|

市場調査レポート

商品コード

1642063

英国のパッケージング:市場シェア分析、産業動向と統計、成長予測(2025~2030年)United Kingdom Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国のパッケージング:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

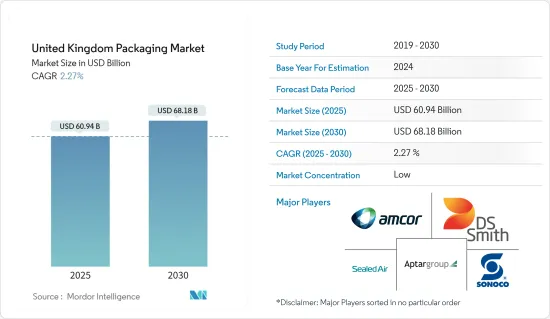

英国のパッケージング市場規模は2025年に609億4,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは2.27%で、2030年には681億8,000万米ドルに達すると予測されます。

主なハイライト

- 英国のパッケージング市場は、製造活動の増加により著しい成長を遂げています。2024年2月、コカ・コーラはスプライトとスプライト・ゼロのオン・ザ・ゴー・ボトルからラベルを一時的に取り除くことを計画し、英国では500mlボトルのパック前面にエンボスロゴをあしらった「ラベルなし」パッケージングを限定的に試行しており、これは同国のパッケージング市場の需要を示しています。

- eコマース販売の成長、環境に優しくリサイクル可能なパッケージに対する飲食品メーカーの需要の増加、製品のパーソナライゼーションに対する需要の増加、産業用パッケージ分野の成長が、同国のパッケージ市場の成長を牽引しています。2023年11月、国際貿易庁の報告によると、英国は中国、米国に次いで世界第3位のeコマース市場を有しており、今後数年間、同国におけるパッケージング・ソリューションの需要を下支えすると予想されています。

- プラスチック使用に対する規制の強化は、市場に大きな影響を与えると予想されます。英国政府は、持続不可能な材料の使用を抑制することで、同時にリサイクル可能なプラスチックの市場価値を高め、世界の反響を呼ぶ持続可能な循環型経済を育成しています。2024年4月、英国は医薬品器具と医薬品パッケージングの使用済みリサイクルのための戦略を開発・実施するCAPA(Circularity in Primary Pharmaceutical Packaging Accelerator)イニシアチブを立ち上げ、同国のリサイクル可能なパッケージングソリューションに弾みをつけた。

- パッケージングの選択における持続可能性と手頃な価格との間の対立は、英国のパッケージング市場においてますます明白になってきています。消費者が環境に優しい選択肢の経済的な意味合いと格闘するにつれ、安価で持続可能でない選択肢への傾向が広まりつつあり、持続可能なパッケージングソリューションの採用に対する市場の課題上昇に影響を与えています。

- しかし、COVID-19の大流行が市場に影響を及ぼし、市場の複数の企業が使い捨てプラスチックの使用へとシフトしました。サプライチェーンは、使い捨てプラスチックパッケージングと医療用品の需要の急増に対応するために緊張しました。このようなプラスチック需要の大幅な急増は、循環型経済への移行という短期的な取り組みや目標に一時的な変化をもたらす可能性が高いです。これとは別に、プラスチックパッケージングの製造チェーンを圧迫することも予想されます。さらに、ロシアとウクライナの戦争は、パッケージングエコシステム全体に影響を与えています。

英国のパッケージング市場の動向

食品セグメントが市場成長を牽引すると予測

- 加工食品需要の増加と軽量でフレキシブルなパッケージングの採用拡大が、短期、中期、長期にわたって様々な影響を与えながら市場を牽引しています。冷凍食品パッケージング市場は、製品の品質に対する消費者の評価により急成長を遂げています。英国ではライフスタイルの変化により冷凍食品パッケージングの需要が増加しています。

- 同国の食品メーカーは、持続可能性を求めてプラスチックベースの製品から紙ベースの製品への置き換えを進めており、これが市場の成長を促進すると期待されています。例えば、2023年9月には、持続可能なパッケージングと紙の世界的リーダーであるモンディが、受賞歴のある米サプライヤーであるVeeteeとの協業により、英国で初めて紙パックのドライライスを発売しており、食品パッケージング分野における市場の成長を示しています。

- スタンドアップパウチは、食品の鮮度を維持し、製品の賞味期限を延ばすことができるため、予測期間を通じて標準的なパッケージング形態になると予想されます。さらに、パウチは見た目の美しさにも優れており、これが製品のマーケティング効果を高めています。このため、パウチは他の形態に代わる安定した選択肢として広く採用されており、予測期間中、需要と顧客受容の面でさらに勢いを増すと予想されます。

- 英国では、持続可能性とリサイクル性がブランドに対する消費者の好みを高める上で重要な役割を果たしています。ポストコンシューマー・リサイクル(PCR)パッケージング・ソリューションに対する市場の需要拡大に対応して、軟包装会社のProAmpac社はProActivePCRレトルトパウチの発売を発表しました。このレトルトパウチはペットフードや人間用食品のパッケージングを目的としたもので、レトルト用途での食品接触に対してFDAとEUの両方に準拠しています。このレトルトパウチは、消費者再利用率(PCR)30%以上のパッケージング材で、バージン樹脂の使用を最小限に抑えています。これらの独創的なパウチは、英国のプラスチック包装税(PPT)規制にも準拠しています。

- COVID-19パンデミック時に大幅に増加し、食品のネット注文を好む消費者行動を高めた後、年間のインターネット食品販売の変化率はパンデミック前の水準に達しています。2023年12月、Eviosysは食品業界の持続可能なパッケージングのパートナーとして選ばれるべく、オックスフォードシャーのワンテージにあるEviosysの研究開発センターを再始動させたが、これは同国市場の需要を示しています。

PET(ポリエチレンテレフタレート)が主要市場シェアを占める見込み

- 英国では、飲料会社がリサイクル可能なプラスチックの使用を増やしているため、ペットボトルは様々な産業で広く使用されています。飲食品市場は、ペットボトルと容器の主要ユーザーのひとつです。食品、飲料、化粧品、医薬品を含む様々な最終用途において、PETボトルは低コストで軽量であるため、PETボトルの使用が増加しており、同国のプラスチックボトル市場を牽引しています。

- さらに、新しい充填技術と耐熱性PETボトルの開発は、市場に新たな可能性と選択肢を提供しました。PETボトルは複数の分野で標準的に使用されているが、飲料、化粧品、衛生用品、洗剤はポリエチレン(PE)ボトルが主流で、これが国内市場の成長を支えています。

- PETプラスチック材料は、英国のFMCGブランドオーナーから高い需要を維持しています。2024年5月、リサイクル技術企業Polytagは、英国における使い捨てプラスチックパッケージングのトレーシングとリサイクルを最適化する取り組みであるPolytag Ecotrace Programmeの創設メンバーとして、英国の小売業者M&Sを指名しました。ポリタグ・エコトレース・プログラムは、ポリタグの不可視UVタグ検出装置を、大量の廃棄物を処理するリサイクルセンターに配備し、同国におけるPETボトルのリサイクルを支援するものです。

- PETボトル市場は、パレットへの積み込みやスーパーマーケットへの輸送を容易にするために、ボトルの設計が進歩しており、市場におけるPETボトルの需要を示しています。例えば、2024年3月に英国のAldiが自社ブランドの平型再生PETワインボトルを発売したが、これは100%再生PETを使用しているとのことで、市場の今後の成長の可能性を示しています。

- 国家統計局(英国)の報告によると、英国では食品とノンアルコール飲料に対する消費支出が増加しており、ボトルパッケージングの需要を支え、リサイクル可能なPETの需要と飲料パッケージングにおけるPET素材の利点に沿ったPETの採用を促進すると思われます。

英国のパッケージング業界の概要

英国のパッケージング市場は断片化されており、いくつかの世界的・地域的プレーヤーで構成されています。現在、全体のシェアで市場を独占しているプレーヤーもいます。顕著な市場シェアを持つこれらの大手企業は、エンドユーザー全体の顧客基盤の拡大に注力しています。Amcor PLC、DS Smith PLC、AptarGroup Inc.、Sealed Air Corporation、Sonoco Products Companyといったこれらの企業は、戦略的協業イニシアティブを活用して市場シェアと収益性を高めています。

- 2024年2月欧州の製紙・包装会社DS Smith PLCは、イングランド南東部にあるKemsley再生紙工場の新しい繊維調製ラインに約6,000万米ドルの投資を計画しています。これにより、同社は効率性の向上とコスト削減を通じて利益を得ることができます。これは、調査対象市場における有機的成長をサポートするためのベンダーによる投資を示しています。

- 2023年11月Amcor社とSaputo Dairy UK社は、UK Packaging Awardsで「Flexible Plastic Pack of the Year」を受賞した。両社は、国民に人気のチーズブランドCathedral City向けに、リサイクル可能な新しいおろしチーズパッケージを開発したことが評価されました。これは、同国における乳製品パッケージに対する需要と、英国で競争力を持つための利害関係者間の協力関係を示しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 業界バリューチェーン分析

- COVID-19のパッケージング業界への影響

- パッケージングにおける持続可能性技術の分析

- 世界のパッケージング市場の概要

第5章 市場力学

- 市場促進要因

- 消費財向け高級パッケージングに対するミレニアル世代からの需要の高まり

- eコマースパッケージングの需要急増

- 成長を続ける軟包装

- 市場抑制要因

- 開発コストの高騰とリサイクル概念の高まり

- 環境問題の高まり

第6章 市場セグメンテーション

- 業界別

- 食品

- 飲料

- ヘルスケア

- 化粧品、パーソナルケア、家庭用品

- 工業

- プラスチック包装別

- 材料タイプ

- PE(ポリエチレン)

- PP(ポリプロピレン)

- PVC(ポリ塩化ビニル)

- PET(ポリエチレンテレフタレート)

- その他の材料タイプ

- タイプ別

- 硬質プラスチックパッケージング

- ボトルとジャー

- トレー・容器

- その他の製品タイプ

- 軟質プラスチックパッケージング

- パウチ&バッグ

- フィルムとラップ

- その他の製品タイプ

- 材料タイプ

- パッケージング材タイプ別

- 紙

- カートンボード

- 段ボールとライナーボード

- その他のタイプ

- ガラス

- 金属(缶、ドラム、キャップ、栓、バルク容器)

- 紙

第7章 競合情勢

- 企業プロファイル

- Amcor PLC

- DS Smith PLC

- Owens Illinois Inc.

- Crown Holdings Inc.

- Berry Global Inc.

- Sealed Air Corporation

- Sonoco Products Company

- Graphic Packaging International LLC

- Greif Inc.

- Ball Corporation

- Westrock Company

- Silgan Holdings Inc.

- AptarGroup Inc.

- Huhtamaki Oyj

- Mondi Group

- Tetra Pak International SA

- Can-Pack UK Ltd

- Ardagh Group

第8章 投資分析

第9章 市場の将来

The United Kingdom Packaging Market size is estimated at USD 60.94 billion in 2025, and is expected to reach USD 68.18 billion by 2030, at a CAGR of 2.27% during the forecast period (2025-2030).

Key Highlights

- The packaging market in the United Kingdom has been witnessing significant growth owing to increased manufacturing activities. In February 2024, Coca-Cola planned to temporarily remove labels from Sprite and Sprite Zero on-the-go bottles in a limited trial of "label-less" packaging for 500-ml bottles with an embossed logo on the front of the pack in the United Kingdom, which shows the demand for the packaging market in the country.

- The growth of e-commerce sales, increased demand from food and beverage manufacturers for eco-friendly and recyclable packaging, increasing demand for product personalization, and the growing industrial packaging sector are driving the growth of the packaging market in the country. In November 2023, the International Trade Administration reported that the United Kingdom has the third-largest e-commerce market in the world after China and the United States, which is expected to support the demand for packaging solutions in the country in the coming years.

- The increase in regulations for plastic use is anticipated to affect the market significantly. By disincentivizing the usage of unsustainable materials, the UK government is simultaneously incentivizing the market value of recyclable plastic, fostering a sustainable circular economy that will have global repercussions. In April 2024, the United Kingdom launched the Circularity in Primary Pharmaceutical Packaging Accelerator (CAPA) initiative to develop and implement strategies for the end-of-use recycling of medicinal devices and pharmaceutical packaging, fueling the country's recyclable packaging solutions.

- The conflict between sustainability and affordability in packaging choices has been increasingly evident in the UK packaging market. As consumers grapple with the financial implications of eco-friendly alternatives, a trend toward cheaper, non-sustainable options is becoming more prevalent, impacting a rising market challenge for adopting sustainable packaging solutions.

- However, with the COVID-19 pandemic affecting the market studied, multiple companies in the market shifted toward the usage of single-use plastics. Supply chains strained to meet a surge in demand for single-use plastic packaging and medical supplies. Such a significant spike in plastic demand is likely to lead to a temporary change in the short-term initiatives and goals of transitioning toward a circular economy. Apart from this, it is also expected to put pressure on the plastic packaging manufacturing chain. Furthermore, the war between Russia and Ukraine has an impact on the overall packaging ecosystem.

United Kingdom Packaging Market Trends

Food Segment Expected to Drive Market Growth

- The increasing demand for processed food and the growing adoption of lightweight, flexible packaging drive the market, with varying impacts over the short, medium, and long term. The market for frozen food packaging is witnessing an upsurge due to the country's consumer appreciation of product quality. The demand for frozen food packaging has increased in the United Kingdom due to changing lifestyles.

- The country's food manufacturers are increasingly replacing plastic-based products in line with their paper-based counterparts for sustainability, which is expected to fuel the market's growth. For instance, in September 2023, Mondi, a global leader in sustainable packaging and paper, launched paper-packed dry rice in the United Kingdom for the first time by collaborating with award-winning rice supplier Veetee, showing the market's growth in the food packaging segment.

- Stand-up pouches are anticipated to become a standard form of packaging throughout the forecast period due to their capacity to maintain the freshness of food products and increase product shelf life. Furthermore, the pouches also offer a great visible aesthetic, which adds to the product's marketing benefits. This has led to the wide adoption of pouches as a stable alternative to other formats and is expected to take further momentum in terms of demand and customer acceptance during the forecast period.

- In the United Kingdom, sustainability and recyclability play a significant role in raising consumer preference for brands. Responding to the expanded market demand for post-consumer recycled (PCR) packaging solutions, a flexible packaging company, ProAmpac, announced the launch of its ProActivePCR Retort pouches. The retort pouches are intended for pet and human food packaging and are both FDA and EU-compliant for food contact in retort applications. They provide packaging with a post-consumer recycled (PCR) content of 30% or more, minimizing the use of virgin resins. These inventive pouches also adhere to United Kingdom Plastics Packaging Tax regulations (PPT).

- The percentage change in annual internet food sales has reached a pre-pandemic level after a significant increase during the COVID-19 pandemic, which has raised consumer behavior to prefer online ordering of foods. In December 2023, Eviosys relaunched Eviosys's R&D center in Wantage, Oxfordshire, to become the food industry's sustainable packaging partner of choice, which shows the demand for the market in the country.

PET (Polyethylene Terephthalate) Expected to Hold Major Market Share

- Plastic bottles are widely used in various industries in the United Kingdom due to the beverage companies' growing use of recyclable plastics. The food and beverage market is one of the major users of plastic bottles and containers. The rising use of PET bottles drives the country's plastic bottle market due to their low cost and lightweight in various end-user applications, including food, beverage, cosmetics, and pharmaceuticals.

- Furthermore, newer filling technologies and the development of heat-resistant PET bottles provided new possibilities and options in the market. While PET bottles are standard in multiple segments, beverages, cosmetics, sanitary products, and detergents are largely sold in polyethylene (PE) bottles, which is supporting the market's growth in the country.

- PET plastic materials sustain high demand from FMCG brand owners in the United Kingdom. In May 2024, the recycling technology firm Polytag named the UK retailer M&S as a founding member of its Polytag Ecotrace Programme, an initiative set to optimize the tracing and recycling of single-use plastic packaging in the United Kingdom. The Polytag Ecotrace Programme would deploy a vast network of Polytag's invisible UV tag detection equipment in strategically chosen recycling centers that handle high volumes of waste, which would support the recycled PET bottles in the country.

- The market has been registering advancements in the design of bottles to make them easy to load onto pallets and transport to supermarkets, which shows the demand for PET bottles in the market. For instance, in March 2024, Aldi in the United Kingdom launched its own-brand flat recycled PET wine bottles, which it said are made from 100% recycled PET, showing the market's future growth potential.

- The Office for National Statistics (United Kingdom) reported that consumer spending on food and non-alcoholic beverages in the United Kingdom has been increasing, which would support the demand for bottle packaging and fuel PET adoptions in line with the demand for recyclable PET and the advantage of PET material in beverage packaging.

United Kingdom Packaging Industry Overview

The packaging market in the United Kingdom is fragmented and consists of several global and regional players. Some of the players currently dominate the market in terms of overall share. These major players with prominent market share focus on expanding their customer base across end users. These companies, such as Amcor PLC, DS Smith PLC, AptarGroup Inc., Sealed Air Corporation, and Sonoco Products Company, leverage strategic collaborative initiatives to increase their market share and profitability.

- February 2024: The European paper and packaging company DS Smith PLC planned to invest about USD 60 million in a new fiber preparation line at its Kemsley recycled paper mill in southeast England. This would enable the company to deliver returns through improved efficiency and reduced costs. This shows the investments by the market vendors to support their organic growth in the market studied.

- November 2023: Amcor and Saputo Dairy UK won 'Flexible Plastic Pack of the Year' at the UK Packaging Awards. The companies were recognized for developing new, recycle-ready grated cheese packaging for the nation's favorite cheese brand, Cathedral City. This shows the demand for dairy product packaging in the country and the collaborations among the stakeholders to be competitive in the United Kingdom.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 on the Packaging Industry

- 4.5 Analysis of Technologies for Sustainability in Packaging

- 4.6 Overview of the Global Packaging Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand from the Millennials for Luxury Packaging for Consumer Goods

- 5.1.2 Soaring Demand for E-commerce Packaging

- 5.1.3 Flexible Packaging Continues to Grow Faster

- 5.2 Market Restraints

- 5.2.1 High Cost of Development and the Rising Concept of Recycling

- 5.2.2 The Rising Environmental Concerns

6 MARKET SEGMENTATION

- 6.1 By End-User Vertical

- 6.1.1 Food

- 6.1.2 Beverage

- 6.1.3 Healthcare

- 6.1.4 Cosmetics, Personal Care, and Household Care

- 6.1.5 Industrial

- 6.2 By Plastic Packaging

- 6.2.1 Material Type

- 6.2.1.1 PE (Polyethylene)

- 6.2.1.2 PP (Polypropylene)

- 6.2.1.3 PVC (Poly Vinyl Chloride)

- 6.2.1.4 PET (Polyethylene Terephthalate)

- 6.2.1.5 Other Material Types

- 6.2.2 By Type

- 6.2.2.1 Rigid Plastic Packaging

- 6.2.2.1.1 Bottles and Jars

- 6.2.2.1.2 Trays and Containers

- 6.2.2.1.3 Other Product Types

- 6.2.2.2 Flexible Plastic Packaging

- 6.2.2.2.1 Pouches & Bags

- 6.2.2.2.2 Films and Wraps

- 6.2.2.2.3 Other Product Types

- 6.2.1 Material Type

- 6.3 By Packaging Material Type

- 6.3.1 Paper

- 6.3.1.1 Carton Board

- 6.3.1.2 Containerboard and Linerboard

- 6.3.1.3 Other Types

- 6.3.2 Glass

- 6.3.3 Metal (Cans, Drums, Caps and Closures, and Bulk Containers)

- 6.3.1 Paper

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor PLC

- 7.1.2 DS Smith PLC

- 7.1.3 Owens Illinois Inc.

- 7.1.4 Crown Holdings Inc.

- 7.1.5 Berry Global Inc.

- 7.1.6 Sealed Air Corporation

- 7.1.7 Sonoco Products Company

- 7.1.8 Graphic Packaging International LLC

- 7.1.9 Greif Inc.

- 7.1.10 Ball Corporation

- 7.1.11 Westrock Company

- 7.1.12 Silgan Holdings Inc.

- 7.1.13 AptarGroup Inc.

- 7.1.14 Huhtamaki Oyj

- 7.1.15 Mondi Group

- 7.1.16 Tetra Pak International SA

- 7.1.17 Can-Pack UK Ltd

- 7.1.18 Ardagh Group