|

市場調査レポート

商品コード

1686575

英国の作物保護化学品:市場シェア分析、産業動向、成長予測(2025~2030年)UK Crop Protection Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国の作物保護化学品:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 209 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

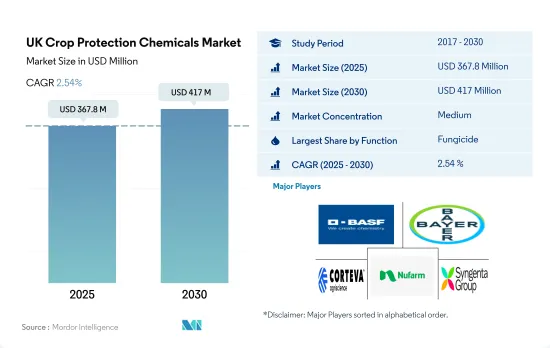

英国の作物保護化学品市場規模は、2025年には3億6,780万米ドルと推定され、2030年には4億1,700万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは2.54%で成長します。

同国では害虫や病害の蔓延が増加しており、深刻な収量減につながり、さまざまな作物保護化学薬品の市場を牽引しています。

- 英国の殺菌剤市場は2022年に1億8,290万米ドルと評価されました。同年の市場シェアは53.2%で、作物保護化学製品の中で最も消費されています。

- 英国で最も広く使用されている殺菌剤には、クロロタロニル、エポキシコナゾール、プロチオコナゾール、テブコナゾールなどがあります。Septoria triticiは英国における小麦で最も被害の大きい葉面病害であり、気圧の高い季節には30~50%の収量損失を引き起こします。多くの小麦生産者は、収量損失を軽減するために殺菌剤の使用を増やしています。

- 雑草は、綿花や冬小麦のような英国の作物に影響を与えます。主な繊維作物である綿花では、30%の収量減を引き起こしています。在来種の雑草であるブラックグラス(Alopecurus myosuroides)は、英国の農場に蔓延しています。この深刻な蔓延により、農家は主要穀物である冬小麦を放棄せざるを得なくなります。雑草は資源を奪い合い、作物の成長を妨げ、収量を減少させるため、経済的損失を引き起こし、除草剤の採用につながりました。除草剤は2022年の英国の作物保護化学品市場の38.2%を占めました。

- 気候の変化と気温の上昇により、害虫の個体数と食性が増加しています。ある調査によると、作物への暑熱ストレスが強まるにつれて、英国では気温が2℃上昇すると穀物の収量が約10%減少すると予測されています。その結果、同国の農家は害虫の圧力に対処するために殺虫剤に頼らざるを得なくなっています。

- 同国では害虫と病害の蔓延が増加しており、深刻な収量減少につながっているため、農家のニーズに基づいたさまざまな農作物保護剤の市場を牽引しています。同市場は予測期間(2023~2029年)にCAGR 2.4%を記録すると予測されます。

英国の作物保護化学品市場動向

英国では、農家による非化学的代替品の採用を含む様々な要因により、農薬の消費が減少しています。

- 英国では農薬の消費量が減少しています。2017~2022年にかけて、畜産への耕作面積の変更、特定の活性物質の撤退、天候が害虫や病気のレベルに与える影響、農家による非化学的代替物質の採用などにより、1ヘクタール当たりの消費量は24万3,800トン減少しました。

- 英国に対する農薬使用削減圧力の高まりは、今後数年間の農薬消費に影響を与える可能性があります。政府は農薬の使用を減らすためにいくつかのイニシアチブを取っています。例えば、2018年1月、英国政府は「A Green Future:Our 25-Year Plan」を発表し、環境を改善し、総合的病害虫管理(IPM)と持続可能な作物保護の導入を拡大しようとしています。

- 2020年、英国農業におけるグリホサートの使用量は、発ガンとの関連性が指摘されているにもかかわらず、重量、処理面積、1ヘクタール当たりの散布率で、4年間で16%増加しました。政府は、収穫前乾燥(グリホサートを使用して作物を人工的に乾燥させる)の増加、または、耕作によって土壌から炭素を放出することなく雑草に対処するためにグリホサートやその他の除草剤に依存する傾向がある不耕起農業の増加により、従来の化学物質への依存を減らす計画です。同様に、殺菌剤イマザリルの使用は53%増加し、同時期にこの薬剤で処理された土地面積は63%増加して8万1,000ヘクタールを超えました。

- 植物の病気や害虫は農業生産に大きな影響を与えるため、気候の変化、病害虫、収穫ロスは、農作物を保護し、害虫の収穫ロスを減らすための農薬消費を促進する可能性があります。

規制の変更と農薬削減に重点を置く政府は、作物保護化学品の価格に影響を与える可能性があります。

- シペルメトリンとエマメクチン安息香酸塩は、大規模に使用される重要な殺虫剤成分です。2022年、これらの成分の価格はそれぞれ1トン当たり2万1,100米ドル、1トン当たり1万7,300米ドルでした。

- 2022年に1トン当たり8,700米ドルと評価されたメタラキシルは、保護・処理作用で知られる浸透性フェニルアミド系殺菌剤です。胞子嚢の形成、菌糸の成長、新たな感染の確立を抑制することで効果を発揮します。真菌の核酸合成(RNAポリメラーゼ1)を阻害します。この殺菌剤は、熱帯・亜熱帯作物への葉面散布、土壌伝染性病原菌の防除のための土壌処理剤、べと病管理のための種子処理剤として推奨されています。

- グリホサートは、雑草駆除のための除草剤として、また耕す代わりに農家に広く使用されていますが、土壌生態系を破壊し、炭素を放出することが観察されています。英国では、再生農法が耕作を減らすことを奨励しているため、農業におけるグリホサートの使用量は2020年までの4年間で16%増加しています。農薬散布面積は9%(23万ヘクタール)拡大しました。小麦農家は、収穫前の作物乾燥のためにグリホサートを顕著に使用しています。2022年、グリホサートの価格は前年比2.2%上昇しました。

- 選択的除草剤であるペンディメタリンは、ジニトロアニリン系除草剤に属します。様々な園芸作物、芝、林業において、一年草、多年草、広葉樹、木本類など幅広い雑草の防除に使用されます。2022年、ペンディメタリンの価格は1トン当たり3,300米ドルでした。

英国の作物保護化学産業の概要

英国の作物保護化学品市場は適度に統合されており、上位5社で63.61%を占めています。この市場の主要企業はBASF SE、Bayer AG、Corteva Agriscience、Nufarm Ltd and Syngenta Group(sorted alphabetically)などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- 英国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 機能別

- 殺菌剤

- 除草剤

- 殺虫剤

- 軟体動物駆除剤

- 線虫駆除剤

- 用途別

- 化学的処理

- 葉面散布

- 燻蒸

- 種子処理

- 土壌処理

- 作物タイプ別

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用植物

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADAMA Agricultural Solutions Ltd.

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Nufarm Ltd

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

- Wynca Group(Wynca Chemicals)

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 52786

The UK Crop Protection Chemicals Market size is estimated at 367.8 million USD in 2025, and is expected to reach 417 million USD by 2030, growing at a CAGR of 2.54% during the forecast period (2025-2030).

Increasing pests and disease infestations in the country are leading to severe yield losses and driving the market for different crop protection chemicals

- The UK fungicide market was valued at USD 182.9 million in 2022. It was the most consumed among crop protection chemicals, with a market share of 53.2% in the same year.

- The most extensively used fungicide formulations in the United Kingdom include chlorothalonil, epoxiconazole, prothioconazole, and tebuconazole. Septoria tritici is UK wheat's most damaging foliar disease, causing yield losses that range from 30% to 50% in high-pressure seasons. Many wheat growers have increased the use of fungicides in their crops to mitigate yield loss.

- Weeds impact UK crops like cotton and winter wheat. They cause a 30% yield loss in cotton, the main fiber crop. Black grass (Alopecurus myosuroides), a native weed, frequently infests UK farms. Severe infestations force farmers to abandon winter wheat, the main cereal crop. Weeds compete for resources, hinder crop growth, and reduce yields, causing economic losses and leading to the adoption of herbicides. Herbicides accounted for 38.2% of the UK crop protection chemicals market in 2022.

- The changing climate and rising temperatures are causing an increase in the population and feeding habits of insect pests. A study reveals that as heat stress on crops intensifies, cereal yields in the United Kingdom are projected to decline by approximately 10% with a 2 °C increase in temperature. Consequently, these circumstances are prompting farmers in the country to rely on insecticides to manage pest pressures.

- Increasing pests and disease infestations in the country have led to severe yield losses, thus driving the market for different crop protection chemicals based on farmers' needs. The market is estimated to register a CAGR of 2.4% during the forecast period (2023-2029).

UK Crop Protection Chemicals Market Trends

The United Kingdom is experiencing a decline in the consumption of pesticides due to various factors, including the adoption of non-chemical alternatives by farmers

- The United Kingdom is experiencing a decline in the consumption of pesticides. From 2017 to 2022, the consumption per hectare decreased by 243.8 thousand metric ton due to changes in the area of cultivation to livestock farming, withdrawal of certain active substances, the impact of the weather on pest and disease levels, and the adoption of non-chemical alternatives by farmers.

- The rising pressure on the United Kingdom to reduce the use of pesticides could impact the consumption of pesticides in the coming years. The government is taking several initiatives to reduce the use of pesticides. For instance, in January 2018, the UK government launched "A Green Future: Our 25-Year Plan" to improve the environment and increase the uptake of integrated pest management (IPM) and sustainable crop protection.

- In 2020, the use of glyphosate in UK farming grew by 16% over four years in terms of weight, the area treated, and application rate per hectare despite being linked to causing cancer and the government plans to reduce reliance on conventional chemicals due to rising pre-harvest desiccation (where crops are artificially dried using glyphosate) and/or an increase in no-till agriculture, which tends to rely upon glyphosate and other herbicides to deal with weeds without releasing carbon from the soil via plowing. Similarly, the use of the fungicide imazalil increased by 53%, while the land area treated with the chemical rose by 63% to more than 81,000 ha during the same period.

- Changing climate, pests and diseases, and harvest losses could drive the consumption of pesticides to protect crops and reduce pest yield losses, as plant diseases and pests can have a significant impact on agriculture production.

Regulatory changes and the government's focus on reducing pesticides may influence the prices of crop protection chemicals

- Cypermethrin and emmamectin benzoate are significant insecticide ingredients used on a large scale. In 2022, these ingredients were priced at USD 21.1 thousand per metric ton and USD 17.3 thousand per metric ton, respectively.

- Metalaxyl, valued at USD 8.7 thousand per metric ton in 2022, is a systemic phenylamide fungicide known for its protective and curative mode of action. It works by suppressing sporangial formation, mycelial growth, and the establishment of new infections. It disrupts fungal nucleic acid synthesis - RNA polymerase 1. This fungicide is recommended for foliar spray on tropical and sub-tropical crops, as a soil treatment for controlling soil-borne pathogens, and as a seed treatment to manage downy mildew.

- Glyphosate, widely used by farmers as a herbicide for weed control and as an alternative to plowing, has been observed to disrupt the soil ecosystem and release carbon. In the United Kingdom, its usage in farming witnessed a growth of 16% over four years till 2020, with regenerative farming practices encouraging reduced plowing. The area of land sprayed with pesticides expanded by 9% (230,000 ha). Wheat farms are notable users of glyphosate for crop desiccation before harvest. In 2022, the price of glyphosate experienced a 2.2% increase compared to the previous year.

- Pendimethalin, a selective herbicide, belongs to the dinitroaniline herbicide family. It is used to control a broad range of weeds, including annual and perennial grasses, broadleaf species, and woody species in various horticultural crops, turf, and forestry. In 2022, pendimethalin was priced at USD 3.3 thousand per metric ton.

UK Crop Protection Chemicals Industry Overview

The UK Crop Protection Chemicals Market is moderately consolidated, with the top five companies occupying 63.61%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, Nufarm Ltd and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 United Kingdom

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Function

- 5.1.1 Fungicide

- 5.1.2 Herbicide

- 5.1.3 Insecticide

- 5.1.4 Molluscicide

- 5.1.5 Nematicide

- 5.2 Application Mode

- 5.2.1 Chemigation

- 5.2.2 Foliar

- 5.2.3 Fumigation

- 5.2.4 Seed Treatment

- 5.2.5 Soil Treatment

- 5.3 Crop Type

- 5.3.1 Commercial Crops

- 5.3.2 Fruits & Vegetables

- 5.3.3 Grains & Cereals

- 5.3.4 Pulses & Oilseeds

- 5.3.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd.

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Nufarm Ltd

- 6.4.7 Sumitomo Chemical Co. Ltd

- 6.4.8 Syngenta Group

- 6.4.9 UPL Limited

- 6.4.10 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms