|

市場調査レポート

商品コード

1637900

炭素管理システム-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Carbon Management System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 炭素管理システム-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

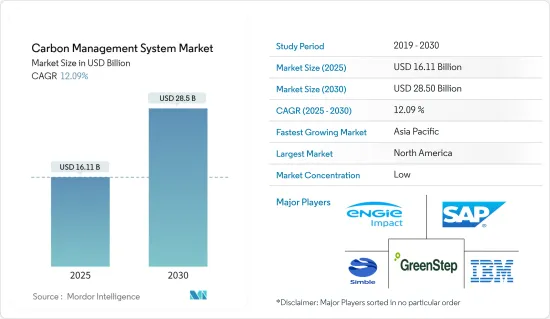

炭素管理システムの市場規模は、2025年に161億1,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは12.09%で、2030年には285億米ドルに達すると予測されます。

気候変動規制の厳格化、炭素排出コストの増大、炭素管理関連技術の進化により、炭素管理システムの需要は継続的に増加しています。

炭素排出施策の採用は、炭素管理システムの世界の需要増加の主要要因です。これらの施策は、排出削減目標、炭素の価格設定と課税、コンプライアンス、規制要件など、炭素管理システムの導入に有利な環境を作り出しています。

先進技術を炭素管理プラットフォームに統合することで、炭素排出量をリアルタイムで追跡し、必要な対策を効果的に講じることが可能になり、炭素管理システムの市場売上を牽引しています。

さらに、持続可能性と企業の社会的責任の重要性に対する企業の意識が高まる中、多くの組織が炭素削減目標を設定し、国際的な気候変動に関する公約に沿った炭素ニュートラルを目指しています。このように、企業による炭素管理システムの導入は、進捗状況を追跡し、開発すべきセグメントを特定するために、かなり増加しています。

規制環境は絶えず進化しているため、企業が異なるシステムを比較して導入することは困難です。技術的な変化は、炭素管理システムプロバイダーが最新の技術動向に対応するための課題となっており、これが市場成長を阻む要因となっています。

持続可能性を維持するため、市場参入企業は炭素管理セグメントにおけるパートナーシップや提携を通じて、その能力とリーチを拡大しつつあります。例えば、国際エネルギー機関(IEA)によると、2050年までにネット・ゼロ・エミッションを達成するためには、2030年までに世界のクリーンエネルギーへの年間投資額が3倍以上の約4兆米ドルに達する必要があります。この取り組みによって、多くの新たな雇用機会が生まれ、世界経済が大幅に活性化し、10年後までには誰もが電気とクリーンな調理法を利用できるようになると期待されています。

気候変動を含む地球環境の課題は、COVID-19の大流行により、より目に見えるものとなりました。組織や政府が持続可能性と環境フットプリントの削減に注力するにつれ、炭素管理ソリューションへの需要が高まっています。また、パンデミック発生時にはリモートワークが必須であったため、企業は環境データの管理や持続可能性への取り組みにおける効果的なコラボレーションのためにデジタルソリューションを採用しています。

炭素管理システム市場の動向

石油・ガス産業が成長を確認する

- 石油・ガス産業は市場成長に大きく貢献すると予想されます。世界最大かつ最も炭素集約的な産業の1つとして、二酸化炭素排出量を削減し、よりサステイナブル未来へ移行することへの圧力が高まっている

- デジタル技術は、石油会社がより厳しい排出削減目標を設定する中で、スコープ1と2の排出量に利益をもたらす可能性があります。油井やパイプラインから排出される有害なメタンを追跡することは極めて重要であり、機械学習はエネルギー使用をより効率的に改良するのに役立ちます。ドローン、センサ、衛星、カメラのデータも不可欠です。

- 複数の企業が、産業運営における二酸化炭素排出量の削減と、ネット・ゼロへの移行促進に取り組んでいます。例えばAVEVAは、セメント、鉄鋼、石油・ガスなど炭素集約型産業の企業向けに施設の設計・建設を行うAker Carbon Captureと緊密に連携しています。

- 温室効果ガス排出量削減に対する投資家の要求が高まっているため、石油・ガス生産者が炭素排出量の評価に使用できるソフトウェアをリリースするデジタル企業が増えています。2024年7月、California Resources Corporationは、Aera Energy LLC(Aera)との全株式統合の完了を発表しました。この変革的な取引により、カリフォルニア州の増大するエネルギー需要に対応するための大規模な規模と資産の耐久性が創出され、同州の野心的な気候変動目標の達成を支援するための先進的な炭素管理プラットフォームが拡大されます。

北米が最大の市場シェアを占める

- 北米における複数の炭素管理プログラムの開始は、空港炭素認証を空港炭素管理の世界標準とするための重要な一歩です。このイニシアチブの発足式では、シアトル・タコマ国際空港が北米で初めて認定を受けました。

- ネット・ゼロ・エミッションに関するいくつかの政府イニシアチブは、市場の需要を促進すると予想されます。米国エネルギー省(DOE)は、2050年までのネット・ゼロ・エミッションという政府目標に呼応して、炭素ネガティブ・ショットを開始しました。これは、大気中から二酸化炭素を回収し、ギガトン規模で二酸化炭素換算で100米ドル/ネット・トン以下で貯蔵する二酸化炭素除去経路の技術革新を総力を挙げて呼びかけるものです。

- また、老朽化した公共施設からのエネルギー排出を削減するための政府の施策により、市場の需要も増加しています。例えば、米国一般調達庁がIBMコーポレーションと締結した契約により、州政府と連邦政府が所有する最もエネルギー集約度の高い50の建物に、効率的でスマートなビル技術が導入されることになりました。

- エネルギー情報局(EIA)によると、米国のエネルギー関連のCO2排出量は、2023年には2022年に比べてわずかに減少しました。排出量は多くの経済産業で減少したが、2023年の米国のエネルギー関連CO2排出量削減の80%以上は電力産業で発生しました。これらの削減は、天然ガスと太陽光発電が発電構成の大部分を占めるようになったため、石炭火力発電が減少したことが主要原因です。したがって、エネルギー産業から排出される二酸化炭素の削減に政府が注力していることは、今後数年間、市場の需要を積極的に支える可能性が高いです。

炭素管理システム産業概要

炭素管理システム市場は細分化されており、多くの参入企業が管理・モニタリング用のソフトウェアを提供しています。このような数の急増は、クラウドサービスの利用拡大が原因となっています。コンサルティングサービスを提供する事業者は、予測期間中も同様のパターンを示し、安定した成長が見込まれます。

- 2024年6月-確実な統合レポーティングソリューションの世界的プロバイダーであるWorkivaは、Workiva Carbonの発売により技術ポートフォリオを拡大しました。環境・社会・ガバナンス(ESG)とサステナビリティプラットフォームを強化し、世界的に厳しい気候変動規制を効果的に遵守できるようにします。

- 2024年3月-SLBは、炭素回収事業をAker Carbon Capture(ACC)と統合し、大規模な産業脱炭素化の加速を支援することで合意したと発表。この合意により、補完的な技術ポートフォリオ、最先端のプロセス設計専門知識、確立されたプロジェクトデリバリープラットフォームが統合される可能性があります。この統合は、ACCが提供する商用炭素回収製品と、SLBの新技術開発と産業化能力を活用することになります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- 環境問題への関心の高まりと炭素フットプリント削減への注力

- 市場課題

- 変動するエネルギーと資源需要の管理

第6章 市場セグメンテーション

- サービス別

- ソフトウェア

- サービス別

- 用途別

- エネルギー

- 温室効果ガス管理

- 大気質管理

- 持続可能性

- その他

- エンドユーザー産業別

- 石油・ガス

- 製造業

- 医療

- ITと電気通信

- その他のエンドユーザー別

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Simble Solutions Ltd

- IBM Corporation

- ENGIE Impact

- GreenStep Solutions Inc.

- SAP SE

- Enablon SA

- IsoMetrix

- Schneider Electric SE

- Salesforce.com Inc.

- Greenstone+Ltd

- Microsoft Corporation

- Sphera

第8章 投資分析

第9章 市場の将来展望

The Carbon Management System Market size is estimated at USD 16.11 billion in 2025, and is expected to reach USD 28.50 billion by 2030, at a CAGR of 12.09% during the forecast period (2025-2030).

The demand for carbon management systems is continuously increasing due to the increasing stringency of climate change regulations, the growing cost of carbon emissions, and evolving technologies related to carbon management.

The introduction of carbon emission policies is a key driver of the increasing demand for carbon management systems globally. These policies create a favorable environment for adopting carbon management systems with emission reduction targets, carbon pricing and taxation, compliance, and regulatory requirements.

The integration of advanced technologies with carbon management platforms enables real-time tracking of carbon emissions to take effective necessary prevention, driving the sales of carbon management systems in the market.

In addition, with growing awareness among businesses about the importance of sustainability and corporate social responsibility, many organizations are setting targets for carbon reduction, aiming for carbon neutrality that aligns with international climate commitments. In this way, the adoption of carbon management systems by companies is increasing considerably to track progress and identify areas for development.

The continuously evolving regulatory environment makes it difficult for businesses to compare different systems for implementation. Technological changes present challenges for carbon management system providers to keep up with the latest technology trends, which are some factors challenging market growth.

In order to preserve sustainability, market players are expanding their capacities and reach through partnerships and alliances in the area of carbon management. For instance, according to the International Energy Agency, to reach net zero emissions by 2050, annual clean energy investment worldwide will demand more than triple by 2030 to approximately USD 4 trillion. This initiative is expected to generate a multitude of new employment opportunities, substantially boost the worldwide economy, and ensure everyone has access to electricity and clean cooking methods by the decade's end.

Global environmental challenges, including climate changes, have become more visible because of the COVID-19 pandemic. The demand for carbon management solutions has grown as organizations and governments focus on sustainability and reducing their environmental footprint. In addition, businesses have been adopting digital solutions for the management of their environmental data and effective collaboration on sustainability initiatives, as remote work was the compulsion during the pandemic.

Carbon Management System Market Trends

The Oil and Gas Industry to Witness Growth

- The oil and gas industry is expected to contribute significantly to market growth. As one of the largest and most carbon-intensive industries worldwide, it is facing increased pressure to reduce its carbon footprint and transition toward a more sustainable future.

- Digital technologies could benefit scope 1 and 2 emissions as oil firms set more challenging targets for emissions reduction. Tracking harmful methane emissions from oil wells and pipelines is crucial, and machine learning helps refine energy use more efficiently. Drones, sensors, satellite, and camera data are also vital.

- Several companies are working on mitigating the carbon dioxide emissions of industrial operations and accelerating the transition to net zero. For instance, AVEVA is working closely with Aker Carbon Capture, which designs and builds facilities for companies in carbon-intensive industries, such as cement, steel, and oil and gas.

- Due to growing investor demand to reduce greenhouse gas emissions, more digital companies are releasing software that oil and gas producers may use to assess their carbon emissions. In July 2024, California Resources Corporation introduced the completion of the all-stock combination with Aera Energy LLC (Aera). This transformational deal creates significant scale and asset durability to meet California's growing energy needs and expands its leading carbon management platform to help the state meet its ambitious climate goals.

North America Accounts for Largest Market Share

- The launch of several Carbon Management Programmes in North America represents a significant step toward making Airport Carbon Accreditation the global standard for airport carbon management. At the initiative's launch ceremony, Seattle-Tacoma International Airport received certification for the first time in North America.

- Several government initiatives regarding net-zero emissions are anticipated to fuel demand in the market. In response to the government's goal of net-zero emissions by 2050, the Department of Energy (DOE) in the United States launched the Carbon Negative Shot, an all-hands-on-deck call for innovation in CO2 removal pathways that will capture carbon dioxide from the atmosphere and store it at gigaton scales for less than USD 100/net tonne of carbon dioxide-equivalent.

- Market demand is also increasing due to government measures to reduce energy emissions from several outdated public buildings. For instance, thanks to a contract signed by the US General Services Administration with IBM Corporation, the 50 most energy-intensive buildings owned by the state and federal governments will have efficient and smart building technology installed.

- According to the Energy Information Administration (EIA), US energy-related CO2 emissions decreased slightly in 2023 compared to 2022. Although emissions decreased across many economic industries, more than 80% of US energy-related CO2 emissions reductions in 2023 occurred in the electric power industry. These reductions were caused largely by reduced coal-fired electricity generation, as natural gas and solar power made up a larger portion of the generation mix. Therefore, the government's focus on reducing carbon emissions generated by the energy industry is likely to support the market demand positively in the coming years.

Carbon Management System Industry Overview

The carbon management system market is fragmented, as many players are offering software for management and monitoring. This surge in numbers is being caused by greater uptake of cloud services. Businesses that offer consultation services are expected to grow steadily and exhibit a similar pattern during the forecast period.

- June 2024 - Workiva, a global provider of assured integrated reporting solutions, expanded its tech portfolio with the launch of Workiva Carbon. This new addition enhances its Environmental, Social, and Governance (ESG) and Sustainability platforms, enabling businesses to adhere to stringent global climate regulations effectively.

- March 2024 - SLB announced an agreement to combine its carbon capture business with Aker Carbon Capture (ACC) to support accelerated industrial decarbonization at scale. The agreement may bring together complementary technology portfolios, leading process design expertise, and an established project delivery platform. The combination will utilize ACC's commercial carbon capture product offering and SLB's new technology developments and industrialization capability.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products and Services

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Environmental Concerns and Focus on Reducing Carbon Footprints

- 5.2 Market Challenges

- 5.2.1 Managing Variable Energy and Resource Demand

6 MARKET SEGMENTATION

- 6.1 By Offering

- 6.1.1 Software

- 6.1.2 Services

- 6.2 By Application

- 6.2.1 Energy

- 6.2.2 Greenhouse Gas Management

- 6.2.3 Air Quality Management

- 6.2.4 Sustainability

- 6.2.5 Other Applications

- 6.3 By End-user Verticals

- 6.3.1 Oil and Gas

- 6.3.2 Manufacturing

- 6.3.3 Healthcare

- 6.3.4 IT and Telecom

- 6.3.5 Other End-user Verticals

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Simble Solutions Ltd

- 7.1.2 IBM Corporation

- 7.1.3 ENGIE Impact

- 7.1.4 GreenStep Solutions Inc.

- 7.1.5 SAP SE

- 7.1.6 Enablon SA

- 7.1.7 IsoMetrix

- 7.1.8 Schneider Electric SE

- 7.1.9 Salesforce.com Inc.

- 7.1.10 Greenstone+ Ltd

- 7.1.11 Microsoft Corporation

- 7.1.12 Sphera