|

市場調査レポート

商品コード

1687875

APACコントラクトロジスティクス:市場シェア分析、産業動向、成長予測(2025年~2030年)APAC Contract Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| APACコントラクトロジスティクス:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

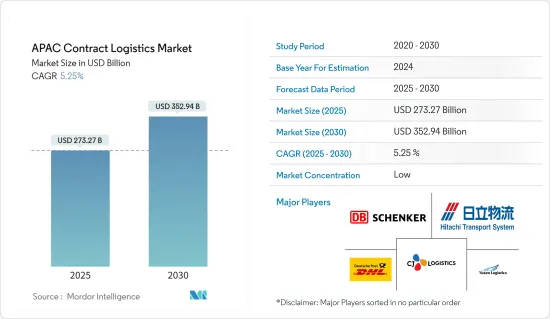

アジア太平洋のコントラクトロジスティクス市場規模は2025年に2,732億7,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは5.25%で、2030年には3,529億4,000万米ドルに達すると予測されます。

この地域が経済不安の嵐を乗り切る能力を備えていることは、より安定を求める投資家や企業にとって好ましい目的地としての地位を強化しています。地域経済統合を強化し、より大きな市場へのアクセスを提供するASEAN主導の地域包括的経済連携協定は、2022年1月に発効し、経済成長に拍車をかけると同時に、ASEAN諸国が最近の疫病から立ち直る助けとなると考えられます。

アジア太平洋は、その迅速な経済開発と盛んなビジネス環境により、この市場で最も急速に地歩を固めている地域です。アジア太平洋は欧州を抜き去り、コントラクトロジスティクスの世界市場でトップの座についた。この地域の成長の原動力となっているのは、堅調な景気拡大、小売業の制定率の上昇、可処分所得の増加です。

2022年、中国は7年連続で世界最大の物流市場の座を占め、同国の物流産業から12兆7,000億人民元(約1兆8,300億米ドル)の収益を上げました。同国のインフラは、中国政府からの多額の資金によって開発されています。中国は「一帯一路」構想の実行により、近い将来、物流・輸送セグメントの世界的リーダーになると考えられます:2022年、2023年のアジア新興国のGDP成長率はそれぞれ5.2%、5.3%に達します。

ただし、回復の速度はサブリージョンによって異なります。しかし、経済の内需は、特に南アジアでは、パンデミック以前の動向にまだ追いついており、これが地域の成長を支えています。南アジアの成長率は2022年も7.0%と堅調で、2023年には7.4%に急上昇します。東アジアの成長率は2023年には4.5%と正常化します。

アジア太平洋コントラクトロジスティクス市場の動向

製造業と自動車セクターからの需要がコントラクトロジスティクスサービスを牽引

アジア太平洋は世界の製造業の中心地のひとつであり、世界の製造業生産高の約48.5%を占めています。今日、世界の多くの国がインダストリー4.0の成長を支えるために先進的製造能力を構築しています。インダストリー4.0は、世界の製造業者が製品を生産し流通させる方法に革命をもたらしつつあります。AI、クラウドコンピューティング、分析、AI、機械学習は、事業に取り入れようとしている主要企業の技術のほんの一部に過ぎないです。

2022年、中国は約9兆8,800億米ドル相当の貨物輸送用自動車を輸出し、約50.57%の成長を示しました。ベトナムはまた、地域の中心性、高い市場統合性、低い生産コストにより、メーカーにとってますます魅力的な市場となっています。Samsung、Apple、Nintendo、LG、パナソニック、Intelはすべてベトナムに拠点を置いています。ベトナムはまた、エレクトロニクスセクターを擁することから、自国を中堅企業にとって魅力的な市場として位置づけ、バリューチェーンの進展を図っています。

NBSによると、2023年3月、中国の工業生産高は前年同期比3.9%増となり、COVID-19パンデミック後の同国経済回復のわずかな改善を示しました。付加価値工業生産高は前年同期比3%増となり、前期比で0.3ポイント増加しました。2022年の中国自動車メーカーの生産台数は前年同期比3.4%増の2,702万台、販売台数は同2.1%増の2,686万台となりました。中国は世界で最も魅力的な製造拠点としての地位を固めつつあり、タイはコストプロファイル改善の恩恵を受けています。

中国がコントラクトロジスティクス市場を牽引

中国の顧客需要が高まるにつれ、企業はより先進的物流チャネルの構築に迫られています。それは、より良いセキュリティやハンドリングを含むロジスティクス管理を必要とする、高価格の消費財や生鮮食品に対する需要の増加によるものです。これは、今後数年間に中国と新興経済諸国におけるハイエンドサービスの需要が大きく伸びることを指し示す、これらの経済におけるより重大な変化のひとつに過ぎないです。

中国はアジア太平洋のコントラクトロジスティクス市場をリードすると予想されます。中国のコントラクトロジスティクス市場は着実に成長しています。このため、製品やサービスの提供拡大、より効率的なネットワークの必要性、変動コストの抑制の必要性など、このセグメントに新たな課題が生まれています。

中国のコントラクトロジスティクス市場は、主に消費者小売、自動車、医薬品、電子機器などの産業に集中しており、消費者小売産業が約50%を占めています。

2023年2月、電子商取引大手Alibaba Group Holdingの物流部門であるCainiao Networkは、ドイツの大手宅配便会社Deutschlandpost DHLグループとポーランドで最も広範な小包ロッカーネットワークを構築する新たな合意を発表しました。ドイツポストeコマースグループの一部門であるDeutsche Post ECommerce Solutionsとの合意は、中国の大手技術企業にとって、欧州で最も急成長しているeコマース市場への足がかりとなります。同契約によると、Deutsche Post ECommerce Group(DHL)とCainiao Network(Alibaba Group Holdingのロジスティクス部門)は、ポーランド全土における小包ロッカーの建設に6,000万ユーロ(6,475万米ドル)を共同で投資します。両社は既存のネットワークを組み合わせ、消費者がより便利に宅配ロッカーを利用できるよう、近代的で使いやすいインターフェースを備えた宅配ロッカーを重要な場所に設置します。ポーランドにおけるDHLの宅配便ショップネットワークはすでに1,200カ所に達しており、DHLの宅配便ロッカーは過去3年間で品質とスピードが3倍に向上しています。

アジア太平洋コントラクトロジスティクス産業概要

アジア太平洋のコントラクトロジスティクス市場はセグメント化されており、大手国際企業と地元企業が混在しています。インドネシアやフィリピンのように、この地域の一部の国は緩やかに成長しており、多くの地元企業といくつかの大手国際企業が存在します。しかし、シンガポール、ベトナム、タイは、国際的な参入企業が多数存在する、競争の激しい市場です。企業は常に、コストの最小化と経営効率の最適化を迫られています。投資のシフトと世界のサプライチェーンの多様化に伴い、国際的な投資家はアジア太平洋物流市場におけるM&Aへの関心を高めています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 市場概要

- 市場力学

- 促進要因

- eコマースの成長

- 世界貿易とサプライチェーンの回復力

- 抑制要因

- 高い初期投資

- 機会

- 国境を越えたeコマース

- 促進要因

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 代替品の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 競争企業間の敵対関係の強さ

- バリューチェーン/サプライチェーン分析

- 政府の規制と取り組み

- 技術動向

- 域内のeコマース産業(国内と越境)について洞察

- アフターセールス/リバースロジスティクスにおけるコントラクトロジスティクス洞察

- コントラクトロジスティクス参入企業が提供する各種サービス(総合倉庫・輸送、サプライチェーンサービス、その他の付加価値サービス)概要

- 主要ルートの貨物輸送コスト/運賃に関するスポットライト

- 貨物輸送コリドー概要

- 主要経済特区(SEZ)と製造拠点に関する洞察

- COVID-19が市場に与える影響

第5章 市場セグメンテーション

- タイプ別

- インソーシング

- 外部委託

- エンドユーザー別

- 製造・自動車

- 消費財・小売

- ハイテク

- 医療医薬品

- その他

- 国別

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- シンガポール

- マレーシア

- インドネシア

- タイ

- その他のアジア太平洋

第6章 競合情勢

- 企業プロファイル

- Deutsche Post DHL Group

- DB Schenker

- Ceva Logistics

- United Parcel Services Inc.

- Logisteed Ltd

- CJ Logistics

- Nippon Express Co. Ltd

- Toll Group

- Nippon Express Co. Ltd

- Yusen Logistics Co. Ltd*

- その他の企業(主要情報/概要)

- Hellmann Worldwide Logistics、S.F.Holding Co. Ltd、Kerry Logistics Network Limited、Yamato holdings Co. Ltd、Leschaco Japan K.K.、Agility Logistics Ltd、Rhenus Logistics、GAC, Geodis、Linc Group、BCR Australia Pty Ltd、Silk Contract Logistics、DSV A/S*

第7章 市場機会と今後の動向

第8章 付録

- GDP分布、活動別、地域別

- 資本移動に関する洞察

- 対外貿易統計-主要国の輸出入(品目別)

- 主要国の主要輸出先に関する洞察

- 主要国の主要輸入原産地に関する洞察

The APAC Contract Logistics Market size is estimated at USD 273.27 billion in 2025, and is expected to reach USD 352.94 billion by 2030, at a CAGR of 5.25% during the forecast period (2025-2030).

The region's ability to weather the storm of economic instability strengthens its position as a preferred destination for investors and companies looking for more stability. Enhancing regional economic integration and providing access to a larger market, the ASEAN-led Regional Comprehensive Economic Partnership Agreement, taking effect in January 2022, would help the ASEAN countries recover from the recent epidemic while spurring economic growth.

Asia-Pacific is the area that is gaining ground the fastest in this market due to its quick economic development and thriving business climate. Asia-Pacific has eclipsed Europe to take the top spot in the global market for contract logistics. The region's growth is fueled by robust economic expansion, rising retail enactment, and increasing disposable income.

For the seventh year in a row, China held the title of largest logistics market in the world in 2022, generating a revenue of CNY 12.7 trillion (about USD 1.83 trillion) from the country's logistics industry. The country's infrastructure is being developed with significant funding from the Chinese government. China will soon become the global leader in the logistics and transportation sectors thanks to the Belt and Road Initiative's execution: 5.2% and 5.3% of the region's GDP growth in emerging Asia in 2022 and 2023, respectively.

However, the rate of recovery differs amongst subregions. However, domestic demand in economies is still catching up to their pre-pandemic trend, particularly in South Asia, which supports regional growth. Growth in South Asia remained robust in 2022 at 7.0% before soaring to 7.4% in 2023. The growth rates in East Asia are normalized at 4.5% in 2023.

APAC Contract Logistics Market Trends

Demand From The Manufacturing And Automotive Sector Is Driving The Contract Logistics Services

Asia-Pacific is one of the world's manufacturing hubs, accounting for almost 48.5% of global manufacturing output. Today, more countries worldwide are building advanced manufacturing capabilities to support Industry 4.0 growth. Industry 4.0 is revolutionizing the way global manufacturers produce and distribute their products. AI, cloud computing, analytics, AI, and machine learning are just a few technologies leading businesses looking to incorporate into their operations.

In 2022, China exported around USD 9.88 trillion worth of motor vehicles for transporting goods, representing a growth of about 50.57%. Vietnam has also become an increasingly attractive market for manufacturers due to the country's regional centrality, high market integration, and low production costs. Samsung, Apple, Nintendo, LG, Panasonic, and Intel are all based in Vietnam. Vietnam is also making progress in the value chain by positioning itself as an attractive market for mid-tech due to its electronic sector.

In March 2023, China's industrial output increased by 3.9% YoY in the first quarter of 2023, according to the NBS, indicating a slight improvement in the country's economic recovery in the wake of the COVID-19 pandemic. Value-added industrial output grew by 3% Y-o-Y, representing a YoY increase of 0.3 percentage points compared to the previous quarter. In 2022, Chinese car manufacturers produced 27.02 million units, an increase of 3.4% YoY, while sales rose 2.1% Y-o-Y to 26.86 million. China is consolidating its position as the world's most attractive manufacturing hub, while Thailand benefits from cost profile improvements.

China Is Leading The Way In The Contract Logistics Market

Companies are pressed to create more advanced distribution channels as customer demand in China grows. It is due to the increased demand for higher-priced consumer goods and perishable foods that require logistics management, including better security and handling. It is only one of the more profound changes in these economies that point to a significant growth in the demand for high-end services in China and developing countries over the next few years.

China is expected to lead the Asia-Pacific contract logistics market. The contract logistics market in China is growing steadily. This has created new challenges for the sector, such as the need to expand product and service offerings, the need for more efficient networks, and the need to control variable costs.

The Chinese contract logistics market is mainly concentrated in consumer retail, automotive, medicine, electronics, and other industries, with the consumer retail industry making up about 50%.

In February 2023, Cainiao Network, a logistics arm of e-commerce giant Alibaba Group Holding, announced a new agreement to build Poland's most extensive parcel locker network with German courier giant Deutschlandpost DHL Group. The agreement with Deutsche Post ECommerce Solutions, a Deutsche Post E-commerce Group division, provides a foothold for the Chinese technology giant into one of Europe's fastest-growing e-commerce markets. According to the agreement, Deutsche Post ECommerce Group (DHL) and Cainiao Network (the logistics arm of Alibaba Group Holding) will jointly invest EUR 60 million (USD 64.75 million) in the construction of parcel lockers throughout Poland. The two companies will combine their existing networks to provide consumers with more convenient access to parcel lockers, which will be installed at critical locations with modern, easy-to-use interfaces. DHL's parcel shop network in Poland has already reached 1,200 locations, and DHL's parcel lockers have tripled in quality and speed in the past three years.

APAC Contract Logistics Industry Overview

The Asia-Pacific Contract logistics market is fragmented, with a mix of major international and local companies. Some of the countries in the region, like Indonesia and the Philippines, are moderately growing, with many local players and some major international players. However, Singapore, Vietnam, and Thailand are highly competitive markets, with the presence of a large number of international players. Companies are constantly under pressure to minimize costs and optimize operational efficiency. In the wake of investment shifts and diversification of global supply chains, international investors are increasingly interested in mergers and acquisitions in the APAC logistics market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Market Overview

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 E-commerce Growth

- 4.2.1.2 Global Trade and Supply Chain Resilience

- 4.2.2 Restraints

- 4.2.2.1 High Initial Investment

- 4.2.3 Opportunities

- 4.2.3.1 Cross-Border E-commerce

- 4.2.1 Drivers

- 4.3 Industry Attractiveness - Porter's Five Force Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Threat of Substitute Products

- 4.3.3 Bargaining Power of Buyers/Consumers

- 4.3.4 Bargaining Power of Suppliers

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Government Regulations and Initiatives

- 4.6 Technological Trends

- 4.7 Insights into E-Commerce Industry in the Region (Domestic and Cross-Border)

- 4.8 Insights into Contract Logistics in the Context of After-Sales/Reverse Logistics

- 4.9 Brief on Different Services Provided by Contract Logistics Players (Integrated Warehousing and Transportation, Supply Chain Services, and Other Value-added Services)

- 4.10 Spotlight on Freight Transportation Costs/Freight Rates for Key Routes

- 4.11 Brief on Freight Transport Corridors

- 4.12 Insights into Key Special Economic Zones (SEZs) and Manufacturing Hubs

- 4.13 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Insourced

- 5.1.2 Outsourced

- 5.2 By End User

- 5.2.1 Manufacturing and Automotive

- 5.2.2 Consumer Goods and Retail

- 5.2.3 High-Tech

- 5.2.4 Healthcare and Pharmaceuticals

- 5.2.5 Other End Users

- 5.3 By Country

- 5.3.1 China

- 5.3.2 India

- 5.3.3 Japan

- 5.3.4 South Korea

- 5.3.5 Australia

- 5.3.6 Singapore

- 5.3.7 Malaysia

- 5.3.8 Indonesia

- 5.3.9 Thailand

- 5.3.10 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Overview (Market Concentration, Major Players)

- 6.2 Company Profiles

- 6.2.1 Deutsche Post DHL Group

- 6.2.2 DB Schenker

- 6.2.3 Ceva Logistics

- 6.2.4 United Parcel Services Inc.

- 6.2.5 Logisteed Ltd

- 6.2.6 CJ Logistics

- 6.2.7 Nippon Express Co. Ltd

- 6.2.8 Toll Group

- 6.2.9 Nippon Express Co. Ltd

- 6.2.10 Yusen Logistics Co. Ltd*

- 6.3 Other companies (Key Information/Overview)

- 6.3.1 Hellmann Worldwide Logistics, S.F.Holding Co. Ltd, Kerry Logistics Network Limited, Yamato holdings Co. Ltd, Leschaco Japan K.K., Agility Logistics Ltd, Rhenus Logistics, GAC, Geodis, Linc Group, BCR Australia Pty Ltd, Silk Contract Logistics, DSV A/S*

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

8 APPENDIX

- 8.1 GDP Distribution, By Activity and By Region

- 8.2 Insights on Capital Flows

- 8.3 External Trade Statistics - Export and Import, By Product For Key Countries

- 8.4 Insights on Key Export Destinations of Key Countries

- 8.5 Insight on Key Import Origins of Key Countries