|

市場調査レポート

商品コード

1693948

北米の軍事衛星:市場シェア分析、産業動向、成長予測(2025年~2030年)North America Military Satellite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の軍事衛星:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 139 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

北米の軍事衛星市場規模は2025年に89億6,000万米ドルと推定され、2030年には132億6,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは8.14%で成長します。

北米衛星市場の需要を牽引するLEO衛星

- 打ち上げ時、衛星や宇宙船は通常、地球を周回する多くの特別な軌道の1つに配置されます。衛星は、その設計や主要目的によって、さまざまな距離で地球を周回します。それぞれの距離には、カバー範囲の拡大やエネルギー効率の低下など、利点と課題があります。地球の平均(中距離)軌道にある衛星には、特定の地域をモニタリングするために設計された航法衛星や特殊衛星が含まれます。NASAの地球観測システムチームを含むほとんどの科学衛星は、地球低軌道にあります。

- この領域で製造・打ち上げられる衛星は用途が異なります。例えば、2017~2022年の間に、180以上の衛星が製造・打ち上げられ、北米諸国の軍や政府によって運用されました。

- 電子情報、地球科学/気象学、レーザイメージング、光学イメージング、気象学などのセグメントでの衛星利用の増加は、予測期間中、北米軍事衛星市場における宇宙センサ需要を促進すると見られています。これらの要因から、予測期間中(2023~2029年)に市場は70%成長すると予測されています。LEO衛星セグメントは75%以上のシェアで市場を独占すると予想されます。

北米軍事衛星市場動向

超小型・超小型衛星の需要拡大が見込まれる

- 小型衛星が従来の衛星の数分の一のコストで従来の衛星のほぼすべての機能を実行できることから、小型衛星コンステレーションの構築、打ち上げ、運用の実行可能性が高まっています。2017~2022年の間に、この地域の様々な参入企業が合計459機の超小型衛星を軌道に乗せた。

- 北米の需要は、主に米国が牽引しており、米国は毎年最も多くの小型衛星を製造しています。同国からの打ち上げは過去3年間で減少しているが、同国の産業には大きな可能性が秘められています。新興企業や超小型衛星開発プロジェクトへの継続的な投資が、この地域の収益成長を押し上げると期待されています。

- 現在、NASAはこれらの衛星の開発を目的としたいくつかのプロジェクトに関与しています。NASAは現在、先進的な探査の実施や、科学研究や教育調査の実施に向けた新たな技術の実証にキューブサットを使用しています。

- 2020年3月、カナダ軍は、陸上指揮支援システム延命プログラム(LCSS LE)プログラムの一環として、移動部隊に衛星通信サービスを供給する契約をエルビットシステムズに発注しました。この契約には、移動部隊のリアルタイムブロードバンド通信を支援するトリプルバンドELSAT 2100 SATCOMオンザムーブ(SOTM)システムが含まれます。2100-ELSAT SOTMシステムにより、カナダ軍は移動指揮車、連絡部隊、優先度の高いセンサ車両、戦術司令部や司令部間の長距離音声データ接続を維持できるようになります。

国防費の増加が北米の軍事衛星需要を牽引

- 北米では、宇宙計画のための政府支出が2022年に約248億米ドルの記録を打ち立てた。この地域は、世界最大の宇宙機関であるNASAが存在する、宇宙技術革新と研究の震源地です。米国政府の宇宙プログラムへの支出により、同国は世界中で人工衛星の開発に最も多額の資金を投じています。研究助成金や投資助成金に関しては、この地域の政府や民間企業は、宇宙産業における研究や技術革新のために専用の資金を用意しています。各機関は、義務と呼ばれる金銭的約束をすることで、利用可能な予算資源を費やしています。例えば、2023年2月まで、米航空宇宙局(NASA)は研究助成金として3億3,300万米ドルを分配しました。

- 2020年10月、宇宙開発庁(SDA)は、極超音速ミサイルの発射を追跡し、早期に警告することができる新しい軍事衛星を設計、製造、打ち上げるために、スペースXに1億4,900万米ドルの契約を発注しました。また、同時期にL3ハリスにも1億9,300万米ドルの同様の契約が結ばれています。両社によって製造される予定の8基の衛星は、赤外線センサを使って宇宙から国防総省にミサイル追跡を提供するために設計されたSDAのTracking Layer Tranche 0の最初の重要な部分となります。カナダ政府によると、米国とは別に、カナダの宇宙産業はカナダのGDPに23億米ドルを上乗せし、1万人を雇用しています。カナダ政府の報告によると、カナダの宇宙関連企業の90%は中小企業です。カナダ宇宙庁(CSA)の予算は控えめで、2022~23年の予算支出見込みは3億2,900万米ドルです。

北米軍事衛星産業概要

北米の軍事衛星市場はかなり統合されており、上位5社で91.08%を占めています。この市場の主要企業は、Ball Corporation、Lockheed Martin Corporation、Northrop Grumman Corporation、Raytheon Technologies Corporation、The Boeing Companyです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 衛星の小型化

- 衛星質量

- 宇宙開発への支出

- 規制の枠組み

- カナダ

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 衛星質量

- 10~100kg

- 100~500kg

- 500~1,000kg

- 10kg以下

- 1,000kg以上

- 軌道クラス

- GEO

- LEO

- MEO

- 衛星サブシステム

- 推進ハードウェアと推進剤

- 衛星バスとサブシステム

- 太陽電池アレイと電源ハードウェア

- 構造、ハーネス、機構

- 用途

- 通信

- 地球観測

- ナビゲーション

- 宇宙観測

- その他

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Ball Corporation

- Cesium Astro

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Raytheon Technologies Corporation

- The Boeing Company

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

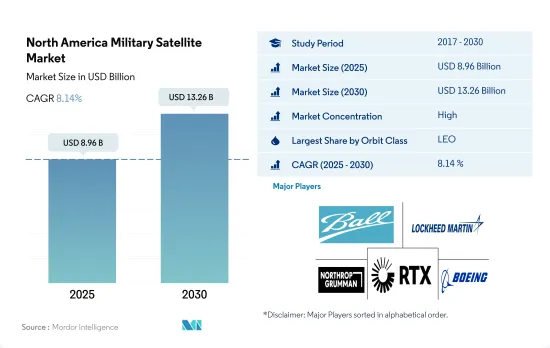

The North America Military Satellite Market size is estimated at 8.96 billion USD in 2025, and is expected to reach 13.26 billion USD by 2030, growing at a CAGR of 8.14% during the forecast period (2025-2030).

LEO satellites are driving demand in the North America satellite market

- At launch, a satellite or spacecraft is usually placed into one of many special orbits around the Earth, or it can be launched into an interplanetary journey. Satellites orbit the Earth at varying distances depending on their design and primary purpose. Each distance has its own benefits and challenges, including increased coverage and decreased energy efficiency. Satellites in mean (medium) Earth orbit include navigational and specialized satellites designed to monitor a specific area. Most science satellites, including NASA's Earth Observation System team, are in low Earth orbit.

- The different satellites manufactured and launched in this region have different applications. For instance, during 2017-2022, 180+ satellites were manufactured and launched, operated by North American countries' military and governments.

- The growing use of satellites in areas such as electronic intelligence, Earth science/meteorology, laser imaging, optical imaging, and meteorology is expected to drive space sensor demand in the North American military satellite market during the forecast period. Owing to these factors, the market is expected to grow by 70% during the forecast period (2023-2029). The LEO satellite segment is expected to dominate the market with more than a 75% share.

North America Military Satellite Market Trends

Growing demand for nano and microsatellites is expected

- The ability of small satellites to perform nearly all of the functions of a traditional satellite at a fraction of the cost of a traditional satellite has increased the viability of building, launching, and operating small satellite constellations. During 2017-2022, various players in the region placed a total of 459 nanosatellites into orbit.

- The demand from North America is primarily driven by the United States, which manufactures the largest number of small satellites annually. Although the launches from the country have decreased over the last three years, the country's industry holds enormous potential. Ongoing investments in start-ups and nano and microsatellite development projects are expected to boost the revenue growth of the region.

- Currently, NASA is involved in several projects aimed at developing these satellites. NASA is currently using CubeSats for conducting advanced exploration and demonstrating newly emerging technologies for conducting scientific research and educational investigations.

- In March 2020, the Canadian Armed Forces awarded a contract to Elbit Systems to supply satellite communication services to mobile units as part of the Land Command Support System Life Extension program (LCSS LE) program. The deal involves triple-band ELSAT 2100 SATCOM on-the-move (SOTM) systems that aid in real-time broadband communications for mobile military units. The 2100-ELSAT SOTM systems will enable the Canadian Armed Forces to maintain long-range voice and data connectivity between mobile command vehicles, liaison elements, high-priority sensor vehicles, and tactical headquarters or command posts.

Increasing defense spending drives the demand for military satellites in North America

- In North America, government expenditure for space programs hit a record of approximately USD 24.8 billion in 2022. The region is the epicenter of space innovation and research, with the presence of the world's biggest space agency, NASA. The US government's spending on its space programs makes the country as a highest spender on the development of satellites across the world. Regarding research and investment grants, the region's governments and the private sector have dedicated funds for research and innovation in the space industry. Agencies spend available budgetary resources by making financial promises called obligations. For instance, till February 2023, the National Aeronautics and Space Administration (NASA) had distributed USD 333 million as research grants.

- In October 2020, the Space Development Agency (SDA) awarded a USD 149 million contract to SpaceX to design, manufacture, and launch a new military satellite capable of tracking and providing early warnings of hypersonic missile launches. A similar contract worth USD 193 million was also awarded to L3Harris during the same timeframe. Eight satellites are scheduled to be manufactured by both companies and are meant to be the first crucial part of the SDA's Tracking Layer Tranche 0, designed to provide missile tracking for the Department of Defense from space using infrared sensors. Apart from the United States, the Canadian space industry adds USD 2.3 billion to the Canadian GDP and employs 10,000 people, according to the Canadian government. The government reports that 90% of Canadian space firms are small- and medium-sized businesses. The Canadian Space Agency's (CSA) budget is modest, and the estimated budgetary spending for 2022-23 was USD 329 million.

North America Military Satellite Industry Overview

The North America Military Satellite Market is fairly consolidated, with the top five companies occupying 91.08%. The major players in this market are Ball Corporation, Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Technologies Corporation and The Boeing Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Satellite Miniaturization

- 4.2 Satellite Mass

- 4.3 Spending On Space Programs

- 4.4 Regulatory Framework

- 4.4.1 Canada

- 4.4.2 United States

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Satellite Mass

- 5.1.1 10-100kg

- 5.1.2 100-500kg

- 5.1.3 500-1000kg

- 5.1.4 Below 10 Kg

- 5.1.5 above 1000kg

- 5.2 Orbit Class

- 5.2.1 GEO

- 5.2.2 LEO

- 5.2.3 MEO

- 5.3 Satellite Subsystem

- 5.3.1 Propulsion Hardware and Propellant

- 5.3.2 Satellite Bus & Subsystems

- 5.3.3 Solar Array & Power Hardware

- 5.3.4 Structures, Harness & Mechanisms

- 5.4 Application

- 5.4.1 Communication

- 5.4.2 Earth Observation

- 5.4.3 Navigation

- 5.4.4 Space Observation

- 5.4.5 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Ball Corporation

- 6.4.2 Cesium Astro

- 6.4.3 Lockheed Martin Corporation

- 6.4.4 Northrop Grumman Corporation

- 6.4.5 Raytheon Technologies Corporation

- 6.4.6 The Boeing Company

7 KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms