|

市場調査レポート

商品コード

1939743

欧州のコントラクトロジスティクス:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Europe Contract Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のコントラクトロジスティクス:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 200 Pages

納期: 2~3営業日

|

概要

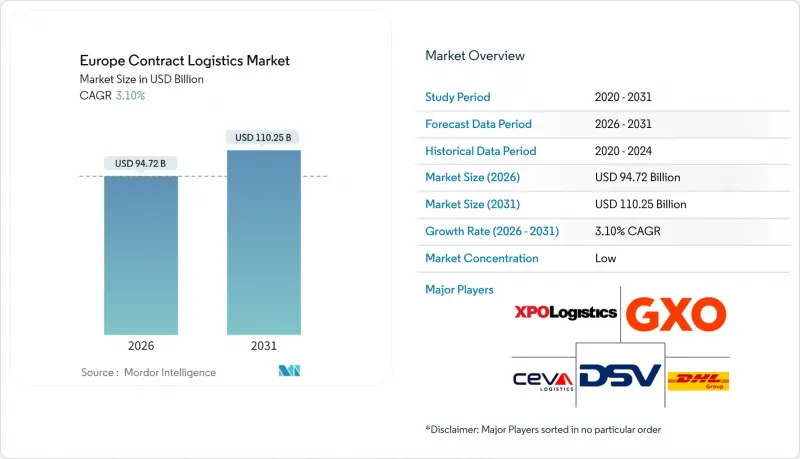

欧州のコントラクトロジスティクス市場規模は、2026年に947億2,000万米ドルと推定され、2025年の918億7,000万米ドルから成長し、2031年には1,102億5,000万米ドルに達すると予測されています。

2026年から2031年にかけては、CAGR 3.10%で成長が見込まれます。

成熟した市場環境は、ECフルフィルメント、サプライチェーンのレジリエンス強化、AIを活用した最適化が従来の運営モデルを変革する中、着実に付加価値ソリューションへと移行しています。東欧へのニアショアリングは貿易回廊を再構築しつつあり、EUの「Fit for 55」パッケージに基づく持続可能性目標は、低炭素輸送資産やグリーン倉庫への投資を促進しています。DSVによるDBシェンカーの大型買収に代表される統合の加速は、労働力不足、不動産価格上昇、規制の複雑化に対処するため、事業者が規模の経済を追求していることを示しています。ロボット技術、エンドツーエンド可視化プラットフォーム、柔軟な倉庫配置を組み込んだ事業者は、欧州コントラクトロジスティクス市場における次なるアウトソーシング需要の波を捉える最適な立場にあります。

欧州のコントラクトロジスティクス市場の動向と洞察

Eコマースの急成長が外部委託型フルフィルメントを加速

小売業者が固定不動産コストを柔軟な倉庫契約と交換する資産軽量モデルへ移行する中、サードパーティロジスティクス(3PL)事業者は増加するEコマース需要を捉えています。超大型物流センターの需要拡大により供給が逼迫し、小売業者は長期リースを確保しつつ日常業務を3PLに委託する傾向が強まっています。プロバイダー各社は、欧州コントラクトロジスティクス市場全体で当日配送目標を達成するため、オムニチャネル仕分け、ロボットピッキング、運送業者非依存型のラストマイルネットワークへの投資を進めています。ファッション・靴業界における高い返品率はリバースロジスティクスの複雑性を高めており、統合された返品処理が新規契約の標準機能となっています。フルフィルメントと返品処理を一つの技術基盤で統合する先駆的企業は、顧客の定着率を高め、プレミアム価格設定を実現しています。

ポストコロナにおけるサプライチェーン耐障害性強化の取り組み

パンデミックにより、レジリエンスはコストセンターから取締役会レベルの優先事項へと位置付けが再定義され、欧州全域でデュアルソーシング、地域バッファ、サプライヤー多様化が推進されました。海上・陸上・鉄道・航空の輸送イベントを単一ダッシュボードに統合するマルチモーダル可視化システムは、欧州コントラクトロジスティクス市場における契約入札時の核心的な選定基準となっています。顧客は、複数の在庫拠点を調整し、混乱時に貨物の経路を動的に変更できる3PLを優先します。2024年から2025年にかけてコントロールタワーアーキテクチャに投資したプロバイダーは、輸送業者が緊急時対応マニュアルを実証できるデータ豊富なパートナーを求める中、受注率の向上を報告しています。可視化の重要性はESG報告にも及び、リアルタイムのカーボン追跡がサービスレベル契約に明記されるケースが増加しています。

ドライバー・倉庫労働者不足

欧州ではプロのトラック運転手不足が深刻化しており、国際道路運送連合(IRU)は2026年までに200万人以上の不足が生じる可能性があると警告しています。倉庫労働者の離職率は、高齢労働者の退職が新規採用を上回るペースで加速しています。事業者側は入社金、柔軟な勤務体系、社内研修アカデミーで対応していますが、賃金上昇が欧州コントラクトロジスティクス市場の利益率を圧迫しています。自動化により一部圧力は緩和されますが、先行投資と変更管理サイクルにより回収期間は長期化します。労働力戦略を近代化しない限り、サービス中断やキャパシティ調整が顧客満足度の低下を招くリスクがあります。

セグメント分析

2025年、欧州のコントラクトロジスティクス市場シェアの60.35%を輸送サービスが占めました。これは道路・鉄道・航空・海上輸送が大陸間貿易を支えているためです。しかしながら、荷主が純粋な輸送速度よりも在庫配置を優先する傾向から、倉庫・流通部門は2031年までCAGR3.92%で最も急速に成長しています。欧州のコントラクトロジスティクス市場において輸送部門の規模は依然堅調ですが、価値は貨物輸送・保管・軽製造業務を統合したパッケージサービスへ移行中です。鉄道貨物輸送は2024年に0.7%減少し、EUがシェア倍増を目指す中、輸送モードの制約が浮き彫りとなりました。ドア・ツー・ドア輸送では道路輸送が依然として主流ですが、運送会社ネットワークには動的経路設定のためのデジタル貨物プラットフォームが組み込まれています。航空貨物輸送は高価値品や時間厳守品に特化したニッチ市場を維持し、短距離海上輸送は地中海・バルト海のゲートウェイを多モード輸送網に接続しています。

倉庫・流通分野でも同様の動向が見られます。人口密集地近郊の超大型ハブ需要は、土地不足や厳格なゾーニング規制と衝突し、優良物件の賃料を押し上げています。事業者側は高層自動化、メザニン型ロボット導入、ダークストア構成によりコストを抑制し、平方メートル当たりの処理能力を3倍に高めています。コールドチェーンの拡張は医薬品や生鮮食品を支え、参入の技術的障壁をさらに高めています。その結果、契約ではパレット移動量を超えたパフォーマンス指標が規定され、ピッキング精度、リバースロジスティクスサイクル、マイクロフルフィルメントの処理速度が追跡されるようになりました。欧州のコントラクトロジスティクス市場は、不動産に関する知見と高度なプロセスエンジニアリングを融合できる企業に報いる構造となっています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 電子商取引の急成長が外部委託型フルフィルメントを加速させております

- ポストCOVIDにおけるサプライチェーンのレジリエンス強化施策

- 東欧における製造業のニアショアリング

- AIを活用した倉庫・ルート最適化

- EU「Fit for 55」脱炭素化インセンティブ

- 返品に伴う統合型リバースロジスティクス需要

- 市場抑制要因

- ドライバー及び倉庫作業員の不足

- 分断化された競合価格圧力

- ESG準拠倉庫不動産コストの急騰

- 複雑な複数国における税関・付加価値税(VAT)コンプライアンス

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争の激しさ

- 電子商取引(国内・越境)に関する洞察

- アフターサービス/リバースロジスティクスに関する洞察

- ブレグジットの影響

- COVID-19及び地政学的イベントの影響

第5章 市場規模と成長予測

- サービスタイプ別

- 交通機関

- 道路輸送

- 鉄道

- 航空

- 海上輸送

- 倉庫保管・配送

- 付加価値サービス(組立、ラベリング、キット化)

- 交通機関

- 契約期間別

- 1~3年

- 3年以上

- エンドユーザー業界別

- 製造業・自動車産業

- 食品・飲料

- 小売・電子商取引

- 医療・医薬品

- 化学品

- その他業種

- 国別

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- ポーランド

- ベルギー

- スウェーデン

- その他欧州地域

第6章 競合情勢

- 市場集中度

- 戦略的動き(M&A、合弁事業、イノベーション)

- 市場シェア分析

- 企業プロファイル

- Deutsche Post DHL Group

- DSV

- GXO Logistics

- XPO Logistics

- CEVA Logistics

- Geodis

- Kuehne+Nagel

- Rhenus Logistics

- ID Logistics

- Hellmann Worldwide Logistics

- DACHSER

- United Parcel Service(UPS SCS)

- Neovia Logistics

- FIEGE Logistik Stiftung & Co. KG

- Savino Del Bene

- Rohlig Logistics

- BLG Logistics Group

- Groupe BBL

- Raben Group

- Noerpel Group

第7章 市場機会と将来の展望

第8章 付録

- 産業別GDP寄与度

- 資本フローに関する分析

- 貿易統計

- 主要な輸入・輸出ルート