炭化ケイ素(SiC)ウエハー:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

Silicon Carbide (SiC) Wafer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1911314

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

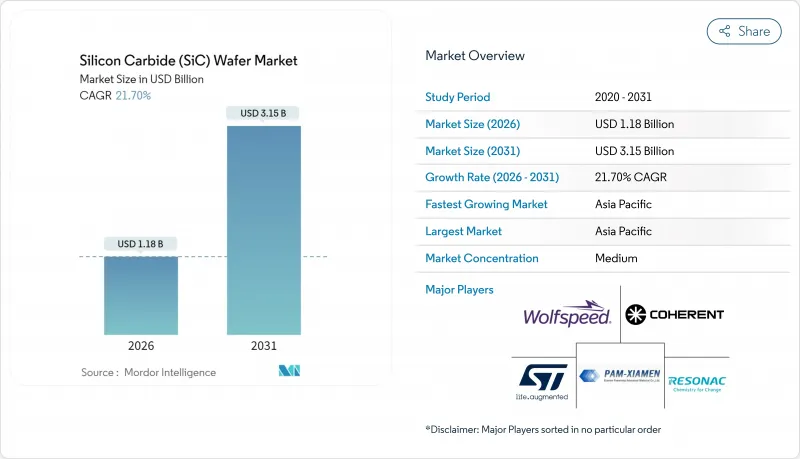

2026年の炭化ケイ素ウエハー市場規模は11億8,000万米ドルと推定され、2025年の9億7,000万米ドルから成長し、2031年には31億5,000万米ドルに達すると予測されています。

2026年から2031年にかけてはCAGR21.7%で拡大する見込みです。

この成長軌道は、自動車業界における800V車両プラットフォームへの移行、産業用パワーエレクトロニクス分野でのワイドバンドギャップ素子の採用拡大、ならびに新規製造ラインを支援する政府の優遇措置によって支えられています。結晶成長の歩留まりが着実に改善していること、8インチ基板の供給拡大、効率的な急速充電インフラへの需要増加が、さらなる拡大を後押ししています。2024年時点でアジア太平洋地域が最大のシェアを占めており、その垂直統合型エコシステムは上流・下流投資を引き続き誘致しています。資本集約度は依然として主要な競争フィルターですが、欠陥低減、ウエハーの微細化、内部サプライチェーンを掌握した企業は、高温・高周波動作環境において従来のシリコンを凌駕する炭化ケイ素ウエハー市場の次なる需要波を捉える態勢を整えています。

世界の炭化ケイ素(SiC)ウエハー市場の動向と洞察

EV普及率の上昇と800V車両プラットフォームへの移行

自動車メーカーは、テスラのモデルSプレイド、ヒュンダイのIONIQ 5、キアのEV6などのモデルを通じて、大規模な800Vシステムの採用を実証しました。これらの高電圧アーキテクチャは充電時間を20分以下に大幅に短縮しましたが、高熱・高電気ストレスに耐えられるパワーMOSFETを必要としました。炭化ケイ素は、シリコンに比べて10倍の耐電界強度と3倍の熱伝導率を有するため、これらの要件を満たし、駆動用インバーターや車載充電器における需要を拡大させています。高級車セグメントが最初にこの技術を採用しましたが、ウエハーコストの低下とサプライチェーンの成熟により、現在では主流のEVプラットフォームへの普及が加速しており、次世代モビリティの重要な基盤技術として炭化ケイ素ウエハー市場の重要性を高めています。

800V充電インフラの急速な拡充

充電ネットワーク事業者は、350kWステーションにおける変換損失を最小化するため、炭化ケイ素を選択しました。エレクトリファイ・アメリカの主要拠点では、SiCベースの整流器とDC-DCモジュールを統合し、シリコンと比較して高い電力密度と低い放熱を実現しています。欧州の回廊プロバイダーであるIONITYも同様の道筋をたどり、自動車メーカーが800Vプラットフォームを採用するよう促す需給の好循環を生み出しました。その結果、車両、充電器、グリッド接続機器にまたがるエコシステムが形成され、ウエハーの需要量が増加すると同時に、エネルギー効率の向上によるコスト削減を通じて、ネットワーク事業者の総所有コスト(TCO)が圧縮されています。

200mm基板の供給制約

200mmブールの結晶成長サイクルは200時間を超えることが多く、150mm相当品よりも欠陥密度が高いため、自動車グレード基板の供給が制約されておりました。歩留まり低下がウエハーの平均販売価格(ASP)を押し上げ、大径化への設計移行を遅らせました。メーカーは先進的なインサイチュ監視技術や種結晶の最適化に投資してこの差を埋めていますが、特に厳しい品質基準を要求する自動車メーカー向けにおいて、短期的には供給不足がカーバイドシリコンウエハーの市場出荷成長を抑制し続けています。

セグメント分析

2025年のシリコンカーバイドウエハー市場では、6インチウエハーが53.75%のシェアを占めました。ウエハー当たりのデバイス数とダイ当たりの減価償却費が、この従来型径を量産基準として位置づけています。しかしながら、8インチウエハーは2031年までに28.6%のCAGRで拡大すると予測されており、トラクションインバーターやPVインバーターにおけるアンペア当たりのコスト優位性を裏付けています。設備投資額は依然として高額です。200mm結晶用高PVT炉の価格は1,500万~2,000万米ドルであるのに対し、6インチ用は800万~1,200万米ドルです。しかしながら、8インチウエハー1枚あたりのダイ生産量は最大2.2倍に達し、歩留まり向上に伴いコスト曲線が引き締まります。スケールメリットが顕在化するにつれ、8インチ基板のシリコンカーバイドウエハー市場規模はますます大きな収益源となる見込みです。

2024年時点では歩留まりが6インチ相当品より15~20%低かったもの、加熱ゾーン設計の最適化や欠陥低減分析への投資により差は縮小しました。自動車および再生可能エネルギー統合企業は200mmウエハーの認定プログラムを開始し、量産供給が安定次第、より広範な採用が進むことを示唆しています。4インチ未満のフォーマットは、研究開発が高電圧自動車用またはグリッドモジュールへ移行するにつれ減少を続け、一方12インチを超えるプロトタイプは学術分野に限定されたままでした。したがって、8インチへのスケールアップの成功は、シリコンカーバイドウエハー市場にとって極めて重要な転換点となります。

2025年における炭化ケイ素ウエハー市場シェアの68.12%をN型導電性ウエハーが占めました。その低抵抗率と安定したドーパントプロファイルにより、パワーMOSFET、ダイオード、ショットキー素子に不可欠な存在となっております。半絶縁基板は、従来ニッチな存在でしたが、5G基地局、レーダー、衛星ペイロードにおけるRFおよびマイクロ波の採用を背景に、2031年までに23.6%のCAGR成長が見込まれています。ネットワークの高度化と防衛電子機器分野では、ギガヘルツ周波数帯における寄生容量を抑制するため、純度が高く電気的に絶縁された格子構造が求められており、半絶縁材料向けシリコンカーバイドウエハー市場の規模は拡大する見込みです。

メーカー各社は、より大径化に伴う抵抗率の均一性を高めるため、成長後アニール処理および補償ドーピング技術の改良を継続しております。航空宇宙および通信企業は、優れた熱処理性能を発揮するGaN-on-SiC HEMT向けに半絶縁性ウエハーを好んで採用しています。その結果、高い熱伝導率、電気的絶縁性、優れたRF性能を保証するウエハーの価値が競合情勢においてますます重視されるようになっています。この動向は、次世代デバイスアーキテクチャの進化において、半絶縁性シリコンカーバイドが重要な役割を担うことを浮き彫りにしています。

シリコンカーバイド(SiC)ウエハー市場は、ウエハー径(4インチ未満、4インチ以上)、導電タイプ(N型導電、半絶縁)、用途別(パワーエレクトロニクス、RFデバイスなど)、最終用途産業別(自動車・電気自動車、再生可能エネルギー・蓄電など)、結晶成長技術別(PVT、CVDなど)、地域別に分類されます。市場予測は金額ベース(米ドル)で提供されます。

地域別分析

北米は、リショアリング優遇措置と深いEVエコシステムに支えられ、第2位となりました。Wolfspeed社のモホークバレー工場では200mmウエハーの量産が開始され、テスラ社は大型SiCトラクションインバーターの検証を実施したことで、地域的な供給契約が促進されました。オンセミはチェコ共和国におけるSiCのエンドツーエンド生産体制構築に向け、最大20億米ドルを投資することを決定しました。これにより欧州自動車メーカーに選択肢を提供しつつ、米国における技術リーダーシップを維持します。一方、ロームとSKシルトロンは高品質基板の生産を通じ、価格下落圧力にもかかわらず高価格を維持する技術的優位性を保っています。

北米はリショアリング優遇策と充実したEVエコシステムを背景に第2位を維持しました。ウルフスピード社のモホークバレー工場では200mmウエハーの量産が開始され、テスラ社による大規模SiCトラクションインバーターの検証が地域の供給契約を促進しました。オンセミコンダクター社はチェコ共和国におけるSiCのエンドツーエンド生産体制構築に最大20億米ドルを投資し、欧州自動車メーカーに選択肢を提供しつつ米国の技術的優位性を維持しています。

欧州はグリーンディールによる電動化政策と強固な自動車基盤を背景に進展しました。インフィニオンはオーストリアとドイツでウエハー生産を拡大し、ポルシェおよびアウディの800Vプラットフォームに対応。最低コストよりも品質と信頼性を重視しました。STマイクロエレクトロニクスはカターニア工場を拡張し、EUの半導体自給目標に沿った地域サプライチェーンの基盤を確立。シリコンカーバイドウエハー市場は価格感応度が高い状態が続きましたが、欧州の買い手は自動車グレードのトレーサビリティと厳格な欠陥仕様を重視しました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 電気自動車の普及拡大と800V車両プラットフォームへの移行

- 800V充電インフラの急速な整備

- SiCのSiに対する高温・高周波性能上の優位性

- ワイドバンドギャップファブに対する政府の優遇措置

- 中国における垂直統合型SiCサプライチェーンの台頭

- 欠陥密度を低減する革新的な200mmバルク成長技術の進展

- 市場抑制要因

- 200mm基板の供給制限

- パッケージングに起因する熱機械的応力

- 資本集約的な結晶成長装置

- SiC切削屑のリサイクル課題

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- マクロ経済要因の影響

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- ウエハー径別

- 4インチ未満

- 6インチ

- 8インチ

- 12インチ以上

- 導電率タイプ別

- N型導電性

- 半絶縁

- 用途別

- パワーエレクトロニクス

- 高周波デバイス

- 光電子工学およびLED

- その他の用途

- 最終用途産業別

- 自動車および電気自動車

- 再生可能エネルギーとエネルギー貯蔵

- 電気通信

- 産業用モーター駆動装置および無停電電源装置(UPS)

- 航空宇宙・防衛

- その他のエンドユーザー産業

- 結晶成長技術別

- 物理蒸気輸送(PVT)

- 化学気相成長法(CVD)

- 改良型レリー昇華法

- その他の技術

- 地域別

- 北米

- 米国

- カナダ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- 韓国

- 台湾

- インド

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Wolfspeed Inc.

- Coherent Corp.

- Xiamen Powerway Advanced Material Co., Ltd.

- STMicroelectronics N.V.

- Resonac Holdings Corporation

- Atecom Technology Co., Ltd.

- SK Siltron Co., Ltd.

- SiCrystal GmbH

- Tankeblue Semiconductor Co., Ltd.

- Semiconductor Wafer Inc.

- GlobalWafers Co., Ltd.

- Sanan Optoelectronics Co., Ltd.

- ROHM Co., Ltd.

- Infineon Technologies AG

- onsemi Corporation

- Mitsubishi Electric Corporation

- Hebei Synlight Crystal Co., Ltd.

- Guangdong TySiC Semiconductor Co., Ltd.

- EpiWorld International Co., Ltd.

- Hench Semiconductor Co., Ltd.

- TYSTC Semiconductor Co., Ltd.

- ProChip Moissic Technologies Inc.

- Dow Silicon Carbide LLC

- Fraunhofer IISB(SiC Foundry)

- Nippon Steel & Sumitomo Metal SiC Materials Co., Ltd.

- LPE S.p.A.

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日