|

市場調査レポート

商品コード

1636167

日本のバンカー燃料:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Japan Bunker Fuel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 日本のバンカー燃料:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

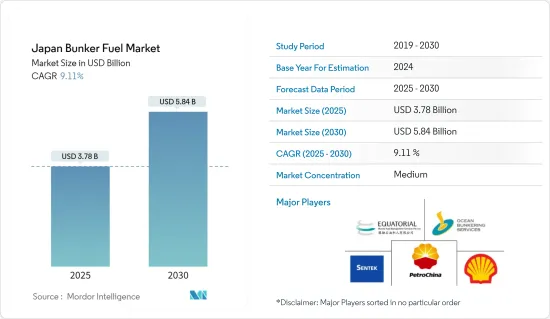

日本のバンカー燃料市場規模は2025年に37億8,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは9.11%で、2030年には58億4,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、より厳しい環境規制の実施によるクリーンなバンカー燃料への需要の高まりや、各地域での電力セクター向けLNG取引の拡大といった要因が、2024~2029年にかけて市場を牽引すると予想されます。

- 一方、バンカー燃料と原油のコストの変化は、市場の成長を妨げると予想されます。

- 就航船舶数と海上輸送需要は、2024~2029年にかけていくつかの将来的な市場機会を生み出すと予想されます。

日本の燃料油市場の動向

超低硫黄燃料油(VLSFO)が大幅な成長を遂げる展望

- バンカー燃料は硫黄分が高く、有害なガスを排出する可能性があります。硫黄濃度を下げるには様々な方法があります。超低硫黄燃料油はこの種の燃料の一つです。2020年1月にIMO規制が施行されるため、硫黄分0.5%以下の超低硫黄燃料油(VLSFO)のニーズが高まっている

- 高硫黄燃料油(HSFO)バンカー燃料市場の大半は、まもなく低硫黄代替燃料に取って代わられると予想されています。市場で販売されているVLSFOの大半は、残留成分と留出成分を、粘度や硫黄含有量の異なるカッターと組み合わせ、仕様に適合した製品を製造したものです。

- 日本では、VLSFOの需要増加を克服するため、製油所の数を増やすことに注力しています。2024年1月現在、日本には20の製油所があります。日本の精製能力は323万b/dで、1980年代前半の600万b/dと比較しています。日本では、VLSFOの需要を満たすために製油所の数を増やし、以前の数に再び到達するための戦略を立てています。これらの戦略はすべて、2024~2029年の間に増加する需要を満たす可能性が高いです。

- 2023年時点で、日本のバンカー需要の70%は外航船舶向けの低硫黄燃料油(VLSFO)です。これは製油所の能力により左右されます。政府は製油所の能力を増強する計画を複数の組織と立てています。2024年2月、コスモスは、製油所の能力が2024-25年度には90%を超える可能性が高いと発表した(23-24年度の87.5%)。

- さらに2023年8月、Pemexは、国際協力機構(JICA)とサステイナブルソリューション企業であるAdaptexと、超低硫黄燃料油(VLSFO)を使用する製油所において、より高いエネルギー効率で操業するための革新的技術の計画を実施する契約を締結したと発表しました。こうした合意はすべて、2024~2029年にかけてVLSFOの需要を増加させ、同組織に将来的な機会をもたらすものです。

- したがって、高い国内需要、最近の動向、今後の製油所プロジェクトに後押しされ、この地域は2024~2029年にかけて市場の需要を牽引すると予想されます。

バンカー燃料としてのLNGが大幅な成長を遂げる可能性が高い

- 日本のLNGバンカリング産業は、世界のLNG使用量の増加、クリーンエネルギー需要、温室効果ガス排出を最小化する機会を原動力として、過去10年間に発展してきました。LNG船は徐々に需要が高まっており、天然ガス価格の低下はこの種の船の市場拡大の始まりを告げるものでした。

- 現在運航されている船舶をLNG船へ転換するには、多大なコストがかかります。したがって、経済的には実現不可能です。新たな公害規制が施行された後、LNGを燃料とする船舶は、すべての燃料オプションの中で最も低い運航コストになると予想されます。さらに、重油、舶用ガス油、舶用ディーゼル油といった従来の船舶燃料供給方法からLNG推進への段階的移行は、より有利です。船舶の運航効率は向上し、二酸化炭素排出量はLNG推進によって大幅に削減されます。

- 各国は現在、新しい環境規制により、LNG動力運搬船の使用に力を入れています。2024年2月には、史上初のLNGを動力源とするケープサイズバルカーが日本に引き渡される予定です。日本郵船の調査によると、この船は日本の造船所で建造された初のケープサイズのLNG燃料ばら積み船です。日本郵船は、LNGフリートの拡充により、サプライチェーン全体の脱炭素化に取り組むとともに、日本郵船グループが掲げる「2021年度から2030年度までに温室効果ガス排出量を45%削減する」という目標を達成します。こうした開発により、2024~2029年にかけてバンカー燃料としてのLNGの需要が増加します。

- 世界エネルギーデータ統計によると、2022年のLNG輸入量は983億立方メートルと報告されており、2021年比で2.96%減少しています。政府が複数の契約を締結して製油所の能力増強に注力しているため、輸入量は今後数年間で増加する可能性が高いです。

- さらに、2023年8月、LNG Japan Corp.は、オーストラリア沖の大規模天然ガスプロジェクトの株式に対して最大8億8,000万米ドルを支払うことに合意しました。スカボロープロジェクトでは、Woodside Energy Groupが所有者の10%を住友商事と双日が保有する合弁会社に譲渡します。さらに、同プロジェクトから2026年から10年間、年間12カーゴ、約90万トンの液化天然ガス(LNG)を供給する契約も結ばれました。これらの契約はすべて、2024~2029年の間にLNGの生産能力を増大させ、同組織に将来の機会をもたらすものです。

- したがって、高い国内需要、最近の動向、今後のプロジェクトに後押しされ、この地域は2024~2029年にかけて市場の需要を牽引すると予想されます。

日本のバンカー燃料産業概要

日本のバンカー燃料市場は半固体化しています。この市場の主要企業は以下の通りです。 PetroChina Company Limited, Ocean Bunkering Services(Pte)Ltd, Shell Eastern Trading(Pte)Ltd, Equatorial Marine Fuel Management Services Pte Ltd, and Sentek Marine & Trading Pte Ltd.

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:10億米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- LNG貿易の増加

- 海上輸送の増加

- 抑制要因

- 原油価格の変動

- 促進要因

- サプライチェーン分析

- PESTLE分析

第5章 市場セグメンテーション

- 燃料タイプ別

- 高硫黄燃料油(HSFO)

- 超低硫黄燃料油(VLSFO)

- 舶用ガスオイル(MGO)

- その他の燃料タイプ

- 船舶タイプ別

- コンテナ

- タンカー

- 一般貨物船

- バルクキャリアー

- その他の船種

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- 燃料サプライヤー

- PetroChina Company Limited

- Ocean Bunkering Services(Pte)Ltd

- Sentek Marine & Trading Pte Ltd

- Equatorial Marine Fuel Management Services

- Shell Eastern Trading(Pte)Ltd

- 船舶所有者

- Cosco Shipping Lines Co Ltd

- Orient Overseas Container Line(OOCL)

- Parakou Group

- Nan Fung Group

- Mediterranean Shipping Company

- The Great Eastern Shipping Co. Ltd

- 燃料サプライヤー

- 市場ランキング/シェア分析

第7章 市場機会と今後の動向

- 海上輸送需要

The Japan Bunker Fuel Market size is estimated at USD 3.78 billion in 2025, and is expected to reach USD 5.84 billion by 2030, at a CAGR of 9.11% during the forecast period (2025-2030).

Key Highlights

- In the medium period, factors such as rising demand for cleaner bunker fuels due to implementing more restrictive environmental regulations and the growing trade of LNG for the power sector in the regions are expected to drive the market between 2024 and 2029.

- On the other hand, changes in the cost of bunker fuel and crude oil are expected to hinder the market's growth.

- Nevertheless, the number of ships in service and the demand for maritime transportation are expected to create several future market opportunities from 2024 to 2029.

Japan Bunker Fuel Market Trends

Very Low Sulfur Fuel Oil (VLSFO) is Expected to Witness Significant Growth

- Bunker fuels have a high sulfur content and may emit harmful fumes. Different methods can be employed to lower sulfur concentration. Ultra-low-sulfur fuel oil is one of the varieties of this kind of fuel. With an IMO regulation going into effect in January 2020, there is a growing need for very low sulfur fuel oil (VLSFO) with a sulfur concentration of less than 0.5%.

- The majority of the market for high-sulfur fuel oil (HSFO) bunker fuel is anticipated to be replaced soon by low-sulfur substitutes. The majority of VLSFO sold on the market is made up of residual and distillate components combined with different cutters with different viscosities and sulfur contents to produce a product that meets specifications.

- The nation is focusing on increasing the number of refineries to overcome the increased demand for VLSFO. As of January 2024, Japan had 20 refineries. The country's refining capacity is 3.23 million b/d, compared to 6 million b/d in the early 1980s. The country is making strategies to increase the number of refineries to fulfill the demand for VLSFO and reach the previous numbers again. All these strategies are likely to fulfill the increased demand between 2024 and 2029.

- As of 2023, Japan's total bunker demand involved 70% of low-sulfur fuel oil (VLSFO) for deliveries of ocean-going vessels. This is more dependent on the refinery's capacity. The government is making plans to increase the refinery's capacity with several organizations. In February 2024, Cosmos announced that the refinery capacity is likely to be above 90% during FY2024-25 compared to 87.5 % in FY23-24.

- Moreover, in August 2023, Pemex announced that it had inked a deal with the Japan International Cooperation Agency (JICA) and the sustainable solutions company Adaptex to implement a plan for innovative technology to operate with greater energy efficiency in the refinery involving very low-sulfur fuel oil (VLSFO). All these types of agreements increase the demand for VLSFO between 2024 and 2029 and create future opportunities for the organization.

- Hence, driven by high domestic demand, recent developments, and upcoming oil refinery projects, the region is expected to drive the demand for the market from 2024 to 2029.

LNG as a Bunker Fuel is Likely to Witness Significant Growth

- The Japan LNG bunkering industry has developed over the last decade, driven by increased global LNG usage, clean energy demand, and the opportunity to minimize greenhouse gas emissions. LNG-powered vessels are becoming progressively higher in demand, and lower natural gas prices signaled the start of an expansion in the market for these kinds of vessels.

- The cost of converting the current operational vessels to LNG-powered vessels is significant. It is, therefore, not feasible economically. After the new pollution restrictions take effect, LNG-based vessels are anticipated to have the lowest operating costs of all the fuel options. Furthermore, a gradual transition from conventional ship fueling methods, such as heavy fuel oil, marine gas oil, and marine diesel oil, to LNG propulsion is more advantageous. The ship's operational efficiency has increased, and its carbon footprint is significantly reduced with LNG-based propulsion.

- Countries are now focusing on using LNG power carriers owing to the new environmental regulations. In February 2024, the first-ever capsized bulk carrier powered by LNG was to be delivered to Japan. The ship is the first Capesize LNG-fueled bulk carrier ever constructed at a Japanese shipyard, according to an NYK investigation. Expanding its fleet of LNG-fueled ships, NYK is taking on the issue of decarbonizing a complete supply chain while meeting the NYK Group's target of a 45% reduction in GHG emissions from FY2021 to FY2030. These developments increase the demand for LNG as a bunker fuel between 2024 and 2029.

- According to the Statistical Review of World Energy Data, LNG imports were reported to be 98.3 billion cubic meters in 2022, which was reduced by 2.96% compared to 2021. The imports are likely to increase in the coming years as the government focuses on increasing the refinery capacity by signing multiple deals.

- Furthermore, in August 2023, LNG Japan Corp. agreed to pay up to USD 880 million for a stake in a massive natural gas project off the coast of Australia. The Scarborough project will see Woodside Energy Group give up 10% of its ownership to the joint venture, which Sumitomo Corp. and Sojitz Corp hold. Furthermore, a deal was reached to deliver 12 cargoes, or roughly 900,000 tons, of liquefied natural gas (LNG) annually for ten years starting in 2026 from the project. All these types of agreements increase the capacity of LNG between 2024 and 2029 and create future opportunities for the organization.

- Hence, driven by high domestic demand, recent developments, and upcoming projects, the region is expected to drive the demand for the market from 2024 to 2029.

Japan Bunker Fuel Industry Overview

The Japanese bunker fuel market is semi-consolidated. Some of the major players in this market are PetroChina Company Limited, Ocean Bunkering Services (Pte) Ltd, Shell Eastern Trading (Pte) Ltd, Equatorial Marine Fuel Management Services Pte Ltd, and Sentek Marine & Trading Pte Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing LNG Trade

- 4.5.1.2 Rising Marine Transportation

- 4.5.2 Restraints

- 4.5.2.1 Fluctuations in Crude Oil Prices

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

5 MARKET SEGMENTATION

- 5.1 By Fuel Type

- 5.1.1 High Sulfur Fuel Oil (HSFO)

- 5.1.2 Very-low Sulfur Fuel Oil (VLSFO)

- 5.1.3 Marine Gas Oil (MGO)

- 5.1.4 Other Fuel Types

- 5.2 By Vessel Type

- 5.2.1 Containers

- 5.2.2 Tankers

- 5.2.3 General Cargo

- 5.2.4 Bulk Carrier

- 5.2.5 Other Vessel Types

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Fuel Suppliers

- 6.3.1.1 PetroChina Company Limited

- 6.3.1.2 Ocean Bunkering Services (Pte) Ltd

- 6.3.1.3 Sentek Marine & Trading Pte Ltd

- 6.3.1.4 Equatorial Marine Fuel Management Services

- 6.3.1.5 Shell Eastern Trading (Pte) Ltd

- 6.3.2 Ship Owners

- 6.3.2.1 Cosco Shipping Lines Co Ltd

- 6.3.2.2 Orient Overseas Container Line (OOCL)

- 6.3.2.3 Parakou Group

- 6.3.2.4 Nan Fung Group

- 6.3.2.5 Mediterranean Shipping Company

- 6.3.2.6 The Great Eastern Shipping Co. Ltd

- 6.3.1 Fuel Suppliers

- 6.4 Market Ranking/Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Demand for Marine Transportation