|

市場調査レポート

商品コード

1636140

インドのコントラクトロジスティクス:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)India Contract Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドのコントラクトロジスティクス:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

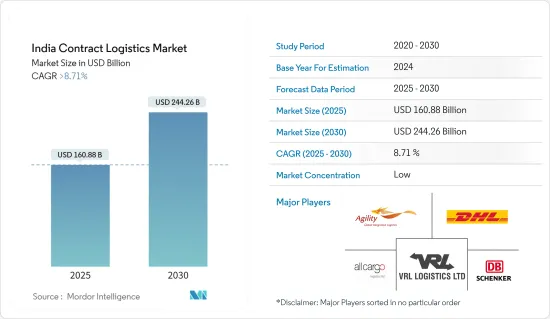

インドのコントラクトロジスティクス市場規模は2025年に1,608億8,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは8.71%を超え、2030年には2,442億6,000万米ドルに達すると予測されます。

主要ハイライト

- インド経済が上昇基調を続ける中、コントラクトロジスティクスの需要が顕著に急増しています。eコマースは情勢を変えつつあり、顧客は自社のコアコンピタンスを優先させるため、オーダーメイドのソリューションとコスト効率に対する需要が高まっています。この進化する情勢は、参入企業に従来の枠を超えた適応を促しています。過去10年間、インドのコントラクトロジスティクス・シーンは、主に国の経済上昇に後押しされ、大きな変貌を遂げてきました。この急成長する市場の魅力は、海外参入企業の注目さえ集めています。

- 例えば、2023年8月、CMA CGMの子会社であるCEVA Logisticsは、ムンバイのステラ・バリューチェーンソリューションズの株式の96%を取得し、話題となりました。この戦略的な動きは、コントラクトロジスティクス、特にeコマース、自動車、食品、消費財、ファッション、小売、医療、医薬品など多様なセグメントにまたがるオムニチャネル・フルフィルメントサービスの重要性が高まっていることを強調しています。ステラ社は現在、インド21都市に70以上の施設を有し、総面積は770万平方フィートに及びます。

- 都市化、経済開発、急増する中産階級がインド国内の消費に拍車をかけています。この急増は、日用品、自動車、生活必需品、高級品にまで及び、小売産業におけるコントラクトロジスティクスの成長を後押ししています。

- さらに、eコマースはインドのコントラクトロジスティクス部門を強化する礎石となっています。モバイルコマースの台頭、革新的な決済方法、地方へのeコマースの進出、人工知能と自動化の採用といった動向は、オンライン販売の力学を再構築しています。こうしたシフトはオンライン販売を強化するだけでなく、コントラクトロジスティクス部門の成長も増幅させる。さらに、ビッグデータ分析、インテリジェントなマテリアルハンドリング機器、先進的追跡モバイルアプリといった最先端の介入が、インドのコントラクトロジスティクス・情勢に革命をもたらしています。

インドのコントラクトロジスティクス市場動向

インドのインソーシングロジスティクスeコマースとデジタル変革の波に乗る

サプライチェーンの俊敏性、デジタル革新、eコマースブームに対する需要の急増に後押しされ、インドのインソーシングロジスティクス部門は大きく拡大しようとしています。主に大企業がこのセグメントを支配しているが、技術によって従来の参入障壁が低くなったため、中堅企業もこのセグメントに進出しています。eコマースの急成長により、多くの企業が社内でロジスティクス能力を育成し、迅速な配送と顧客体験の管理強化を図っています。ロジスティクス・セクターが進化するにつれ、サービスに対する需要が急増しており、eコマースの急速な進展がそれに拍車をかけています。インドのeコマース物流市場の主要促進要因には、インターネット普及率の上昇、ラストワンマイルデリバリーの台頭、魅力的な割引によって拡大するオンラインショッピングの嗜好、オンライン食料品物流の範囲の拡大などがあります。

予測によると、インドのeコマース産業は2030年までに3,250億米ドルに急増します。2024年には、サードパーティロジスティクスプロバイダーは今後7年間で約170億件の出荷を処理することになります。インドのインターネット加入者は約9億3,616万人で、約3億5,000万人が取引に積極的に参加するベテラン・オンラインユーザーです。2023年12月、インドのeコマースの巨人Flipkartは、新たな資金調達ラウンドで10億米ドルを確保する準備を進めており、親会社のWalmartは6億米ドルを投入する見込みです。このラウンドをさらに強化し、2024年5月にはGoogleLLCがフリップカートに3億5,000万米ドルを投入します。この資金調達は、Flipkartの大株主であるWalmart Inc.が主に主導するもので、Flipkartの事業を拡大し、より広範なインドの顧客層に向けてデジタルフレームワークを近代化することを目的としています。さらに、両社はFlipkartとGoogleのクラウドプラットフォームとの統合を強化する戦略も練っています。

eコマースが世界の盛り上がりを見せる中、小売企業にとってコントラクトロジスティクスの役割は最重要となっています。オンライン戦略とオムニチャネル戦略の一体化が重視される中、コントラクトロジスティクスの重要性が浮き彫りになっています。在庫管理、梱包、輸送、レポーティング、予測、倉庫管理などを統括するコントラクトロジスティクスは、小売企業のオンライン注文への対応を強化する上で極めて重要な役割を果たしています。

製造業と自動車産業の成長がコントラクトロジスティクス市場を牽引

「Make in India」イニシアティブに後押しされ、コントラクトロジスティクス市場は力強い成長を遂げています。製造業はますますコア・コンピタンスを重視し、コスト効率を追求し、先進技術をサプライチェーン活動に取り入れるようになっています。

同時に、製造業はサプライチェーン・マネジメントのアウトソーシングという動向の先駆者となっています。このシフトは、サービスプロバイダーが重要なパートナーへと進化し、文書化、追跡、倉庫管理、法令遵守を含む包括的なソリューションを提供することによって後押しされています。さらに、自動車部門はマルチモーダルロジスティクスの需要を高めています。

他方、2023~24年、インドでは自動車部品の輸入が3%増加し、総額209億米ドルとなり、2022~23年の203億米ドルから増加しました。アジアからの輸入が全体の66%を占め、次いで欧州が26%、北米が8%でした。特筆すべきは、アジアからの輸入が3%増加したことです。主要輸入品目は、エンジン・コンポーネント、ボディ&シャーシ、サスペンション&ブレーキ、トランスミッション&ステアリングです。このように、自動車輸出輸入の増加は、国全体のコントラクトロジスティクスサービスを促進すると予想されます。

インドのコントラクトロジスティクス産業概要

インドのコントラクトロジスティクス市場は熾烈な競争状態にあり、多くの国際企業や小規模な国内企業が存在する断片的な市場です。

コントラクトロジスティクス市場の主要企業は、インドにおける機会から最大限の利益を得ようとイニシアティブをとっています。コントラクトロジスティクス市場の主要企業には、Deutsche Post DHL、DB Schenker、Kuehne+Nagel International AG、Allcargoなどがあります。インドのコントラクトロジスティクス部門は一定の成長曲線を描いています。この成長は、より効率的なネットワークの運営や製品・サービスポートフォリオの拡大から、予測不可能なコストの管理まで、産業の新たな課題をもたらしています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 技術動向に関する洞察

- 政府規制とイニシアティブ概要

- バリューチェーン/サプライチェーン分析

- 貨物輸送コスト/運賃に関する洞察

- 域内のeコマース産業(国内と越境)に関する洞察

- アフターセールス/リバースロジスティクスの文脈におけるコントラクトロジスティクスに関する洞察

- 物流セクターにおけるGST実施の影響に関する洞察

- コントラクトロジスティクス参入企業が提供する各種サービス(総合倉庫・輸送、サプライチェーンサービス、その他の付加価値サービス)概要

- 主要な経済特区(SEZS)と製造拠点に関する洞察

- 地政学とパンデミックが市場に与える影響

第5章 市場力学

- Marjetの促進要因

- 電子商取引の成長

- 政府の施策が市場を後押し

- 市場抑制要因

- 熟練労働者の不足

- 高額な設備投資

- 市場機会

- 技術革新

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第6章 市場セグメンテーション

- タイプ別

- インソーシング

- アウトソーシング

- エンドユーザー別

- 製造・自動車

- 消費財・小売

- ハイテク

- 医療と製薬

- その他のエンドユーザー(エネルギー、建設、航空宇宙など)

第7章 競合情勢

- 市場集中概要

- 企業プロファイル

- 海外市場参入企業

- Kuehne+Nagel Private Limited

- Hellmann Worldwide Logistics India Private Limited

- Agility Logistics

- CH Robinson Worldwide Freight India Private Limited

- DSV Panalpina

- Nippon Express (India) Private Limited

- FedEx Corporation

- Expeditors International (India) Private Limited*

- 国内市場参入企業

- All Cargo Logistics Limited

- VRL Logistics Ltd

- Adani Logistics Company

- Aegis Logistics Ltd

- Transport Corporation of India

- Gati Litmited

- Delhivery Private Limited

- Future Supply Chain Solutions Ltd

- TVS Supply Chain Solutions*

- 海外市場参入企業

- その他の企業(Mahindra Logistics、Safexpress Pvt Ltd、Snowman Logistics、GS Logistics、Nitco Logistics、Gateway Distriparks Limited*)

第8章 市場の将来展望

第9章 付録

- GDP分布(活動別、地域別)

- 資本フロー洞察(セクター別投資額)

- 主要輸出先に関する洞察

- 主要輸入原産国洞察

The India Contract Logistics Market size is estimated at USD 160.88 billion in 2025, and is expected to reach USD 244.26 billion by 2030, at a CAGR of greater than 8.71% during the forecast period (2025-2030).

Key Highlights

- As the Indian economy continues its upward trajectory, the demand for contract logistics is witnessing a notable surge. E-commerce is reshaping the landscape, and as customers prioritize their core competencies, there's an increasing demand for tailored solutions and cost efficiency. This evolving landscape is pushing players to adapt beyond their traditional boundaries. Over the past decade, the Indian contract logistics scene has undergone significant transformations, primarily fueled by the nation's economic ascent. The allure of this burgeoning market has even drawn the attention of foreign players.

- For instance, in August 2023, CMA CGM's subsidiary, CEVA Logistics, made headlines by acquiring a 96 percent stake in Mumbai's Stellar Value Chain Solutions. This strategic move underscores the growing prominence of contract logistics, especially with omnichannel fulfillment services spanning diverse sectors such as e-commerce, automotive, food products, consumer goods, fashion, retail, healthcare, and pharmaceuticals. Stellar, now a pivotal player, boasts an expansive footprint with 7.7 million square feet of space distributed across over 70 facilities in 21 cities throughout India.

- Urbanization, economic development, and a burgeoning middle class have fueled domestic consumption in India. This surge spans everyday fast-moving consumer goods, personal automobiles, household essentials, and even luxury items, all propelling the growth of contract logistics within the retail sector.

- Moreover, e-commerce stands as a cornerstone in bolstering the country's contract logistics sector. Trends like the rise of mobile commerce, innovative payment methods, e-commerce's reach into rural territories, and the adoption of artificial intelligence and automation are reshaping online sales dynamics. These shifts not only bolster online sales but also amplify the growth of the contract logistics sector. Furthermore, cutting-edge interventions such as big data analytics, intelligent material handling equipment, and advanced tracking mobile apps are revolutionizing India's contract logistics landscape.

India Contract Logistics Market Trends

India's Insourced Logistics: Riding the Wave of E-Commerce and Digital Transformation

Driven by the surging demand for supply chain agility, digital innovation, and the e-commerce boom, India's insourced logistics sector is on the brink of significant expansion. While predominantly dominated by large corporations, mid-sized enterprises are making their foray into the sector, due to technology reducing traditional entry barriers. The e-commerce surge has prompted numerous businesses to cultivate in-house logistics capabilities, ensuring quicker deliveries and enhanced control over customer experiences. As the logistics sector evolves, it's responding to the burgeoning demand for services, largely spurred by the rapid advancements in e-commerce. Key drivers for India's e-commerce logistics market include increased internet penetration, the rise of last-mile delivery, a growing preference for online shopping-amplified by attractive discounts-and the broadening scope of online grocery logistics.

Forecasts suggest the Indian e-commerce industry will soar to USD 325 billion by 2030. In 2024, third-party logistics providers are set to handle around 17 billion shipments over the next seven years. With approximately 936.16 million internet subscribers in India, about 350 million are seasoned online users actively participating in transactions. In December 2023, Indian e-commerce titan Flipkart is gearing up to secure USD 1 billion in a fresh funding round, with its parent entity, Walmart, expected to infuse USD 600 million. Further bolstering this round, in May 2024, Google LLC is channeling USD 350 million into Flipkart. This funding, predominantly led by Walmart Inc.-Flipkart's majority stakeholder-aims to amplify Flipkart's operations and modernize its digital framework for a broader Indian customer base. Additionally, both entities are strategizing to enhance Flipkart's integration with Google's cloud platform.

As e-commerce garners global momentum, the role of contract logistics has become paramount for retailers. The emphasis on cohesive online and omnichannel strategies highlights the critical nature of contract logistics. By overseeing inventory management, packaging, transportation, reporting, forecasting, and warehousing, contract logistics plays a pivotal role in enhancing online order fulfillment for retailers.

Growth in the Manufacturing and Automotive Sector Driving the Contract Logistics Market

Fueled by the 'Make in India' initiative, the contract logistics market is witnessing robust growth, largely due to the rapid expansion of the manufacturing industry. Manufacturers are increasingly emphasizing core competencies, seeking cost efficiencies, and integrating advanced technologies into their supply chain activities.

Simultaneously, the manufacturing sector has pioneered the trend of outsourcing supply chain management. This shift is bolstered by the evolution of service providers into pivotal partners, delivering comprehensive solutions that encompass documentation, tracking, warehousing, and legal compliance. Furthermore, the automobile sector is amplifying the demand for multi-modal logistics.

On the other hand, In 2023-24, India saw a 3 percent rise in auto component imports, totaling USD 20.9 billion, up from USD 20.3 billion in 2022-23. Asia dominated the import landscape, contributing 66 percent, trailed by Europe at 26 percent and North America at 8 percent. Notably, imports from Asia experienced a 3 percent uptick. Major import categories encompassed engine components, body & chassis, suspension & braking, and drive transmission & steering. Thus, the growing automobile export imports are expected to drive contract logistics services across the country.

India Contract Logistics Industry Overview

The Contract Logistics market in India is fiercely competitive, fragmented in nature with the presence of many international and too many small domestic companies.

Key players in the contract logistics market are taking initiatives to gain maximum benefit from the opportunities in India. Some of the major players in the contract logistics market include Deutsche Post DHL, DB Schenker, Kuehne + Nagel International AG, Allcargo, among others. The contract logistics sector in India is on a constant growth curve. This growth has brought with it a new set of industry challenges, from running more efficient networks and expanding product and service portfolios to gaining control over unpredictable costs.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Insights in Technological Trends

- 4.3 Brief on Government Regulations and Initiatives

- 4.4 Value Chain/Supply Chain Analysis

- 4.5 Insights on Freight Transportation Costs /Freight Rates

- 4.6 Insights on E-Commerce Industry in the Region (Domestic and Cross-Border)

- 4.7 Insights on Contract Logistics in the Context of After-Sales/Reverse Logistics

- 4.8 Insights on the impact of Implementation of GST in the Logistics Sector

- 4.9 Brief on Different Services Provided by Contract Logistics Players (Integrated Warehousing & Transportation, Supply Chain Services, and Other Value-Added Services)

- 4.10 Insights into Key Special Economic Zones (SEZS) and Manufacturing Hubs

- 4.11 Impact of Geopolitics and Pandemic on the Market

5 MARKET DYNAMICS

- 5.1 Marjet Drivers

- 5.1.1 Growth in Ecommerce

- 5.1.2 Government intiatives are boosting the market

- 5.2 Market Restriants

- 5.2.1 Skilled Labor Shortages

- 5.2.2 High Intiatial Investments

- 5.3 Market Oppurtunities

- 5.3.1 Technological Innovations

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Consumers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Insourced

- 6.1.2 Outsourced

- 6.2 By End User

- 6.2.1 Manufacturing and Automotive

- 6.2.2 Consumer Goods & Retail

- 6.2.3 High - Tech

- 6.2.4 Healthcare and Pharmaceutical

- 6.2.5 Other End Users (Energy, Construction, Aerospace, etc.)

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 International Players

- 7.2.1.1 Kuehne + Nagel Private Limited

- 7.2.1.2 Hellmann Worldwide Logistics India Private Limited

- 7.2.1.3 Agility Logistics

- 7.2.1.4 CH Robinson Worldwide Freight India Private Limited

- 7.2.1.5 DSV Panalpina

- 7.2.1.6 Nippon Express (India) Private Limited

- 7.2.1.7 FedEx Corporation

- 7.2.1.8 Expeditors International (India) Private Limited *

- 7.2.2 Domestic Players

- 7.2.2.1 All Cargo Logistics Limited

- 7.2.2.2 VRL Logistics Ltd

- 7.2.2.3 Adani Logistics Company

- 7.2.2.4 Aegis Logistics Ltd

- 7.2.2.5 Transport Corporation of India

- 7.2.2.6 Gati Litmited

- 7.2.2.7 Delhivery Private Limited

- 7.2.2.8 Future Supply Chain Solutions Ltd

- 7.2.2.9 TVS Supply Chain Solutions *

- 7.2.1 International Players

- 7.3 Other Companies (Mahindra Logistics, Safexpress Pvt Ltd, Snowman Logistics, GS Logistics, Nitco Logistics, Gateway Distriparks Limited*)

8 FUTURE OUTLOOK OF THE MARKET

9 APPENDIX

- 9.1 GDP Distribution, by Activity and Region

- 9.2 Insight into Capital Flows (investments by sector)

- 9.3 Insight into Key Export Destinations

- 9.4 Insight into Key Import Origin Countries