|

市場調査レポート

商品コード

1687080

軍事衛星- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Military Satellite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 軍事衛星- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 194 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

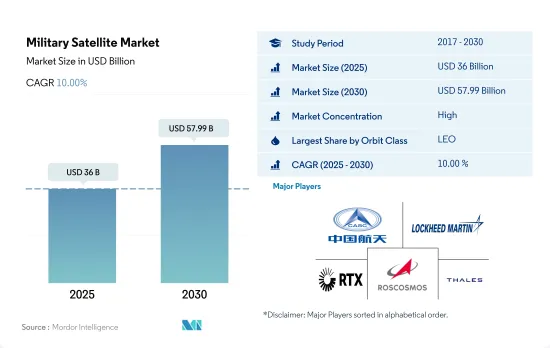

軍事衛星市場規模は2025年に360億米ドルと推定され、2030年には579億9,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは10.00%で成長します。

通信中継の高速化がLEOセグメントを牽引し、2023年には84.8%の主要シェアを占めます。

- 衛星や宇宙船は通常、地球を周回する多くの特別な軌道のひとつに配置されます。地球低軌道(LEO)、静止軌道(GEO)、地球中軌道(MEO)の3つの軌道のうち、地球に近いLEO軌道が最も広く好まれています。

- 気象衛星や通信衛星の多くは、地上から最も遠い地球高軌道をとる傾向があります。平均(中)地球軌道の衛星には、特定の地域をモニタリングするために設計された航法衛星や特殊衛星が含まれます。それぞれの距離には、カバー範囲の拡大やエネルギー効率の低下など、利点と課題があります。NASAの地球観測システムチームを含むほとんどの科学衛星は、地球低軌道にあります。

- 2017~2022年にかけて、MEO軌道で打ち上げられた57機の衛星のうち、ほとんどがナビゲーション/全地球測位目的で作られたものです。同様に、GEO軌道にある147機の衛星のうち、ほとんどが通信と地球観測の目的で配備されました。この期間に製造・打ち上げられた約4,131機のLEO衛星は、北米の組織が所有していました。

- エレクトロニクスインテリジェンス、地球科学/気象学、レーザー・イメージング、光学イメージングといったセグメントでの衛星利用の増加が、予測期間中の衛星開発需要を牽引すると見られています。

世界の防衛衛星数の急増が軍事衛星市場を後押しする見込み

- 世界の国防費は2022年に2兆米ドルを超え、軍事大国である米国は国防費を7,730億米ドル急増させました。米国宇宙軍の重要性が増しているのは、すべての軍事衛星通信衛星の運用を引き継いでいるためです。米国軍は宇宙システムを空、陸、海の各プラットフォームと統合しており、軍事力の衛星への依存度が高まっている

- 米国に続いて、中国、インド、ロシア、英国がそれぞれ14%、5%、6.8%、13%防衛費を増加させました。主要な防衛参入企業は、防衛衛星セグメントの予算を確立しています。例えば、2022年3月、フランス国防省は宇宙領域に7億600万米ドルの支出を計画し、2019~2025年の間に軍事宇宙能力とサービスに53億ユーロを計上しました。

- 市場では、産業の新たな機会を開拓するために巨額の研究開発費を費やす民間企業の参入が見られます。北米の企業は、軍事衛星市場における新しい衛星バスの開発を重視しています。例えば、2023年1月、Lockheed Martin初のマルチミッション宇宙船、LM 400は、軍事ユーザー向けに適応可能な柔軟な中型衛星で、同社のデジタルファクトリーの生産ラインから準備され、2023年に打ち上げが予定されています。2017~2022年にかけて、製造・打ち上げられた約230以上の衛星が北米の軍事・政府機関によって所有されました。高い軍事予算支出と技術開発が、2023~2029年の間に91%に達する健全な成長率で北米市場を牽引すると予想されます。

世界の軍事衛星市場動向

世界の衛星小型化需要の高まりが市場成長を牽引

- 小型衛星は、従来の衛星のほぼすべての機能をわずかなコストで実行できるため、小型衛星コンステレーションの構築、打ち上げ、運用の実行可能性が高まっています。北米の需要は、毎年最も多くの小型衛星を製造している米国が主に牽引しています。北米では、2017~2022年にかけて、合計596機の超小型衛星が様々な地域の参入企業によって軌道に投入されました。NASAも現在、これらの衛星の開発を目的としたいくつかのプロジェクトに関与しています。

- 欧州の市場需要は、主にドイツ、フランス、ロシア、英国が牽引しており、毎年最も多くの小型衛星を製造しています。2017~2022年の間に、50機以上の超小型衛星と超小型衛星が様々な地域の参入企業によって軌道に投入されました。電子部品とシステムの小型化と商業化が市場参入企業を牽引し、その結果、現在の市場シナリオを活用し、強化することを目指す新たな市場参入企業が出現しています。例えば、英国を拠点とする新興企業Open CosmosはESAと提携し、約90%の競合あるコスト削減を実現しながら、エンドユーザーに業務用超小型衛星打ち上げサービスを提供しています。

- アジア太平洋の需要は、主に中国、日本、インドが牽引しており、これらの国は毎年最も多くの小型衛星を製造しています。2017~2022年の間に、190機以上の超小型衛星が様々な地域の参入企業によって軌道に投入されました。中国は宇宙ベースの能力増強に向けて多大な資源を投入しています。同国はこれまでアジア太平洋で最も多くの超小型衛星を打ち上げてきました。

投資機会の急増が世界の衛星製造市場を押し上げると予想されます。

- 北米では、宇宙計画のための世界政府支出が2021年に過去最高の約1,030億米ドルに達しました。この地域は、世界最大の宇宙機関であるNASAの存在により、宇宙イノベーションと研究の震源地となっています。2022年、米国政府は宇宙プログラムに約620億米ドルを支出し、宇宙プログラムへの支出額が世界一となりました。米国では、連邦政府機関は毎年議会から資金援助を受けており、NASAは2023年に323億3,000万米ドルをその子会社のために受け取りました。

- 欧州諸国は、宇宙領域における様々な投資の重要性を認識しており、世界の宇宙産業で競合を維持するために、革新的な活動への支出を増やしています。2022年11月、ESAは、地球観測における欧州のリードを維持し、航法サービスを拡大し、米国との宇宙探査におけるパートナーであり続けることを目的として、今後3年間で宇宙資金を25%増額することを提案したと発表しました。欧州宇宙機関(ESA)は、2023~2025年にかけての約185億ユーロの予算を支持するよう22カ国に求めています。ドイツ、フランス、イタリアが主要拠出国です。

- アジア太平洋における宇宙関連活動の増加に伴い、2022年、日本の予算案は宇宙予算の増額を記録し、その額は14億米ドルを超えました。これには、H3ロケット、技術検査衛星9号、情報収集衛星(IGS)計画の開発が含まれます。同様に、22年度のインドの宇宙開発予算案は18億3,000万米ドルでした。2022年、韓国科学情報通信省は、人工衛星、ロケット、その他の主要な宇宙機器の製造のために6億1,900万米ドルの宇宙予算を発表しました。

軍事衛星産業概要

軍事衛星市場はかなり統合されており、上位5社で85.32%を占めています。この市場の主要企業は、China Aerospace Science and Technology Corporation(CASC)、Lockheed Martin Corporation、Raytheon Technologies Corporation、ROSCOSMOS、Thalesです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 衛星の小型化

- 衛星質量

- 宇宙開発への支出

- 規制の枠組み

- 世界

- オーストラリア

- ブラジル

- カナダ

- 中国

- フランス

- ドイツ

- インド

- イラン

- 日本

- ニュージーランド

- ロシア

- シンガポール

- 韓国

- アラブ首長国連邦

- 英国

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 衛星質量

- 10~100kg

- 100~500kg

- 500~1,000kg

- 10kg以下

- 1,000kg以上

- 軌道クラス

- GEO

- LEO

- MEO

- 衛星サブシステム

- 推進ハードウェアと推進剤

- 衛星バスとサブシステム

- 太陽電池アレイと電源ハードウェア

- 構造、ハーネス、機構

- 用途

- 通信

- 地球観測

- ナビゲーション

- 宇宙観測

- その他

- 地域

- アジア太平洋

- 欧州

- 北米

- その他

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Airbus SE

- BAE Systems

- China Aerospace Science and Technology Corporation(CASC)

- Elbit Systems

- General Dynamics

- Indian Space Research Organisation(ISRO)

- Information Satellite Systems Reshetnev

- Lockheed Martin Corporation

- Raytheon Technologies Corporation

- ROSCOSMOS

- Thales

- Viasat, Inc.

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Military Satellite Market size is estimated at 36 billion USD in 2025, and is expected to reach 57.99 billion USD by 2030, growing at a CAGR of 10.00% during the forecast period (2025-2030).

Faster relay of communication is driving the LEO segment to occupy a major share of 84.8% in 2023

- A satellite or a spacecraft is usually placed into one of many special orbits around the Earth, or it can be launched into an interplanetary journey based on its intended application. Out of the three orbits, namely low Earth orbit (LEO), geostationary orbit (GEO), and medium Earth orbit (MEO), the LEO orbit is the most widely preferred one because of its proximity to the Earth.

- Many weather and communication satellites tend to have high Earth orbits, which are farthest from the surface. Satellites in mean (medium) Earth orbit include navigational and specialized satellites designed to monitor a specific area. Each distance has benefits and challenges, including increased coverage and decreased energy efficiency. Most science satellites, including NASA's Earth Observation System team, are in low Earth orbit.

- During 2017-2022, out of the 57 satellites launched in the MEO orbit, most were built for navigation/global positioning purposes. Similarly, out of the 147 satellites in the GEO orbit, most were deployed for communication and Earth observation purposes. Around 4,131 LEO satellites manufactured and launched were owned by North American organizations in that period.

- The increasing use of satellites in areas such as electronics intelligence, Earth science/meteorology, laser imaging, and optical imaging is expected to drive the demand for the development of satellites during the forecast period.

The surge in the number of defense satellites globally is expected to aid the military satellites market

- The global defense expenditure crossed over USD 2 trillion in 2022, with the major military power, the United States, surging its defense expenditure by USD 773 billion. The increasing importance of the US Space Force is due to it taking over the operation of all military satellite communications satellites. The US armed forces are integrating space systems with air, land, and sea platforms as military forces increasingly rely on satellites for operations.

- The United States was followed by China, India, Russia, and the United Kingdom, which also increased their defense expenditures by 14%, 5%, 6.8%, and 13%, respectively. The major defense players have well-established budgets for their defense satellite domain. For instance, in March 2022, France's Armed Forces Ministry planned to spend USD 706 million in the space domain and earmarked EUR 5.3 billion on military space capabilities and services during 2019-2025.

- The market is witnessing the entry of private players spending huge amounts on R&D to exploit new opportunities in the industry. Companies in North America have emphasized developing new satellite buses in the military satellite market. For instance, in January 2023, Lockheed Martin's first multi-mission spacecraft, the LM 400, is a flexible mid-sized satellite adaptable for military users, readied from the company's Digital Factory production line and scheduled for launch in 2023. During 2017-2022, around 230+ satellites manufactured and launched were owned by military and government organizations in North America. High military budget spending and technology development are expected to drive the North American market at a healthy growth rate, amounting to 91%, during 2023-2029.

Global Military Satellite Market Trends

Rising demand for satellite miniaturization globally is driving market growth

- The ability of small satellites to perform nearly all the functions of traditional satellites at a fraction of their cost has increased the viability of building, launching, and operating small satellite constellations. The demand from North America is primarily driven by the United States, which manufactures the largest number of small satellites each year. In North America, during 2017-2022, a total of 596 nanosatellites were placed into orbit by various regional players. NASA is also currently involved in several projects aimed at developing these satellites.

- The market demand in Europe is primarily driven by Germany, France, Russia, and the United Kingdom, which manufacture the largest number of small satellites each year. During 2017-2022, more than 50 nano and microsatellites were placed into orbit by various regional players. The miniaturization and commercialization of electronic components and systems have driven market participation, resulting in the emergence of new market players who aim to capitalize on and enhance the current market scenario. For instance, UK-based startup Open Cosmos partnered with ESA to provide commercial nanosatellite launch services to end users while ensuring competitive cost savings of around 90%.

- The demand from Asia-Pacific is primarily driven by China, Japan, and India, which manufacture the largest number of small satellites annually. During 2017-2022, more than 190 nano and microsatellites were placed into orbit by various regional players. China is investing significant resources toward augmenting its space-based capabilities. The country has launched the most significant number of nano and microsatellites in Asia-Pacific to date.

The surge in investment opportunities is expected to boost the global satellite manufacturing market

- In North America, global government expenditure for space programs reached a record of approximately USD 103 billion in 2021. The region is the epicenter of space innovation and research, with the presence of the world's biggest space agency, NASA. In 2022, the US government spent nearly USD 62 billion on its space programs, making it the highest spender on space programs in the world. In the United States, federal agencies receive aid from Congress every year, known as funding, NASA received USD 32.33 billion in 2023 for its subsidiaries.

- European countries are recognizing the importance of various investments in the space domain and are increasing their spending on innovative activities to remain competitive in the global space industry. In November 2022, ESA announced that it had proposed a 25% boost in space funding over the next three years designed to maintain Europe's lead in Earth observation, expand navigation services, and remain a partner in space exploration with the United States. The European Space Agency (ESA) is asking its 22 nations to back a budget of some EUR 18.5 billion for 2023-2025. Germany, France, and Italy are the major contributors.

- In line with the increase in space-related activities in the Asia-Pacific region, in 2022, Japan's draft budget registered a rise in its space budget, which amounted to over USD 1.4 billion. It included the development of the H3 rocket, Engineering Test Satellite-9, and the nation's Information Gathering Satellite (IGS) program. Similarly, the proposed budget for India's space programs for FY22 was USD 1.83 billion. In 2022, the South Korean Ministry of Science and ICT announced a space budget of USD 619 million for manufacturing satellites, rockets, and other key space equipment.

Military Satellite Industry Overview

The Military Satellite Market is fairly consolidated, with the top five companies occupying 85.32%. The major players in this market are China Aerospace Science and Technology Corporation (CASC), Lockheed Martin Corporation, Raytheon Technologies Corporation, ROSCOSMOS and Thales (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Satellite Miniaturization

- 4.2 Satellite Mass

- 4.3 Spending On Space Programs

- 4.4 Regulatory Framework

- 4.4.1 Global

- 4.4.2 Australia

- 4.4.3 Brazil

- 4.4.4 Canada

- 4.4.5 China

- 4.4.6 France

- 4.4.7 Germany

- 4.4.8 India

- 4.4.9 Iran

- 4.4.10 Japan

- 4.4.11 New Zealand

- 4.4.12 Russia

- 4.4.13 Singapore

- 4.4.14 South Korea

- 4.4.15 United Arab Emirates

- 4.4.16 United Kingdom

- 4.4.17 United States

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Satellite Mass

- 5.1.1 10-100kg

- 5.1.2 100-500kg

- 5.1.3 500-1000kg

- 5.1.4 Below 10 Kg

- 5.1.5 above 1000kg

- 5.2 Orbit Class

- 5.2.1 GEO

- 5.2.2 LEO

- 5.2.3 MEO

- 5.3 Satellite Subsystem

- 5.3.1 Propulsion Hardware and Propellant

- 5.3.2 Satellite Bus & Subsystems

- 5.3.3 Solar Array & Power Hardware

- 5.3.4 Structures, Harness & Mechanisms

- 5.4 Application

- 5.4.1 Communication

- 5.4.2 Earth Observation

- 5.4.3 Navigation

- 5.4.4 Space Observation

- 5.4.5 Others

- 5.5 Region

- 5.5.1 Asia-Pacific

- 5.5.2 Europe

- 5.5.3 North America

- 5.5.4 Rest of World

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Airbus SE

- 6.4.2 BAE Systems

- 6.4.3 China Aerospace Science and Technology Corporation (CASC)

- 6.4.4 Elbit Systems

- 6.4.5 General Dynamics

- 6.4.6 Indian Space Research Organisation (ISRO)

- 6.4.7 Information Satellite Systems Reshetnev

- 6.4.8 Lockheed Martin Corporation

- 6.4.9 Raytheon Technologies Corporation

- 6.4.10 ROSCOSMOS

- 6.4.11 Thales

- 6.4.12 Viasat, Inc.

7 KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms