|

市場調査レポート

商品コード

1851215

耐放射線性エレクトロニクス:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Radiation Hardened Electronics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 耐放射線性エレクトロニクス:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月22日

発行: Mordor Intelligence

ページ情報: 英文 151 Pages

納期: 2~3営業日

|

概要

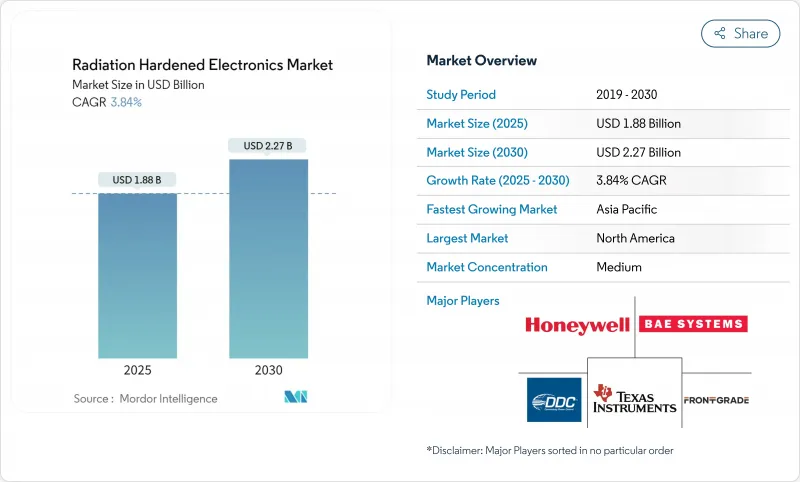

耐放射線性エレクトロニクス市場規模は2025年に18億8,000万米ドル、2030年には22億7,000万米ドルに達すると予測され、CAGRは3.84%です。

需要は引き続き、深宇宙や戦略的防衛ミッション向けの超高信頼性部品と、急増する低軌道(LEO)コンステレーションや成層圏プラットフォーム向けのコスト最適化された耐放射線デバイスとに二分されます。地政学的な要因、とりわけNATOの核近代化計画、アジアにおける原子力発電所の建設再開、小型衛星打ち上げの活発化によって、製品のロードマップと資格審査の優先順位が再形成されつつあります。商業鋳造所は、防衛関連のプライムと提携し、成熟したシリコンノードを拡張する一方で、次世代電力システム向けに窒化ガリウム(GaN)や炭化ケイ素(SiC)を統合しています。90nm未満のRHBP(Radiation-Hard-By-Process)能力におけるサプライチェーンのボトルネックは、進化する輸出規制とともに、開発サイクルを短縮し、コストを低減するRHBD(Radiation-Hard-By-Design)手法への並行的な推進を促しています。

世界の耐放射線性エレクトロニクス市場の動向と洞察

LEOおよび深宇宙衛星コンステレーションの急増

LEOメガ衛星コンステレーションは、性能目標の新たな階層化を推進している:大量生産衛星向けの30~50 krad(Si)耐性部品と、静止衛星や深宇宙衛星向けの100 krad(Si)耐性部品です。デバイスベンダーは現在、高集積化と低シールド質量を両立させた小型化GaNパワーステージなどの製品ラインを並行して運営しています。同時に、耐放射線FPGAを利用した軌道上でのリコンフィギュレーションにより、オペレータは物理的なアクセスなしにミッション・ソフトウェアを更新できるようになり、コンステレーション・ライフサイクルが延長されます。月補給衛星や火星中継衛星の受注残は堅調で、ディープスペースの需要はさらに高まっています。

NATO地域における戦略・戦術防衛エレクトロニクスの近代化

米国と欧州の防衛省は、高高度電磁パルスシナリオから重要なシステムを保護するために、信頼できる国産マイクロエレクトロニクスに資金を投入しています。2025年度米国国防総省予算では、放射線に強いRFとオプトエレクトロニクスのプロトタイプを加速するために2,488万4,000米ドルが割り当てられています。試験インフラもこれに準じている:海軍水上戦センター・クレーンの短パルス・ガンマ線施設は、1億米ドルを投じて近代化を推進し、核近代化プログラムの同時進行を可能にしています。

高い信頼性コストと長い検証サイクル

耐放射線性ASICの開発には、市販の同等品に比べ5~10倍のコストがかかります。戦略的耐放射線性エレクトロニクス協議会(Strategic Radiation-Hardened Electronics Council)は、2025年までに年間6,000時間までSEEテストビームが過剰になると予測しており、このギャップが認定待ち行列を引き延ばしています。そのため、宇宙事業者は、COTSベースの選定プロセスを合理化してリードタイムを短縮し、軌道上のライフリスクと打ち上げのタイミングとのバランスを取ることを試みています。

セグメント分析

宇宙セグメントは、2024年の耐放射線性エレクトロニクス市場の46.3%を占め、全イオン化線量と単一事象影響イミュニティの仕様ベースラインを支えています。特注のGEO宇宙船から急増するLEOコンステレーションに移行するオペレーターは、現在、低コストと迅速なリフレッシュのために弾力性の一部を交換し、より低い遮蔽質量で30krad(Si)の設計目標に適合するハイブリッド製品ラインを触媒しています。NASAのアルテミス月プログラムと商業的な太陽系ロジスティクスは、深宇宙の放射線帯に耐える100krad(Si)以上のデバイスに対する安定した需要を支えています。

高高度UAV/HAPSプラットフォームは、2030年まで4.2%の成長が予測され、航空宇宙エレクトロニクスを準宇宙放射線スペクトルに拡張します。設計者はRHBD FPGAを適応型ペイロードに活用し、ワイドバンドギャップのパワーステージを使用して厳しいエネルギー予算に対応します。このサブセグメントの耐放射線性エレクトロニクス市場規模は、6Gネットワークのバックホール試験がプロトタイプから運用フリートへと移行するにつれて拡大すると予測されます。

2024年の耐放射線性エレクトロニクス市場シェアは集積回路が31.5%を占め、ミックスドシグナルASICが複数のアナログフロントエンドと電源管理機能を1つのダイに集約してボードレベルの質量を削減しています。SEEに対応したビームタイムに関する供給リスクは、チップハウスが同一のIPブロックを2つの鋳造フローで同時に認定することを促し、継続計画を強化しています。

フィールドプログラマブルゲートアレイは、衛星オペレータが軌道上でのリコンフィギュレーションを重視する中、CAGR最速の4.6%を示しています。最新のKintex UltraScale XQRKU060クラスは、200万個のロジック・セルと、コンフィギュレーション・メモリのアップセットを緩和するオンチップ・スクラブ・コントローラを融合しています。耐放射線性エレクトロニクス市場では、FPGAが固定機能シリコンとソフトウェアのみのフォールト緩和のギャップを埋め、ディスクリートロジックからシェアを奪っています。

地域分析

北米は2024年の売上高の39.8%を占め、持続的な防衛予算とNASAの探査イニシアティブに支えられました。信頼のおける国内鋳造工場と、NSWC Craneなどの専用ビームライン設備が、認証ループを短縮し、多くの元請けサプライチェーンを支えています。月通信や小惑星探査ミッションへの宇宙商取引の多様化は、この地域の需要をさらに支えるはずです。

アジア太平洋地域は、中国、インド、韓国がロケット艦隊の規模を拡大し、新造原子炉の試運転を行うため、2030年までのCAGRが最も早く4.1%を記録します。政府の宇宙機関は、輸入部品への依存を減らすために、地元の大学と共同でRHBD設計センターに投資しています。新興の商業打ち上げプロバイダーも同様に、機敏な衛星ビジネスモデルに対応するため、耐放射線FPGAを採用しています。

欧州では、ESAの大規模なミッション・パイプラインと強力な原子力発電所の改修スケジュールが組み合わされています。NEUROSPACEイニシアチブなどのニューロモルフィック・オン・ボード・プロセッシング・プログラムは、この地域の超低消費電力コンピュートへの軸足を浮き彫りにしています。アラブ首長国連邦とサウジアラビアにある中東宇宙事務所は、火星探査機と地球観測クラスターを追求し、現地での組み立てと試験のニッチな機会を開いています。南米はまだ発展途上だが、自国製のアビオニクスを求めるブラジルとアルゼンチンの小型衛星プロジェクトから恩恵を受けています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- LEOおよびディープスペース衛星群の急増

- NATO地域における戦略・戦術防衛エレクトロニクスの近代化

- アジアと中東における原子力発電所の新設の機運

- 高高度UAVと超音速航空機のエレクトロニクス耐障害性のニーズ

- 医用画像診断における放射線許容基準の義務化(米国FDA、EU MDR)

- 宇宙船のPPUにSiC/GaNラッドハードパワーデバイスが急速に採用される

- 市場抑制要因

- 高い信頼性設計コストと長い認定サイクル

- RHBP(Rad-Hard-by-Process)ノード用の鋳造能力は90nmに制限される

- 性能トレードオフvs COTSチップ(速度、密度)

- ITAR/輸出管理サプライチェーンのボトルネック

- エコシステム分析

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- エンドユーザー別

- 宇宙

- 航空宇宙および防衛(航空、陸上、海軍)

- 原子力発電と燃料サイクル

- メディカルイメージングと放射線治療

- 高高度UAV/HAPSプラットフォーム

- 産業用粒子加速器および研究所

- コンポーネント別

- ディスクリート半導体

- センサー(光学、画像、環境)

- 集積回路(ASIC、SoC)

- マイクロコントローラおよびマイクロプロセッサ

- メモリ(SRAM、MRAM、FRAM、EEPROM)

- フィールドプログラマブルゲートアレイ(FPGA)

- パワーマネージメントIC

- 製品タイプ別

- アナログおよびミックスドシグナル

- デジタルロジック

- パワーおよびリニア

- プロセッサーとコントローラー

- 製造技術別

- ラドハードバイデザイン(RHBD)

- ラドハードバイプロセス(RHBP)

- RADハード・バイ・ソフトウェア/ファームウェア緩和

- 半導体材料別

- シリコン

- 炭化ケイ素(SiC)

- 窒化ガリウム(GaN)

- その他(InP、GaAs)

- 放射線タイプ別

- 全電離線量(TID)

- シングルイベント効果(SEE)

- 変位損傷線量(DDD)

- 中性子および陽子フルエンス

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- 南米

- 中東・アフリカ

第6章 競合情勢

- 市場集中度

- 戦略的な動き(M&A、JV、資金調達、技術ロードマップ)

- 市場シェア分析

- 企業プロファイル

- Honeywell International Inc.

- BAE Systems plc

- CAES(Cobham Advanced Electronic Solutions)

- Texas Instruments Inc.

- STMicroelectronics N.V.

- Microchip Technology Inc.

- Infineon Technologies AG

- Frontgrade Technologies

- Teledyne e2v Semiconductors

- Xilinx(RT Series, AMD)

- Renesas Electronics Corp.

- Solid State Devices Inc.

- Micropac Industries Inc.

- Everspin Technologies Inc.

- Vorago Technologies

- Analog Devices HiRel

- International Rectifier HiRel(Infineon)

- Maxwell Technologies(ES-capacitors)

- 3D Plus

- GSI Technology, Inc.