|

市場調査レポート

商品コード

1910470

北米シリアルバー市場- シェア分析、業界動向と統計、成長予測(2026年~2031年)North America Cereal Bar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米シリアルバー市場- シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 148 Pages

納期: 2~3営業日

|

概要

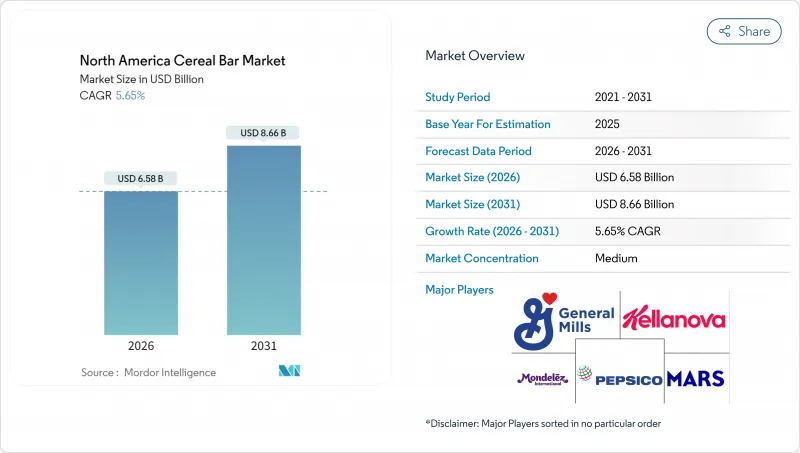

北米のシリアルバー市場は、2025年の623万米ドルから2026年には658万米ドルへ成長し、2026年から2031年にかけてCAGR5.65%で推移し、2031年までに866万米ドルに達すると予測されています。

この成長は、消費者の健康意識の高まり、規制の変更、そしてシリアルバーを単なる嗜好品から本格的な食事代替品へと変革する急速な製品改良によって牽引されています。米国食品医薬品局(FDA)が2025年2月に施行予定の「健康」に関する新たな定義では、添加糖分やナトリウムを多く含むレシピを抑制しつつ、全食品原料を組み込んだレシピを優先します。これを受け小売業者は自然食品・有機製品の棚スペースを拡大しており、各ブランドは米国農務省有機認証(USDA Organic)や非遺伝子組み換えプロジェクト認証(Non-GMO Project Verified)などの取得を推進しています。さらに北米消費者の71%が「タンパク質は自然食品から摂取したい」と回答しており、これにより高タンパク・低糖質のシリアルバーが一般食料品店で人気を集めています。電子商取引や消費者向け定期購入モデルの成長も、顧客獲得コストの削減やパーソナライズされた栄養バンドルの提供を可能にすることで、市場の加速に大きく貢献しています。

北米シリアルバー市場の動向と洞察

高まる健康意識と機能性栄養への注目

北米の消費者は、シリアルバーを単なる嗜好品ではなく機能性栄養製品として捉える動向が強まっています。この動向は、風味よりもタンパク質含有量、腸内環境改善成分、微量栄養素強化を重視する製品への選好が高まっていることを示しています。消費者の多くは、適切な栄養摂取と定期的な身体活動が加齢プロセスに好影響を与えると信じています。さらに、多くの消費者は栄養補助食品に頼るよりも、自然食品からタンパク質を摂取することを好みます。この嗜好の変化により、1食あたり10~15グラムのタンパク質を提供し、成分表がシンプルで分かりやすいシリアルバーの需要が高まっています。プレミアム製品には現在、スイカ、ハニーデューメロン、マンゴーの皮などから抽出されたプレバイオティック繊維が配合されており、健康志向の買い物客のニーズに応えています。彼らは腸内環境を総合的な健康の重要な要素として重視しています。

クリーンラベルおよび非遺伝子組み換え製品の拡充

クリーンラベル製品は、短い原材料表示、認識しやすい成分、最小限の加工を特徴とし、かつてはプレミアム製品の差別化要素でしたが、現在では大衆市場での流通を実現するための必須要件へと進化しています。オーガニックスナックバーの売上は著しく伸びており、近年では数多くのオーガニックバーが発売されています。この成長は、小売業者が米国農務省(USDA)のオーガニック認証を取得した製品に棚スペースを割り当てる傾向が強まっていることを反映しています。同様に、非遺伝子組み換え(Non-GMO)プロジェクト認証は、自然食品小売チャネルにおける流通の標準的な要件として台頭しています。非遺伝子組み換えプロジェクト認証を示すバタフライシールを掲げていないブランドは、ホールフーズマーケットやスプラウツファーマーズマーケットなどの主要小売店から商品が撤去されるリスクに直面しています。同時に、甘味料の革新も勢いを増し続けています。ステビア、モンクフルーツ、タガトース、アルロースなどの代替品が、高果糖コーンシロップやサトウキビ糖に取って代わりつつあり、インスリン急上昇を回避する低グリセミックオプションを求める消費者のニーズに応えています。

表示、健康強調表示、アレルゲンに関する規制変更

米国食品医薬品局(FDA)が2025年1月に提案したパッケージ前面の栄養情報表示枠では、飽和脂肪酸、ナトリウム、添加糖類の含有量を「低」「中」「高」で表示することが義務付けられます。企業は3~4年以内に準拠する必要があり、業界全体の年間コストは3億3,300万米ドルと推定されています。「高」添加糖の表示がある製品は、ターゲット、ウォルマート、クローガーなどの主要小売店の健康・ウェルネスコーナーでの陳列を失うリスクがあります。これによりブランドは再配合プロセスを余儀なくされ、利益率の低下や製品革新の遅延を招く可能性があります。カナダでは、2026年1月から施行されるパッケージ前面栄養表示シンボルにより、飽和脂肪酸、ナトリウム、糖類の閾値を超える製品には二言語表示と警告シンボルが義務付けられます。これにより、北米全域で事業を展開するブランドにはコンプライアンス上の課題が生じます。同様に、メキシコのNOM-051表示規制では、過剰なカロリー、糖質、飽和脂肪酸、トランス脂肪酸、ナトリウムを含む製品に黒い八角形の警告ラベルを義務付けています。この規制により、複数の警告シンボルに伴うネガティブなイメージを回避するため、2024年には再配合の波が引き起こされました。こうした重複する規制要件は、SKU(在庫管理単位)の複雑さを増大させます。単一製品が米国、カナダ、メキシコの規制を満たすためには、3種類の異なるラベルデザインが必要となる場合があります。これにより包装コストが15~20%増加し、市場投入までの期間が6~9カ月延長されます。専任の規制対応チームを持たない中小ブランドは、特に大きなコンプライアンス上の課題に直面しています。その結果、プライベート・エクイティ支援プラットフォームが中小ブランドを買収し、法的・表示コストをより大規模なポートフォリオで分散させるという統合圧力が高まっています。

セグメント分析

エネルギーバーおよび栄養バーは、2031年までにCAGR7.22%で成長すると予測されており、グラノーラ/ミューズリーバーの成長率を大きく上回ります。グラノーラ/ミューズリーバーは2025年に総販売量の44.88%を占めると見込まれますが、その成長率は127ベーシスポイント遅れています。エネルギー・栄養バーの成長が速い背景には、製品処方の進歩が挙げられます。現在では1食あたり15グラムのタンパク質を提供しながら、カロリーを200キロカロリー以下に抑えることが可能となりました。これらの特徴は、特に体重管理や持久力活動に注力する健康志向の消費者のニーズに応え、市場で好まれる選択肢となっています。

一方、グラノーラバーは米国食品医薬品局(FDA)による「健康」の定義改定により課題に直面しています。改訂されたガイドラインでは、グラノーラバーの主要成分である蜂蜜・オート麦・ナッツのクラスターに不可欠な添加糖類や飽和脂肪の使用が抑制されています。この規制変更により、メーカーは製品の魅力を維持しつつ、より厳格な基準に対応する必要が生じ、グラノーラバーは障壁に直面しています。結果として、グラノーラバーは変化する消費者嗜好と規制要件への適応がますます求められています。

オーガニックバーは2031年までCAGR7.45%で成長し、従来型製品の成長率を上回ると予測されています。2025年時点で従来型製品が総販売量の76.95%を占めていましたが、オーガニックバーは182ベーシスポイントの差でこれを上回ると予測されています。この成長は、2019年から2023年にかけて記録された427件のオーガニックバー新製品発売に後押しされ、小売業者が自然食品・オーガニック製品の品揃え拡大に努めていることを反映しています。ホールフーズ・マーケットやスプラウツ・ファーマーズ・マーケットなどの小売業者は、シリアルバー売り場の新規SKU(在庫管理単位)に対し、米国農務省(USDA)オーガニック認証または非遺伝子組み換え(Non-GMO)プロジェクト認証基準を満たすことを義務付ける方針を実施しています。これらの要件は、食品市場の10%を占めるナチュラル製品セグメントへの参入を実質的に規制するものであり、このセグメントは従来型カテゴリーよりも38倍速いペースで成長しています。

2024年3月、ゼネラルミルズ傘下のキャスカディアンファームは「オーガニックグラノーラバー」を発売し、USDAオーガニック認証の取得、非遺伝子組み換え原料の使用、人工添加物の不使用を強調しました。この戦略的ポジショニングにより、同製品はクローガーの「シンプルトゥルース」オーガニック商品群およびアルバートソンの「Oオーガニックス」商品配置計画への採用を実現しました。透明性とより健康的な選択肢を求める消費者のニーズに応えることで、カスカディアンファームは急成長する有機食品市場における存在感を強化し、自然で持続可能な製品への嗜好の高まりに対応しています。

北米シリアルバー市場レポートは、製品タイプ(グラノーラ/ミューズリーバー、エネルギー&栄養バー、その他)、機能性表示(オーガニック/従来品)、価格帯(大衆向け/プレミアム)、流通チャネル(スーパーマーケット/ハイパーマーケット、オンライン小売店など)、地域(米国、カナダなど)別に分析されています。市場予測は、金額(米ドル)および数量(トン)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 高まる健康意識と機能性栄養への注目

- クリーンラベルおよび非遺伝子組み換え製品の提供拡大

- 植物由来およびビーガン製品ラインの成長

- スポーツ、フィットネス、アウトドア活動への参加増加

- グルテンフリー、アレルギー対応、特殊食フォーマットの台頭

- 電子商取引および消費者向け直接販売の流通拡大

- 市場抑制要因

- 表示、健康強調表示、アレルゲンに関する規制変更

- 加工食品の健康効果に対する消費者の懐疑的な見方

- 新規配合の量産化における課題

- 新規配合の量産化における課題

- サプライチェーン分析

- 規制の見通し

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測(金額ベースおよび数量ベース)

- 製品タイプ別

- グラノーラ/ミューズリーバー

- エネルギー・栄養バー

- その他

- 機能性表示別

- オーガニック

- 従来型

- 価格帯別

- 大衆向け

- プレミアム

- 流通チャネル別

- スーパーマーケット/ハイパーマーケット

- オンライン小売店

- コンビニエンスストア

- その他流通チャネル

- 地域別

- 米国

- カナダ

- メキシコ

- その他北米地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- General Mills Inc.

- Kellanova

- PepsiCo, Inc.

- Mondelez International, Inc.

- Mars, Incorporated

- Post Holdings Inc.

- The Simply Good Foods Company

- McKee Foods Corporation

- Bobo's Oat Bars, LLC

- Nature's Path Foods, Inc.

- Core Foods, LLC

- Probar LLC

- Riverside Natural Foods Ltd

- Kashi Company

- Atkins Nutritionals

- Quaker Oats Company

- Health Warrior

- GoGo Quinoa Inc.

- Freedom Foods Group Limited

- Bariatrix Nutrition Inc.