|

市場調査レポート

商品コード

1630442

南米のバンカー燃料:市場シェア分析、産業動向、成長予測(2025年~2030年)South America Bunker Fuel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 南米のバンカー燃料:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

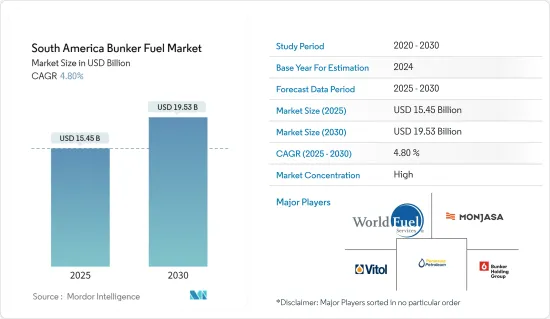

南米のバンカー燃料の市場規模は2025年に154億5,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは4.8%で、2030年には195億3,000万米ドルに達すると予測されます。

主なハイライト

- 中期的には、重要物資の海上輸送の増加や、よりクリーンなバンカー燃料の需要を促進する厳しい環境規制の実施といった要因が、南米のバンカー燃料市場の成長を牽引します。

- 一方、石油市場の変動はバンカー燃料サプライヤーの収益性に影響を与え、計画や投資を困難にする可能性があるため、バンカー燃料市場に大きな影響を与えると予想されます。

- とはいえ、クリーンなバンカー燃料の使用の増加は、南米のバンカー燃料市場に大きな機会を生み出します。

- ブラジルは、原油生産量の大幅な増加や同国からの輸出の着実な増加などの要因により、同地域のバンカー燃料市場を独占すると予想されます。

南米のバンカー燃料市場動向

超低硫黄燃料油(VLSFO)が大きく成長

- 国際海事機関(IMO)による船舶からの硫黄排出量削減の義務付けを受け、南アフリカのバンカー燃料市場における浅硫黄燃料油(VLSFO)の需要は近年大幅に増加しています。

- 2023年4月現在、南アフリカのバンカー燃料市場で使用されるVLSFOのほとんどが輸入品であるため、国内のバンカー燃料市場ではVLSFOの入手が特に逼迫しています。低硫黄燃料油は、ダーバン港、ポートエリザベス港、ケープタウン港、およびアルゴアベイ(ポートエリザベス沖とングクラ沖)の海上バンカリングで入手できます。

- 2022年12月から2023年4月までの価格変動は5%程度です。これとは対照的に、VLSFOの価格はより大きく変動しており、これがこの燃料の需要をさらに高めています。

- 2022年10月、船舶燃料業界専門の商品商社であるFUEL &MARINE OIL CORP(FAMOIL)は、ペルーでのオペレーションにバンカー配送船を追加しました。同社はタンカーEcomar IIを船隊に加えました。同船は、タララ、パイタ、バヨバル、サラベリー、チンボテ港ピスコ、サンニコラス、マタラニ、ロで超低硫黄燃料油(VLSFO)と高硫黄燃料油を供給します。

- さらに、南米市場におけるVLSFOの需要は、同地域で操業する船舶数の増加によっても牽引されています。これらの燃料が海洋生物に与える環境への影響に関する規制が厳しくなっていることも、結果的にVLSFOの需要を押し上げています。

- 全体として、IMOの硫黄キャップ実施後の需要増加などの要因により、予測期間中に市場は大きな成長を遂げると予想されます。

市場を独占するブラジル

- ブラジルはこの地域で最大の経済大国であり、予測期間中に最も急成長する経済大国となる見込みです。同国は、人口増加、工業化、都市化により、世界で最も急成長している国のひとつです。

- ブラジルからの石油輸出の増加は、南米のバンカー燃料市場を牽引する極めて重要な役割を果たすと予想されます。ブラジルは主要産油国として石油生産量を拡大しており、輸出の増加は同地域のバンカー燃料市場に大きな機会をもたらしています。

- 国際航路が南米海域を通過するため、船舶が使用するバンカー燃料の需要は急増すると予想されます。ブラジルは有力な石油輸出国として戦略的に重要な位置にあるため、南米におけるバンカー燃料の入手可能性と価格動向に影響を与える重要なプレーヤーとなっています。

- 例えば、2022年11月、ノルウェーのKanfer Shipping ASはNimofast Brasil S.A.とパートナーシップ契約を結び、2025年以降ブラジルで中小規模のLNG船とLNGバンカリングソリューションを確立します。LNG船とLNGバンカー船は、パラナ州にあるニモファストLNG輸入・配給ターミナルに常設されるFSUを経由して船積みされます。

- さらに、ブラジルからの石油輸出の増加は、この地域における海上貿易活動の活発化という幅広い動向と一致しています。船舶の往来が激しくなるにつれて、船舶の主要エネルギー源としてのバンカー燃料の需要も相応に増加すると予想されます。

- このバンカー燃料需要の急増は、世界貿易における南米の重要性の高まりを反映しているだけでなく、ブラジルのような石油輸出国が船舶燃料のような関連セクターの動向に大きな影響を与える可能性があるという、エネルギー市場の相互連関性を浮き彫りにしています。

- ブラジルは、回収可能な超深部石油埋蔵量が世界最大で、ブラジルの石油生産量の96.7%が海洋で生産されています。2022年の石油生産量は1億6,310万トンで、2021年の1億5,690万トンから増加しました。

- したがって、石油・ガス生産量の増加が見込まれる中、ブラジルとその他の地域との貿易活動はさらに増加すると予想されます。主要な国際取引は海上ルートを通じて行われるため、ブラジルは近い将来、バンカー燃料の新興市場になると予想されます。

- 上記の要因はすべて、予測期間中、同国がバンカー燃料の面でこの地域を支配するのに役立つと予想されます。

南米のバンカー燃料産業の概要

南米のバンカー燃料市場は半分断されています。主要企業(順不同)には、Bunker Holding A/S、Monjasa Holding A/S、AP Moeller Maersk A/S、World Fuel Services Corp、Peninsula Petroleum Ltd.などがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模および需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 南米における必需品の海上輸送の増加

- よりクリーンなバンカー燃料への支援政策

- 抑制要因

- 石油市場の不安定性

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 燃料タイプ別

- 高硫黄燃料油(HSFO)

- 超低硫黄燃料油(VLSFO)

- 海洋ガス油(MGO)

- 液化天然ガス(LNG)

- その他の燃料(メタノール、LPG、バイオディーゼル)

- 船舶タイプ別

- コンテナ

- タンカー

- 一般貨物

- バルクコンテナ

- その他の船舶タイプ

- 地域別

- ブラジル

- チリ

- アルゼンチン

- その他南米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Fuel Suppliers

- Vitol Holding BV

- Monjasa Holding A/S

- Bunker Holding A/S

- World Fuel Services Corp

- Peninsula Petroleum Ltd

- TotalEnergies SA

- Chevron Corporation

- Ship Owners

- AP Moeller Maersk A/S

- Mediterranean Shipping Company SA

- China COSCO Holdings Company Limited

- CMA CGM Group

- Hapag-Lloyd AG

- Ocean Network Express

- Fuel Suppliers

- Market Ranking/Share(%)Analysis

第7章 市場機会と今後の動向

- クリーン燃料の利用

目次

Product Code: 71505

The South America Bunker Fuel Market size is estimated at USD 15.45 billion in 2025, and is expected to reach USD 19.53 billion by 2030, at a CAGR of 4.8% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the ever-rising marine transportation of essential commodities and implementation of stricter environmental regulations driving the demand for cleaner bunker fuels drive the growth in the South American bunker fuel market.

- On the other hand, the oil market's volatility is significantly expected to affect the bunker fuel market as it can impact the profitability of bunker fuel suppliers and make planning and investing difficult.

- Nevertheless, the increase in the use of clean bunker fuels creates a significant opportunity for the South American bunker fuel market.

- Brazil is expected to dominate the bunker fuel market in the region owing to factors like substantial crude oil production and a steady rise in exports from the country.

South America Bunker Fuel Market Trends

Very Low Sulfur Fuel Oil (VLSFO) to Witness Significant Growth

- The demand for shallow sulfur fuel oil (VLSFO) in the South African Bunker fuel market has seen a significant rise in recent years, following the International Maritime Organization's (IMO) mandate on reducing sulfur emissions from ships.

- As of April 2023, VLSFO availability is particularly strained in the domestic bunker fuel market, as most of the VLSFO used in the South Africa bunker fuel market is imported. Low-sulfur fuel oil is available in the ports of Durban, Port Elizabeth, and Cape Town, as well as at offshore bunkering in AlgoaBay (off Port Elizabeth and Ngqura).

- Moreover, the price fluctuations for VLSFO in the region are lesser compared to their counterparts, as between December 2022 and April 2023, the changes in prices were recorded at around 5%. In contrast, the counterparts have registered more variance, which further adds to the demand for this fuel.

- In October 2022, FUEL & MARINE OIL CORP (FAMOIL), a commodity trading house specializing in the marine fuel industry, added a bunker delivery vessel to its operation in Peru. The company added the tanker Ecomar II to its fleet. The vessel supplies Very Low Sulfur Fuel Oil (VLSFO) and High Sulfur Fuel Oil at Talara, Paita, Bayovar, Salaverry, Chimbote ports Pisco, San Nicolas, Matarani, and Llo.

- Moreover, the demand for VLSFO in the South American market is also driven by the growing number of vessels operating in the region. The stricter regulations on the environmental impact of these fuels on marine life have consequently driven the demand for VLSFO.

- Overall, the market is expected to witness significant growth during the forecast period owing to factors like increasing demand, which spurred up after the implementation of the IMO sulfur cap.

Brazil to Dominate the Market

- Brazil is the largest economy in the region and is expected to be the fastest-growing economy in the forecast period. The country is one of the fastest-growing countries worldwide because of the increasing population, industrialization, and urbanization.

- The increasing exports of oil from Brazil are anticipated to play a pivotal role in driving the market for bunker fuel in South America. Brazil, as a major oil-producing nation, has been expanding its oil output, and the growing exports present a significant opportunity for the bunker fuel market in the region.

- As international shipping routes pass through South American waters, the demand for bunker fuel used by marine vessels is expected to surge. Brazil's strategic location as a prominent exporter of oil makes it a crucial player in influencing the availability and pricing dynamics of bunker fuel in South America.

- For instance, In November 2022, Norwegian company Kanfer Shipping AS signed a partnership deal with Nimofast Brasil S.A. to establish small and medium-scale LNG shipping and LNG bunkering solutions in Brazil from 2025 onwards. The LNG vessels and LNG bunker ships will be loaded via the permanently based FSU at the Nimofast LNG import- and distribution terminal in the state of Parana.

- Moreover, the rise in oil exports from Brazil aligns with the broader trend of increased maritime trade activities in the region. As shipping traffic intensifies, the demand for bunker fuel as the primary energy source for marine vessels is expected to witness a corresponding uptick.

- This surge in demand for bunker fuel not only reflects the growing importance of South America in global trade but also underscores the interconnected nature of energy markets, where oil-exporting countries like Brazil can significantly impact the dynamics of related sectors such as marine fuels.

- Brazil owns the largest recoverable ultra-deep oil reserves in the world, with 96.7% of Brazil's oil production produced offshore. In 2022, the oil production was 163.1 million tonnes, increased from 156.9 million tonnes in 2021.

- Hence, with the expected increase in oil and gas production, trading activities between Brazil and the rest of the world are expected to increase further. With major international trading activities carried out through the marine route, Brazil is expected to become the emerging market for bunker fuel in the near future.

- All of the above factors are expected to help the country dominate the region in terms of bunker fuel during the forecast period.

South America Bunker Fuel Industry Overview

The South American bunker fuel market is semi-fragmented. Some of the major companies (in no particular order) are Bunker Holding A/S, Monjasa Holding A/S, AP Moeller Maersk A/S, World Fuel Services Corp, and Peninsula Petroleum Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Rising Marine Transportation of Essential Commodities in South America

- 4.5.1.2 Supportive Policies for Cleaner Bunker Fuel

- 4.5.2 Restraints

- 4.5.2.1 Volatile Nature of Oil Market

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Fuel Type

- 5.1.1 High Sulfur Fuel Oil (HSFO)

- 5.1.2 Very Low Sulfur Fuel Oil (VLSFO)

- 5.1.3 Marine Gas Oil (MGO)

- 5.1.4 Liquefied Natural Gas (LNG)

- 5.1.5 Other Fuel Types (Methanol, LPG, and Biodiesel)

- 5.2 Vessel Type

- 5.2.1 Containers

- 5.2.2 Tankers

- 5.2.3 General Cargo

- 5.2.4 Bulk Container

- 5.2.5 Other Vessel Types

- 5.3 Geography

- 5.3.1 Brazil

- 5.3.2 Chile

- 5.3.3 Argentina

- 5.3.4 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Fuel Suppliers

- 6.3.1.1 Vitol Holding BV

- 6.3.1.2 Monjasa Holding A/S

- 6.3.1.3 Bunker Holding A/S

- 6.3.1.4 World Fuel Services Corp

- 6.3.1.5 Peninsula Petroleum Ltd

- 6.3.1.6 TotalEnergies SA

- 6.3.1.7 Chevron Corporation

- 6.3.2 Ship Owners

- 6.3.2.1 AP Moeller Maersk A/S

- 6.3.2.2 Mediterranean Shipping Company SA

- 6.3.2.3 China COSCO Holdings Company Limited

- 6.3.2.4 CMA CGM Group

- 6.3.2.5 Hapag-Lloyd AG

- 6.3.2.6 Ocean Network Express

- 6.3.1 Fuel Suppliers

- 6.4 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Utilization of Clean Bunker Fuels