|

市場調査レポート

商品コード

1910931

インドの紙と板紙包装市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)India Paper And Paperboard Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドの紙と板紙包装市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 134 Pages

納期: 2~3営業日

|

概要

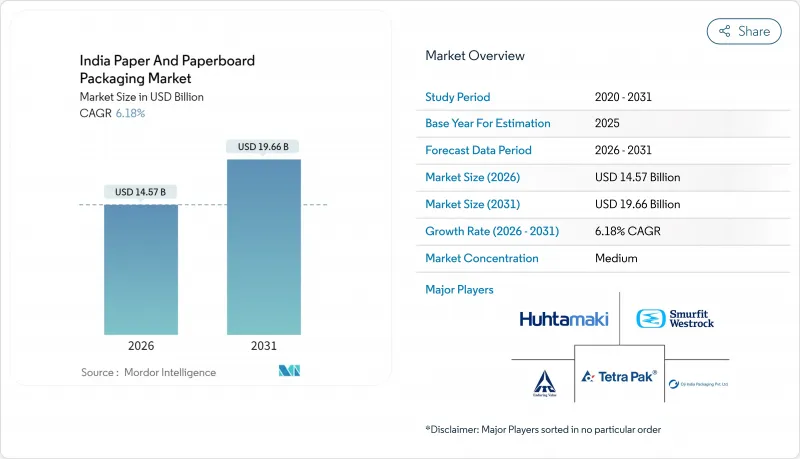

2026年のインドの紙と板紙包装市場の規模は145億7,000万米ドルと推定され、2025年の137億2,000万米ドルから成長が見込まれます。

2031年までの予測では196億6,000万米ドルに達し、2026~2031年にかけてCAGR6.18%で拡大する展望です。

需要の勢いは、全国的な使い捨てプラスチックからの移行、電子商取引物流の急速な拡大、循環型経済包装へのブランドコミットメントを反映しています。オンライン小売では耐衝撃性がありながら軽量な輸送形態が求められるため、段ボール箱が主流を占めています。一方、液体用カートンは高級飲料の成長と無菌充填への投資の恩恵を受けています。飲食品ブランドはリサイクル可能な単一材料包装の採用を加速させており、第一線都市と第二線都市におけるクイックコマース拠点の拡大により、小型二次包装の潜在市場が拡大しています。供給面では、再生繊維の生産能力、農業残渣パルプライン、高速フレキソ印刷機の拡充が進んでいますが、エネルギー価格の上昇や輸入古紙価格の変動により、利益率への圧力は継続しています。

インドの紙と板紙包装市場の動向と展望

電子商取引における段ボール需要の増加

注文量の急増と、最大35kgまで許可されたクイックコマースの重量物配送により、コンバータはラストマイル効率化のため強度と坪量を両立した段ボール設計を追求しています。フリップカートのプラスチック緩衝材廃止方針により、既に数百万個の小包が紙ベース包装へ転換されました。アダニ・ウィルマーなどのFMCGサプライヤーはオンラインチャネル向けに大型SKUを導入し、段ボール使用量の増加を促進しています。バンガロールとデリーの地域ハブネットワークは補充を迅速化しますが、同時に接触点を増やし、ブランド価値を維持する高印刷グラフィックへの需要を拡大しています。その結果、段ボールメーカーはインラインフレキソフォルダーやデジタル印刷モジュールを導入し、準備時間の短縮と廃棄物の削減を図っています。したがって、インドの紙と板紙包装市場は、電子商取引の浸透と材料中立の持続可能性要件が交差する点から構造的な上昇効果を得ています。

食品ブランドの再生可能単一材料包装への移行

都市部の消費者が包装ラベルの廃棄時性能を精査する中、リサイクル可能性が購買決定要因となりました。大手食品加工業者は、多層プラスチックを使用せずに油脂・湿気バリア機能を実現する水性またはバイオポリマーコーティングを施した単一基材板紙へのラミネート再設計を進めています。フータマキ社とインド産業連盟の提携により、単一材料形態が機械的リサイクルプロセスをいかに容易にするかを明示したオープンソース設計ガイドが作成されました。ブランドオーナーが2026年に強化される拡大生産者責任(EPR)目標の達成を目指す中、繊維の純度とトレーサビリティを保証できるベンダーが優先されます。コーティング化学はインラインで大規模に適用可能なため、コンバータは利益率とスピードの両面で優位性を獲得し、インドの紙と板紙包装市場における長期的な追い風を強化しています。

輸入古紙の価格変動性

インドでは再生板紙原料の約30%を海上輸送による再生繊維に依存しており、輸送障害や入札競争がスポット価格を押し上げ、製紙工場の利益率を圧迫しています。インド製紙工業会は中国・チリからの多層板紙輸入に対し、価格破壊を理由に関税賦課を要請しました。JKペーパーの2024年度利益58%減は、コスト急騰が収益に直結する実例です。2025年半ばには北米の新パルプラインが世界価格を抑制しましたが、為替変動と紅海航路リスクにより変動性は高止まりし、インドの紙と板紙包装市場の短期成長ペースを鈍化させています。

セグメント分析

段ボール原紙は2025年の売上高の48.23%を占め、緩衝性とパレット効率を重視するECフルフィルメントセンターに支えられています。液体用カートンは規模こそ小さいも、高級乳製品ジュース・無菌調理食品ソリューションを背景にCAGR7.28%が見込まれています。段ボール用グレードのインド紙と板紙包装市場規模は、切り替えコストを低減するインライン印刷・ダイカット技術への投資を原動力に、2026~2031年にかけてさらに22億9,000万米ドル増加すると予測されています。テトラパック社の画期的な5% ISCC PLUS認証再生ポリマー層導入を契機に、UFlexなどの液体用カートン大手は年間生産量を120億パックに拡大する計画です。一方、折り畳み式カートンは、単一材料ガイドラインに適合する水性バリアコートによる改良により、消費財セグメントでの安定した基盤を維持しています。特殊板紙と成形繊維は、ニッチな保護要件と環境配慮型ブランディングを背景に、原料価格変動を緩和するプレミアム価格差を確保しています。

競合という観点では、ITCのような大手グループは農林業から完成板紙までの全プロセスを管理しており、原料のヘッジングと製品開発サイクルの短縮を可能にしています。これに対し、段ボールメーカーはデジタル市場に近い場所に印刷プロセスを配置し、即日での箱補充を実現することで対応しています。インドの紙と板紙包装市場が超ローカル配送へと移行する中、これは運営上の優位性となっています。

飲食品ブランドは、厳格な衛生基準と拡大するコールドチェーンにより、2025年に売上高の39.35%を占めました。一方、パーソナルケア・化粧品セグメントは7.72%のCAGR予測で高い成長率を示しています。フードサービス産業では、ファストフード店が再生繊維とPLA分散体で作られた耐油性クラムシェル容器を採用し、使い捨てプラスチック禁止令に対応しています。パーソナルケア製品のインド紙と板紙包装市場規模は、高級ブランドがプラスチック容器から硬質紙管やオフセット印刷スリーブへ移行する動きを受け、2031年までに5億6,800万米ドルの成長が見込まれます。

医療セグメントでは、国内製薬生産量の増加に伴い、ブリスター包装用裏地や医療用カートンの需要が安定しています。電子機器メーカーは静電気防止繊維トレイを求めつつも、発泡材との機能的同等性を考慮したコスト比較により、急激な成長は抑制されています。産業用・自動車部品セグメントでは、多層段ボール箱が「メイクインインディア」施策による調達拡大と相まって、幅広い最終用途セグメントでバランスの取れた収益基盤を確保しています。

その他の特典

- エクセル形態の市場予測(ME)シート

- アナリストサポート(3ヶ月間)

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 電子商取引の拡大に伴う段ボール需要の増加

- 食品ブランドの再生可能単一材料包装への移行

- 使い捨てプラスチック製品に対する政府の禁止措置

- クイックコマース地域拠点の台頭

- 自動化高速フレキソ印刷への投資

- 農業残渣パルプの生産能力増強

- 市場抑制要因

- 輸入古紙の価格変動性

- 慢性的なコンテナボードのエネルギーコスト上昇

- 中小コンバータ向けGST還付の遅延

- 請求書発行と出版におけるデジタル代替

- 産業サプライチェーン分析

- 規制情勢

- 技術の展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 産業間の競争

第5章 市場規模と成長予測

- 製品タイプ別

- 折り畳み式段ボール箱

- 段ボール包装

- 液体用カートン

- その他

- エンドユーザー産業別

- 飲食品

- 医療医薬品

- パーソナルケア・化粧品

- 電気・電子機器

- 工業・自動車

- 包装形態別

- 一次小売包装

- 二次輸送用包装

- 棚出し可能/ディスプレイ用包装

- 保護用インサートと緩衝材

- 材料グレード別

- バージンパルプ

- 再生繊維

- ハイブリッド/混合繊維

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- TCPL Packaging Limited

- Parksons Packaging Limited

- Smurfit WestRock plc

- KCL Limited

- Borkar Packaging Private Limited

- Canpac Trends Private Limited

- Trident Paper Box Industries

- Tetra-Pak India Private Limited

- UFlex Ltd

- Oji India Packaging Private Limited

- ITC Limited-Paperboards and Specialty Papers Division

- JK Paper Limited

- Horizon Packs Private Limited

- Astron Packaging Limited

- A N Y Graphics Private Limited

- Meghna Packaging Private Limited

- GPA Global India

- Huhtamaki India Limited

- Mayur Uniquoters Limited