され、2030年には16億7,000万米ドルに達すると予測され、予測期間中(2025-2030年)のCAGRは6.25%で成長すると予測されます。

乳製品や肉に代わる植物性たんぱく質への需要の高まりにより、F&Bセグメントが市場を独占しています。

- F&Bセグメントは食肉および食肉代替物のサブセグメントが支配的であり、予測期間中に数量ベースで4.74%のCAGRで推移する見込みです。蛋白質原料は肉の食感を模倣する特性を提供するため、菜食主義者に適しています。健康的な食習慣に関する知識の高まりと環境への配慮が、同地域におけるこれらの品目の需要を促進しています。エンドウ豆たんぱく質と小麦たんぱく質は、肉代替食品の製造に使用される主な植物性たんぱく質成分です。小麦たんぱく質は最も速いペースで成長しており、予測期間中に数量ベースで3.15%のCAGRで推移すると予想されます。これは、小麦たんぱく質に含まれるグルテンの弾力性と柔軟性の特性によるもので、具体的には肉製品の構造を変化させる。動物性たんぱく質に類似した高品質のアミノ酸組成の存在は、構造化植物性たんぱく質製品に使用されます。

- 動物飼料は依然として第2位のエンドユーザー・セグメントです。アルゼンチンが市場を独占し、予測期間中に金額ベースで7.34%のCAGRで推移すると予想されています。大豆は豊富な栄養源であり、他のたんぱく質源に比べて化学組成の変動が少ないです。そのため、大豆は飼料に広く使用されています。濃縮大豆は消化しやすいアミノ酸を含み、脂質と水分の保持を助けるため、鶏のプレスターターミールに最適です。この分野でのたんぱく質の売上が高いのは、国内の大豆生産量が多いためです。2022年のアルゼンチンの大豆生産量は4,895万トンでした。2031年には5,286万トンに増加すると予想されています。同国の大豆生産量の多さは、手頃な価格での大量供給につながります。供給量の増加は、メーカーが動物飼料に他の原料の代わりに大豆たんぱく質を配合することを促します。

代替たんぱく質ベースの食品がブラジル全土で脚光を浴び、同地域の市場シェアを押し上げる

- 南米における植物性たんぱく質消費は、主に大豆たんぱく質の需要増加によって牽引されています。過去5年間は、大豆、乳清、乳たんぱく質製品がこの地域の高たんぱく質製品発売の70%を占めていたが、植物ベースのたんぱく質源が人気を集めています。主流の飲食品製品には、エンドウ豆、米、チアシード、オーツ麦、ジャガイモ由来のたんぱく質が配合されています。ラテンアメリカの消費者の40%以上が、植物性たんぱく質が健康を改善すると回答しています。エンドウ豆とコメのたんぱく質は、市場で最も人気のある植物性たんぱく質です。エンドウ豆たんぱく質は、予測期間中、数量ベースで9.82%の最高のCAGRで推移すると予想されます。植物たんぱく質の用途は、焼き製品のたんぱく質強化の高まりに支えられたF&Bセグメントでの用途によって支えられています。ベーカリー分野では従来の植物たんぱく質が主流であるが、特定の機能特性や栄養価の高さから新興の供給源も支持を集めています。

- 2022年にはブラジルが最大のシェアを占め、同年の売上はF&Bセグメントの植物性たんぱく質が独占しました。この背景には、2050年までに3倍になると推定される、約6,600万人のブラジル人を含む同国の高齢化があります。消費者はますます健康的な食生活を求めるようになっています。レビュー期間中、ブラジルでは、The New Butchers、Future Farm、Behind The Foods、Superbomといった新興企業の出現により、植物性たんぱく質ベースの製品がいくつか発売されました。ブラジルは、南米諸国の中で最速の成長ポテンシャルを記録し、予測期間中にCAGR 6.46%を記録する見込みです。同地域の人口の約半分を擁する同国は、膨大な消費者基盤を有しているため、競合他社から大きな注目を集めています。

南米の植物性たんぱく質成分市場動向

地域別植物性たんぱく質消費量で最大のシェアを占めるブラジル

- グラフは、南米各国の一人当たりの植物性たんぱく質消費量を示しています。ブラジルでは、農業と食品生産が極めて重要な経済の柱として際立っています。この需要の高まりは、2050年までに3倍になると予測され、約6,600万人にのぼるとされる同国の高齢化が大きな要因となっています。ブラジルの植物性たんぱく質は、たんぱく質・バー、エネルギー・バー、朝食用シリアル、加工肉における味や食感の向上から、フィットネス分野における代替肉や筋肉増強サプリメントまで、多様な用途に利用されています。特筆すべきは、大豆たんぱく質が市場を席巻し、小麦たんぱく質とエンドウ豆たんぱく質が僅差で追っていることです。

- アルゼンチンでは、4,000万人以上が菜食主義を採用していることから、野菜中心の料理の需要が急増しています。この変化は、ブエノスアイレス、コルドバ、メンドーサといった大都市で特に顕著で、住民は日々の多量栄養素のニーズを満たすために植物性食品を利用するようになっています。

- ブラジルのような国々では、グルテンや乳糖不耐症に悩む人口の増加を背景に、植物由来の乳製品の人気が急速に高まっています。実際、この地域の人口の80~85%が乳糖不耐症です。その結果、代替乳製品への需要が高まっています。植物性たんぱく質食品の売上増加は、食生活を向上させるだけでなく、農業による二酸化炭素排出の抑制にも役立ちます。しかし、進化する市場力学と需要の高まりは、サプライ・チェーンにおける持続可能性の課題をもたらす可能性があります。その結果、この地域の他の国々もブラジルの動向を反映し、日常の食生活におけるエンドウ豆やその他の蛋白源の消費拡大を提唱しています。

大豆とエンドウ豆の生産は予測期間中に大幅な成長を遂げるだろう

- 南米諸国では主要原材料の栽培が急増しており、大豆、エンドウ豆、小麦が植物性たんぱく質調達の主導権を握っています。特に、この地域の大豆栽培面積は、2000年の26.4 Mhaから2019年には55.1 Mhaへと2倍以上に増加しています。しかし、悪天候、特に干ばつや、ロシアのウクライナ侵攻などの地政学的な出来事といった課題が、大豆生産の減少につながっています。2022年2月までに、ブラジルの大豆収穫量は4,610MBUに達し、1月の当初予想の5,162MBUから大幅に減少しました。

- アルゼンチンはグリーンピースの主要生産国として際立っており、ドライエンドウの栽培面積は増加傾向を示し、1971年から2020年の期間には変動していたが、2020年には167,541ヘクタールに達します。世界の輸出シェア7%を占めるアルゼンチンは、この地域の主要な小麦生産国・輸出国です。アルゼンチンの小麦栽培は、主に3つの地域に集中している:同国の小麦栽培は、北部、中部、南部(ボルサ・コメルシオ・ロサリオ)の3つの地域に集中しており、後者2地域が総生産量の95%以上を占めています。一方、ブラジルは小麦の輸入に大きく依存しており、パラグアイ、ロシア、ウルグアイ、カナダから15%、アルゼンチンから75%を輸入しています。ウクライナ危機により、主要な小麦輸入国、特に黒海からの供給に依存している国の間で懸念が高まっており、アルゼンチンの作付農家は戦略的に小麦の作付計画を立てています。特に、アルゼンチンの主要農業地域であるパンパでは、小麦が最近の作物輪作で目立つようになってきています。

南米の植物性たんぱく質成分産業概要

南米の植物性たんぱく質成分市場は細分化されており、上位5社で38.41%を占めています。この市場の主要企業は以下の通りです。 Archer Daniels Midland Company, Ingredion Incorporated, International Flavors & Fragrances, Inc., Kerry Group plc and Sudzucker AG(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- エンドユーザー市場規模

- ベビーフードおよび乳児用調製乳

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品および乳製品代替製品

- 高齢者栄養・医療栄養

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- スポーツ/パフォーマンス栄養

- 動物飼料

- パーソナルケアと化粧品

- たんぱく質消費動向

- 植物

- 生産動向

- 植物

- 規制の枠組み

- ブラジルとアルゼンチン

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- たんぱく質タイプ

- ヘンプたんぱく質

- エンドウ豆たんぱく質

- ポテトたんぱく質

- 米たんぱく質

- 大豆たんぱく質

- 小麦たんぱく質

- その他の植物性たんぱく質

- エンドユーザー

- 動物飼料

- 飲食品

- サブエンドユーザー別

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品・乳製品代替品

- 肉・鶏肉・魚介類および肉代替製品

- RTE/RTC食品

- スナック

- パーソナルケアと化粧品

- サプリメント

- サブエンドユーザー別

- ベビーフードおよび乳児用調製粉乳

- 高齢者栄養と医療栄養

- スポーツ/パフォーマンス栄養

- 国別

- アルゼンチン

- ブラジル

- その他南米

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- Archer Daniels Midland Company

- Bremil Group

- BRF S.A.

- Bunge Limited

- Ingredion Incorporated

- International Flavors & Fragrances, Inc.

- Kerry Group plc

- Sudzucker AG

- Tereos SCA

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The South America Plant Protein Ingredients Market size is estimated at 1.24 billion USD in 2025, and is expected to reach 1.67 billion USD by 2030, growing at a CAGR of 6.25% during the forecast period (2025-2030).

The F&B segment dominates the market due to the growing demand for plant protein from dairy and meat alternatives

- The F&B segment is dominated by the meat and meat alternatives sub-segment, which is expected to record a CAGR of 4.74% by volume during the forecast period. Protein ingredients provide properties that mimic meat texture, making them suitable for vegans. The growing knowledge of healthy eating habits and environmental concerns are driving the demand for these items in the region. Pea protein and wheat protein are the major plant protein ingredients used in manufacturing meat substitutes. Wheat protein is growing at the fastest rate, and it is expected to record a CAGR of 3.15% by volume during the forecast period. This is due to the elasticity and flexibility traits of gluten, which are present in wheat protein, specifically changing the structure of meat products. The presence of high-quality amino acid composition, which is similar to animal protein, is used in structured plant protein products.

- Animal feed remained the second-largest end-user segment. Argentina dominated the market and is expected to record a CAGR of 7.34% by value during the forecast period. Soy is a rich nutritional source with a less variable chemical composition than other protein sources. Thus, soy is widely used in feed. Soy concentrates are ideal for chicken's pre-starter meal as they contain easily digestible amino acids and aid with lipid and water retention. The high sales of proteins in this segment are attributed to the nation's massive soy production. In 2022, soybean production in Argentina was 48.95 million ton. It is expected to increase to 52.86 million ton by 2031. High soy production in the country leads to high supply volume at affordable prices. The rise in supply encourages manufacturers to incorporate soy protein instead of other ingredients in animal feed.

Alternative protein-based food is gaining prominence across Brazil, boosting the market share of the region

- Plant protein consumption in South America is driven primarily by increasing demand for soy proteins. Over the last five years, soy, whey, and milk protein products accounted for 70% of all regional high-protein launches, but plant-based protein sources are gaining traction. Mainstream food and beverage products incorporate proteins derived from peas, rice, chia seeds, oats, and potatoes. More than 40% of Latin American consumers reported that plant-based protein improved their health. Pea and rice proteins are the most popular plant proteins on the market. Pea protein is expected to register the highest CAGR of 9.82% by volume during the forecast period. The application of plant proteins is supported by application in the F&B segment, supported by the growing protein fortification of baked products. Conventional plant proteins dominate the bakery segment, but emerging sources are also gaining traction because of their specific functional properties and nutritional value.

- Brazil claimed the largest share in 2022; plant protein in the F&B segment dominated sales in the same year. This could be attributed to the country's aging population, which is estimated to triple by 2050, encompassing around 66 million Brazilians. Consumers are increasingly adopting healthy diets. During the review period, the nation witnessed several plant protein-based product launches with the emergence of start-ups, The New Butchers, Future Farm, Behind The Foods, and Superbom. Brazil recorded the fastest growth potential among all South American countries, and it is expected to register a CAGR of 6.46% during the forecast period. The country, bearing about half of the region's population, has a vast consumer base and, thus, receives significant attention from competitors.

South America Plant Protein Ingredients Market Trends

Brazil holds the largest share in the regional plant protein consumption

- The graph illustrates the per capita consumption of plant protein across South American nations. In Brazil, agriculture and food production stand out as pivotal economic pillars. This heightened demand is largely driven by the country's aging demographic, projected to triple by 2050, encompassing approximately 66 million individuals. Plant proteins in Brazil find diverse applications, from enhancing taste and texture in protein and energy bars, breakfast cereals, and processed meats to serving as meat alternatives and muscle-gain supplements in the fitness sector. Notably, soy protein dominates the market, leading the pack, closely trailed by wheat and pea proteins.

- Argentina has seen a surge in demand for vegetable-centric dishes, attributed to over 40 million individuals adopting a vegan diet. This shift is especially pronounced in major urban centers like Buenos Aires, Cordoba, and Mendoza, where residents are turning to plant-based diets to meet their daily macronutrient needs.

- Countries like Brazil are witnessing a swift rise in the popularity of plant-based dairy products, driven by a growing segment of the population grappling with gluten and lactose intolerances. In fact, an overwhelming 80-85% of the region's populace is lactose intolerant. Consequently, the appetite for alternative dairy options is on the upswing. The uptick in sales of plant-based protein foods not only enhances diets but also aids in curbing agricultural carbon emissions. However, evolving market dynamics and escalating demand could pose sustainability challenges in supply chains. As a result, other nations in the region are mirroring Brazil's trend, advocating for increased consumption of peas and other protein sources in their daily diets.

Soy and pea production will witness significant growth during forecast period

- South American countries have seen a surge in the cultivation of key raw materials, with soybeans, peas, and wheat taking the lead in plant protein sourcing. Notably, the soybean cultivation area in the region more than doubled from 26.4 Mha in 2000 to 55.1 Mha by 2019. However, challenges like adverse weather, particularly droughts, and geopolitical events, such as Russia's invasion of Ukraine, have led to a decline in soybean production. By February 2022, Brazil's soybean crop had reached 4,610 MBU, a significant drop from the initial January forecast of 5,162 MBU.

- Argentina stands out as a key producer of green peas, with the cultivation area for dry peas showing an upward trend, reaching 167,541 ha by 2020 after fluctuating over the 1971-2020 period. Dominating global exports with a 7% share, Argentina emerges as the primary wheat producer and exporter in the region. The nation's wheat cultivation is concentrated in three main areas: North, Central, and South (Bolsa Comercio Rosario), with the latter two regions contributing over 95% of the total production. In contrast, Brazil heavily relies on wheat imports, with 15% sourced from Paraguay, Russia, Uruguay, and Canada and a significant 75% coming from Argentina. Concerns are rising among major wheat importers, especially those dependent on Black Sea supplies, due to the Ukrainian crisis, and Argentine crop farmers are strategically planning their wheat planting. Notably, in the Pampas, Argentina's primary agricultural region, wheat has been gaining prominence in recent crop rotations.

South America Plant Protein Ingredients Industry Overview

The South America Plant Protein Ingredients Market is fragmented, with the top five companies occupying 38.41%. The major players in this market are Archer Daniels Midland Company, Ingredion Incorporated, International Flavors & Fragrances, Inc., Kerry Group plc and Sudzucker AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Plant

- 3.3 Production Trends

- 3.3.1 Plant

- 3.4 Regulatory Framework

- 3.4.1 Brazil and Argentina

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Protein Type

- 4.1.1 Hemp Protein

- 4.1.2 Pea Protein

- 4.1.3 Potato Protein

- 4.1.4 Rice Protein

- 4.1.5 Soy Protein

- 4.1.6 Wheat Protein

- 4.1.7 Other Plant Protein

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Confectionery

- 4.2.2.1.6 Dairy and Dairy Alternative Products

- 4.2.2.1.7 Meat/Poultry/Seafood and Meat Alternative Products

- 4.2.2.1.8 RTE/RTC Food Products

- 4.2.2.1.9 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

- 4.3 Country

- 4.3.1 Argentina

- 4.3.2 Brazil

- 4.3.3 Rest of South America

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Archer Daniels Midland Company

- 5.4.2 Bremil Group

- 5.4.3 BRF S.A.

- 5.4.4 Bunge Limited

- 5.4.5 Ingredion Incorporated

- 5.4.6 International Flavors & Fragrances, Inc.

- 5.4.7 Kerry Group plc

- 5.4.8 Sudzucker AG

- 5.4.9 Tereos SCA

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 222 Pages

- 納期

- 2~3営業日