|

市場調査レポート

商品コード

1687201

倉庫ロボット-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Warehouse Robotics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 倉庫ロボット-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

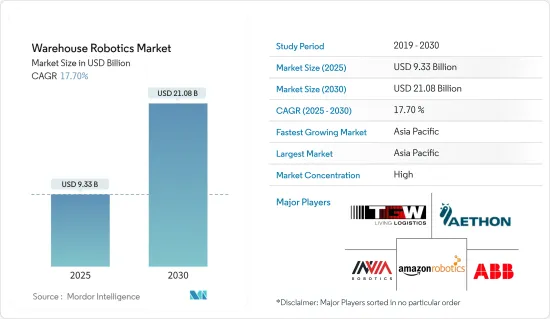

倉庫ロボットの市場規模は2025年に93億3,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは17.7%で、2030年には210億8,000万米ドルに達すると予測されます。

主要ハイライト

- SKU多様性の拡大が倉庫自動化を促進:倉庫ロボット市場は、SKUの多様性の急増を原動力に加速度的に成長しています。50%以上の企業が、ロングテールの消費者の需要に応えるためにSKU数を増やすと予想されています。この動向は、従来の倉庫モデルを再構築しており、大量パレット注文システムは、少量、複数SKU注文に取って代わられつつあります。この課題に対応するため、自動小口入出庫システム(AS/RS)が不可欠となっています。これらのシステムは、軽量クレーンを活用して、トート、ケース、木箱を管理し、保管を最適化し、重要な労働力と配送リソースを解放します。

- 倉庫規模の拡大:倉庫は2,000年の6万5,000平方フィートから2020年には20万平方フィート以上に拡大し、SKUの増加に対応しています。

- 小売業者と卸売業者の力学の変化:ジャストイン・タイム注文と消費者直送の流通は、大パレットの注文を減らし、自動化の必要性を加速させています。

- ピッキングロボットとAGV:最新世代のピッキングロボットと無人搬送車(AGV)は、大規模倉庫で膨大なSKU範囲にまたがる少量の注文を処理するのに理想的です。

- 投資の急増が技術の進歩を促進:資本の流入が倉庫自動化技術を前進させています。ベンチャーキャピタル企業はロボット工学に積極的に投資しており、倉庫ロボット工学の新興企業に対する資金調達額は2020年第1四半期に前年同期比57%増の3億8,100万米ドルに達しました。

- Locus Roboticsの拡大2020年6月、Locus Roboticsは研究開発の強化と欧州連合への進出のために4,000万米ドルを調達しました。

- Amazonのイノベーションハブ:Amazonがマサチューセッツ州に最先端のロボットハブを開発するために4,000万米ドルを投資したことで、自動化の進展が期待されます。

- Shopifyの戦略的買収:Shopifyは2019年に6 River Systemsを4億5,000万米ドルで買収し、クラウドベースのソフトウェアと協働モバイルロボットを組み込んでフルフィルメント機能を拡大しました。

- eコマースブームが採用を加速:eコマースの急成長は、倉庫ロボットの採用を促進し続けています。オンライン小売の急増に伴い、効率的な在庫管理とフルフィルメント業務が不可欠となっています。

- 市場規模の予測:Cowenは、eコマースにおける倉庫・物流ロボットの米国市場は2024年までに80億米ドル近くに達すると予測しています。

- 新しいフルフィルメントモデル:AlbertsonsとTakeoff Technologiesは、AIとロボットを活用した都市型フルフィルメントセンターを検査的に導入し、都市部の小規模倉庫業務を効率化します。

- Krogerの拡大:KrogerはOcadoと提携し、大規模なロボット駆動施設を備えたカスタマー・フルフィルメントセンターを最大20カ所開設する計画です。

- 労働力不足とコスト削減がイノベーションを促進:労働力不足への対応とオペレーションコストの削減のために、倉庫ロボットの活用が進んでいます。自動化は、不必要な労働力の移動を減らし、オペレーションを合理化することで、効率を向上させます。

- 無駄な動作コスト:米国の倉庫では、無駄な動きが原因で年間43億米ドルの損失が発生しており、ロボットソリューションの重要性が強調されています。

- 産業用ロボットの成長:産業用ロボットの稼働台数は、2018年の240万8,000台から2021年には378万8,000台に増加すると予測されています。

- Alibabaの人員削減:ロボット労働力を導入することで、Alibabaは倉庫の労働力を70%削減し、同時に熟練労働者により多くの機会を創出しました。

倉庫ロボット市場の動向

移動ロボット(AGVとAMR)がタイプ別最大セグメント

移動ロボット、特に無人搬送車(AGV)と自律型移動ロボット(AMR)が倉庫ロボット市場を独占しています。このセグメントは2021年の世界売上高の22.80%を占め、自動化の極めて重要な原動力となっています。

- 力強い成長:モバイルロボットは最も急成長しているセグメントであり、CAGRは16.64%と予測され、適応性の高いロボットソリューションが市場で好まれていることを示しています。

- 収益予測:このセグメントの2021年の売上高は22億5,000万米ドル、2027年には56億3,000万米ドルに成長すると予測されており、倉庫での採用が増加していることを裏付けています。

- 技術の進歩:センサ技術、AI、コンピュータービジョンへの投資により、モバイルロボットの能力が向上しています。先進的自律型ロボットのためのAmazonのキャンバス技術買収はその顕著な例です。

- 産業への応用:モバイルロボットは、特に小売業(2021年の市場シェア27.46%)や飲食品セグメントで、商品のハンドリングや温度管理環境の効率性を高めるなど、産業を問わず広く利用されています。

アジア太平洋が大きな市場シェアを占める見込み

アジア太平洋は倉庫ロボット市場において支配的かつ急成長している地域であり、2021年には世界シェアの46.72%を占めます。

- CAGR予測:同地域は、中国やインドなどの国々におけるロボット技術の急速な導入に牽引され、CAGR 16.06%で首位を維持すると予想されます。

- 市場規模:アジア太平洋の倉庫ロボット市場は、2021年に46億2,000万米ドルの収益を上げ、2027年には112億米ドルに成長すると予測されています。

- eコマースの拡大:インドと中国におけるeコマース市場の活況は重要な促進要因であり、インドの市場は2020年の462億米ドルから2030年には3,500億米ドルに成長すると予測されています。

- 製造業のリーダーシップ:アジア太平洋の世界の製造拠点としての地位が、特に中国、日本、韓国での倉庫自動化技術の採用を後押ししています。

- 技術革新:アジアの企業はAIを活用したロボットソリューションに投資しています。中国のロボット企業であるGeek+は、AIを搭載した物流ロボットで大きな進歩を遂げ、既存の世界企業と競合しています。

倉庫ロボット産業概要

倉庫ロボット市場は世界の参入企業が支配的で、市場構造は統合されています。既存のオートメーション企業とロボット専業企業が産業の最前線に立ち、研究、提携、買収を活用して市場での地位を維持しています。

Honeywellのロボットハブ:Honeywellのロボット・イノベーションハブへの5,000万米ドルの投資は、倉庫オートメーションセグメントをリードする同社のコミットメントを示しています。

投資家の自信:GreyOrangeやVecna Roboticsなどの新興企業が多額の資金を調達したことは、倉庫ロボットの成長可能性に対する強い自信を示しています。

技術リーダーが市場力学を形成:ABB Limited、Fanuc Corporation、Honeywell International Inc.、KUKA AG、安川電機などの主要企業が市場をリードしています。これらの企業は、AMR、AS/RS、AI搭載システムなどの先進的なソリューションを開発しています。

革新的なソリューションSwisslogのKRスカラロボットやLocus RoboticsのRaaS(Robot-as-a-Service)サブスクリプションモデルは、従来の市場アプローチを破壊し、費用対効果が高く利用しやすい自動化ソリューションを提供しています。

戦略的パートナーシップ:Berkshire Greyが世界の小売業者と2,300万米ドルを投じて食料品の即日フルフィルメント契約を結んだように、eコマースプラットフォームやロジスティクスプロバイダーとのコラボレーションは、市場拡大のための重要な戦略です。

市場における今後の成功要因:成功するためには、企業はAIと機械学習の進歩に焦点を当て、ロボットの能力を強化する必要があります。さまざまな倉庫構成に適応する柔軟なソリューション、小売業者とのパートナーシップ、拡大可能な自動化プラットフォームが重要になります。また、高い導入コストや規制上の課題に対処することも、全産業で広く採用されるためには不可欠です。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

- COVID-19の産業への影響評価

第5章 市場力学

- 市場促進要因

- SKU数の増加

- 技術とロボットへの投資の増加

- 市場課題

- 厳しい規制要件

- 高コスト

第6章 市場セグメンテーション

- タイプ別

- 産業用ロボット

- 仕分けシステム

- コンベア

- パレタイザー

- 自動保管・検索システム(ASRS)

- 移動ロボット(AGVとAMR)

- 機能別

- 保管

- 梱包

- 積み替え

- その他

- エンドユーザー産業別

- 飲食品

- 自動車

- 小売

- 電気・電子

- 製薬

- その他

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- アジア

- 中国

- 韓国

- 日本

- オーストラリアとニュージーランド

- ラテンアメリカ

- 中東・アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- ABB Limited

- Kiva Systems(Amazon Robotics LLC)

- TGW Logistics Group GMBH

- Singapore Technologies Engineering Ltd(Aethon Incorporation)

- InVia Robotics Inc.

- Fanuc Corporation

- Honeywell International Incorporation

- Toshiba Corporation

- Omron Adept Technologies

- Yaskawa Electric Corporation(Yaskawa Motoman)

- Kuka AG

- Fetch Robotics Inc.

- Geek+Inc.

- Grey Orange Pte Ltd

- Hangzhou Hikrobot Technology Co. Ltd

- Syrius Robotics

- Locus Robotics

第8章 投資分析

第9章 市場の将来

The Warehouse Robotics Market size is estimated at USD 9.33 billion in 2025, and is expected to reach USD 21.08 billion by 2030, at a CAGR of 17.7% during the forecast period (2025-2030).

Key Highlights

- Expanding SKU Diversity Drives Warehouse Automation: The warehouse robotics market is witnessing accelerated growth driven by the surge in SKU diversity. Over 50% of businesses are expected to increase the number of SKUs to cater to long-tail consumer demands. This trend is reshaping traditional warehouse models, where large-pallet order systems are being replaced by small, multi-SKU orders. To meet this challenge, automated mini-load storage and retrieval systems (AS/RS) are becoming vital. These systems leverage lightweight cranes to manage totes, cases, and crates, optimizing storage and freeing up crucial labor and delivery resources.

- Increase in Warehouse Size: Warehouses have expanded from 65,000 sq. ft in 2000 to over 200,000 sq. ft in 2020 to accommodate the rising volume of SKUs.

- Shift in Retailer-Wholesaler Dynamics: Just-in-time ordering and direct-to-consumer distribution are reducing large-pallet orders, accelerating the need for automation.

- Picking Robots and AGVs: The latest generation of picking robots and Automated Guided Vehicles (AGVs) is ideal for handling small orders spread over vast SKU ranges in large warehouses.

- Surging Investments Fuel Technological Advancements: The influx of capital is propelling warehouse automation technologies forward. Venture capital firms have been actively investing in robotics, with funding for warehouse robotics startups reaching USD 381 million in Q1 2020, a 57% year-over-year increase.

- Locus Robotics' Expansion: In June 2020, Locus Robotics raised USD 40 million to enhance R&D and expand into the European Union.

- Amazon's Innovation Hub: Amazon's investment of USD 40 million to develop a cutting-edge robotics hub in Massachusetts is expected to boost automation advancements.

- Shopify's Strategic Acquisition: Shopify's USD 450 million acquisition of 6 River Systems in 2019 expanded its fulfillment capabilities, incorporating cloud-based software and collaborative mobile robots.

- E-commerce Boom Accelerates Adoption: The rapid growth of e-commerce continues to drive the adoption of warehouse robotics. Efficient inventory management and fulfillment operations are becoming critical as online retail surges.

- Projected Market Value: Cowen projects that the U.S. market for warehouse and logistics robots in e-commerce will reach nearly USD 8 billion by 2024.

- New Fulfillment Models: Albertsons and Takeoff Technologies have collaborated to pilot urban fulfillment centers powered by AI and robotics to streamline small urban warehouse operations.

- Kroger's Expansion: Kroger is planning to open up to 20 customer fulfillment centers in partnership with Ocado, featuring large-scale robot-driven facilities.

- Labor Shortages and Cost Reduction Drive Innovation: Warehouse robotics are being increasingly used to tackle labor shortages and reduce operational costs. Automation helps improve efficiency by reducing unnecessary labor movement and streamlining operations.

- Wasted Motion Costs: U.S. warehouses lose USD 4.3 billion annually due to wasted motion, emphasizing the importance of robotic solutions.

- Industrial Robots Growth: The operational stock of industrial robots is projected to grow from 2,408 thousand units in 2018 to 3,788 thousand units by 2021.

- Alibaba's Workforce Reduction: By deploying robotic labor, Alibaba reduced its warehouse workforce by 70%, while creating more opportunities for skilled labor.

Warehouse Robotics Market Trends

Mobile Robots (AGVs and AMRs) Largest Segment by Type

Mobile robots, particularly Automated Guided Vehicles (AGVs) and Autonomous Mobile Robots (AMRs), dominate the warehouse robotics market. This segment captured 22.80% of global revenue in 2021, making it a pivotal driver of automation.

- Strong Growth: Mobile robots are the fastest-growing segment, with a CAGR of 16.64% forecasted, indicating a clear market preference for adaptable robotic solutions.

- Revenue Projections: The segment generated USD 2.25 billion in revenue in 2021 and is expected to grow to USD 5.63 billion by 2027, underlining the increased adoption in warehouses.

- Technological Advancements: Investments in sensor technology, AI, and computer vision are enhancing the capabilities of mobile robots. Amazon's acquisition of Canvas Technology for advanced autonomous robots is a notable example.

- Industry Applications: Mobile robots are widely used across industries, particularly in retail (27.46% market share in 2021) and food and beverage sectors, where they enhance efficiency in product handling and temperature-controlled environments.

Asia Pacific is Expected to Hold Significant Market Share

Asia-Pacific is the dominant and fastest-growing region in the warehouse robotics market, capturing 46.72% of the global share in 2021.

- CAGR Projections: The region is expected to maintain its leadership with a CAGR of 16.06%, driven by the rapid adoption of robotics technologies in countries like China and India.

- Market Size: The Asia-Pacific warehouse robotics market generated USD 4.62 billion in revenue in 2021, with forecasts estimating growth to USD 11.20 billion by 2027.

- E-commerce Expansion: The booming e-commerce market in India and China is a significant driver, with India's market expected to grow from USD 46.2 billion in 2020 to USD 350 billion by 2030.

- Manufacturing Leadership: Asia-Pacific's status as a global manufacturing hub is propelling the adoption of warehouse automation technologies, especially in China, Japan, and South Korea.

- Technological Innovation: Companies in Asia are investing in AI-powered robotics solutions. Geek+, a Chinese robotics company, has made significant advancements with its AI-powered logistics robots, competing with established global players.

Warehouse Robotics Industry Overview

The warehouse robotics market is dominated by global players, with a consolidated market structure. Established automation companies and specialized robotics firms are at the forefront of the industry, leveraging research, partnerships, and acquisitions to maintain their market positions.

Honeywell's Robotics Hub: Honeywell's USD 50 million investment in a Robotics Innovation Hub showcases the company's commitment to leading the warehouse automation sector.

Investor Confidence: Emerging players such as GreyOrange and Vecna Robotics have raised substantial funds, indicating strong confidence in the growth potential of warehouse robotics.

Technology Leaders Shape Market Dynamics: Key players like ABB Limited, Fanuc Corporation, Honeywell International Inc., KUKA AG, and Yaskawa Electric Corporation lead the market. These companies are developing advanced solutions, including AMRs, AS/RS, and AI-powered systems.

Innovative Solutions: Swisslog's KR SCARA robots and Locus Robotics' RaaS (robots-as-a-service) subscription model are disrupting traditional market approaches, providing cost-effective and accessible automation solutions.

Strategic Partnerships: Collaboration with e-commerce platforms and logistics providers, such as Berkshire Grey's USD 23 million contract with a global retailer for same-day grocery fulfillment, is a key strategy for market expansion.

Factors Driving Future Success in the Market: To succeed, companies need to focus on AI and machine learning advancements to enhance robotic capabilities. Flexible solutions that adapt to various warehouse configurations, partnerships with retailers, and scalable automation platforms will be critical. Addressing high implementation costs and regulatory challenges will also be essential to ensure wider adoption across industries.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Number of SKUs

- 5.1.2 Increasing Investments in Technology and Robotics

- 5.2 Market Challenges

- 5.2.1 Stringent Regulatory Requirements

- 5.2.2 High Cost

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Industrial Robots

- 6.1.2 Sortation Systems

- 6.1.3 Conveyors

- 6.1.4 Palletizers

- 6.1.5 Automated Storage and Retrieval System (ASRS)

- 6.1.6 Mobile Robots (AGVs and AMRs)

- 6.2 By Function

- 6.2.1 Storage

- 6.2.2 Packaging

- 6.2.3 Trans-shipment

- 6.2.4 Other Functions

- 6.3 By End-user Industry

- 6.3.1 Food and Beverage

- 6.3.2 Automotive

- 6.3.3 Retail

- 6.3.4 Electrical and Electronics

- 6.3.5 Pharmaceutical

- 6.3.6 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.3 Asia

- 6.4.3.1 China

- 6.4.3.2 South Korea

- 6.4.3.3 Japan

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.6 Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ABB Limited

- 7.1.2 Kiva Systems (Amazon Robotics LLC)

- 7.1.3 TGW Logistics Group GMBH

- 7.1.4 Singapore Technologies Engineering Ltd (Aethon Incorporation)

- 7.1.5 InVia Robotics Inc.

- 7.1.6 Fanuc Corporation

- 7.1.7 Honeywell International Incorporation

- 7.1.8 Toshiba Corporation

- 7.1.9 Omron Adept Technologies

- 7.1.10 Yaskawa Electric Corporation (Yaskawa Motoman)

- 7.1.11 Kuka AG

- 7.1.12 Fetch Robotics Inc.

- 7.1.13 Geek+ Inc.

- 7.1.14 Grey Orange Pte Ltd

- 7.1.15 Hangzhou Hikrobot Technology Co. Ltd

- 7.1.16 Syrius Robotics

- 7.1.17 Locus Robotics