|

市場調査レポート

商品コード

1683923

欧州の国内宅配便市場:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Domestic Courier - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の国内宅配便市場:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 365 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

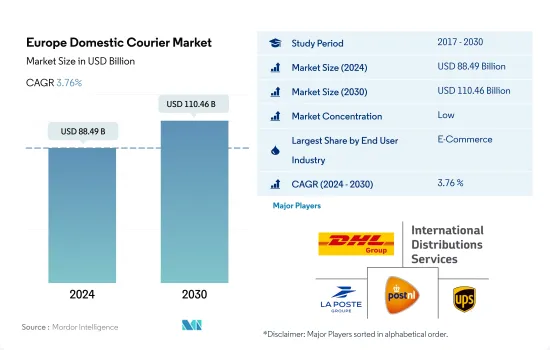

欧州の国内宅配便市場規模は2024年に884億9,000万米ドルと推定され、2030年には1,104億6,000万米ドルに達すると予測され、予測期間中(2024年~2030年)のCAGRは3.76%で成長する見込みです。

eコマース企業は顧客により良いサービスを提供するため、欧州でネットワークを拡大しています。

- 消費者が注文品の迅速かつ便利な到着を期待しているため、国内の宅配便サービスはeコマース業界においてますます重要になってきています。パンデミックは過去数年間に買い物行動に劇的な変化をもたらし、買い物のプロセスをオンライン・ショッピングへとシフトさせました。さらに、eコマース企業は顧客により良いサービスを提供するため、欧州でのネットワークを拡大しています。例えば、スペインの小売業者DIAは、ジローナからウエルバまで、スペインの海岸線に沿ったすべての町に配送サービスを拡大し、500万人以上の新規顧客を獲得しています。

- 2022年には、ポルトガル、トルコ、ポーランドが、それぞれ13.3%、10.2%、10.1%と、欧州で最も売上高が増加しました。2021年には、すべての欧州諸国において、小売支出は個人消費に占める割合が大きく、i.一般的に30%から50%でした。欧州では、ドイツ市場が売上高において最大かつ最も重要な小売市場でした。ドイツに次いで欧州で経済規模が大きいのはフランス、英国、イタリアで、これらは国内宅配便サービスの主要な需要創出国です。

- 医療用品の需要の増加、医療費の増加、より迅速で効率的な配送サービスの必要性など、いくつかの要因から、ヘルスケア製品の宅配便サービスは、この地域で今後数年間成長すると予想されます。また、2023年以降、欧州5カ国(ドイツ、英国、フランス、イタリア、スペイン)の小売総売上高はパンデミック以前の水準で成長し、市場の成長を牽引すると予想されます。その結果、欧州の国内宅配便市場は予測期間中にプラス成長が見込まれます。

イタリアの国内宅配需要がCEPの成長を促進、売上は22%増で116億米ドルを達成

- ドイツの宅配便業者は2022年のクリスマス期間に7億2,500万個の小包を輸送しました。B2Cの小包輸送が最大のセグメントで、3億9,500万個の小包が個人の受取人に配達されました。平均すると、ピーク時には1日あたり2,000万個、個人宅への800万個を含む1日あたり1,450万個の小包が配達されました。ドイツ市場における国内CEPの需要は、2023年から2027年にかけて9.36%の割合で予測されるeコマースの成長により増加すると予想されます。

- eコマース分野は、フランス国内宅配便市場の成長の主な原動力になると予想されます。2022年のフランス国内宅配便市場は約830億米ドルと評価され、2027年には1,520億米ドルに達すると予測されています。eコマースにおける需要の増加は、大幅な小包配達につながり、フランスの国営郵便サービスであるLa Posteグループだけでも、2022年には26億個の小包を配達しています。DHL Global Forwarding France SAS、General Logistics Systems France SA、United Parcel Services France SASなど、フランスのCEP市場における他の主要企業も大きく貢献しています。

- イタリアでは、国内配送需要がCEP配送の推進に大きな役割を果たしています。CEPからの収入も大幅に増加し、2020年の96億米ドルから2021年には116億米ドルに22%増加しました。1人当たりの小包配達数も増加し、2020年の21個から2021年には24個へと17%増加しました。この結果、世帯は平均55個の小包を受け取ることになります。

欧州の国内宅配便市場動向

欧州連合(EU)、景気回復を後押しする135の輸送プロジェクトに57億6,000万米ドルを割り当て

- 欧州では、貿易と旅行の増加により、輸送・保管部門のGDPは2021年に10.48%増加します。2022年には、約135の輸送インフラ・プロジェクトが、総額60億米ドルのEU補助金に選ばれました。輸送・倉庫部門は、さまざまな業界の業務をサポートする上で重要な役割を担っており、ドイツがフランスや英国を抜いて圧倒的な存在としてリードしています。世界的に見ても、ドイツは商品の輸出入ともに第3位です。ドイツ連邦政府は交通インフラへの投資を拡大する意向を表明し、2022年には連邦高速道路に120億ユーロ(128億米ドル)以上、水路に約17億ユーロ(18億1,000万米ドル)を割り当て、交通網の改善へのコミットメントを示しました。

- ドイツ政府は道路よりも鉄道に投資する意向です。2022年、ドイツ鉄道、連邦政府、地方政府は、鉄道インフラ・プロジェクトにおよそ136億ユーロ(145億1,000万米ドル)を投資します。ニーダーザクセン州、ハンブルク州、ブレーメン州、メクレンブルク=西ポメラニア州、シュレースヴィヒ=ホルシュタイン州はDBと提携し、2030年までに鉄道網の近代化に投資します。

- 2022年、欧州連合(EU)は約135の交通インフラプロジェクトへの助成金54億ユーロを承認しました。これらのプロジェクトは、EU加盟国の大洪水後の経済回復を支援し、交通網を強化し、持続可能な輸送を促進し、安全性を高め、雇用機会を創出することを目的としています。支援されるプロジェクトはすべて、EU加盟国を結ぶ欧州横断交通ネットワークの一部であり、2030年までにTEN-Tコアネットワークを完成させ、2050年までに総合ネットワークを完成させるというEUの目標に沿ったものです。

2023年2月以降、ロシアからの輸入禁止により、中東、アジア、北米からのディーゼル輸入が増加しています。

- ガソリン価格は2022年第1四半期にユーロ圏19カ国の大半で1リットル当たり2ユーロ(2.13米ドル)を超えました。価格上昇の主な理由は、ロシアとウクライナの紛争による供給問題で、ロシアはEUの石油需要の4分の1以上を供給していました。2021年、ユーロ圏のガソリン1リットルの平均価格は1.30ユーロ(1.38米ドル)だったが、2022年の年初には1リットル当たり約1.55ユーロ(1.65米ドル)となりました。

- ロシアは欧州最大のディーゼル供給国です。2023年、欧州ではディーゼル価格が下落しました。EUがロシアからの石油製品輸入禁止を実施した2023年2月以降、ロシアから欧州へのディーゼル輸出は平均24,000バレル/日で、2022年にロシアが欧州に送った630,000バレル/日から96%減少しました。2月から5月までの欧州向けディーゼル輸出は、中東から51%(16万b/d)、アジアから97%(14万7,000b/d)、北米から65%(4万7,000b/d)増加しました。

- デンマークはガソリン価格が最も高く、フィンランドはディーゼル価格が最も高いです。オーストリアはガソリンが最も安く、スペインはディーゼルが最も安いです。英国の燃料価格は2022年に過去最高を記録し、7月のガソリン平均価格は1リットル当たり245.55米ドル、ディーゼルは251.79米ドルに達しました。2023年に入ってから、英国のガソリンスタンドの平均価格はリッター150ペソ(1.88.02米ドル)を突破し、ディーゼルはリッター152.41ペソ(191.04米ドル)に上昇しました。2023年1月のスペインの燃料価格は、英国よりもガソリンでリッターあたり約20セント、ディーゼルで40セント低くなりました。

欧州国内宅配便産業の概要

欧州の国内宅配便市場は細分化されており、上位5社で36.18%を占めています。この市場の主要企業は以下の通り。 DHL Group, International Distributions Services(including GLS), La Poste Group, Post NL and United Parcel Service of America, Inc.(UPS).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 人口動態

- 経済活動別GDP分布

- 経済活動別GDP成長率

- インフレ率

- 経済パフォーマンスとプロファイル

- eコマース産業の動向

- 製造業の動向

- 運輸・倉庫業のGDP

- 輸出動向

- 輸入動向

- 燃料価格

- 物流実績

- インフラ

- 規制の枠組み

- 中東欧(CEE)

- フランス

- ドイツ

- イタリア

- オランダ

- 北欧

- ロシア

- スペイン

- スイス

- 英国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 配達速度

- 特急

- 非特急

- 出荷重量

- 重量貨物

- 軽量貨物

- 中量貨物

- エンドユーザー産業

- eコマース

- 金融サービス(BFSI)

- ヘルスケア

- 製造業

- 第一次産業

- 卸売・小売業(オフライン)

- その他

- モデル

- 企業間取引(B2B)

- 企業対消費者(B2C)

- 消費者間取引(C2C)

- 国名

- アルバニア

- ブルガリア

- クロアチア

- チェコ共和国

- デンマーク

- エストニア

- フィンランド

- フランス

- ドイツ

- ハンガリー

- アイスランド

- イタリア

- ラトビア

- リトアニア

- オランダ

- ノルウェー

- ポーランド

- ルーマニア

- ロシア

- スロバキア共和国

- スロベニア

- スペイン

- スウェーデン

- スイス

- 英国

- その他の欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- DHL Group

- FedEx

- GEODIS

- International Distributions Services(including GLS)

- La Poste Group

- Logista

- Otto GmbH & Co. KG

- Post NL

- Poste Italiane

- United Parcel Service of America, Inc.(UPS)

第7章 CEOへの主な戦略的質問CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 技術の進歩

- 情報源と参考文献

- 図表リスト

- 主要洞察

- データパック

- 用語集

The Europe Domestic Courier Market size is estimated at 88.49 billion USD in 2024, and is expected to reach 110.46 billion USD by 2030, growing at a CAGR of 3.76% during the forecast period (2024-2030).

E-commerce companies are expanding their networks in Europe to provide better services to customers

- Domestic courier services are becoming increasingly important in the e-commerce industry as consumers expect their orders to arrive quickly and conveniently. The pandemic brought a drastic change in shopping behavior over the past years, shifting the shopping process toward online shopping. Moreover, e-commerce companies are expanding their networks in Europe to provide better services to customers. For instance, the Spanish retailer DIA is expanding its delivery services to all towns along the Spanish coastline, from Girona to Huelva, reaching more than 5 million new customers.

- In 2022, Portugal, Turkey, and Poland had the highest rise in sales in terms of volume in Europe at 13.3%, 10.2%, and 10.1%, respectively. In 2021, retail spending constituted a large proportion of private consumption in all European countries, i.e., typically between 30% and 50%. The German market in Europe was the largest and most important retail market in terms of turnover. After Germany, the largest economies in Europe were France, the United Kingdom, and Italy, the major demand generators for domestic courier services.

- Courier services for healthcare products are expected to grow in the coming years in the region due to several factors, including the increasing demand for medical supplies, rising healthcare spending, and the need for faster and more efficient delivery services. Also, From 2023 onward, it is expected that the total retail sales in Europe-5 countries (Germany, the United Kingdom, France, Italy, and Spain) will grow at pre-pandemic levels and drive the growth of the market. As a result, the European domestic courier market is expected to grow positively during the forecast period.

Italy's domestic delivery demand fuels CEP growth, revenue hits USD 11.6 billion with 22% increase

- Germany's parcel service providers moved a volume of 725 million parcels during the Christmas period in 2022. B2C parcel shipments were the largest segment, with 395 million parcels delivered to private recipients. On average, deliveries included 20 million shipments per day during peak times and 14.5 million parcels daily, including 8 million to private residences. The demand for domestic CEP in the German market is expected to increase due to the projected growth of e-commerce at a rate of 9.36% from 2023 to 2027.

- The e-commerce segment is expected to be the primary driver of growth in the French domestic courier market. In 2022, the French domestic courier market was valued at approximately USD 83 billion, and it is projected to reach USD 152 billion by 2027. The increased demand in e-commerce has led to significant parcel deliveries, with France's national postal service, La Poste Group, alone delivering 2.6 billion parcels in 2022. Other significant players in the French CEP market, such as DHL Global Forwarding France SAS, General Logistics Systems France SA, and United Parcel Services France SAS, also make substantial contributions.

- Domestic delivery demand plays a major role in driving CEP deliveries in Italy. Revenue from CEP also experienced a significant increase, rising by 22% to USD 11.6 billion in 2021 from USD 9.6 billion in 2020. The number of parcels delivered per person also grew, rising from 21 in 2020 to 24 in 2021, representing a 17% increase. This resulted in households receiving 55 parcels on average.

Europe Domestic Courier Market Trends

European Union allocated USD 5.76 billion to 135 transportation projects to boost economic recovery

- In Europe, the GDP of the transport and storage sector rise by 10.48% in 2021 due to rise in trade and travel. In 2022, around 135 transport infrastructure projects were selected for EU grants totaling USD 6 billion.The transportation and warehouse sector plays a crucial role in supporting operations across various industries, with Germany leading as the dominant player, surpassing France and the United Kingdom. Globally, Germany ranks third in both imports and exports of goods. The German federal government expressed its intention to increase investments in transportation infrastructure, allocating over EUR 12 billion (USD 12.80 billion) for federal highways and around EUR 1.7 billion (USD 1.81 billion) for waterways in 2022, thereby demonstrating its commitment to improving transportation networks.

- The German government intends to invest more in rail than roads. In 2022, Deutsche Bahn, the federal government, and the local and regional governments invested roughly EUR 13.6 billion (USD 14.51 billion) in rail infrastructure projects. Lower Saxony, Hamburg, Bremen, Mecklenburg-Western Pomerania, and Schleswig-Holstein are partnering with DB to invest in modernizing their rail network by 2030.

- In 2022, the European Union approved EUR 5.4 billion through grants for approximately 135 transport infrastructural projects. These projects aim to aid post-pandemic economic recovery in the EU Member States, enhance transport links, promote sustainable transportation, boost safety, and create job opportunities. All supported projects are part of the Trans-European Transport Network, which connects EU Member States and aligns with the European Union's goal of completing the TEN-T core network by 2030 and the comprehensive network by 2050.

Since February 2023, diesel imports from the Middle East, Asia, and North America have increased due to the ban on imports from Russia

- Gasoline prices surpassed EUR 2 (USD 2.13) per liter in most of the 19 eurozone countries in Q1 2022. The main reason behind the increased prices was supply issues due to the conflict between Russia and Ukraine, as Russia supplied more than a quarter of the EU's petroleum needs. In 2021, the average price for a liter of gasoline in the eurozone was EUR 1.30 (USD 1.38); at the start of 2022, the price was about EUR 1.55 (USD 1.65) per liter.

- Russia has been Europe's largest supplier of diesel. In 2023, diesel prices declined in Europe. Since February 2023, when the European Union implemented the ban on petroleum product imports from Russia, diesel exports from Russia to Europe have averaged 24,000 barrels per day (b/d), down by 96% from the 630,000 b/d Russia sent to Europe in 2022. From February through May, diesel exports to Europe increased by 51% (160,000 b/d) from the Middle East, by 97% (147,000 b/d) from Asia, and by 65% (47,000 b/d) from North America.

- Denmark is the most expensive country for petrol, and Finland is the most expensive for diesel. Austria has the cheapest petrol, and Spain is the cheapest for diesel. Fuel prices in the United Kingdom reached record highs in 2022, with the average price of petrol hitting USD 245.55 per liter and diesel reaching USD 251.79 per liter in July. The average cost of petrol at UK forecourts has risen to break 150 p a liter (USD 1.88.02) since the start of 2023, and diesel has risen to 152.41p a liter (USD 191.04). Spanish fuel prices were lower than in the United Kingdom by about 20 cents per liter for petrol and 40 cents per liter for diesel in January 2023.

Europe Domestic Courier Industry Overview

The Europe Domestic Courier Market is fragmented, with the top five companies occupying 36.18%. The major players in this market are DHL Group, International Distributions Services (including GLS), La Poste Group, Post NL and United Parcel Service of America, Inc. (UPS) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Demographics

- 4.2 GDP Distribution By Economic Activity

- 4.3 GDP Growth By Economic Activity

- 4.4 Inflation

- 4.5 Economic Performance And Profile

- 4.5.1 Trends in E-Commerce Industry

- 4.5.2 Trends in Manufacturing Industry

- 4.6 Transport And Storage Sector GDP

- 4.7 Export Trends

- 4.8 Import Trends

- 4.9 Fuel Price

- 4.10 Logistics Performance

- 4.11 Infrastructure

- 4.12 Regulatory Framework

- 4.12.1 Central and Eastern Europe (CEE)

- 4.12.2 France

- 4.12.3 Germany

- 4.12.4 Italy

- 4.12.5 Netherlands

- 4.12.6 Nordics

- 4.12.7 Russia

- 4.12.8 Spain

- 4.12.9 Switzerland

- 4.12.10 United Kingdom

- 4.13 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes Market Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Speed Of Delivery

- 5.1.1 Express

- 5.1.2 Non-Express

- 5.2 Shipment Weight

- 5.2.1 Heavy Weight Shipments

- 5.2.2 Light Weight Shipments

- 5.2.3 Medium Weight Shipments

- 5.3 End User Industry

- 5.3.1 E-Commerce

- 5.3.2 Financial Services (BFSI)

- 5.3.3 Healthcare

- 5.3.4 Manufacturing

- 5.3.5 Primary Industry

- 5.3.6 Wholesale and Retail Trade (Offline)

- 5.3.7 Others

- 5.4 Model

- 5.4.1 Business-to-Business (B2B)

- 5.4.2 Business-to-Consumer (B2C)

- 5.4.3 Consumer-to-Consumer (C2C)

- 5.5 Country

- 5.5.1 Albania

- 5.5.2 Bulgaria

- 5.5.3 Croatia

- 5.5.4 Czech Republic

- 5.5.5 Denmark

- 5.5.6 Estonia

- 5.5.7 Finland

- 5.5.8 France

- 5.5.9 Germany

- 5.5.10 Hungary

- 5.5.11 Iceland

- 5.5.12 Italy

- 5.5.13 Latvia

- 5.5.14 Lithuania

- 5.5.15 Netherlands

- 5.5.16 Norway

- 5.5.17 Poland

- 5.5.18 Romania

- 5.5.19 Russia

- 5.5.20 Slovak Republic

- 5.5.21 Slovenia

- 5.5.22 Spain

- 5.5.23 Sweden

- 5.5.24 Switzerland

- 5.5.25 United Kingdom

- 5.5.26 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 DHL Group

- 6.4.2 FedEx

- 6.4.3 GEODIS

- 6.4.4 International Distributions Services (including GLS)

- 6.4.5 La Poste Group

- 6.4.6 Logista

- 6.4.7 Otto GmbH & Co. KG

- 6.4.8 Post NL

- 6.4.9 Poste Italiane

- 6.4.10 United Parcel Service of America, Inc. (UPS)

7 KEY STRATEGIC QUESTIONS FOR CEP CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.1.5 Technological Advancements

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms