北米の飼料用プロバイオティクス:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

North America Feed Probiotics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 217 Pages

- 納期

- 2~3営業日

- 商品コード

- 1683106

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

北米の飼料用プロバイオティクスの市場規模は、2025年に8億5,000万米ドルと推定され、2030年には11億1,000万米ドルに達し、予測期間(2025~2030年)のCAGRは5.57%で成長すると予測されています。

- プロバイオティクスは動物において、成長と生産の強化、病原体からの宿主の保護、免疫システムの改善、骨の強化、寄生虫との戦いなど、数多くの利点があることが証明されています。これらの利点により、この地域における飼料用プロバイオティクスの市場価値は2019年から2020年にかけて10.1%増加しました。

- ビフィズス菌と乳酸菌は、2022年に北米で最大の飼料プロバイオティクス副添加物であり、最大の市場シェアを占めました。これらのプロバイオティクス微生物は、消化管微生物叢のバランスと活動を調整することができます。

- 米国は動物人口が多く、飼料生産量が多いため、北米の飼料用プロバイオティクス市場で最大の国です。米国では、ビフィズス菌と乳酸菌が最大の飼料用プロバイオティクスの種類であり、飼料用プロバイオティクス市場の66.4%以上を占めています。

- 飼料用プロバイオティクスは主に家禽類と反芻動物に使用され、2022年の市場シェアはそれぞれ48.1%と25.8%です。プロバイオティクスは家禽の成長パフォーマンスと全体的な健康を促進し、抗生物質の使用が禁止されているため、抗生物質の代替品として家禽の飼料に配合されることが増えています。

- 北米における予測期間中の飼料プロバイオティクス市場の主な促進要因は、プロバイオティクス飼料の消費に関連する利点に対する認識の高まりと抗生物質の使用禁止です。全体として、北米の飼料用プロバイオティクス市場は、動物におけるプロバイオティクスの利点と、抗生物質の代わりにプロバイオティクスなどの代替ソリューションへのシフトにより、安定した成長が見込まれています。

- 北米の飼料用プロバイオティクス市場は近年著しい成長を遂げています。2022年の市場規模は7億2,240万米ドルで、2017~2022年の間に39%以上増加しました。この成長は、同地域の動物飼料におけるプロバイオティクスの重要性に対する認識が高まったことに起因すると考えられます。

- 北米では米国が最大のシェアを占めており、2022年の市場規模は5億580万米ドル、次いでメキシコが1億260万米ドル、カナダが7,730万米ドルです。米国の消費量が多いのは、動物人口が多いためです。2021年、同国には約17億8,000万頭の動物がおり、地域総人口の59.7%を占めています。

- 2022年、北米における飼料プロバイオティクスの消費シェアは、家禽類が48.1%と最大でした。反芻動物分野と養豚分野は、それぞれ市場シェアの25.7%と23.7%を占めています。反芻動物セグメントは、輸出需要と国内消費の増加により、CAGR 6.1%を記録し、予測期間中に最も速い速度で成長すると予想されます。

- 北米では2022年に約2億8,070万トンの配合飼料が生産され、米国がシェアの76.1%を占めました。生産量が多いのは、同国の動物人口が多いためです。

- 北米では食肉需要の高まりと動物の健康的な食生活に対する意識から、飼料用プロバイオティクスの需要が増加しています。同市場は予測期間中にCAGR 5.5%を記録し、力強い成長が見込まれています。

北米の飼料用プロバイオティクス市場動向

赤身肉よりも家禽肉の消費量が多く、米国は卵と家禽肉の世界最大の生産国であることが家禽肉生産の需要を促進しています。

- 北米の家禽産業は過去5年間で大きな成長を遂げ、2017年から2022年にかけて家禽頭数は5.0%増加しました。この成長の主因は、家禽肉とその他の家禽製品の需要増です。米国は世界最大の鶏肉生産国であり、世界第2位の輸出国であり、また主要鶏卵生産国として北米の鶏肉産業を支配しています。米国は2022年にはこの地域の鶏肉生産量の62.0%を占めています。この業界の高い利益率が新たな鶏肉生産者を惹きつけ、この地域の生産者数の増加をもたらしています。例えば、カナダの鶏卵生産者数は2016年の1,062社から2021年には1,205社に増加しています。

- 家禽類、特にブロイラー肉は、他の家畜に比べて成熟と市場体重が早いため、大量に生産されます。ブロイラーを含む家禽類は狭いスペースで飼育できるため、生産者は狭い土地など様々な環境で家禽を飼育することができます。こうした利点により家禽の生産はより現実的なものとなり、その結果、メキシコの家禽生産は2022年に前年比12%増加しました。

- 家禽肉の消費量は牛肉や豚肉の消費量を大きく上回っています。赤身肉を食べることによる健康リスクの高まりから、より赤身で健康的なタンパク源として鶏肉を選ぶ人が増えています。この動向は今後も続くと予想され、同地域の鶏肉産業の成長を牽引します。国内外市場からの鶏肉製品需要の増加と鶏肉生産量の増加が、予測期間中の市場成長をさらに促進すると予想されます。

小売業の拡大、高品質水産物の需要が、マクロ栄養素と微量栄養素を豊富に含む養殖用飼料の需要を増加させています。

- 北米地域の養殖飼料生産量は世界生産量のごく一部で、2022年にはわずか3.8%に過ぎないです。しかし、多様な水産物への需要が現地生産を牽引しており、飼料生産は2017年から2022年にかけて9.2%増加しています。栄養バランスの取れた飼料に対する需要の高まりを受けて、この地域の飼料製造業者は、生産量を2022年の220万トンから2029年には260万トンに増加させると予想されます。水産養殖種に提供される配合飼料には、集約的な飼育条件下での健全な成長に必要なマクロ栄養素と微量栄養素が含まれており、これがこの地域における水産養殖用飼料の需要増に寄与しています。

- 2022年に飼料生産量の73.2%を占めた魚類は、飼料生産量において最も顕著な種です。人間の食事における魚の健康上の利点に対する意識の高まり、食品消費パターンの変化、小売セクターの拡大、国際市場における高い需要が、この地域における魚生産の成長に寄与しています。魚用飼料の生産量は、生産者が動物の健康と成績を確保するための栄養管理に重点を置いているため、2022年の160万トンから2029年には190万トンに増加すると予想されます。

- カナダの養殖生産者は2020年に飼料に3億9,380万米ドルを費やし、これは2016年から6.6%増加し、高品質の水産食品に対する需要の増加を示しています。全体として、多様な水産物に対する需要の増加と養殖種に対する栄養バランスの取れた飼料の必要性は、今後数年間、北米地域における養殖飼料生産の成長を促進すると予想されます。

北米の飼料用プロバイオティクス産業の概要

北米の飼料用プロバイオティクス市場は適度に統合されており、上位5社で53.67%を占めています。この市場の主要企業は以下の通りです。 Adisseo, DSM Nutritional Products AG, Evonik Industries AG, IFF(Danisco Animal Nutrition)and Kerry Group PLC(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 動物頭数

- 家禽

- 反芻動物

- 豚

- 飼料生産

- 水産養殖

- 家禽

- 反芻動物

- 養豚

- 規制の枠組み

- カナダ

- メキシコ

- 米国

- バリューチェーンと流通チャネルの分析

第5章 市場セグメンテーション

- サブ添加物別

- ビフィズス菌

- 腸球菌

- 乳酸菌

- ペディオコッカス

- レンサ球菌

- その他のプロバイオティクス

- 動物別

- 水産養殖

- サブアニマル別

- 魚類

- エビ

- その他の水産養殖種

- 家禽類

- サブアニマル別

- ブロイラー

- レイヤー

- その他の家禽

- 反芻動物

- サブアニマル別

- 肉牛

- 乳牛

- その他の反芻動物

- 豚

- その他の動物

- 水産養殖

- 国別

- カナダ

- メキシコ

- 米国

- その他北米地域

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)。

- Adisseo

- Cargill Inc.

- CHR. Hansen A/S

- DSM Nutritional Products AG

- Evonik Industries AG

- IFF(Danisco Animal Nutrition)

- Kemin Industries

- Kerry Group PLC

- Lallemand Inc.

- Marubeni Corporation(Orffa International Holding B.V.)

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要洞察

- データパック

- 用語集

目次

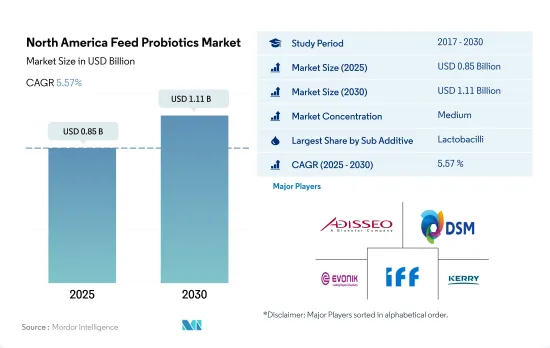

The North America Feed Probiotics Market size is estimated at 0.85 billion USD in 2025, and is expected to reach 1.11 billion USD by 2030, growing at a CAGR of 5.57% during the forecast period (2025-2030).

- Probiotics have been proven to have numerous benefits in animals, including enhancing growth and production, protecting the host against pathogens, improving the immune system, strengthening bones, and fighting parasitism. These benefits have driven the market value of feed probiotics in the region, which increased by 10.1% between 2019 and 2020.

- Bifidobacteria and lactobacilli were the largest feed probiotic sub-additives in North America in 2022, accounting for the largest market share. These probiotic microorganisms can modulate the balance and activities of the gastrointestinal microbiota.

- The United States is the largest country in the North American feed probiotics market due to its high animal population and high feed production. In the United States, bifidobacteria and lactobacilli are the largest feed probiotic types, accounting for more than 66.4% of the feed probiotic market.

- Feed probiotics are predominantly used in poultry and ruminants, with a market share of 48.1% and 25.8%, respectively, in the market in 2022. Probiotics promote the growth performance and overall health of poultry and are increasingly being included in poultry diets as an alternative to antibiotics since the usage of antibiotics is banned in animal feed.

- The major driving factors for the feed probiotics market during the forecast period in North America are the increased awareness of the benefits associated with probiotic feed consumption and the ban on antibiotics usage. Overall, the North American feed probiotics market is expected to experience steady growth due to the benefits of probiotics in animals and the shift toward alternative solutions, such as probiotics, in place of antibiotics.

- The feed probiotics market in North America has witnessed significant growth in recent years. In 2022, the market was valued at USD 722.4 million, an increase of more than 39% during 2017-2022. The growth could be attributed to the increased awareness of the importance of probiotics in animal diets in the region.

- The United States holds the largest share of the market in North America, valued at USD 505.8 million in 2022, followed by Mexico and Canada at USD 102.6 million and USD 77.3 million, respectively. The high consumption in the United States is due to the presence of a large animal population. In 2021, the country had approximately 1.78 billion animals, accounting for 59.7% of the total regional population.

- Poultry birds accounted for the largest consumption share of feed probiotics in North America, with 48.1%, in 2022, owing to the high poultry population in the region. The ruminants and swine segments accounted for 25.7% and 23.7% of the market share, respectively. The ruminant segment is expected to grow at the fastest rate during the forecast period, registering a CAGR of 6.1%, owing to increasing export demand and domestic consumption.

- North America produced around 280.7 million metric tons of compound feed in 2022, with the United States accounting for 76.1% of the share. The high production was attributed to the large animal population in the country.

- The demand for feed probiotics is increasing in North America due to the rising demand for meat and awareness of healthy diets for animals. The market is expected to witness strong growth, registering a CAGR of 5.5% during the forecast period.

North America Feed Probiotics Market Trends

Higher consumption of poultry meat than red meat and the United States is globally largest producer of eggs and poultry meat is driving the demand for poultry production

- The North American poultry industry experienced significant growth over the last five years, with the poultry headcount increasing by 5.0% from 2017 to 2022. This growth is largely due to the increasing demand for poultry meat and other poultry products. The United States dominates the North American poultry industry as the world's largest producer and second-largest exporter of poultry meat, as well as a major egg producer. The United States accounted for 62.0% of the region's total poultry production in 2022. The high-profit margin in the industry is attracting new poultry producers, leading to an increase in the number of producers in the region. For example, the number of egg producers in Canada has increased from 1,062 in 2016 to 1,205 in 2021.

- Poultry birds, especially broiler meat, are produced in large quantities due to their quick maturity and market weight, which is faster than other livestock. Poultry birds, including broilers, can be raised in small spaces, making it possible for producers to raise poultry in a variety of environments, including small plots of land. These advantages make poultry production more feasible, and as a result, Mexican poultry production increased by 12% in 2022 from the previous year.

- Poultry meat consumption is significantly higher than that of beef or pork. More people are choosing poultry as a leaner and healthier source of protein due to the rising health risks linked to eating red meat. This trend is expected to continue, driving the growth of the poultry industry in the region. The increasing demand for poultry products from both domestic and international markets and rising poultry production are expected to further drive the growth of the market during the forecast period.

Expansion of retail industry, and demand for high-quality seafood is increasing the demand for macro-nutrients and micro-nutrients rich aquaculture feed

- Aquaculture feed production in the North American region accounts for a small fraction of the global production, representing only 3.8% in 2022. However, the demand for diverse seafood products is driving local production, and feed production has grown by 9.2% between 2017 and 2022. In response to the increasing demand for nutritionally balanced feed, feed millers in the region are expected to increase production from 2.2 million metric tons in 2022 to 2.6 million metric tons in 2029. The compound feed offered to aquaculture species contains the macro- and micronutrients needed for healthy growth under intensive rearing conditions, which is contributing to the increased demand for aquaculture feed in the region.

- Fish, which accounted for 73.2% of feed production in 2022, is the most prominent species in terms of feed production. The rising awareness of the health benefits of fish in the human diet, changing food consumption patterns, the expansion of the retail sector, and high demand in the international market are contributing to the growth of fish production in the region. Fish feed production is expected to increase from 1.6 million metric tons in 2022 to 1.9 million metric tons in 2029 as producers focus on nutritional management to ensure the health and performance of their animals.

- Canada's aquaculture producers spent USD 393.8 million on feed in 2020, a 6.6% increase from 2016, demonstrating the increasing demand for high-quality aquatic food. Overall, the increasing demand for diverse seafood products and the need for nutritionally balanced feed for aquaculture species are expected to drive the growth of aquaculture feed production in the North American region in the coming years.

North America Feed Probiotics Industry Overview

The North America Feed Probiotics Market is moderately consolidated, with the top five companies occupying 53.67%. The major players in this market are Adisseo, DSM Nutritional Products AG, Evonik Industries AG, IFF(Danisco Animal Nutrition) and Kerry Group PLC (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Animal Headcount

- 4.1.1 Poultry

- 4.1.2 Ruminants

- 4.1.3 Swine

- 4.2 Feed Production

- 4.2.1 Aquaculture

- 4.2.2 Poultry

- 4.2.3 Ruminants

- 4.2.4 Swine

- 4.3 Regulatory Framework

- 4.3.1 Canada

- 4.3.2 Mexico

- 4.3.3 United States

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Sub Additive

- 5.1.1 Bifidobacteria

- 5.1.2 Enterococcus

- 5.1.3 Lactobacilli

- 5.1.4 Pediococcus

- 5.1.5 Streptococcus

- 5.1.6 Other Probiotics

- 5.2 Animal

- 5.2.1 Aquaculture

- 5.2.1.1 By Sub Animal

- 5.2.1.1.1 Fish

- 5.2.1.1.2 Shrimp

- 5.2.1.1.3 fish

- 5.2.1.1.4 Other Aquaculture Species

- 5.2.2 Poultry

- 5.2.2.1 By Sub Animal

- 5.2.2.1.1 Broiler

- 5.2.2.1.2 Layer

- 5.2.2.1.3 Other Poultry Birds

- 5.2.3 Ruminants

- 5.2.3.1 By Sub Animal

- 5.2.3.1.1 Beef Cattle

- 5.2.3.1.2 Dairy Cattle

- 5.2.3.1.3 Other Ruminants

- 5.2.4 Swine

- 5.2.5 Other Animals

- 5.2.1 Aquaculture

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Adisseo

- 6.4.2 Cargill Inc.

- 6.4.3 CHR. Hansen A/S

- 6.4.4 DSM Nutritional Products AG

- 6.4.5 Evonik Industries AG

- 6.4.6 IFF(Danisco Animal Nutrition)

- 6.4.7 Kemin Industries

- 6.4.8 Kerry Group PLC

- 6.4.9 Lallemand Inc.

- 6.4.10 Marubeni Corporation (Orffa International Holding B.V.)

7 KEY STRATEGIC QUESTIONS FOR FEED ADDITIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 217 Pages

- 納期

- 2~3営業日