バンカー燃料:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Bunker Fuel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1687424

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

バンカー燃料の市場規模は2025年に1,536億5,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは2.9%で、2030年には1,772億6,000万米ドルに達すると予測されます。

主なハイライト

- 中期的には、LNG取引の増加がバンカー燃料の需要を押し上げると予想されます。LNGは主に産業、商業、住宅分野の電力セクター向けに取引されています。中国やインドのような石炭依存度の高い国々は、中東やロシア、オーストラリア、ナイジェリアのような少数の国からの天然ガスの輸入量を増やすことで、徐々にクリーンなエネルギーへと移行しつつあります。

- 一方、環境問題への懸念や海運業からの排出ガスに関する厳しい規制により、予測期間中は重質バンカー燃料、特に高硫黄燃料油の使用が制限されると予想されます。

- とはいえ、アジア太平洋や中東・アフリカなどの地域にまたがる新興諸国の経済業績の改善に伴い、海上輸送の需要と運航船舶の数は増加すると予想され、今後数年間、バンカー燃料市場のプレーヤーに大きな成長機会を提供します。

- 予測期間中、アジア太平洋が市場を独占し、需要の大半は中国やインドのような国々から生み出されると予想されます。

バンカー燃料市場の動向

LNGはバンカー燃料として大幅な市場成長が見込まれる

- 世界のLNGバンカリング市場は、温室効果ガスの排出を削減できることからクリーンエネルギーへの需要が高まる中、世界のLNG使用量の増加に牽引され、過去10年間で発展してきました。

- 現在運航中の船舶をLNGベースの船舶に改造するのは非常に高価です。したがって、経済的に実行可能ではないです。しかし、新しい排出規制が適用されれば、LNGベースの船舶の運航コストは、すべての代替燃料の中で最も低くなると予想されます。さらに、LNG推進への漸進的な移行は、重油、舶用ガス油、舶用ディーゼル油などで船舶に燃料を供給する従来の方法よりも有利です。LNGベースの推進力は二酸化炭素排出量を大幅に削減し、船舶の運航効率を高める。

- 燃料としてのLNG需要は2030年までに3,000万トンに増加すると予想されており、欧州、アジア、北米では、増加するガスエンジン船隊に対応するため、LNGバンカー船を増設しています。造船所に発注されているこれらの大容量LNGバンカー船(LNGBV)は、主要LNGターミナルで積荷を積み、ガスエンジン搭載の外航船に燃料を補給するよう設計されています。

- 2024年2月現在、LNGアクティブバンカー船は48隻で、2022年より11隻多いです。全船隊のうち半数近くが欧州で、その他はアジアと北米で操業しています。2024年末までには、LNGバンカリング船隊の数は55隻に達し、2024年だけで合計67,900cmの容量が追加される見込みです。

- 船主、特に欧州海域やアメリカ海域で操業する船主は現在、従来型船よりもLNGベースの船を好んでいます。さらに、LNG燃料船はばら積み船の市場にはあまり浸透していないです。ばら積み船は重い荷物を運ぶように設計されており、LNG技術がこの種の船に適用されるのは比較的新しいからです。ばら積み船は、稼働中の船舶の中で最大のシェアを占めています。

- さらに、燃料としてLNGを使用することは、実績があり、商業的に利用可能なソリューションです。LNGは、特に排出ガス規制がますます強化される船舶にとって、非常に大きなメリットをもたらします。中期的には従来型の石油ベースの燃料が大半の船舶の主要な燃料選択肢であり続けると予想されますが、長期的なシナリオではLNGが一般的な選択肢になると思われます。

- 2024年4月、技術グループであるバルチラ傘下のバルチラ・ガス・ソリューションズは、スペインのガス網を所有・運営するエナガスの子会社で、スペインの船主であるスケール・ガス向けに建造中の1万2500m3のLNGバンカリング新造船に荷役システムを供給すると発表しました。この船舶は、スペイン交通・モビリティ・都市計画省による復興・変革・強靭化計画の一環である「持続可能なデジタル交通支援プログラム」の共同出資によるものです。

- LNGは従来の燃料よりも比較的安価で、石油ベースの船舶燃料に比べて温室効果ガス排出量を23%削減できるため、世界の脱炭素目標の達成に貢献します。これらの要因から、LNGは将来的に最も人気のある船舶用燃料になると予測されています。

アジア太平洋が市場を独占する見込み

- アジア太平洋は、インド、中国、シンガポール、日本といった国々の巨大な海上貿易の潜在力により、バンカー燃料市場を独占すると予想されます。

- 2023年現在、中国は輸出額で第1位、輸入額で第2位です。2023年、中国は約2兆5,000億米ドルの商品を輸入し、3兆3,000億米ドルを輸出しました。中国の主な輸出品は、機械・電気機器、自動車部品、化学・プラスチック、鉄鋼製品、家具などです。

- オーストラリアは、世界最大のLNG輸出国のひとつです。LNG輸出の増加は、オーストラリアの国際貿易の成長を支えています。LNGの需要は世界的に大幅に増加しているため、輸出量は今後数年間で増加する可能性が高いです。

- 国際貿易と国内貿易における海洋部門のシェアを高めるため、インド政府は2035年までに220億米ドルを投資し、既存港の近代化と新港の建設を行うと発表しました。港湾インフラ開発により、予測期間中にアジア太平洋の海事産業と船舶用燃料サプライヤーの需要が増加すると予想されます。

- 2024年2月、LNGバンカー船の用船者であるパビリオン・エナジー社は、LNGバンカー船Brassavolaが初のSTS(Ship to Ship)LNGバンカーオペレーションを完了したと発表しました。Brassavolaは、リオ・ティントが傭船した二重燃料ばら積み船Mount ApiにLNGを引き渡しました。

- 従って、前述の要因から、予測期間中、アジア太平洋がバンカー燃料市場を独占すると予想されます。

バンカー燃料産業の概要

世界のバンカー燃料市場は断片化されています。市場の主要企業(順不同)には、Gazpromneft Marine Bunker LLC、ExxonMobil Corporation、Shell PLC、TotalEnergies SE、BP PLCなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模および需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 世界のLNG貿易の増加

- 発電用天然ガスへの依存度の高まり

- 抑制要因

- 環境問題への懸念と海運業からの排出に関する厳しい規制

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 投資分析

第5章 市場セグメンテーション

- 燃料タイプ

- 高硫黄燃料油(HSFO)

- 超低硫黄燃料油(VLSFO)

- 海洋ガス油(MGO)

- 液化天然ガス(LNG)

- その他の燃料

- 船舶タイプ

- コンテナ

- タンカー

- 一般貨物船

- バルクキャリアー

- その他の船種

- 地域

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- ノルディック

- トルコ

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ナイジェリア

- カタール

- エジプト

- その他中東とアフリカ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- 燃料サプライヤー

- ExxonMobil Corporation

- Shell PLC

- Gazpromneft Marine Bunker LLC

- BP PLC

- PJSC Lukoil Oil Company

- TotalEnergies SE

- Chevron Corporation

- Clipper Oil

- Gulf Agency Company Ltd

- Bomin Bunker Holding GmbH & Co. KG

- 船舶オーナー

- AP Moeller Maersk AS

- Mediterranean Shipping Company SA

- China COSCO Shipping Corporation Limited

- CMA CGM Group

- Hapag-Lloyd AG

- Ocean Network Express

- Evergreen Marine Corp Taiwan Ltd

- Yang Ming Marine Transport Corporation

- HMM Co. Ltd

- Pacific International Lines Pte Ltd

- 他の主要企業のリスト

- 市場ランキング分析

- 燃料サプライヤー

第7章 市場機会と今後の動向

- 海上輸送需要の高まりと運航船舶数の増加

目次

Product Code: 62667

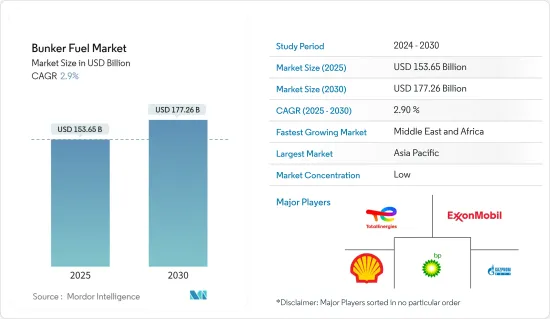

The Bunker Fuel Market size is estimated at USD 153.65 billion in 2025, and is expected to reach USD 177.26 billion by 2030, at a CAGR of 2.9% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, increasing LNG trade is expected to boost the demand for bunker fuel. LNG is majorly traded for the power sector in industrial, commercial, and residential segments. Countries with high coal dependencies, such as China and India, are gradually moving toward cleaner energy by increasing the import volume of natural gas from the Middle East and a few other nations, like Russia, Australia, and Nigeria.

- On the other hand, environmental concerns and the strict regulations related to emissions from the maritime industry are anticipated to limit the usage of heavy bunker fuels, especially high sulfur fuel oil, during the forecast period.

- Nevertheless, with the improved economic performance of developing countries across regions such as Asia-Pacific and Middle East and Africa, the demand for marine transportation and the number of ships in operation are expected to increase, offering significant growth opportunities for players in the bunker fuels market over the coming years.

- Asia-Pacific is expected to dominate the market during the forecast period, with the majority of the demand being generated from countries like China and India.

Bunker Fuel Market Trends

LNG Likely to Witness Significant Market Growth as a Bunker Fuel

- The global LNG bunkering market has evolved over the past decade, driven by the increase in global LNG usage amid growing demand for clean energy due to its ability to reduce greenhouse gas emissions.

- The conversion of the current operating vessels into LNG-based vessels is highly expensive. Hence, it is not economically viable. However, the operational cost of LNG-based vessels is expected to be the lowest among all the fuel alternatives once the new emission regulations become applicable. Further, a gradual shift to LNG for propulsion is more advantageous than the traditional methods of fueling ships with heavy fuel oil, marine gas oil, marine diesel oil, etc. LNG-based propulsion reduces the carbon footprint significantly and increases a ship's operational efficiency.

- With demand for LNG as a fuel expected to rise to 30 million tonnes by 2030, Europe, Asia, and North America are adding LNG bunkering vessels to keep pace with the swelling gas-powered fleet. These larger capacity LNG bunker vessels (LNGBVs) on order at shipyards are designed to load at major LNG terminals and refuel gas-powered ocean-going tonnage.

- As of February 2024, there were 48 LNG active bunkering vessels, 11 more than in 2022. Out of the total fleet, nearly half operate in Europe, while the rest operate in Asia and North America. By the end of 2024, the number of LNG bunkering vessel fleets is likely to reach 55 units, with a total added capacity of 67,900 cm in 2024 alone.

- Shipowners, particularly those operating in the European or American Sea, now prefer LNG-based vessels over conventional vessels. Furthermore, LNG-fueled ships have not penetrated the market for bulk carriers to a significant extent, as these ships are designed to carry heavy loads, and LNG technology is relatively new to apply for this type of vessel. The bulk carriers amount to the largest share of the in-operation ships.

- Moreover, the use of LNG as a fuel is both a proven and commercially available solution. LNG offers enormous advantages, especially for ships in the light of ever-tightening emission regulations. Conventional oil-based fuels are expected to remain the primary fuel option for most ships in the mid-term, while LNG is likely to become a popular choice in the long-term scenario.

- In April 2024, Wartsila Gas Solutions, part of the technology group Wartsila, announced that it would supply the cargo handling system for a new 12,500 m3 LNG bunkering vessel being built for Spanish shipowner Scale Gas, a subsidiary of Enagas, the owner and operator of Spain's gas grid. The vessel is co-financed by the Support for Sustainable and Digital Transport Programme, part of the Recovery, Transformation and Resilience Plan from the Spanish Ministry of Transport, Mobility and Urban Agenda.

- LNG demand is likely to increase significantly in the forecast period as the order book for LNG vessels continues to increase due to it being relatively cheaper than conventional fuels and offering a 23% reduction in greenhouse gas emissions over oil-based marine fuel, which will aid in meeting global decarbonization goals. These factors project LNG to be the most popular marine fuel in the future.

Asia-Pacific Expected to Dominate the Market

- Asia-Pacific is expected to dominate the bunker fuels market due to the immense maritime trade potential of countries like India, China, Singapore, and Japan.

- As of 2023, China ranked first in terms of exported goods and second for imported goods by value. In 2023, China imported goods worth around USD 2.5 trillion and exported USD 3.3 trillion. China's major exports are mechanical and electric machinery and equipment and automotive products, including vehicle parts, chemicals and plastics, iron and steel articles, and furniture.

- Australia is among the biggest exporters of LNG globally. Rising LNG exports have supported the growth in international trade in Australia. The export volume is likely to rise in the coming years as the demand for LNG is increasing significantly worldwide.

- To increase the share of the marine sector in international and domestic trade, the Indian government announced an investment of USD 22 billion by 2035 to modernize its existing ports and build new ports. The port infrastructure development is expected to increase the demand from the maritime industry and marine fuel suppliers in Asia-Pacific during the forecast period.

- In February 2024, Pavilion Energy, charterer of LNG bunker vessels, announced that LNG bunker vessel Brassavola had completed its first ship-to-ship (STS) LNG bunkering operation. In its maiden STS LNG bunkering operation, Brassavola delivered LNG to Rio Tinto chartered dual-fueled bulk carrier Mount Api.

- Therefore, in line with the aforementioned factors, Asia-Pacific is expected to dominate the bunker fuels market during the forecast period.

Bunker Fuel Industry Overview

The global bunker fuels market is fragmented. Some of the major players in the market (in no particular order) include Gazpromneft Marine Bunker LLC, ExxonMobil Corporation, Shell PLC, TotalEnergies SE, and BP PLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increased LNG Trade Worldwide

- 4.5.1.2 Increasing Dependencies over Natural Gas for Power Generation

- 4.5.2 Restraints

- 4.5.2.1 Environmental Concerns and the Strict Regulations Related to Emissions from the Maritime Industry

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Fuel Type

- 5.1.1 High Sulfur Fuel Oil (HSFO)

- 5.1.2 Very Low Sulfur Fuel Oil (VLSFO)

- 5.1.3 Marine Gas Oil (MGO)

- 5.1.4 Liquefied Natural Gas (LNG)

- 5.1.5 Other Fuel Types

- 5.2 Vessel Type

- 5.2.1 Containers

- 5.2.2 Tankers

- 5.2.3 General Cargo

- 5.2.4 Bulk Carriers

- 5.2.5 Other Vessel Types

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Spain

- 5.3.2.5 NORDIC

- 5.3.2.6 Turkey

- 5.3.2.7 Russia

- 5.3.2.8 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Malaysia

- 5.3.3.6 Thailand

- 5.3.3.7 Indonesia

- 5.3.3.8 Vietnam

- 5.3.3.9 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Nigeria

- 5.3.5.5 Qatar

- 5.3.5.6 Egypt

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Fuel Suppliers

- 6.3.1.1 ExxonMobil Corporation

- 6.3.1.2 Shell PLC

- 6.3.1.3 Gazpromneft Marine Bunker LLC

- 6.3.1.4 BP PLC

- 6.3.1.5 PJSC Lukoil Oil Company

- 6.3.1.6 TotalEnergies SE

- 6.3.1.7 Chevron Corporation

- 6.3.1.8 Clipper Oil

- 6.3.1.9 Gulf Agency Company Ltd

- 6.3.1.10 Bomin Bunker Holding GmbH & Co. KG

- 6.3.2 Ship Owners

- 6.3.2.1 AP Moeller Maersk AS

- 6.3.2.2 Mediterranean Shipping Company SA

- 6.3.2.3 China COSCO Shipping Corporation Limited

- 6.3.2.4 CMA CGM Group

- 6.3.2.5 Hapag-Lloyd AG

- 6.3.2.6 Ocean Network Express

- 6.3.2.7 Evergreen Marine Corp Taiwan Ltd

- 6.3.2.8 Yang Ming Marine Transport Corporation

- 6.3.2.9 HMM Co. Ltd

- 6.3.2.10 Pacific International Lines Pte Ltd

- 6.3.3 List of Other Prominent Companies

- 6.3.4 Market Ranking Analysis

- 6.3.1 Fuel Suppliers

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Risisng Demand for Marine Transportation and Increasing Number of Ships in Operation

バンカー燃料:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日