|

市場調査レポート

商品コード

1642997

米国のコントラクトロジスティクス:市場シェア分析、産業動向、成長予測(2025~2030年)United States Contract Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国のコントラクトロジスティクス:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

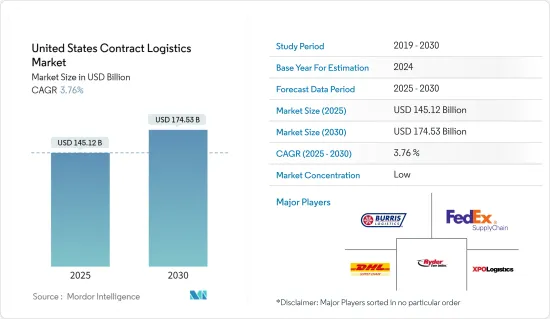

米国のコントラクトロジスティクス市場規模は2025年に1,451億2,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは3.76%で、2030年には1,745億3,000万米ドルに達すると予測されます。

主なハイライト

- 米国のコントラクトロジスティクス部門は、急成長するeコマースと技術の進歩から利益を得るための戦略的態勢を整えており、変革の時を迎えています。この進化はオンラインショッピングの急増に大きく後押しされ、消費者行動とロジスティクス要件の両方を再構築しています。

- 急増する需要に対応するため、ロジスティクス企業は倉庫ネットワークの拡大に大きく投資しています。予測によると、米国では増加する在庫を管理し、即日配達の期待に応えるために、さらに5億平方フィートの倉庫スペースが必要になるといいます。主要ロジスティクス企業は、効率を高め、製品フローを加速するために、自動化やロボット工学のような最先端技術でインフラをアップグレードしています。

- 2024年現在、米国のコントラクトロジスティクス市場では、持続可能性とデジタル化が重視されています。企業はエネルギー効率の高い輸送方法と最先端の追跡技術を採用し、環境への影響を軽減しながら業務能力を強化することを目指しています。さらに、北米のコントラクトロジスティクス市場の主要貢献国として浮上しています。

- サプライチェーン最適化のためのAIとMLの統合は、この市場拡大の極めて重要な原動力として際立っています。企業はAIを活用してルートプランニングを強化し、在庫管理を強化し、予測分析を行っています。例えば、XPOロジスティクスは、ルート最適化とリアルタイムの追跡にテクノロジーを活用し、サービス提供を強化し、コントラクトロジスティクスの主要企業としての地位を固めています。

- 例えば、C.H.Robinsonは、予測分析を使用して、自社のフリートのパフォーマンスを監督し、タイムリーなメンテナンスを保証し、サービスの中断を減らしています。これらのアプリケーションにより、企業は非効率を最小限に抑え、より正確に需要を予測することができます。

米国のコントラクトロジスティクス市場動向

eコマース売上の急増が市場拡大を後押し

米国では、eコマースの台頭がコントラクトロジスティクスの成長を大きく後押しし、合理化された倉庫管理、配送、ラストワンマイルの配送サービスに対する需要の高まりに拍車をかけています。オンライン・ショッピングの急増に伴い、ロジスティクス・プロバイダーはインフラを拡張し、フルフィルメントの需要に応えるために最先端技術を採用しました。

米国の配送指標は2023年に顕著な改善を見せた。スタティスタの報告によると、発行率は前年比3.6%減の6.4%、定時配達率は98%で横ばい、初回配達成功率は前年比12.2%増の97%、国内平均輸送日数は前年比24%短縮の2.56日となった。

この勢いは2024年まで続き、平均輸送日数はさらに短縮されて2.32日となります。経済的な逆風の中でも、業界予測によれば、2024年の米国の小売eコマース売上は2023年から10.5%増加する見込みです。

eコマースの急増に伴い、フェデックス、USPS、UPSといった大手物流企業は、ルートの最適化、インフラの強化、最先端の荷物追跡によって小包配達のスピードを強化しています。2024年には、フェデックスは平均2.08日、UPSは平均2.22日の輸送時間を達成しました。一方、USPSは懸命の努力にもかかわらず、平均輸送日数が2.55日に増加しました。

結論として、eコマースの絶え間ない成長が、米国のコントラクトロジスティクス市場を大きく前進させています。ロジスティクス・プロバイダーと輸送業者が需要の増加に適応するにつれ、この分野は効率と配送実績のさらなる改善の態勢が整いつつあります。

自動車産業と製造業が牽引するコントラクトロジスティクス市場

製造業がコアコンピタンスに磨きをかけるにつれ、ロジスティクス業務をサードパーティプロバイダーに任せる企業が増えています。このシフトは特に自動車分野で顕著であり、企業は複雑なサプライチェーンをナビゲートするために、専門的なロジスティクス・サービスへの依存を強めています。例えば、大手自動車メーカーのフォードやゼネラルモーターズは、XPOロジスティクスやDHLサプライチェーンなどのロジスティクス・プロバイダーと提携しています。この提携は、サプライチェーンを合理化し、業務効率を高め、コストを削減することを目的としています。

フェデックスやDHLを含む大手ロジスティクス企業は、2024年に米国の戦略的拠点で倉庫容量を拡大します。この拡張は、自動車メーカーからの急増する需要に直接対応するものです。ロジスティクス・インフラ、特に倉庫や配送センターには、製造業や自動車業界の進化するニーズに対応するため、多額の投資が行われています。

世界ロジスティクス分野で著名なDHLは、米国に最新の電気自動車(EV)センターオブエクセレンス(CoE)を開設しました。このセンターは、自動車モビリティ部門とその関連会社の電動化の旅を指導する態勢を整えています。新設された米国センターは、メキシコ、インドネシア、中国、アラブ首長国連邦、イタリア、英国などの戦略的立地にある既存のEVセンター・オブ・エクセレンスを補完する、より広範な世界・ネットワークの一部です。

結論として、コントラクトロジスティクス市場は、自動車業界や製造業界におけるサードパーティー・ロジスティクス・プロバイダーへの依存度の高まりに後押しされ、大きな成長を遂げています。この動向は、企業がサプライチェーンの最適化を図り、新技術を取り入れるにつれて、今後も続くと予想されます。

米国のコントラクトロジスティクス業界の概要

市場は細分化されており、XPO Logistics、Ryder System Inc.、FedEx Supply Chain、Burris Logistics、UPS Supply Chain Solutions、KUEHNE+NAGELなどが主要企業です。ロジスティクスの自動化、IoT、トラック上の人為的損傷を検出するためのセンサーやUAVのアプリケーションなどの技術的進歩は、配送やロジスティクスにおけるAIの役割と並んで、業界に革命をもたらしました。市場は依然として断片化されており、国内外のプレーヤーが多様に混在しています。

効果を高めるために、各社は手を結んでいます。例えば、国内大手の海上ドレージ・プロバイダーであるIMCロジスティクスは、長年の顧客であるKuehne+Nagelと戦略的パートナーシップを結びました。PR Newswireが報じたように、Kuehne+NagelはIMC Logisticsの株式51%を取得する予定です。この提携は、包括的な貨物輸送サービスに対する急増する需要に応えることを目的としており、米国内の海港、鉄道ハブ、顧客施設、内陸部との間の移動を促進します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 現在の市場シナリオ

- 市場力学

- 市場促進要因

- eコマースの成長

- 技術の進歩

- 市場抑制要因

- 労働力不足

- 燃料費と輸送費の高騰

- 市場機会

- 持続可能性への取り組み

- カスタマイズとオーダーメード・ソリューション

- 市場促進要因

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- バリューチェーン/サプライチェーン分析

- 業界の規制と政策に関する洞察

- 技術統合に関する洞察

- 地域のeコマース産業(国内および越境)に関する洞察

- コントラクトロジスティクス・プレイヤーが提供する各種サービス(総合倉庫・輸送、サプライチェーン・サービス、その他の付加価値サービス)に関する考察

- 注目-貨物輸送コスト/運賃

- 地政学とパンデミックが市場に与える影響

第5章 市場セグメンテーション

- タイプ別

- インソース

- アウトソース

- エンドユーザー別

- 製造・自動車

- 消費財・小売

- ハイテク

- ヘルスケアと医薬品

- その他のエンドユーザー(エネルギー、建設、航空宇宙など)

第6章 競合情勢

- 市場集中の概要

- 企業プロファイル

- XPO Logistics

- Ryder Supply Chain Solutions

- DHL Supply Chain North America

- FedEx Logistics

- Burris Logistics

- Kuehne+Nagel

- GXO Logistics

- UPS

- GAC United States

- GEODIS

- Hellmann Worldwide Logistics

- DB Schenker

- Hub Group*

- その他の企業

第7章 市場の将来展望

第8章 付録

- マクロ経済指標(GDP分布、活動別)

- 経済統計-運輸・倉庫業の経済貢献度

- 対外貿易統計-品目別、仕向地・原産地別輸出入額

The United States Contract Logistics Market size is estimated at USD 145.12 billion in 2025, and is expected to reach USD 174.53 billion by 2030, at a CAGR of 3.76% during the forecast period (2025-2030).

Key Highlights

- Strategically poised to benefit from the burgeoning e-commerce landscape and technological advancements, the United States contract logistics sector is witnessing a transformation. This evolution is largely fueled by a surge in online shopping, reshaping both consumer behavior and logistics requirements.

- In response to surging demand, logistics firms are significantly investing in expanding their warehousing networks. Projections indicate that the U.S. will need an additional 500 million square feet of warehouse space to manage growing inventories and meet same-day delivery expectations. Leading logistics companies are upgrading their infrastructure with cutting-edge technologies like automation and robotics to boost efficiency and accelerate product flow.

- As of 2024, the U.S. contract logistics market is placing a heightened focus on sustainability and digitalization. Firms are embracing energy-efficient transportation methods and state-of-the-art tracking technologies, aiming to bolster operational capabilities while reducing environmental impact. Furthermore, the nation emerges as the leading contributor to North America's contract logistics market.

- AI and ML integration for supply chain optimization stands out as a pivotal driver of this market's expansion. Businesses are leveraging AI to enhance route planning, strengthen inventory management, and perform predictive analyses. For instance, XPO Logistics utilizes technology for route optimization and real-time tracking, enhancing its service offerings and solidifying its position as a key player in the contract logistics landscape.

- For instance, C.H. Robinson employs predictive analytics to oversee its fleet's performance, guaranteeing timely maintenance and reducing service disruptions. These applications empower companies to minimize inefficiencies and forecast demands with greater precision

United States Contract Logistics Market Trends

Surge in E-Commerce Sales Fuels Market Expansion

In the U.S., the rise of E-Commerce has significantly propelled the growth of contract logistics, spurring heightened demand for streamlined warehousing, distribution, and last-mile delivery services. As online shopping surged, logistics providers expanded their infrastructures and adopted cutting-edge technologies to meet fulfillment demands.

Delivery metrics in the U.S. showed marked improvements in 2023: the issue ratio dipped 3.6% year-over-year (YoY) to 6.4%, the on-time delivery ratio held steady at 98%, the first-attempt delivery success rate jumped 12.2% YoY to 97%, and average domestic transit times shortened by 24% YoY to 2.56 days, as reported by Statista.

This momentum carried into 2024, with average transit times further refining to 2.32 days. Even amidst economic headwinds, U.S. retail e-commerce sales in 2024 are set to rise by 10.5% from 2023, as per industry forecasts.

In tandem with the E-Commerce surge, major logistics players like FedEx, USPS, and UPS have bolstered parcel delivery speeds via route optimization, infrastructure enhancements, and state-of-the-art package tracking. In 2024, FedEx and UPS achieved average transit times of 2.08 days and 2.22 days respectively. Conversely, USPS, despite their concerted efforts, saw an uptick in average transit time to 2.55 days.

In conclusion, the continuous growth of E-Commerce is driving significant advancements in the U.S. contract logistics market. As logistics providers and carriers adapt to increasing demands, the sector is poised for further improvements in efficiency and delivery performance.

Contract Logistics Market Propelled by the Automotive and Manufacturing Sectors

As manufacturers hone in on their core competencies, a growing number are turning to third-party providers for logistics operations. This shift is especially evident in the automotive sector, where firms increasingly rely on specialized logistics services to navigate their intricate supply chains. For example, leading automotive giants Ford and General Motors have teamed up with logistics providers like XPO Logistics and DHL Supply Chain. This collaboration aims to streamline their supply chains, boosting operational efficiency and driving down costs.

Major logistics companies, including FedEx and DHL, are expanding their warehouse capacities at strategic U.S. locations in 2024. This expansion is a direct response to the surging demands from automotive manufacturers. Significant investments are being made in logistics infrastructure, particularly in warehouses and distribution centers, to meet the evolving needs of the manufacturing and automotive sectors.

DHL, a prominent player in the global logistics arena, has inaugurated its latest Electric Vehicle (EV) Center of Excellence (CoE) in the U.S. This center is poised to guide the auto-mobility sector and its affiliates on their electrification journey. The newly established U.S. center is part of a broader global network, complementing existing EV Centers of Excellence in strategic locations such as Mexico, Indonesia, China, the UAE, Italy, and the UK.

In conclusion, the contract logistics market is experiencing significant growth, driven by the increasing reliance of the automotive and manufacturing sectors on third-party logistics providers. This trend is expected to continue as companies seek to optimize their supply chains and embrace new technologies.

United States Contract Logistics Industry Overview

The market is fragmented, with XPO Logistics, Ryder System Inc., FedEx Supply Chain, Burris Logistics, UPS Supply Chain Solutions, KUEHNE+NAGEL, etc as its major players. Technological advancements, such as logistic automation, IoT, and the application of sensors and UAVs for detecting human-made damages on tracks, alongside AI's role in delivery and logistics, have revolutionized the industry. The market remains fragmented, featuring a diverse mix of local and international players.

In a bid to boost effectiveness, companies are joining hands. For instance, IMC Logistics, the nation's leading marine drayage provider, has entered into a strategic partnership with its long-standing client, Kuehne+Nagel. As reported by PR Newswire, Kuehne+Nagel is set to acquire a 51% stake in IMC Logistics. This collaboration aims to meet the surging demand for comprehensive cargo transportation services, facilitating movement to and from seaports, rail hubs, customer facilities, and inland locations across the United States.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Market Drivers

- 4.2.1.1 E Commerce Growth

- 4.2.1.2 Technological Advancements

- 4.2.2 Market Restraints

- 4.2.2.1 Labor Shortage

- 4.2.2.2 Rising Fuel and Transportation costs

- 4.2.3 Market Opportunities

- 4.2.3.1 Sustainability Initiatives

- 4.2.3.2 Customization and Tailored Solutions

- 4.2.1 Market Drivers

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Insights on Industry Policies and Regulations

- 4.6 Insights on Technological Integration

- 4.7 Insights on E-commerce Industry in the Region (Domestic and Cross-border)

- 4.8 Brief on Different Services Provided by Contract Logistics Players (Integrated Warehousing and Transportation, Supply Chain Services, and Other Value-Added Services)

- 4.9 Spotlight - Freight Transportation Costs/Freight Rates

- 4.10 Impact of Geopolitics and Pandemic on the Market

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Insourced

- 5.1.2 Outsourced

- 5.2 By End-User

- 5.2.1 Manufacturing and Automotive

- 5.2.2 Consumer Goods and Retail

- 5.2.3 High-tech

- 5.2.4 Healthcare and Pharmaceuticals

- 5.2.5 Other End-Users(Energy, Construction, Aerospace, etc.)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 XPO Logistics

- 6.2.2 Ryder Supply Chain Solutions

- 6.2.3 DHL Supply Chain North America

- 6.2.4 FedEx Logistics

- 6.2.5 Burris Logistics

- 6.2.6 Kuehne + Nagel

- 6.2.7 GXO Logistics

- 6.2.8 UPS

- 6.2.9 GAC United States

- 6.2.10 GEODIS

- 6.2.11 Hellmann Worldwide Logistics

- 6.2.12 DB Schenker

- 6.2.13 Hub Group*

- 6.3 Other Companies

7 FUTURE OUTLOOK OF THE MARKET

8 APPENDIX

- 8.1 Macroeconomic Indicators (GDP Distribution, by Activity)

- 8.2 Economic Statistics - Transport and Storage Sector Contribution to Economy

- 8.3 External Trade Statistics - Exports and Imports by Product and by Country of Destination/Origin