男性用グルーミング製品:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

Men's Grooming Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1910510

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

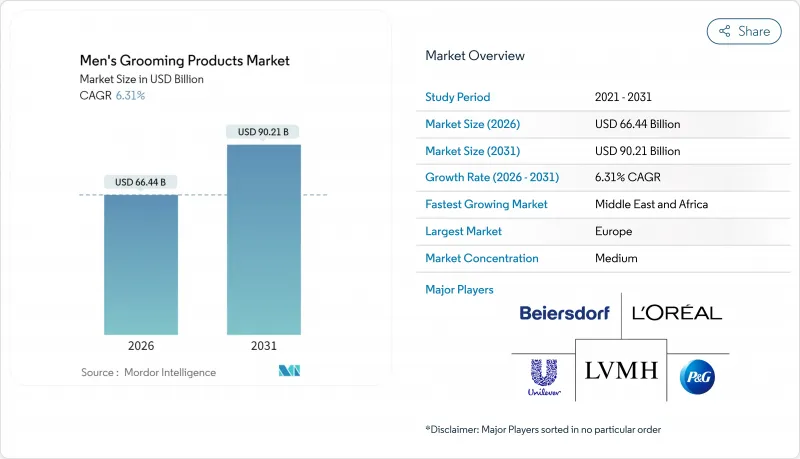

男性用グルーミング製品市場は、2025年に625億米ドルと評価され、2026年の664億4,000万米ドルから2031年までに902億1,000万米ドルに達すると予測されています。

予測期間(2026年~2031年)におけるCAGRは6.31%と見込まれています。

可処分所得の増加、ソーシャルメディアの影響力、そして男性性に対する文化的認識の変化が、男性に多面的なセルフケア習慣の採用を促しており、これは今や長年確立されてきた女性の美容行動を反映するものです。プレミアム化、成分の透明性、クリーンラベルへの需要、そして急速なデバイス革新がカテゴリー幅を拡大する一方、持続可能性への懸念が包装デザインや原材料の選択を再構築しています。これにより有機製品の数が伸びています。例えば、ドイツ連邦農業食品研究所(Bundesanstalt fur Landwirtschaft und Ernahrung)によれば、2024年12月時点でドイツ国内では合計109,567製品が有機認証を取得しています。競合の勢いは、成長分野を確保するため、世界のコングロマリットが機敏なデジタルネイティブブランドを買収する動きにより強まっています。一方、オムニチャネル小売戦略は消費者のアクセスを拡大し、データ駆動型のパーソナライゼーションを促進しており、男性用グルーミング製品市場の長期的な拡大ストーリーを強化しています。

世界の男性用グルーミング製品市場の動向と洞察

男性向けスキンケアと専門的ルーティンの拡大

男性向けスキンケアの採用は、従来のアフターシェーブ用途を超え、ニキビ・老化・敏感肌といった特定のお悩みに対応する専門的な処方へと加速しています。2023年8月の「ホットペッパービューティーアカデミー」調査によれば、洗顔料が日本の男性消費者にとって最も選ばれる化粧品となりました。同調査では、過去1年間に洗顔料を少なくとも1点購入した日本人男性が49%に上ることが明らかになりました。これを受け、2025年1月に発売されるDove Men+Careの「アドバンスドケアフェイス&ボディクレンジング」コレクションは、乾燥肌修復・敏感肌鎮静・ニキビケアの3分野をターゲットとし、男性消費者の80%が高度なスキンケアソリューションに関心を持っていることを反映しています。同様に、エスティローダーの「ラボシリーズ」がAmazonプレミアムビューティーに進出したことは、男性向けスキンケアの高度化に対する業界の確信を示しており、知識のある消費者向けに科学的に裏付けられた処方箋を強調しています。サントリーウェルネスの「KIZEN」米国市場投入では、発売前テストで90%の満足度を達成し、特に保湿効果に92%が満足と回答。これは配合の精密さが採用を促進することを示しています。この拡大は新たな収益源を創出すると同時に、製品ポートフォリオ全体の平均販売価格を引き上げます。さらに、2022年化粧品規制近代化法に基づくFDAの化粧品規制は安全基準を確保し、専門的な配合に対する消費者の信頼を構築することで市場の成長を促進しています。

ひげケア・スタイリング市場の成長

ひげケアは基本的な手入れから洗練されたスタイリングシステムへと進化し、専門的なツールや処方が明確な市場セグメンテーションを形成しています。例えば、ハイランド社の「ザ・ウォッシュ」発売は35歳未満の消費者が抱える薄毛の懸念に対応しています。さらに2023年、コスメティカ・イタリアの報告によれば、シェービングソープとジェルがイタリアにおける男性用ケア製品の消費を牽引し、顕著な58.4%のシェアを占めました。特許開発の分野では、シキミ酸やウルソール酸などの天然抽出物を配合した脱毛予防・治療用組成物が登場し、治療用途が拡大しています。さらに、ひげスタイリングツールは精密工学と人間工学に基づいたデザインを融合させ、専門的な製造能力への投資を正当化するプレミアム価格帯を形成しています。有機パーソナルケア製品向けのNSF/ANSI 305規格は、天然ひげケア処方のプレミアムなポジショニングを可能にし、市場の成長をさらに後押ししています。

激しい市場競争

先進地域における市場飽和は競争圧力を強め、利益率を圧迫するとともに、シェア維持のためのマーケティング投資拡大を必要としています。2025年6月に6ドル未満の価格帯で34の新製品を投入したスエーブのリローンチは、価値重視のポジショニング戦略を示しており、「デュプカルチャー」マーケティングを通じ、オラプレックスなどのプレミアムブランドに対する競争力ある価格設定を強調しています。プロクター・アンド・ギャンブル社のグルーミング部門は、2025年6月時点で数量ベース4%の増加にもかかわらず、純売上高が16億8,000万米ドルにとどまり、競合環境による価格圧力が見て取れます。さらに、小売業者がブランド品と同等の性能を低価格帯で実現する高度な処方を開発するプライベートブランド拡大が、ブランドメーカーを脅かしています。ハリーズやダラーシェーブクラブといったデジタルネイティブブランドは従来の流通モデルを破壊し、既存企業に消費者直販能力や定期購入サービスへの多額の投資を迫りました。こうした競争激化はユニリーバによるドクタースクワッチ買収などの大規模買収が示す通り、業界再編を加速させており、市場参入を目指す小規模独立ブランドにとって障壁となっています。

セグメント分析

シェービング製品は2025年に24.35%の市場シェアを維持し、確立された消費習慣とリピート購入パターンを反映しています。一方、スキンケア製品は2031年までにCAGR8.11%を達成し、男性グルーミングの優先順位における根本的な変化を示しています。プレシェーブ、アフターシェーブ、カミソリ・刃といった伝統的なシェービングカテゴリーは、パナソニックの「シリーズ900」のような技術革新の恩恵を受けています。同製品は毎分7万回のカット動作とレスポンシブひげセンサー+テクノロジーを特徴としています。ヘアケア製品は、薄毛対策に特化した処方により着実な成長を見せており、ハイランドの「ザ・ウォッシュ」は予防ケアに投資する35歳未満の消費者層をターゲットとしています。香水やボディケアを含むその他の製品タイプは、著名人との提携を通じて拡大しています。2025年5月に世界のアンバサダーとしてドウェイン・ウェイド氏を迎えたアラミスの「Intuition」発売がその好例です。

スキンケア市場の加速は、洗練された消費者教育と、ニキビ・老化・敏感肌といった特定のお悩みに対応したターゲット処方によるものです。2023年3月に発売されたダヴメン+ケア「アドバンストケアフェイス+ボディ」コレクションは市場の成熟度を示しており、男性の80%が高度なスキンケアソリューションに関心を示しています。同様に、2024年8月にAmazonプレミアムビューティーへ進出を果たしたラボシリーズは、臨床的有効性を求める知識層向けに科学的に裏付けられた処方開発を推進しています。特許開発事例としては、皮膚刺激の懸念を解消しスキンケア採用を促進する、リシンを用いたウルシオール誘発性接触皮膚炎治療組成物が挙げられます。さらに、MoCRA(医薬品・化粧品・食品規制法)に基づくFDA化粧品規制は安全基準を確立し、専門的スキンケア処方に消費者信頼を構築。これによりカテゴリー全体でプレミアム価格設定が支えられています。

2025年時点でマスマーケット製品は72.85%の市場シェアを占め、幅広い消費者へのアクセス性と確立された流通網を示しています。一方、プレミアムセグメントは2031年までCAGR7.52%を達成し、優れた処方と体験への投資意欲を反映しています。プレミアムポジショニングは、AI駆動型コーチングと精密設計を特徴とするフィリップス社の「i9000プレステージウルトラ」のような技術革新の恩恵を受けています。一方、マス市場戦略はバリューポジショニングに焦点を当てており、2025年3月に6米ドル未満の34製品で再発売されたスエーブ社の事例が代表的です。これは、手頃な価格帯でプレミアムな性能を求める消費者をターゲットとしています。

プレミアム市場の成長加速は、消費者の洗練化と、優れた結果をもたらすパーソナライズされた体験への投資意欲に起因します。例えば、2025年6月に15億米ドルの評価額を獲得したドクター・スクワッチは、プレミアムな自然派ポジショニングの有効性を示しており、ユニリーバによる買収は高利益率製品の国際展開を目的としています。同様に、スコッチ・ポーターが米国で最も成長著しい男性グルーミングブランドとして認知されていることは、コミュニティへの影響力と総合的なウェルネスアプローチを重視しながら70%超の成長を達成したプレミアムポジショニングの成功を反映しています。さらに、特許保護は技術的差別化によるプレミアム価格設定を可能にしており、ロレアルは2023年にスマートグルーミング技術を含む370件以上の国際特許出願を行っています。大衆市場における回復力は流通アクセスの容易さとリピート購入パターンに起因しますが、プライベートブランド拡大による利益率の圧迫は、競争優位性を維持するための継続的なイノベーションを必要としています。

地域別分析

文化的ニュアンス、経済動向、進化する消費者嗜好によって形作られる地域的な力学が、世界の男性用グルーミング製品市場を定義しています。プレミアム製品への深い理解と確立されたブランド環境を有する欧州は、最大の市場シェアを占めています。2025年時点で欧州は世界収益の27.45%を占め、伝統的な高級ブランド、EU統一化粧品規制、安定したコスト構造がこれを支えています。西欧では高級フレグランスや最先端のアンチエイジングソリューションが好まれる一方、東欧ではコスト効率の高い製造基盤と急成長する中産階級の需要が特徴です。北欧発のサステナビリティ動向は急速に広がり、再生可能包装の普及を推進しています。英国、ドイツ、イタリアなどの国々は、天然由来成分の配合や確立されたグルーミング習慣に対する需要を牽引しています。北米は欧州に次ぐ成長地域であり、富裕層の消費者基盤、高まるブランド認知度、そして「メトロセクシャル」動向の台頭により、ハイテクグルーミング機器やサブスクリプションサービスへの顕著な投資が行われています。

中東・アフリカ地域では、驚異的な8.36%のCAGRにより、最も成長が著しい地域として位置づけられています。ドバイの戦略的物流拠点やサウジアラビアの「ビジョン2030」小売イニシアチブが、世界のグルーミングブランドの進出を後押ししています。若年層中心の都市人口、ソーシャルメディアの影響力拡大、観光業の急成長といった要因が消費を牽引しています。南アフリカは重要な流通拠点として機能する一方、ナイジェリアは購買力の安定化を条件に、将来的な成長が期待されています。

北米は技術主導のグルーミングソリューションと急成長するD2Cブランドの最前線にあります。サントリーの「KIZEN」保湿剤は米国での試用で90%の満足度を獲得し、科学的に開発された輸入品に対する市場の受容性を示しています。カナダの消費者は米国と同様の嗜好を示し、特にクリーンラベル製品を好みます。一方、メキシコのマキラドーラ制度は国境付近でのカミソリ組立を促進しています。アジア太平洋地域では二つの傾向が見られます。日本と韓国がイノベーションをリードする一方、インドと中国は規模拡大を牽引し、毎年数百万人の新規参入者が男性グルーミング市場に加わっています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 男性向けスキンケアおよび専門的なルーティンの拡大

- ひげケアおよびスタイリング市場の成長

- グルーミングツールにおける技術革新

- 自然派・オーガニック製品の台頭

- パーソナライゼーションとカスタマイゼーション

- プレミアム化動向

- 市場抑制要因

- 激しい市場競争

- 包装に関連する環境問題

- 原材料コストの変動

- アレルギー反応および皮膚過敏症

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品タイプ別

- スキンケア製品

- 洗顔料

- 保湿剤

- フェイスマスク

- その他のスキンケア製品

- ヘアケア製品

- シャンプーおよびコンディショナー

- スタイリング製品

- ヘアカラー剤

- その他のヘアケア製品

- シェービング製品

- プレシェーブ

- シェービングクリーム

- プレシェーブオイル

- シェービングソープ

- その他のプレシェーブ製品

- シェービング後

- アフターシェーブ

- バーム

- その他のアフターシェーブ製品

- カミソリと刃

- プレシェーブ

- その他の製品タイプ

- スキンケア製品

- 価格帯別

- マス

- プレミアム

- カテゴリー別

- 従来型

- ナチュラル&オーガニック

- 流通チャネル別

- スーパーマーケット/ハイパーマーケット

- コンビニエンスストア

- 専門店

- オンライン小売店

- その他の小売チャネル

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- チリ

- その他南米

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- スウェーデン

- ベルギー

- ポーランド

- オランダ

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- タイ

- シンガポール

- インドネシア

- 韓国

- オーストラリア

- ニュージーランド

- その他アジア太平洋地域

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

- ナイジェリア

- エジプト

- モロッコ

- トルコ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Procter & Gamble Co.

- Beiersdorf AG

- L'Oreal SA

- Edgewell Personal Care Co.

- Unilever PLC

- Natura & Co Holding SA

- LVMH Moet Hennessy Louis Vuitton SA

- Chanel Ltd.

- Coty Inc.

- Combe Inc.

- Koninklijke Philips N.V.

- Panasonic Corp.

- Harry's Inc.

- Dollar Shave Club

- Beardbrand LLC

- Marico Ltd.

- Scotch Porter LLC

- Johnson & Johnson Services Inc.

- Kao Corp.

- Braun GmbH

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日