|

市場調査レポート

商品コード

1644466

アジア太平洋地域のエンタープライズコラボレーション:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Asia Pacific Enterprise Collaboration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域のエンタープライズコラボレーション:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

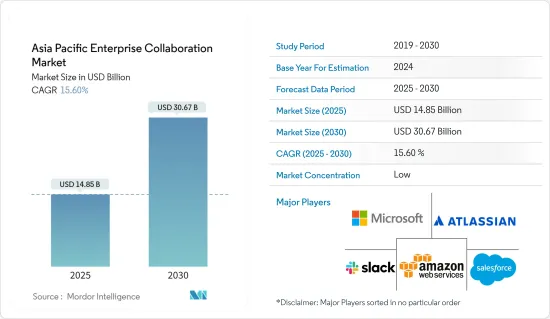

アジア太平洋地域のエンタープライズコラボレーション市場規模は、2025年に148億5,000万米ドルと推計され、予測期間(2025-2030年)のCAGRは15.6%で、2030年には306億7,000万米ドルに達すると予測されます。

同市場の成長は、エンタープライズコラボレーションソリューションが最大の生産性、ビジネスの俊敏性、柔軟性を提供することに起因しています。

主なハイライト

- エンタープライズコラボレーションは、プロセスを合理化しコラボレーションを促進するテクノロジーへのアクセスを提供することで、従業員が職場内外で交流しコミュニケーションすることを可能にします。多くの従業員がリモートで働き、また他の従業員が従来のオフィスで働くなど、従業員の分散化が進むにつれて、企業は市場をリードするソリューションを採用するようになると予想されます。

- エンタープライズコラボレーション・ツールを利用することで、スタッフは簡単にプロジェクトを把握・管理し、個人の責任を促し、より強い信頼の絆を築くことができます。このプラットフォームは、組織内のすべてのコミュニケーションとチームワークに必要な情報を一元化する場所を提供します。重複する機能を持つ冗長なアプリケーションを排除することで、効率を高める。

- パンデミック(世界的大流行)の影響により、企業が商業スペースの新規取得の決定を少なくとも4分の1から2分の1遅らせたため、オフィス需要は減少する可能性が高いです。その結果、多くの企業が事業継続のためにWFHを選択し続けると思われます。その結果、より安全な企業間コラボレーションを提供するソリューションへの需要が大幅に高まっています。例えば、WFHの攻勢により、IGELは最近、VMware、シトリックス・システムズ、マイクロソフト、アマゾンに接続されたLinux OSに数万席を提供し、売上を伸ばしています。また、アジアではUDポケットの需要がかつてないほど高まっています。

- さらに、エンタープライズコラボレーション市場の収益増加は、モバイル・デバイスの利用拡大によるところが大きく、ネットワーキング・サイトも市場拡大に貢献すると予想されます。市場を後押ししている主な要因は、内部と外部のコラボレーションを単一のスペースで実現する必要性と、さまざまな地域にまたがる複数の利害関係者間のコミュニケーションとコラボレーションの促進を重視する組織の増加です。

- さらに、インドではBFSIセクターが急速に拡大しているため、この地域のエンタープライズコラボレーション市場はより急速に成長すると思われます。例えば、インドのNiti Aayogは、インドの財務大臣が2021-2022年の予算で保険部門のFDI上限を49%から74%に引き上げたと報告しています。その結果、BFSIセクターは今後数年間で大きな成長を遂げることが予想されます。

- 企業コラボレーションのためのテクノロジーは、顧客、パートナー、利害関係者、ベンダーからリアルタイムのフィードバックを得るのに理想的であり、より効果的な対応と創造性の向上を可能にします。テクノロジーの急速な開拓、新興国ウェブサイトの台頭、コラボレーション用モバイルデバイスの利用も、市場拡大にプラスの影響を与えそうな要因です。

- 各社はコグニティブ・コラボレーションにも注力しています。コグニティブ・コラボレーションとは、コグニティブ学習と情報共有をあらゆる分野のインタラクションに導入することで、人工知能をビジネス知識やワークフローに応用することです。コグニティブを活用した顧客対応技術には、自然言語処理、予測分析、インテリジェント・ルーティングなどがあります。

- 予測期間を通じて、企業間コラボレーション市場の成長は、ネットワーキングウェブサイトの利用の増加によって影響を受けると予想されます。さらに、エンタープライズコラボレーションを拡大する主な障壁は、その高い導入コストと、法的リスクや発見リスクの回避の難しさであると予想されます。

- COVID-19パンデミックウイルスの世界の流行は、パンデミックと戦うためにアジアのいくつかの国で採用されたロックダウンと社会的距離の戦略により、従業員の在宅勤務(WFH)の需要を増大させると予想されました。COVID-19の大流行中、企業向けコラボレーション・ソリューションの需要が大幅に増加しました。様々な組織の従業員間のコミュニケーションの必要性により、エンタープライズコラボレーションソリューションが増加しました。

APACエンタープライズコラボレーション市場動向

クラウドベースの導入が市場を牽引

- エンタープライズコラボレーションソリューションは、ビジネスコミュニケーションとコラボレーションの基盤となるコンポーネントへと進化しました。クラウドの拡大により、オンプレミス機器の管理要件がなくなり、オフィスコラボレーションツールへのアクセシビリティが向上しました。遠隔地での雇用機会の開発が、クラウドコラボレーションの普及を後押ししています。クラウドを利用することで、地理的に分散した従業員が同僚とリアルタイムでコラボレーションできるようになります。

- Yottaによると、2020年に実施された調査では、インド企業の約37%がデジタルインフラをクラウドに収容していることが明らかになった。2022年までには、インフラの60%以上がクラウド化され、キャプティブ・アベイラビリティやサードパーティのコロケーションの必要性がなくなると予測されています。

- クラウドベースのサービスは、組織がリスクを回避するための有効な選択肢となっています。クラウドベースのEFSSソリューションのおかげで、システムのITインフラは更新や改善のための資本をそれほど必要としなくなった。電子技術やIT技術の急速な更新により、リターンを生む前に投資が時代遅れになるリスクがあります。

- 生成されるデータの着実な増加は、クラウドベースのワークロード展開の主要な原動力になると予想されます。さまざまな業界が大量のデータを扱っています。データセンターは、さまざまなアプリケーションや企業間のコラボレーションを伴う複雑なワークロードを実行する必要がある企業に適しています。

- さらに、多くの国では、特定の地域や国の境界内に留まらなければならない特定の種類のデータを指定する法律や政策があります。中国、オーストラリア、香港、シンガポールでは、政府文書や医療記録などの情報に関してデータ居住法が制定されています。さらに、会計、金融、法律、モーゲージブローカー、銀行など多くの専門家団体は、クラウドサービスプロバイダーがどのように情報を使用し、特定の地域の管轄区域内に保管するかを管理するために、データレジデンシー要件をカバーする会員向けの専門基準を設けています。

- 各事業者はまた、コグニティブ・コラボレーションを重視しており、コグニティブ学習をビジネス知識やワークフローに統合し、人工知能を応用しています。例えば、2021年10月、IBMはテクノロジー・ビジネス管理のためのSaaSアプリケーションのマーケットリーダーであるApptioと提携しました。この提携後、両社はレッドハットOpenShiftとIBMのオープン・ハイブリッド・クラウド・アプローチの採用を促進し、ハイブリッド・クラウド技術の意思決定を強化する上で顧客を支援することになります。

- 生成されるデータ量の一貫した増加は、クラウドベースのワークロード展開の主要な推進力になると予想されます。数多くの業界が膨大な量のデータを扱っています。データセンターは、企業コラボレーションのために複数のアプリケーションや複雑なワークロードを実行する企業に適しています。高い生産性を可能にし、すべてのアプリケーション・ツールがリアルタイムのデータにアクセスできます。

- さらに、グーグルは2022年3月にインドの多国籍コングロマリット、マヒンドラ・グループと提携しました。この提携は、同グループのさまざまな事業部門にイノベーションを促すものだった。さらに、RISE with SAPプログラムの一環として、Mahindraはデータレイクとデータウェアハウスとともに、ミッションクリティカルなアプリケーションをオンプレミスのデータセンターからGoogle Cloudに移行する予定だった。

小売・消費財が大きな市場シェアを占める見込み

- 消費財の需要拡大、eコマースの拡大、デジタルトランスフォーメーションはすべて、小売業が大きく成長する要因となっています。この結果、ビッグデータ・ソリューションが業界のデータ生成に利用されています。物理的な小売店やオンラインストアの従業員は、ユーザーからドキュメントやアプリを通じて移動するコンテンツを単一のコラボレーション・プラットフォームでデバイスに接続することで、より迅速な意思決定を行うことができます。

- HCL Techのデータによると、小売業者や雇用者の半数以上が、さまざまな部門や地理的な場所にいる個人と頻繁にコラボレーションする必要があります。リテールエンタープライズコラボレーションソリューションを使用するビジネス上の利点には、ユーザーエクスペリエンスの向上、意思決定プロセスの迅速化、コミュニケーションの質の向上などがあります。さらに、ブランドの完全性が促進され、売上と利益が増加します。

- 小売、消費者、ロジスティクスの各分野における情報伝達の迅速化は、タイムリーな在庫補充を可能にし、ビジネスに多大な貢献をもたらします。電子データ交換は、サプライチェーンのさまざまなメンバーが、調達、販売、購入に関する情報をリアルタイムで交換するのに役立ちます。

- 小売業におけるファイル共有のためのエンタープライズコラボレーションは、すべての従業員に情報へのアクセスとともに、データとコンテンツの管理、セキュリティ、同期を提供します。これにより、いつでもどこでも顧客の質問に答え、カートを満杯にする継続的なサービスが保証されます。

- 小売コンピュータ・ビジョン・ソリューションとアナリティクスの世界的プロバイダーであるトラックス社の店舗監視とインテリジェンス・ソリューションであるリテール・ウォッチは、中国で正式に発売されました。トラックスは最近、上海で開催された第22回中国小売見本市(ChinaShop)で、中国市場向けの全く新しい棚監視ロボットソリューションと協働プラットフォームをデビューさせました。

- ソーシャルメディア・プラットフォームの中には、オンライン・マーケットプレースとして機能するものもあり、ユーザーはプラットフォームを離れることなく購入することができます。M-コマースはこの地域全体で人気が高まっており、インドネシア、タイ、フィリピンの消費者がM-コマースの導入で最も高いレベルを示しています。このような開発と世界のインターネットユーザー数の増加の結果、チームでのオンラインコミュニケーションを可能にするオンラインコラボレーションツールと呼ばれるソフトウェアへの需要が高まるでしょう。

アジア太平洋地域のエンタープライズコラボレーション産業の概要

アジア太平洋地域のエンタープライズコラボレーション市場は、国内外の市場で複数のベンダーが活動しているため、競争が激しいです。市場は断片化されているように見えます。主要企業は、地理的範囲を拡大し、競争力を維持するために、合併、買収、拡張を採用しています。市場の主要企業には、Microsoft Corporation、Amazon Web Services、Salesforce.Com Inc.などがいます。市場の最近の動向としては、以下のようなものがある:

- 2024年1月- キャップジェミニは、あらゆる規模の組織におけるジェネレーティブAIソリューションとテクノロジーの採用を加速することを目的とした、AWSとの複数年にわたる戦略的協業契約の締結を発表しました。この協業を通じて、キャップジェミニとAWSは、コスト、規模、信頼などの課題を克服しながら、顧客がジェネレーティブAIの導入によるビジネス価値を実現できるよう支援することに注力しています。また、キャップジェミニの既存のAWSセンター・オブ・エクセレンス(CoE)ネットワークを活用することで、共同顧客の投資を個々のパイロットや概念実証から本番規模に移行できるようにします。

- 2023年11月- デジタル、クラウド、ビッグデータ、セキュリティの分野で業界をリードするAtosグループのEvidenは、AWSとの新たな戦略的協業契約(SCA)を発表しました。このSCAは、顧客がクラウドとAIの変革プロジェクトに不可欠な専門知識に迅速にアクセスし、価値実現までの時間を短縮できるよう、EvidenとAWSが共同でソリューション、コンサルティング、イノベーションサポートの多面的なプログラムを提供することを約束するものです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- エンタープライズコラボレーションツールの進化

- 業界の魅力度-ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

第5章 市場力学

- 市場促進要因

- 効率化のためのAPI統合

- 企業全体におけるモバイルデバイス利用の増加

- リモートワークなど

- 市場の課題

- データコラボレーションにおけるセキュリティ懸念など

- 世界とアジア太平洋のエンタープライズコラボレーション市場の比較

- COVID-19の業界への影響評価

第6章 市場セグメンテーション

- 展開タイプ別

- オンプレミス

- クラウドベース

- 企業規模別

- 中小企業

- 大企業

- エンドユーザー業界別

- IT・通信

- BFSI

- ヘルスケア

- 小売・消費財

- その他業界別(教育、運輸・物流、製造、官公庁)

- 国別

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域(東南アジア、A&Z)

第7章 競合情勢

- 企業プロファイル

- Microsoft Corporation

- Amazon Web Services

- Atlassian Corporation PLC

- Slack Technologies Inc.

- Salesforce.Com Inc.

- Google(Workspace)

- Cisco System Inc.

- Zoho Corporation Pvt Ltd.

- Jive Software Inc.

- Asana

第8章 投資分析

第9章 市場機会と今後の動向

The Asia Pacific Enterprise Collaboration Market size is estimated at USD 14.85 billion in 2025, and is expected to reach USD 30.67 billion by 2030, at a CAGR of 15.6% during the forecast period (2025-2030).

The growth of the market is attributed to the enterprise collaboration solutions' provision of maximum productivity, business agility, and flexibility.

Key Highlights

- Enterprise collaboration enables employees to interact and communicate within and outside their work environment by providing access to technology that can streamline processes and encourage collaboration. Organizations are anticipated to adopt market-leading solutions as the workforce becomes more distributed, with many workers working remotely and others from conventional offices.

- With enterprise collaboration tools, staff members can easily keep track of and manage projects, encourage individual responsibility, and build stronger bonds of trust, all of which contribute to greater transparency within the workplace. The platform provides a centralized location for all communication and teamwork requirements within the organization. It boosts efficiency by eliminating redundant applications with overlapping features.

- The office demand was likely to decline during the pandemic due to corporates delaying their decisions on new offtake of commercial spaces by at least a quarter or two. As a result, significant corporates will continue to choose WFH for their business continuity. The demand for solutions that offer safer enterprise collaboration has greatly increased as a result. For instance, Due to the WFH assault, IGEL has recently experienced increased sales, providing tens of thousands of seats for its Linux OS connected to VMware, Citrix Systems, Microsoft, and Amazon. In addition, IGEL has also experienced unprecedented demand for its UD Pocket offering in Asia.

- Additionally, the rise in market revenue for enterprise collaboration is largely due to the growing use of mobile devices, and networking websites are also expected to contribute to market expansion. The main factors propelling the market are the need to combine internal and external collaboration in a single space and organizations' increased focus on fostering communication and collaboration among multiple stakeholders across different geographies.

- Furthermore, the enterprise collaboration market in this region will grow much faster because of India's rapidly expanding BFSI sector. For instance, the Niti Aayog of India reported that the Indian Finance Minister increased the FDI cap for the insurance sector in the 2021-2022 budget from 49% to 74%. As a result, the BFSI sector is anticipated to experience significant growth over the coming years.

- Technologies for enterprise collaboration are ideal for getting real-time feedback from customers, partners, stakeholders, and vendors, enabling more effective responses and improved creativity. The rapid development of technology, the rise in networking websites, and the use of mobile devices for collaboration are additional factors likely to positively affect the market's expansion.

- The companies are also focusing on cognitive collaboration, which is applying artificial intelligence to business knowledge and workflows by bringing cognitive learning and information sharing to all areas of interactions. Cognitive-powered customer interaction technologies include Natural Language Processing, Predictive Analysis, and intelligent routing.

- Throughout the forecast period, the growth of the enterprise collaboration market is anticipated to be impacted by the increase in the use of networking websites. Moreover, the main barriers to expanding enterprise collaboration are expected to be its high implementation costs and difficulty avoiding legal and discovery risks.

- The outbreak of the COVID-19 pandemic virus worldwide was anticipated to augment the demand for employees' work from home (WFH), owing to the lockdown and social distancing strategy adopted across several counties of Asia to fight the pandemic. During the COVID-19 pandemic, the demand for enterprise collaboration solutions significantly increased. Due to the need for communication among employees in various organizations, enterprise collaboration solutions increased.

APAC Enterprise Collaboration Market Trends

Increasing Adoption of Cloud-based Deployment Drive the Market

- Enterprise collaboration solutions have evolved into foundational business communications and collaboration components. The expansion of the cloud has improved accessibility to office collaboration tools by removing the management requirements of on-premises equipment. The development of remote employment opportunities has boosted the popularity of cloud collaboration. The cloud allows geographically dispersed employees to collaborate with coworkers in real-time.

- Yotta claims that a survey carried out in 2020 revealed that about 37% of Indian businesses had their digital infrastructure housed in the cloud. By 2022, it was predicted that more than 60% of the infrastructure would be in the cloud, negating the need for captive availability and third-party co-location.

- Cloud-based services have become a viable option for assisting an organization to navigate risks. Because of cloud-based EFSS solutions, the system's IT infrastructure no longer requires as much capital to be updated and improved. The investment risks becoming outdated before it generates a return due to the rapid updating of electronic and IT technology.

- The steady increase in data generated is anticipated to serve as the primary driver of cloud-based workload deployment. Many different industry verticals deal with a massive amount of data. A data center is better suited for a company that needs to run various applications and complex workloads involving enterprise collaboration.

- In addition, many nations have laws or policies that specify certain types of data that must stay within the boundaries of a particular area or country. Data residency laws have been established in China, Australia, Hong Kong, and Singapore for information such as government documents and medical records. Furthermore, many professional associations, including those in accounting, finance, law, mortgage brokers, and banking, have professional standards for their members that cover data residency requirements to control how cloud service providers use the information and keep it within specific territorial jurisdictions.

- The businesses also emphasize cognitive collaboration, integrating cognitive learning into business knowledge and workflows to apply artificial intelligence. For instance, in October 2021, IBM partnered with Apptio, a market leader in SaaS applications for technology business management. After forming this partnership, the businesses would aid clients in promoting the adoption of Red Hat OpenShift and IBM's open hybrid cloud approach and enhancing hybrid cloud technology decision-making.

- The consistent growth in the amount of data generated is anticipated to be the primary driver of cloud-based workload deployment. Numerous industry verticals work with enormous amounts of data. A data center is better suited for a company that runs multiple applications and complex workloads for enterprise collaboration. It makes high productivity possible, and all application tools have access to real-time data.

- Additionally, Google partnered with the Indian multinational conglomerate Mahindra Group in March 2022. This partnership encouraged the group's various business units to innovate. Further, as part of the RISE with SAP program, Mahindra was expected to move its mission-critical applications from its on-premises data centers to Google Cloud, along with its data lake and data warehouse.

Retail and Consumer Goods is Expected to Account For Significant Market Share

- The growing demand for consumer goods, the volume of e-commerce, and digital transformation all contribute to the retail sector's significant growth. Big Data solutions have been used to generate data in the industry as a result of this. The physical retail or online store employees can make decisions more quickly by connecting the content moving from users, through documents or apps, to devices with a single collaboration platform.

- More than half of retailers and employers frequently need to collaborate with individuals from various departments and geographical locations, according to data from HCL Tech. The business advantages of using a Retail Enterprise Collaboration solution include improved user experience, faster decision-making processes, and improved communication quality. Additionally, brand integrity is promoted while sales and profits are increased.

- The faster transfer of information in the retail, consumer, and logistics sectors can help businesses enormously by timely replenishing the stock. Electronic data exchange can help different members of the supply chain exchange information in real-time for any procurement, sales, and purchases, thus cutting on the need for inventory stocking for a more extended period.

- Enterprise collaboration for File Sharing in retail provides data and content control, security, and synchronization, along with access to the information to all its employees. This ensures a continuous service to customers anywhere and anytime to answer their questions and fill carts.

- Retail Watch, a store monitoring and intelligence solution from Trax, a global provider of retail computer vision solutions and analytics, has officially launched in China. Trax recently debuted at the 22nd China Retail Trade Fair (ChinaShop) in Shanghai with its brand-new shelf monitoring robotic solutions and collaboration platform for the China market, developed in collaboration with the regional robotics business Ecovacs.

- Some social media platforms also function as an online marketplace, allowing users to purchase without leaving the platform. M-commerce has grown in popularity throughout the region, with Indonesian, Thai, and Filipino consumers showing the highest levels of m-commerce adoption. As a result of these developments and the growing number of internet users globally, there will be an increased demand for Software called online collaboration tools that enables teams to communicate online.

APAC Enterprise Collaboration Industry Overview

The Asia-Pacific Enterprise Collaboration Market is highly competitive due to multiple vendors operating in the domestic and international markets. The market appears to be fragmented. The significant players adopt mergers, acquisitions, and expansions to expand their geographic reach and stay competitive. Some major players in the market are Microsoft Corporation, Amazon Web Services, and Salesforce.Com Inc., among others. Some of the recent developments in the market are:

- January 2024 - Capgemini announced the signing of a multi-year strategic collaboration agreement with AWS, designed to accelerate the adoption of generative AI solutions and technologies amongst organizations of all sizes. Through this collaboration, Capgemini and AWS are focused on helping clients realize the business value of adopting generative AI while navigating challenges, including cost, scale, and trust. It will enable joint clients to move their investments from individual pilots and proof of concepts to scale production by leveraging Capgemini's existing network of AWS Centers of Excellence (CoEs).

- November 2023 - Eviden, the Atos Group business leading in digital, cloud, big data and security, announced a new Strategic Collaboration Agreement (SCA) with AWS. The SCA is a joint commitment for Eviden and AWS to deliver a multi-faceted program of solutions, consultancy, and innovation support to help customers quickly access critical expertise for cloud and AI transformation projects and increase their time to value.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Evolution of Enterprise Collaboration Tools

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Buyers/Consumers

- 4.3.2 Bargaining Power of Suppliers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 API Integration for Greater Efficiency

- 5.1.2 Increase in Usage of Mobile Devices across Enterprises

- 5.1.3 Remote Working Conditions etc.

- 5.2 Market Challenges

- 5.2.1 Security Concerns in Data Collaboration etc.

- 5.2.2 Comparison of Global and Asia-Pacific Enterprise Collaboration market

- 5.2.3 Assessment of COVID-19 Impact on the industry

6 MARKET SEGMENTATION

- 6.1 By Deployment Type

- 6.1.1 On-premise

- 6.1.2 Cloud-based

- 6.2 By Size of Enterprise

- 6.2.1 Small and Medium Enterprises

- 6.2.2 Large Enterprises

- 6.3 By End-user Industry

- 6.3.1 Telecommunications and IT

- 6.3.2 BFSI

- 6.3.3 Healthcare

- 6.3.4 Retail and Consumer Goods

- 6.3.5 Other End-user Industry Verticals (Education, Transportation and Logistics, Manufacturing, Government)

- 6.4 By Country

- 6.4.1 China

- 6.4.2 Japan

- 6.4.3 India

- 6.4.4 South Korea

- 6.4.5 Rest of Asia-Pacific (Southeast Asia, A&Z)

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Microsoft Corporation

- 7.1.2 Amazon Web Services

- 7.1.3 Atlassian Corporation PLC

- 7.1.4 Slack Technologies Inc.

- 7.1.5 Salesforce.Com Inc.

- 7.1.6 Google (Workspace)

- 7.1.7 Cisco System Inc.

- 7.1.8 Zoho Corporation Pvt Ltd.

- 7.1.9 Jive Software Inc.

- 7.1.10 Asana