|

市場調査レポート

商品コード

1406208

アメリカの貨物機:市場シェア分析、産業動向と統計、2024~2029年の成長予測America Freighter Aircraft - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アメリカの貨物機:市場シェア分析、産業動向と統計、2024~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 75 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

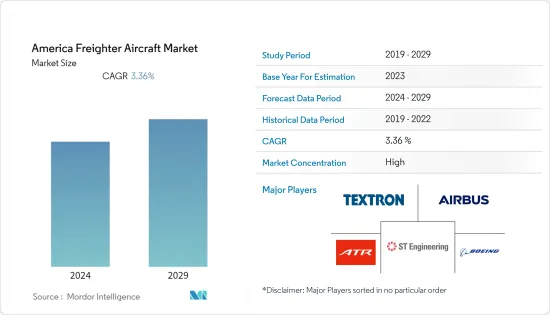

アメリカの貨物機市場は、2024年に37億2,000万米ドルと評価され、予測期間中のCAGRは3.36%を記録し、2029年には43億8,000万米ドルに達すると予測されています。

貨物機または貨物専用機は、旅客ではなく貨物の輸送用に設計または改造された固定翼機です。このような航空機には通常、旅客用の設備は組み込まれておらず、一般的に貨物を搭載するための1つまたは複数の大型ドアを備えています。貨物機は、民間の旅客航空会社や貨物航空会社、個人、または各国の軍隊によって運航されています。

アメリカ地域における貨物機需要の増加につながる航空貨物需要の増加と、各国間の貿易関係の増加が、予測期間中に貨物機市場が大きく成長する主な要因です。旅客機から貨物機への転換の増加は、eコマース事業が牽引する大きな需要により、航空貨物のキャパシティ制約の解決策として機能すると予想されます。

一方、規制の増加は長期的には市場の妨げになると思われます。より円滑な貨物輸送を確保するため、地域全体の様々な政府によって様々な規制や政策が策定されています。一部の貨物機運航会社はこの政策を遵守しているが、まだ多くの貨物機運航会社がこの政策を遵守する必要があり、これが予測期間中の貨物機運航の妨げにつながる可能性があります。

アメリカの貨物機市場動向

予測期間中、非貨物機の派生で大きな成長が見込まれる

非貨物機の派生機は、予測期間中にアメリカの貨物機市場で大きな成長を示すと思われます。この成長は、航空会社が老朽化した旅客機を貨物機に変更することを好むようになっていることに起因しています。旅客機から貨物機への改造の増加は、eコマース事業が牽引する大きな需要による航空貨物容量の制約に対するソリューションとして機能します。これらの改造旅客機は、eコマース・パッケージのような、より軽量でよりボリュームのある貨物を運ぶことになります。このような改造の際、航空機は貨物の重量に対応できる床で補強されます。

さらに、航空機の火災検知、換気、温度制御システムにも変更が加えられます。これは、貨物機には旅客機とは異なる要件があり、異なる基準に準拠する必要があるためです。旅客機から貨物機へ(P2F)利用可能な航空機プログラムには、B737、B757、A320、A321などがあります。例えば、カナダの貨物航空会社カーゴジェットは、8機のボーイングB777旅客機に投資し、純粋な貨物構成に変更する予定です。米国の改造会社マンモス・フリーターズは、貨物航空会社カーゴジェット航空(W8)のために、ボーイングB777-200LR改造プロジェクトのプロトタイプに取り組んでいます。これらの航空機の納入は、2023年から2025年の間に予定されています。このように、航空貨物需要の増加による旅客機から貨物機への転換投資の増加が、市場の成長を牽引しています。

予測期間中、米国が市場を独占

米国は同市場で最も高いシェアを占めており、予測期間中もその支配が続く。この成長は、多数の航空機貨物フリートが存在し、航空部門への支出が増加していることによります。充実した航空部門の存在、航空会社と空港の数の増加、航空貨物輸送の需要の増加が、同国全体の市場成長を牽引しています。

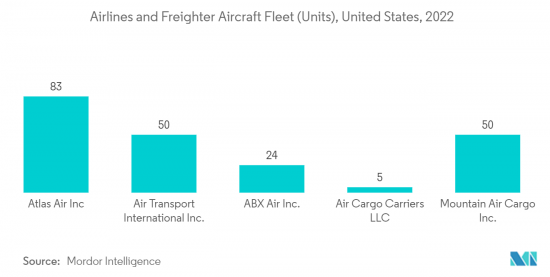

北米の航空会社は、2022年の需要が2021年比で5.1%減少し、キャパシティは4.2%増加しました。航空貨物の需要は2019年比で13.7%増加し、キャパシティは8.2%増加しました。米国と中国の貿易摩擦は2019年、北米の航空会社に大きな打撃を与えました。2021年、IATAはフェデラルエクスプレス(フェデックス)が世界最大の貨物航空会社と発表し、2020年の196億6,000万CTKを5.1%上回る207億CTK(貨物トンキロ)を記録しました。現在、同社は8つの異なる機種からなる697機の航空機を運航しています。

貨物輸送能力の高い先進的な貨物機の調達が増加し、米国の航空会社から旅客機から貨物機への転換の契約が増加していることが、市場の成長を後押ししています。例えば、米国最大の貨物航空会社であるフェデックスは、2023年に2機のボーイングB777貨物機を引き渡し、2024年から2025年にかけてさらに6機のB777Fを配備する計画です。また、2023年にはボーイングB767-300型貨物機を14機受領し、2024年から2025年にかけてさらに24機のB767F型貨物機を配備する計画です。さらにフェデックスは、短距離路線用に新型のATR 72-600F型機を配備し、老朽化したATR-42型機をセスナ・スカイクーリエ408型貨物機に置き換えることで、燃料効率の向上を図る計画です。このような市場開拓は、おそらくアメリカ全土の市場成長を牽引すると見込まれています。

アメリカの貨物機産業の概要

アメリカの貨物機市場は、少数の世界のプレーヤーが市場で大きなシェアを占めており、その性質上、統合されています。同市場における著名なプレーヤーには、ボーイング社、エアバスSE、テキストロン社、ATR、シンガポール・テクノロジーズ・エンジニアリング社などがあります。主なOEMによる旅客機から貨物機への転換への支出の増加と、貨物航空会社向けの高度なソリューションの開発の高まりが、市場の成長を牽引しています。航空貨物業界からの需要増加に対応するため、市場の主なプレーヤーは、より燃料効率の高い新世代の貨物機の開発に投資しています。例えば、ボーイング社は2022年に、100機目の契約機737-800ボーイング転換貨物機を引き渡しました。この貨物機は2022年9月にエアキャップ・カーゴに引き渡されました。それに加え、エアバスSEは、A300-600の設計をベースとしたBelugaST「Super-Transporter」航空機を導入し、世界中の顧客にアウトサイズ貨物輸送を提供します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 航空機タイプ

- 貨物専用機

- 非貨物専用機の派生型

- エンジンタイプ

- ターボプロップ機

- ターボファン機

- 地域

- 北米

- 米国

- カナダ

- ラテンアメリカ

- ブラジル

- メキシコ

- その他のラテンアメリカ

- 北米

第6章 競合情勢

- 企業プロファイル

- Airbus SE

- ATR

- The Boeing Company

- Textron Inc.

- Air Transport Services Group, Inc.

- Aeronautical Engineers Inc.

- KF Aerospace

- Singapore Technologies Engineering Ltd.

- IAI

- Precision Aircraft Solutions

第7章 市場機会と今後の動向

The American freighter aircraft market was valued at USD 3.72 billion in 2024 and is expected to reach 4.38 billion by 2029, registering a CAGR of 3.36% during the forecast period.

A cargo aircraft or a freighter aircraft is a fixed-wing aircraft that is designed or converted for the carriage of cargo rather than passengers. Such aircraft usually do not incorporate passenger amenities and generally feature one or more large doors for loading cargo. Freighters may be operated by civil passenger or cargo airlines, by private individuals, or by the armed forces of individual countries.

The increase in the demand for air cargo leading to an increase in the demand for freighter aircraft in the American region and the increase in trade relationships among different countries are the major factors that will help the freighter aircraft market to witness significant growth during the forecast period. The increase in passenger-to-freighter conversions is expected to act as a solution for the air cargo capacity constraints due to the major demand driven by the e-commerce business.

On the other hand, increasing regulations will likely hamper the market in the long run. There are various regulations or policies that are being formed by various governments across the region to ensure smoother freighter operations. Although some freighter operators have adhered to the policies, there are many freighter operators who still need to comply with the policies, and this can lead to hampering freighter operations during the forecast period.

America Freighter Aircraft Market Trends

Derivative of Non-Cargo Aircraft Segment is Expected to Show Significant Growth During the Forecast Period

The derivative of the non-cargo aircraft segment will showcase significant growth in the American freighter aircraft market during the forecast period. The growth can be attributed to the increasing preference of airlines to modify their old and aging passenger aircraft with freighter aircraft. An increase in passenger-to-freighter conversions will act as a solution for the air cargo capacity constraints due to the major demand driven by the e-commerce business. These converted passenger planes will carry lighter, more voluminous cargo, such as e-commerce packages. During such conversions, aircraft are reinforced with floors that can handle the weight of the freight.

In addition, changes are made to the aircraft's fire detection, ventilation, and temperature control systems. This is because freighter aircraft have different requirements than passenger aircraft and must comply with different standards. Some of the available passenger-to-freighter (P2F) aircraft programs are B737, B757, A320, and A321. For instance, Cargojet, a cargo airline in Canada, invested in eight Boeing B777 passenger aircraft that will be converted to a pure cargo configuration. Mammoth Freighters, a US-based modification company, is working on its prototype Boeing B777-200LR conversion project for the cargo carrier Cargojet Airways (W8). The deliveries of these aircraft will be scheduled between 2023 and 2025. Thus, growing investment in converting passengers to freighter aircraft due to increased demand for air cargo drives the market growth.

United States Dominates the Market During the Forecast Period

The United States held the highest shares in the market and continued its domination during the forecast period. The growth is due to the presence large number of aircraft freighter fleets and growing expenditure on the aviation sector. The presence of well flourished aviation sector, the growing number of airlines and airports, and increased demand for air cargo transportation drive the growth of the market across the country.

North American air carriers witnessed a 5.1% drop in demand in 2022 compared to 2021, with a capacity increase of 4.2%. Air cargo demand was up 13.7%, and capacity was 8.2% higher compared to 2019. US-China trade tensions hard-hit the North American carriers in 2019. In 2021, IATA announced that Federal Express (FedEx) was the largest cargo airline in the world, which recorded 20.7 billion Cargo Tonne Kilometers (CTK), 5.1% ahead of the 19.66 billion CTK in 2020. Currently, the company operates 697 aircraft, which consist of eight different aircraft variants.

Rising procurement of advanced freighter aircraft with high cargo-carrying capacity and growing contracts from American airlines for passenger-to-freighter conversions drive the growth of the market. For instance, in 2023, FedEx, the largest cargo airline in the US, took delivery of two Boeing B777 freighter aircraft and plans to deploy an additional six B777F aircraft during 2024 and 2025. The company also received 14 Boeing B767-300 freighter aircraft in 2023 and plans to deploy an additional 24 B767F aircraft during 2024 and 2025. Furthermore, FedEx plans to deploy new ATR 72- 600F aircraft for shorter routes and replace its aging ATR-42 aircraft with a Cessna SkyCourier 408 cargo aircraft, which will help to improve fuel efficiency. Such development will likely drive market growth across the country.

America Freighter Aircraft Industry Overview

The American freighter aircraft market is consolidated in nature, with a presence of few global players holding significant shares in the market. Some of the prominent players in the market are The Boeing Company, Airbus SE, Textron Inc., ATR, and Singapore Technologies Engineering Ltd. Increasing expenditure on passenger to freighter conversions from key OEMs and rising development of advanced solutions for cargo airlines drive the market growth. To address the increasing demand from the air cargo industry, the key players in the market are investing in developing a newer generation of freighter aircraft that will be more fuel-efficient. For instance, in 2022, the Boeing Company delivered the 100th contracted 737-800 Boeing Converted Freighter. The freighter aircraft was delivered to AerCap Cargo in September 2022. In addition to that, Airbus SE introduced the BelugaST 'Super-Transporter' aircraft, which is based on the A300-600 design and will be used to offer outsized freight transportation for customers worldwide.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Aircraft Type

- 5.1.1 Dedicated Cargo Aircraft

- 5.1.2 Derivative of Non-Cargo Aircraft

- 5.2 Engine Type

- 5.2.1 Turboprop Aircraft

- 5.2.2 Turbofan Aircraft

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Latin America

- 5.3.2.1 Brazil

- 5.3.2.2 Mexico

- 5.3.2.3 Rest of Latin America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Airbus SE

- 6.1.2 ATR

- 6.1.3 The Boeing Company

- 6.1.4 Textron Inc.

- 6.1.5 Air Transport Services Group, Inc.

- 6.1.6 Aeronautical Engineers Inc.

- 6.1.7 KF Aerospace

- 6.1.8 Singapore Technologies Engineering Ltd.

- 6.1.9 IAI

- 6.1.10 Precision Aircraft Solutions