貨物用航空機:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Freighter Aircraft - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 136 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690086

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

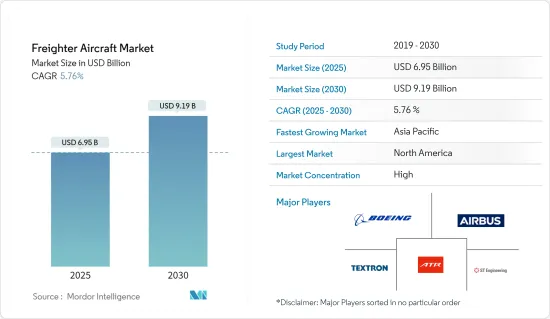

貨物用航空機の市場規模は2025年に69億5,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは5.76%で、2030年には91億9,000万米ドルに達すると予測されます。

各国間の新たな貿易関係の増加と世界のeコマース活動の急成長が、主に貨物用航空機市場の需要を牽引しています。また、航空貨物需要の増加も、世界の貨物用航空機の需要拡大につながります。

世界的に、各国政府はより円滑な貨物輸送を確保するために様々な規則や政策を策定しています。一部の貨物用航空機運航会社はガイドラインを遵守しているが、多くの会社はまだ遵守する必要があり、予測期間中に貨物用航空機運航の妨げになる可能性があります。また、デジタル化と持続可能性への注目の高まり、オムニチャネルとしての航空貨物、貨物用航空機容量の増加、委託価格の上昇といった最新の動向も、市場の成長を後押しすると予想されます。

貨物用航空機の市場動向

予測期間中、非貨物用航空機セグメントの派生型が最も高い成長を記録すると予測される

非貨物用航空機の派生セグメントは、予測期間中に最も高い成長を示すと予想されます。この成長は、航空貨物量の増加に対応するため、航空会社が古い旅客機を貨物用航空機に改造・更新することを好む傾向が高まっているためと予想されます。旅客機から貨物用航空機への改造の増加は、eコマース事業による需要の増加により、航空貨物容量の制約に対するソリューションとして機能すると予想されます。改造された旅客機は、eコマース・パッケージのような、より軽量でよりボリュームのある貨物を運ぶことになります。このような改造の際には、航空機の換気、火災検知、温度制御システムに変更が加えられます。これは、貨物用航空機には旅客機とは異なる要件があり、他の基準に準拠しなければならないためです。

旅客機から貨物用航空機への転換(P2F)を行う主な航空機プログラムには、ボーイングB757、B737、エアバスA321、A320などがあります。新たな貨物用航空機に対する需要の高まりを受けて、アストラル・アビエーションは、史上初のエアバスA320旅客機から貨物用航空機(P2F)への改造機を運航すると発表しました。IAIはまた、2024年に韓国の仁川空港に、ボーイングB777を改造するための新施設をシャープ・テクニクスとともに開設する予定です。このような世界の開発は、今後数年間の市場の成長を促進すると予想されます。

アジア太平洋地域は予測期間中に目覚ましい成長を見せる見込み

アジア太平洋地域は、今後数年間で最も高いCAGRで推移すると予想されます。航空貨物需要の高まりは、主にこの地域のeコマース需要の増加によるものです。中国、インド、日本、カンボジア、ベトナムでは、オンラインショッピングの嗜好が高まっており、電子機器システムやその他の商業製品の生産設備が市場の成長を牽引しています。

中国国内航空市場はナローボディ機の需要を牽引し、貨物用航空機運航のためにナローボディ機がより普及しています。旅客輸送量の増加と世界の航空輸送量の回復が予想されることから、航空機の相手先商標製品メーカー(OEM)は、今後数年間に予想される需要増に対応するため、航空機を調達する態勢を整えています。例えば、2023年5月、成都を拠点とする四川航空は、同社初のエアバスA330-300旅客機から貨物用航空機への転換(P2F)を受け、貨物用航空機を4機に増やしました。

この地域のeコマース企業は、高い都市密度、新興経済諸国、技術に精通した顧客から恩恵を受け、地域全体のeコマース市場をさらに引き付けています。成田国際空港は、国際貨物を最も多く取り扱う日本の空港です。例えば、2023年5月、JALはボーイングB767-300ER型機3機を旅客機から離陸させ、メインデッキに大型コンテナを搭載できる純粋な貨物用航空機に改造するため、機体のオーバーホール施設に送ると発表しました。このように、貨物用航空機に対する需要の高まりと航空貨物輸送の増加は、アジア太平洋全域で市場の成長を後押ししています。

貨物用航空機産業の概要

貨物用航空機市場は統合されており、航空機OEM、OEMと協力協定を結ぶ第三者請負業者または独立企業、および第三者請負業者が独自に改造ソリューションを開発しています。ボーイング社、エアバスSE、ATR、シンガポール・テクノロジーズ・エンジニアリング社、テキストロン社が市場の有力プレーヤーです。

2021年11月、エアバスはエア・リース・コーポレーションから7機を受注し、A350貨物用航空機プログラムを開始しました。2021年12月には、CMA CGMエアカーゴ、エールフランス、シンガポール航空の3社がA350Fを発注しました。航空機の納入は予測期間中に予定されています。ボーイング、シンガポール・テクノロジーズ・エンジニアリング、IAI、プレシジョン・エアクラフト・ソリューションなどの企業が、コンバージョンサービスを提供しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 航空機タイプ

- 貨物機

- 非貨物機の派生型

- エンジンタイプ

- ターボプロップ機

- ターボファン機

- 地域

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- トルコ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- The Boeing Company

- Airbus SE

- Textron Inc.

- ATR

- Air Transport Services Group Inc.

- KF Aerospace

- Singapore Technologies Engineering Ltd

- Aeronautical Engineers Inc.

- Precision Aircraft Solutions

- Israel Aerospace Industries Ltd

第7章 市場機会と今後の動向

目次

The Freighter Aircraft Market size is estimated at USD 6.95 billion in 2025, and is expected to reach USD 9.19 billion by 2030, at a CAGR of 5.76% during the forecast period (2025-2030).

The rise in new trade relationships among countries and rapid growth in global e-commerce activities primarily drive the freighter aircraft market's demand. The increased demand for air cargo also leads to a growing demand for freighter aircraft worldwide.

Globally, governments have formed various rules or policies to ensure smoother freighter operations. Although some freighter operators have adhered to the guidelines, many still need to comply, which can hamper freighter operations during the forecast period. The latest trends, such as an increasing focus on digitization and sustainability, air freight as an omnichannel, increasing freighter aircraft capacity, and increasing the price of consignment, are also expected to boost market growth.

Freighter Aircraft Market Trends

The Derivative of the Non-cargo Aircraft Segment is Anticipated to Register the Highest Growth during the Forecast Period

The derivative of the non-cargo aircraft segment is expected to showcase the highest growth during the forecast period. The growth is anticipated due to the rising preference of airlines to modify and update their old passenger aircraft with freighter aircraft to meet the rising volume of air cargo. Increasing passenger-to-freighter conversions is expected to act as a solution for the air cargo capacity constraints due to the increased demand driven by the e-commerce business. The converted passenger aircraft will carry lighter, more voluminous cargo like e-commerce packages. During such conversions, changes are made to the aircraft's ventilation, fire detection, and temperature control systems because the freighter aircraft have different requirements than passenger aircraft and must comply with other standards.

Some major passenger-to-freighter (P2F) aircraft programs are Boeing B757, B737, and Airbus A321 and A320. Due to the increased demand for new freighters, Astral Aviation announced it would operate the first-ever Airbus A320 passenger-to-freighter (P2F) converted aircraft. IAI also plans to open a new facility with Sharp Technics at South Korea's Incheon Airport in 2024 to convert Boeing B777s. Such developments worldwide are expected to drive the market's growth in the coming years.

Asia-Pacific is Expected to Showcase Remarkable Growth during the Forecast Period

Asia-Pacific is expected to record the highest CAGR in the coming years. The rising demand for air cargo is mainly due to the region's increasing e-commerce demand. The growing preference for online shopping and production facilities for electronics systems and other commercial goods in China, India, Japan, Cambodia, and Vietnam drives the market's growth.

The Chinese domestic aviation market drives the demand for narrow-body aircraft, making them more prevalent for freighter operations. Rising passenger traffic and the expected revival in global air traffic have poised aircraft original equipment manufacturers (OEMs) to procure aircraft in their fleet to meet the anticipated rising demand in coming years. For instance, in May 2023, Chengdu-based Sichuan Airlines received its first Airbus A330-300 passenger-to-freighter (P2F) conversion to increase its cargo fleet to four aircraft.

E-commerce companies in the region benefit from high urban density, a developed economy, and technically savvy customers, further attracting the e-commerce market across the region. Narita International Airport was the Japanese airport handling the most international freight. For instance, in May 2023, JAL announced that it would launch three Boeing B767-300ER aircraft from its passenger fleet and send them to an airframe overhaul facility for conversion into pure freighters that can carry large containers on the main deck. Thus, growing demand for freighters and rising air cargo transportation boost the market's growth across Asia-Pacific.

Freighter Aircraft Industry Overview

The freighter aircraft market is consolidated, with aircraft OEMs, third-party contractors or independent companies that enter cooperation agreements with OEMs, and third-party contractors developing their conversion solutions independently. The Boeing Company, Airbus SE, ATR, Singapore Technologies Engineering Ltd, and Textron Inc. are prominent players in the market.

In November 2021, Airbus launched the A350 Freighter program with a seven-aircraft order from Air Lease Corporation. In December 2021, three airlines, including CMA CGM Air Cargo, Air France, and Singapore Airlines, placed orders for the A350F. The aircraft's deliveries are scheduled during the forecast period. Companies like Boeing, Singapore Technologies Engineering Ltd, IAI, and Precision Aircraft Solution are additional players providing conversion services.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Aircraft Type

- 5.1.1 Dedicated Cargo Aircraft

- 5.1.2 Derivative of Non-cargo Aircraft

- 5.2 Engine Type

- 5.2.1 Turboprop Aircraft

- 5.2.2 Turbofan Aircraft

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Turkey

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 The Boeing Company

- 6.2.2 Airbus SE

- 6.2.3 Textron Inc.

- 6.2.4 ATR

- 6.2.5 Air Transport Services Group Inc.

- 6.2.6 KF Aerospace

- 6.2.7 Singapore Technologies Engineering Ltd

- 6.2.8 Aeronautical Engineers Inc.

- 6.2.9 Precision Aircraft Solutions

- 6.2.10 Israel Aerospace Industries Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 136 Pages

- 納期

- 2~3営業日