|

市場調査レポート

商品コード

1645105

炭素会計:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Carbon Accounting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 炭素会計:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

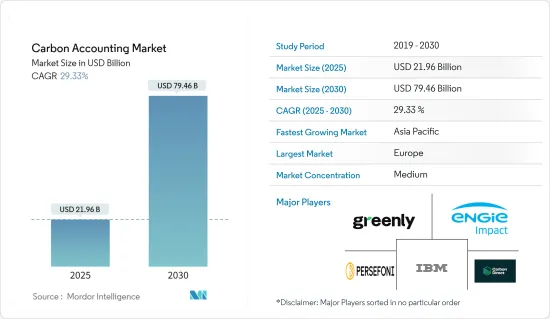

炭素会計市場規模は2025年に219億6,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは29.33%で、2030年には794億6,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、持続可能性目標達成に向けた企業の関心の高まりや、炭素排出量測定・規制をめぐる規制・コンプライアンスの厳格化といった要因が、予測期間中の炭素会計市場の最も大きな促進要因の1つになると予想されます。

- その一方で、正確な計算のためのデータ蓄積や炭素会計手法の導入は複雑であり、予測期間中、市場にとって脅威となることが予想されます。

- しかし、より革新的で効率的な炭素会計手法とソフトウェアの開発における継続的な進歩は続いています。この要因は、今後市場にいくつかの機会を生み出すと予想されます。

- アジア太平洋が市場を独占しており、予測期間中に最も高いCAGRで推移する可能性が高いです。中国、インド、日本、その他の諸国が、これらの国における産業やインフラ開発活動の増加により、市場を牽引しています。

炭素会計市場の動向

電力事業セグメントが著しい成長を遂げる

- 電力事業は温室効果ガス排出の重要な原因であるため、炭素会計にとって最も重要な産業の一つです。これらの産業は、発電を石油・石炭・天然ガスなどの化石燃料に大きく依存しています。これらの排出源は温室効果ガスを大量に排出するため、投資家や利害関係者への情報提供とともに、これらの企業が規制やコンプライアンス要件を遵守するために炭素会計が必要となります。

- 開発企業は、広範な炭素会計を実施することで排出量の多い排出源を特定し、その増加に対抗して排出量を削減するための戦略や方針を策定します。これらの戦略や方針には、再生可能エネルギー源への投資、効率の改善、炭素回収技術の導入、よりクリーンな化石燃料技術の採用などが含まれます。炭素会計は、発電施設、送配電システム、インフラといった複雑な運用要素にまたがるカーボンフットプリントを評価し、取り組みの優先順位付けと資源の最適化を可能にします。

- 国際再生可能エネルギー機関によると、二酸化炭素排出量の削減とよりクリーンなエネルギー源の採用という世界の要請により、主要企業は再生可能エネルギー発電プロジェクトの開発に多額の投資を行い、再生可能エネルギーの設備容量を大幅に増加させています。2023年、世界の再生可能エネルギー設備容量は、2022年の3,396.32GWに対し約3,869.7GWとなり、約14%の成長率を記録しました。

- さらに、炭素会計は、潜在的な供給の途絶、インフラの損傷、消費者の需要の変化など、気候変動がもたらすリスクを評価し、軽減するための重要なデータを電力会社に記載しています。これは、低炭素の未来に向けた長期的で弾力的な計画とサステイナブル投資の意思決定に役立ちます。

- 例えば、2024年3月、主要な再生可能エネルギープロジェクト開発・運営会社であるGE Vernovaは、コートジボワールにあるGlobeleqのAzito Energie S.A.発電所に炭素会計ソフトウェアを導入すると発表しました。同発電所は、同国最大の天然ガス発電所です。GEヴェルノヴァは、このソフトウェアが炭素排出に関する必要な情報を提供し、より効率的なプロセスや設備を開発するための情報源を特定することを期待しています。

- したがって、上記のように、電力事業セグメントは予測期間中に大きな成長率を示すことが期待されています。

アジア太平洋が市場を独占する

- アジア太平洋は、今後数年間、世界の炭素会計市場を独占すると考えられます。同地域は、エネルギー需要を満たすために化石燃料に主に依存しているため、急速な工業化、人口増加、気候変動への対応への緊急性の高まりがその原動力となっています。製造業の中心地であり新興経済諸国である中国、インド、日本、東南アジア諸国などは、世界の温室効果ガス排出の主要な原因となっています。しかし、これらの国々はサステイナブル開発目標を積極的に追求し、二酸化炭素排出量を抑制する施策を実施しています。

- アジア太平洋における産業活動とエネルギー需要の増大は、排出量を正確に測定、報告し、最終的に削減するための強固な炭素会計プラクティスに対する需要を促進しています。この地域で事業を展開する多国籍企業は、環境規制や報告要件の厳格化に直面しており、先進的炭素会計システムの導入を推進しています。さらに、この地域では太陽光発電や風力発電などの再生可能エネルギー開発に力を入れており、排出削減量を定量化するための包括的な炭素ライフサイクル分析が急務となっています。

- 2023年11月、中国政府は製造業への外資参入規制を撤廃する意向を表明し、外資系企業を受け入れるという国家の継続的なコミットメントを示しました。この先進的な措置は、中国の製造業の成長を促進し、製造業全体に影響を与え、予測期間中に炭素会計市場を前進させると予想されます。

- さらに、アジア太平洋市場では、新しいクリーン技術、インフラのアップグレード、その他様々なクリーンエネルギーソリューション製品やプロジェクトにおいて、大きな開発と投資が行われています。このため、炭素排出量を追跡・削減し、非効率な資源を特定するために炭素会計手法を採用する必要があります。このため、様々な国際的企業との協力や、より正確な炭素会計手法の開発が行われています。アジア太平洋の消費者や利害関係者の環境意識の高まりは、透明性の高い炭素報告に対する企業の需要をさらに高めています。

- 電池、自動車、計器、機器などの製造業の大規模な開拓は、国際市場参入企業が多様な産業に対応する炭素会計サービスプロバイダー、ソフトウェア開発者、コンサルティング会社を開拓する巨大な機会をもたらしています。

- したがって、アジア太平洋が予測期間中に市場セグメントを支配すると予想されます。

炭素会計産業概要

世界の炭素会計市場は半固定的です。この市場の主要企業(順不同)には、Greenly、International Business Machines Corporation、ENGIE Impact、Persefoni AI、Carbon Directなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 企業の持続可能性目標

- 厳しい規制とコンプライアンス

- 抑制要因

- 炭素会計の複雑さ

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 市場タイプ

- クラウドベース

- オンプレミス

- エンドユーザー

- 石油・ガス

- 電力事業

- 建設インフラ

- 通信

- 飲食品

- その他

- 2029年までの市場規模・需要予測(地域別)

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- ノルディック

- ロシア

- トルコ

- その他の欧州

- アジア太平洋

- 中国

- インド

- オーストラリア

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- ナイジェリア

- エジプト

- カタール

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Greenly

- International Business Machines Corporation

- ENGIE Impact

- Persefoni AI

- Normative

- Carbon Direct

- Sphera

- Emitwise

- SINAI Technologies

- Diligent Corporation

- 市場ランキング/シェア分析

第7章 市場機会と今後の動向

- 革新的な炭素会計ソリューションの開発

目次

Product Code: 50002216

The Carbon Accounting Market size is estimated at USD 21.96 billion in 2025, and is expected to reach USD 79.46 billion by 2030, at a CAGR of 29.33% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as growing corporate focus on achieving their sustainability goals and increasing stringent regulations and compliances over carbon emission measuring and regulations are expected to be among the most significant drivers for the carbon accounting market during the forecast period.

- On the other hand, the complexity of accumulating data and implementing carbon accounting methodology for accurate calculation is high, which is expected to pose a threat to the market during the forecast period.

- However, continued advancements in developing more innovative and efficient carbon accounting methodologies and software are ongoing. This factor is expected to create several opportunities for the market in the future.

- Asia-Pacific dominates the market and will likely register the highest CAGR during the forecast period. China, India, Japan, and others drive it due to the growing number of industries and infrastructural development activities in these countries.

Carbon Accounting Market Trends

The Power Utilities Segment to Witness Significant Growth

- The power utilities end-user segment is one of the most essential industries for carbon accounting as these segments are significant contributors to greenhouse gas emissions. These industries heavily rely on fossil fuels such as oil, coal, and natural gas for power generation. These sources are heavy emitters of greenhouse gases, which makes carbon accounting necessary for these companies to comply with the regulations and compliance requirements, along with informing investors and stakeholders.

- Utilities will identify the highest emitting sources by conducting extensive carbon accounting practices and developing strategies and policies to counter the growth and reduce emissions. These strategies and policies can include investing in renewable energy sources, improving efficiency, implementing carbon capture technologies, or adopting cleaner fossil fuel technology. Carbon accounting allows for assessing the carbon footprint across complex operational components like generation facilities, transmission/distribution systems, and supporting infrastructure, prioritizing efforts and optimizing resources.

- According to the International Renewable Energy Agency, the global imperative of reducing carbon emissions and adopting cleaner energy sources has led significant power utility companies to invest heavily in developing renewable energy power projects, significantly increasing the renewable energy installed capacity. In 2023, the global renewable energy installed capacity was around 3869.7 GW compared to 3396.32 GW in 2022, registering a growth rate of approximately 14%.

- Moreover, carbon accounting provides power utilities with crucial data to assess and mitigate risks posed by climate change, such as potential supply disruptions, infrastructure damage, and shifting consumer demands. This informs long-term resilient planning and sustainable investment decisions for a low-carbon future.

- For instance, in March 2024, GE Vernova, a primary renewable energy project developer and operator, announced that it would deploy carbon accounting software in Globeleq's Azito Energie S.A. power plant in Cote D'Ivoire. This is the largest natural gas power plant in the country. GE Vernova expects the software to provide necessary information on carbon emissions and identify sources to develop more efficient processes and equipment.

- Therefore, as mentioned above, the power utilities segment is expected to witness a significant growth rate during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific will dominate the global carbon accounting market in the coming years. It is driven by rapid industrialization, population growth, and the increasing urgency to address climate change, as the region predominantly relies on fossil fuels to meet its energy demands. As manufacturing hubs and developing economies, countries like China, India, Japan, and Southeast Asian nations are major contributors to global greenhouse gas emissions. However, they are also actively pursuing sustainable development goals and implementing policies to curb their carbon footprints.

- The growing intensity of industrial activities and energy demands across Asia-Pacific drives the demand for robust carbon accounting practices to accurately measure, report, and ultimately reduce emissions. Multinational corporations operating in the region face stricter environmental regulations and reporting requirements, driving the adoption of sophisticated carbon accounting systems. Additionally, the region's focus on renewable energy development, such as solar and wind power, creates a pressing need for comprehensive carbon lifecycle analysis to quantify emissions savings.

- In November 2023, the Chinese government declared its intention to eliminate all restrictions on foreign involvement in manufacturing, showcasing the nation's ongoing commitment to embracing foreign enterprises. This progressive step is anticipated to foster growth in the Chinese manufacturing sector, subsequently influencing the overall manufacturing landscape and propelling the carbon accounting market forward during the forecast period.

- Moreover, the Asia-Pacific market has witnessed significant developments and investments in new clean technologies, infrastructure upgrades, and various other clean energy solution products and projects. This necessitates adopting carbon accounting methods to track and reduce carbon emissions and identify inefficient resources. This has led to collaboration with various international players and the development of more precise carbon accounting methodologies. The rising environmental consciousness among consumers and stakeholders in Asia-Pacific further fuels companies' demand for transparent carbon reporting.

- The large-scale development of manufacturing industries, such as batteries, automobiles, instruments, and equipment, presents enormous opportunities for international market players to explore carbon accounting service providers, software developers, and consulting firms catering to diverse industries.

- Thus, the Asia-Pacific region is expected to dominate the market segment during the forecast period.

Carbon Accounting Industry Overview

The global carbon accounting market is semi-consolidated. Some key players in this market (in no particular order) include Greenly, International Business Machines Corporation, ENGIE Impact, Persefoni AI, and Carbon Direct.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Corporate Sustainability Goals

- 4.5.1.2 Stringent Regultions and Compliance

- 4.5.2 Restraints

- 4.5.2.1 High Complexity in Carbon Accounting

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Cloud Based

- 5.1.2 On Premise

- 5.2 End Users

- 5.2.1 Oil and Gas

- 5.2.2 Power Utilities

- 5.2.3 Construction and Infrastructure

- 5.2.4 Telecommunication

- 5.2.5 Food and Beverages

- 5.2.6 Other End Users

- 5.3 Geography [Market Size and Demand Forecast till 2029 (for Regions Only)]

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 NORDIC

- 5.3.2.7 Russia

- 5.3.2.8 Turkey

- 5.3.2.9 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Australia

- 5.3.3.4 Japan

- 5.3.3.5 South Korea

- 5.3.3.6 Malaysia

- 5.3.3.7 Thailand

- 5.3.3.8 Indonesia

- 5.3.3.9 Vietnam

- 5.3.3.10 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 Saudi Arabia

- 5.3.4.2 United Arab Emirates

- 5.3.4.3 Nigeria

- 5.3.4.4 Egypt

- 5.3.4.5 Qatar

- 5.3.4.6 South Africa

- 5.3.4.7 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Colombia

- 5.3.5.4 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Greenly

- 6.3.2 International Business Machines Corporation

- 6.3.3 ENGIE Impact

- 6.3.4 Persefoni AI

- 6.3.5 Normative

- 6.3.6 Carbon Direct

- 6.3.7 Sphera

- 6.3.8 Emitwise

- 6.3.9 SINAI Technologies

- 6.3.10 Diligent Corporation

- 6.4 Market Ranking/Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Innovative Carbon Accounting Solutions