テレコムオペレーションマネジメント-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Telecom Operations Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1644390

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

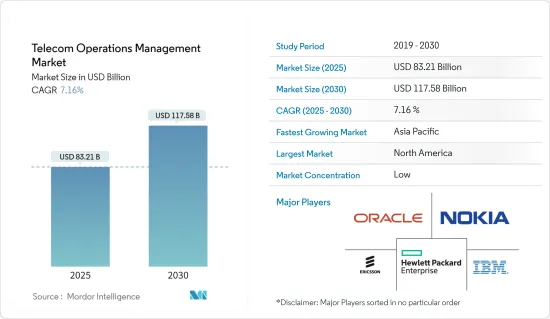

テレコムオペレーションマネジメント市場規模は、2025年に832億1,000万米ドルと推定され、2030年には1,175億8,000万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは7.16%です。

COVID-19の発生により、通信会社は、何百万人もの従業員や学生が自宅待機となり、ネットワーク上の帯域幅需要が30%から40%増加することに対応するための業務に十分に対応できるようになるはずです。FieceTelecomによると、コロナウィルスの大流行は、あらゆる規模の企業にデジタルトランスフォーメーション計画の加速を促しています。すでにデジタルトランスフォーメーションとクラウド戦略の導入に取り組んでいた企業は、パンデミックの最初の数週間をうまく乗り切ることができました。Verizonビジネスの調査結果では、回答者の43%がデジタルと関連技術による事業拡大を計画しているなど、いくつかのポイントが指摘されています。また、30%はすでにデジタルで製品やサービスを提供する新しい方法を追加しています。

主要ハイライト

- 通信産業はデジタルトランスフォーメーションの重要な促進要因のひとつであり、世界のデジタライゼーションの牽引役であると同時に、市場環境の大きな変化を目の当たりにしている産業でもあります。

- 通信産業による相互運用性と技術への投資は、世界経済を通じた資本フローと情報のパラダイムシフトを強化し、同時に、産業を超えたまったく新しいビジネスモデルの出現のためのビルディングブロックを提供しています。帯域幅に対する需要が急増し、モバイルインターネットユーザーが増加する中、通信サービスプロバイダーは先進的で革新的なソリューションを提供するために進化しています。

- また、レガシーネットワークは、5Gネットワークのインフラ要件の増大と相まって、複雑な環境を生み出し、通信サービスプロバイダー(CSP)を困難なものにしています。それゆえ、通信における技術的に先進的運用支援システムの採用ニーズが高まっている

- 低コストのデータと音声サービスへのニーズが継続的に高まっていることが、市場の成長を後押ししています。このため、MNOからネットワークサービスを卸売価格で購入し、MNOのサービスよりも低料金でバンドルサービスとして販売するサービスプロバイダーが台頭しています。

- ほとんどの企業組織がマルチベンダー、マルチクラウド構成を採用しているため、ネットワークアーキテクチャが複雑化していることも、調査対象市場の拡大に寄与しています。さらに、これらの企業は限られたリソースで需要を満たし、変更プロセスを合理化することを目指しているため、より柔軟で適応性の高いネットワークアーキテクチャを必要としています。

- さらに、クラウド、M2M(Machine to Machine)トランザクション、モバイルマネーといったサービスの増加は、予測期間中に通信運用管理の需要をさらに高めると予想されます。

- さらに、企業がモバイル化を進め、従業員の交流や使いやすさを向上させるためにBYODのような新しいコンセプトを採用する中、高速で高品質なネットワークの提供が不可欠となっています。企業はBYODの積極的な導入に前向きで、予測期間中の市場成長を促進しています。

通信運用管理市場の動向

クラウドが大きく成長する見込み

- 世界中の通信事業者は、新しいサービス、収益機会、体験を促進するために、クラウドを中心とした変革の旅に乗り出しています。通信事業者は、自社のクラウドネイティブでオープンでモジュール化されたソリューションを、完全に管理された高パフォーマンスのクラウドプラットフォームと組み合わせることで、その旅を加速させることができます。クラウドプロバイダーは、通信事業者をサポートするために、いくつかの戦略的地域に注力しています。これには、通信会社がビジネスサービスプラットフォームとして5Gを収益化するのを支援すること、データ主導のエクスペリエンスを通じて顧客とのエンゲージメントを強化すること、コア通信システム全体の運用効率を改善するのを支援することなどが含まれます。

- デル Technologiesは2021年10月、通信サービスプロバイダー(CSP)がオープンでクラウドネイティブなネットワーク展開を加速し、新たな収益機会を創出できるよう支援する新しい通信ソフトウェア、ソリューション、サービスを発表しました。オープンRAN(ORAN)のような新技術により、CSPは将来の成長を支えるネットワークインフラを展開するための幅広い選択肢を得ることができます。

- GoogleはAmdocsとの提携を発表し、通信サービスプロバイダーがアムドックスの市場をリードするポートフォリオをGoogleクラウド上で実行できるようにし、新しいデータ分析、サイト信頼性エンジニアリング、5Gエッジソリューションを企業顧客に提供できるようにします。アムドックスは、アムドックスとGoogleクラウドの共同Go-to-marketイニシアチブの一環として、Altice USAがGoogleクラウド上でアムドックスのデータとインテリジェンスシステムを稼動させたと発表しました。また、Netcrackerとの新たなパートナーシップにより、同社のデジタルBSS/OSSとオーケストレーション・スタック全体がGoogle Cloud上に展開されました。サービスプロバイダは、ミッションクリティカルなIT用途をオンデマンドで拡大・購入し、無制限にGoogle Cloudリソースにアクセスし、所有コストを削減し、新しいサービスの可用性を加速できるようになりました。

- 2021年6月、AT&TはMicrosoftと提携し、5GモバイルコアネットワークをMicrosoft Azureのハイブリッドクラウドに移行しました。Microsoftは、AT&Tの5Gコアを動かすAT&TのNetwork Cloudプラットフォーム技術を買収します。また、コンテナ化または仮想化されたネットワークサービスを実行するAT&Tのエンジニアリングとライフサイクル管理ソフトウェアも買収します。

- さらに、ZENIC ONE(UME)システムは、人工知能とビッグデータを初めて統合し、ツールとアプリケーションによる管理と制御を追加しました。そのため、デバイスから報告された操作に関連する情報をリアルタイムで収集し、AIのインテリジェントなビッグデータ分析を組み合わせることで、ネットワークの操作状況をモニタリングし、問題を迅速に特定し、サービスを回復することができるため、O&M効率を大幅に向上させることができます。このような事例は、市場成長の強力な原動力になると予想されます。

- Ericssonによると、世界のスマートフォン契約数は2021年に60億件を突破し、今後数年間でさらに数億件増加すると予想されています。このようなユーザー数の増加が、予測期間中の市場成長の原動力となると考えられます。さらに、デジタルインディア構想などの取り組みにより、通信事業におけるクラウドプラットフォームの統合やクラウドベースのモデルが活発化し、市場成長の原動力となることが期待されます。

北米が大きなシェアを占める見込み

- 北米は、事業運営ソリューションへの支出が多いことから、通信事業運営管理市場で大きなシェアを占めると予測されています。また、同地域の通信は高度に発展しており、通信事業者間の競合も激しいことから、同地域の通信分析市場はさらに活性化すると予想されます。顧客サポートに使用されるITインフラや技術の継続的な進歩、市場ベンダーの数の多さ、日常業務やヘルプデスクソフトウェアを管理するための熟練した技術的専門知識へのアクセスのしやすさが、通信業務管理市場の成長地域に貢献しています。

- 同市場には複数の新規参入企業が現れ、市場成長をさらに後押ししています。例えば、2022年7月、Adani Groupはセルラー通信セグメントへの参入を確認し、2022年に展開する予定です。同社は、計画中の市場進出の一環として、オーストラリアで新たに3つの無線サービスプロバイダーをリリースする予定で、このセグメントに参入する最初のインド企業の1つとなります。同グループはまた、北米市場に10億米ドルを投資することも提案しています。

- さらに、モバイルインターネットやスマートフォンの普及率上昇、低価格化、地域密着型コンテンツの増加など、消費者行動の変化により、eコマース、金融サービス、ビデオ、ソーシャルメディアなどのセグメントでモバイルサービスが活況を呈しています。その結果、北米では電気通信事業管理の需要が増加傾向にあります。

- コネクテッドデバイスやモバイルデバイスの大幅な増加が、ネットワークサービスの強化需要に拍車をかけています。北米は常に技術導入の最前線に位置しているため、この地域ではコネクテッドデバイスの導入が最も進んでいます。

- 例えば、Cisco Systems Inc.によると、北米の1人当たりの平均デバイス数と接続数は2018年に8.2であり、2023年には13.4に達すると予想されています。このような動向は、同地域市場の成長の主要促進要因として作用すると予想されます。

- さらに、IoT、マルチクラウド環境、AIなどの技術的進歩を展開することで、ネットワークアーキテクチャの複雑性が増します。GSMAによると、北米のIoT接続数は2019年の28億に対し、2025年には54億に達すると予想されています。したがって、これらの技術を導入することで、柔軟で適応性の高いネットワークアーキテクチャに対する需要が高まり、同地域の市場成長に拍車をかけています。

テレコムオペレーションマネジメント産業概要

テレコムオペレーションマネジメント市場は競争が激しく、セグメント化されています。これは、IBM Corporation、Oracle Corporation、Telefonaktiebolaget LM Ericsson、Hewlett Packard Enterprise Development LP、Nokia Corporationのような大手企業が存在するためです。大手企業は提携関係を結び、市場シェア拡大のための革新的なソリューションを打ち出しています。

- 2022年2月-Telecom EgyptとGrid Telecomは、ギリシャ・エジプト間の新たな海底ケーブル・オプションに関する戦略的MoUに調印しました。両社は、ギリシャ・エジプト間の接続オプションを検討するとともに、近隣諸国との相互接続を通じて、Telecom EgyptとGrid Telecomのネットワークと国際的なフットプリントの利用を検討します。

- 2021年9月-オマーンのVodafoneはEricssonと、新しい4Gと5Gのコアと無線アクセス(RAN)グリーンフィールドネットワークの展開、運用、保守に関する契約を締結しました。Ericssonは、Ericssonクラウドコア、クラウドVoLTE、NFVIによる完全なコアネットワークソリューションと、エンドツーエンドのトランスポート・ネットワークソリューションを記載しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場予測

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- COVID-19の市場への影響評価

- 産業の使用事例

第5章 市場力学

- 市場促進要因

- 運用コストの増大と複雑化

- 市場課題

- 効率的なシステムインテグレーターの不足

第6章 市場セグメンテーション

- 展開別

- オンプレミス

- クラウド

- タイプ別

- ソフトウェア

- ネットワーク管理

- 顧客・製品管理

- 収益管理

- 在庫管理・その他

- サービス別

- ソフトウェア

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- IBM Corporation

- Telefonaktiebolaget LM Ericsson

- Oracle Corporation

- Hewlett Packard Enterprise Development LP

- Nokia Corporation

- Amdocs Inc.

- Netcracker Technology Corp

- Cisco Systems Inc.

- Accenture PLC

- SAP SE

- NEC Corporation

- Comarch SA

- ZTE Corporation

- ServiceNow Inc.

- TATA Consultancy Services Limited

第8章 投資分析

第9章 市場機会と今後の動向

目次

The Telecom Operations Management Market size is estimated at USD 83.21 billion in 2025, and is expected to reach USD 117.58 billion by 2030, at a CAGR of 7.16% during the forecast period (2025-2030).

With the outbreak of COVID-19, telecom companies should be well equipped to handle the operations for meeting the 30% to 40% increase in bandwidth demand on their networks as millions of employees and students became homebound. According to FieceTelecom, the coronavirus pandemic has pushed companies of all sizes to accelerate their digital transformation plans. The companies that had already engaged in the adoption of digital transformation and cloud strategies were better able to sustain in the first few weeks of the pandemic. Verizon Business' survey results echoed some of the points, including 43% of the respondents now planning to expand their businesses through digital and related technologies. Also, 30% have already added new methods for delivering their products and services digitally.

Key Highlights

- The telecommunications industry is regarded as one of the significant adopters of digital transformation, both as a key driver of worldwide digitization and as an industry witnessing a large-scale change in its market environment.

- Investment by the telecommunications industry in interoperability and technology has reinforced a paradigm shift in capital flows and information through the global economy while providing the building blocks for the emergence of entirely new business models across industries. With the rapidly growing demand for bandwidth and the increasing number of mobile Internet users, communication service providers are evolving to offer advanced and innovative solutions.

- Also, legacy networks, combined with the growing infrastructure requirements for 5G networks, have created a complex environment, making it challenging for communication service providers (CSPs). Hence, the need for the adoption of technologically advanced operations support systems in telecommunications is increasing.

- The continuously growing need for low-cost data and voice services is boosting the market growth. This is encouraging the service providers, who purchase the network services from the MNOs at wholesale rates and sell these as bundled services at lower rates than those of MNOs.

- The market studied is augmented by the increasing complexity in network architectures, as most enterprise organizations have multi-vendor, multi-cloud configurations. Furthermore, as these organizations aim to meet the demand with limited resources and streamline their change processes, they require more flexible and adaptable network architectures.

- In addition, the increasing number of services such as cloud, Machine to Machine (M2M) transactions, and mobile money are further expected to augment demand for telecom operations management over the forecast period.

- Furthermore, with businesses going mobile and adopting new concepts like BYOD to increase employee interaction and ease of use, it has become essential to provide a high speed and quality network. The organizations are looking forward to adopting BYOD aggressively in their operations, thereby fueling the market growth over the forecast period.

Telecom Operations Management Market Trends

Cloud is Expected to Witness Significant Growth

- Telecom companies worldwide are embarking on transformation journeys centered on the cloud to drive new services, revenue opportunities, and experiences. The telecom operators can accelerate the journey by combining their cloud-native, open and modular solutions with the fully managed, high-performing Cloud platform. Cloud providers are focusing on some strategic regions to support telecommunications companies. These include helping telecommunications companies monetize 5G as a business services platform, empowering them to engage their customers through data-driven experiences better, and assisting them in improving operational efficiencies across core telecom systems.

- In Oct 2021, Dell Technologies introduced new telecom software, solutions, and services to help communications service providers (CSPs) accelerate their open, cloud-native network deployments and create new revenue opportunities. New technologies like Open RAN (ORAN) give CSPs a broader set of options for deploying network infrastructure to support future growth.

- Google announced a partnership with Amdocs to enable communications service providers to run Amdocs' market-leading portfolio on Google Cloud and to deliver new data analytics, site reliability engineering, and 5G edge solutions to enterprise customers. Amdocs announced that Altice USA had gone live with Amdocs data and intelligence systems on the Google Cloud as part of the Amdocs and Google Cloud joint go-to-market initiative. Also, a new partnership with Netcracker to deploy its entire Digital BSS/OSS and Orchestration stack on Google Cloud. Service providers can now scale and purchase their mission-critical IT applications on-demand, access unlimited Google Cloud resources, reduce ownership costs, and accelerate new services' availability.

- In June 2021, AT&T partnered with Microsoft to shift its 5G mobile core network to Microsoft Azure's hybrid cloud. Microsoft is acquiring AT&T's Network Cloud platform technology that runs AT&T's 5G core. The deal also involves buying AT&T engineering and lifecycle management software that runs containerized or virtualized network services.

- Moreover, the ZENIC ONE (UME) system integrates Artificial Intelligence and Big Data for the first time to add management and control with tools and applications. Therefore, the system can collect the information related to the operation reported by the device in real-time and combine AI intelligent big data analysis to monitor the network operation status, promptly pinpoint problems and recover services, thus significantly improving the O&M efficiency. Such instances are expected to provide a strong impetus for market growth.

- As per Ericsson, the number of smartphone subscriptions worldwide surpassed six billion in 2021 and is expected to grow further by several hundred million in the next few years. This increase in users will drive market growth over the forecasted period. Additionally, initiatives such as the Digital India initiative are expected to uplift the cloud platform integration or cloud-based model in telecom operation that will drive the market growth.

North America is Expected to Hold Significant Share

- North America is anticipated to occupy a significant share in the telecom operations management market studied, owing to the region's high expenditure on business operation solutions. Besides, telecommunications in the region is highly developed with intense competition among the communication providers, which is expected further to boost the market for telecom analytics in the region. The continuous advancements in IT infrastructure and technology used for customer support, a significant number of market vendors, and the accessibility of proficient technical expertise in managing the daily operations and helpdesk software contribute toward the telecom operations management market growth region.

- The market is witnessing several new players, further driving the market growth. For instance, in July 2022, Adani Group confirmed its entry into the cellular telecom space and will do so with a rollout in 2022. The company is expected to release three new wireless service providers in Australia as part of its planned expansion into the market, making it one of the first Indian firms to enter this area. The group has also proposed to invest USD 1 billion in the North American market.

- Furthermore, the shift in consumer behavior, along with rising mobile internet adoption and smartphone, improved affordability, and the increasing availability of locally relevant content, has led to a boom in mobile services across areas such as e-commerce, financial services, video, and social media. As a result, the demand for telecom operations management has been witnessing an upward trend in North America.

- Substantial growth in connected and mobile devices is spurring the demand for enhanced network services. Since North America has always remained at the forefront of technology adoption, the region witnessed the maximum adoption of connected devices.

- For instance, according to Cisco Systems, the average number of devices and connections per capita in North America stood at 8.2 in 2018 and is expected to reach 13.4 by 2023, which is the highest amongst any other region globally. Such trends are expected to act as major drivers for growth in the regional market.

- Further, deploying technological advancements, such as IoT, multi-cloud environments, or AI, increases network architectures' complexity. According to the GSMA, the number of IoT connections in North America is expected to reach 5.4 billion in 2025, compared to 2.8 billion in 2019. Hence, deploying these technologies is increasing the demand for flexible and adaptable network architectures, thereby fueling the market growth in the region.

Telecom Operations Management Industry Overview

The Telecom Operations Management Market is highly competitive and fragmented. This is due to the presence of significant players such as IBM Corporation, Oracle Corporation, Telefonaktiebolaget LM Ericsson, Hewlett Packard Enterprise Development LP, Nokia Corporation, etc. The prominent companies are entering into collaborations and are launching innovative solutions to increase their market share.

- February 2022 - Telecom Egypt and Grid Telecom have signed a strategic MoU for new subsea cable options between Greece and Egypt. The two companies will explore connectivity options between Greece and Egypt, as well as the use of Telecom Egypt's and Grid Telecom's networks and international footprint through interconnectivity to neighboring countries.

- September 2021 - Vodafone in Oman has signed an agreement with Ericsson to deploy, operate and maintain a new 4G and 5G core and radio access (RAN) greenfield network. Ericsson will supply a complete core network solution based on Ericsson Cloud Core, Cloud VoLTE, and NFVI, as well as an end-to-end transport network solution.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Denition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

- 4.3 Assessment of Impact of COVID-19 on the Market

- 4.4 Industry Use Cases

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Operational Costs and Complexity

- 5.2 Market Challenges

- 5.2.1 Shortage of Efficient System Integrators

6 MARKET SEGMENTATION

- 6.1 By Deployment

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.2 By Type

- 6.2.1 Software

- 6.2.1.1 Network Management

- 6.2.1.2 Customer and Product Management

- 6.2.1.3 Revenue Management

- 6.2.1.4 Inventory Management and Others

- 6.2.2 Services

- 6.2.1 Software

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Telefonaktiebolaget LM Ericsson

- 7.1.3 Oracle Corporation

- 7.1.4 Hewlett Packard Enterprise Development LP

- 7.1.5 Nokia Corporation

- 7.1.6 Amdocs Inc.

- 7.1.7 Netcracker Technology Corp

- 7.1.8 Cisco Systems Inc.

- 7.1.9 Accenture PLC

- 7.1.10 SAP SE

- 7.1.11 NEC Corporation

- 7.1.12 Comarch SA

- 7.1.13 ZTE Corporation

- 7.1.14 ServiceNow Inc.

- 7.1.15 TATA Consultancy Services Limited

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日