衛星ケーブルとアセンブリの市場機会と促進要因、産業動向分析、2025年~2034年予測

Satellite Cables and Assemblies Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1665227

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

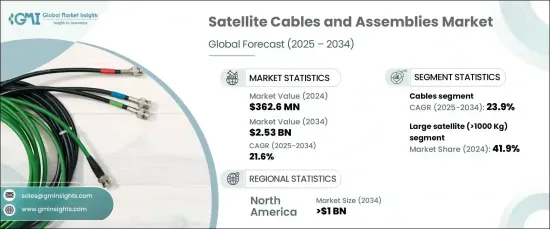

世界の衛星ケーブルとアセンブリ市場は、2024年に3億6,260万米ドルと評価され、2025~2034年までの推定CAGRは21.6%と、著しい成長を遂げようとしています。

この急成長の背景には、衛星ブロードバンドサービスの拡大により、遠隔地やサービスが行き届いていない地域で信頼性の高い高速インターネットへの需要が高まっていることがあります。通信、メディア、防衛などの主要産業は、先進的衛星通信ネットワークへの依存度を高めており、先進的ケーブルや組立部品が必要とされています。特に地方における衛星ベースのインターネットサービスの台頭は、高速データ転送をサポートできる堅牢なケーブルとコネクターの重要な必要性を強調しています。

市場は衛星タイプによって、小型衛星(500kgまで)、中型衛星(501~1,000kg)、大型衛星(1,000kg以上)に区分されます。2024年には、大型衛星が41.9%のシェアで市場を独占します。重量が1,000kgを超えることが多いこれらの衛星は、複雑な通信、地球観測、科学研究のミッションに不可欠です。これらの衛星は、配電、データ伝送、通信サブシステムを管理するために高性能のケーブルとアセンブリを必要とします。大型衛星の配備が進むにつれて、宇宙の過酷な条件に耐えられるように設計された耐久性のある軽量ケーブルの需要が高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034 |

| 開始金額 | 3億6,260万米ドル |

| 予測金額 | 25億3,000万米ドル |

| CAGR | 21.6% |

衛星ケーブルとアセンブリ市場は、部品別にケーブル、コネクタ、その他に分類されます。予測期間中のCAGRは23.9%で、ケーブルセグメントが最も急成長すると予測されています。ケーブルは、衛星システム内の信頼性の高い電力とデータの伝送を確保する上で極めて重要な役割を果たしています。産業は、放射線、極端な温度、機械的ストレスへの耐性など、厳しい性能基準を満たす製品の開発に注力しています。衛星技術の進歩により、宇宙での運用の完全性を維持しながら高速データ転送をサポートできる、柔軟で軽量かつ耐久性のあるケーブルの必要性が高まっています。

北米の衛星ケーブルとアセンブリ市場は2034年までに10億米ドルに達すると予想されており、米国がこの成長の最前線にあります。宇宙通信、探査、衛星ベースのサービスに対する投資の増加が、高性能衛星ネットワークをサポートする先進的ケーブルシステムの需要を促進しています。米国政府の取り組みや民間企業の衛星打ち上げへの参加が、革新的な衛星技術の開発を後押ししています。衛星コンステレーションとブロードバンド構想の拡大は、このダイナミックで急速に進化する市場において、信頼性が高く効率的で耐久性のあるケーブルの必要性をさらに強調しています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 二次資料

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 変革

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- 衛星ブロードバンドと通信システムへの需要の高まり

- 衛星打上げ活動と宇宙開発イニシアティブの増加

- 衛星の小型化とコスト削減技術の進歩

- 高性能で軽量な衛星ケーブルとアセンブリへのニーズの高まり

- IoTやAIアプリケーションにおける衛星システムの利用拡大

- 産業の潜在的リスク・課題

- 先進的ケーブルとアセンブリ材料に関連する高コスト

- 過酷な環境条件下での品質基準維持の課題

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推定・予測:衛星タイプ別、2021~2034年

- 主要動向

- 小型衛星(500Kg以下)

- 中型衛星(501~1,000Kg)

- 大型衛星(1,000Kg以上)

第6章 市場推定・予測:導体材料別、2021~2034年

- 主要動向

- 金属合金

- 繊維

第7章 市場推定・予測:部品別、2021~2034年

- 主要動向

- ケーブル

- ラウンドケーブル

- フラット/リボンケーブル

- コネクター

- その他

第8章 市場推定・予測:断熱タイプ別、2021~2034年

- 主要動向

- 熱硬化性

- 熱可塑性

第9章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Amphenol Corporation

- Axon'Cable SAS

- Cicoil Flat Cables

- Cinch Connectivity Solutions

- Eaton Corporation

- Huber+Suhner

- Meggitt PLC

- Nexans SA

- Prysmian Group

- Smiths Group PLC

- TE Connectivity

- W.L. Gore &Associates, Inc.

目次

The Global Satellite Cables And Assemblies Market, valued at USD 362.6 million in 2024, is poised for remarkable growth with an estimated CAGR of 21.6% from 2025 to 2034. This surge is driven by the growing demand for reliable, high-speed internet in remote and underserved regions, fueled by the expansion of satellite broadband services. Key industries such as telecommunications, media, and defense increasingly rely on advanced satellite communication networks, necessitating sophisticated cable and assembly components. The rise of satellite-based internet services, particularly in rural areas, underscores the critical need for robust cables and connectors capable of supporting high data transfer speeds.

The market is segmented by satellite type into small satellites (up to 500 kg), medium satellites (501-1000 kg), and large satellites (over 1000 kg). In 2024, large satellites dominated the market with a 41.9% share. These satellites, often weighing over 1,000 kg, are vital for complex communication, Earth observation, and scientific research missions. They require high-performance cables and assemblies to manage power distribution, data transmission, and communication subsystems. The increasing deployment of large satellites drives demand for durable, lightweight cables engineered to withstand the harsh conditions of space.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $362.6 Million |

| Forecast Value | $2.53 Billion |

| CAGR | 21.6% |

By component, the satellite cables and assemblies market is categorized into cables, connectors, and others. The cables segment is projected to be the fastest-growing, with an impressive CAGR of 23.9% during the forecast period. Cables play a pivotal role in ensuring reliable power and data transmission within satellite systems. The industry is focused on developing products that meet stringent performance standards, including resistance to radiation, temperature extremes, and mechanical stress. Advances in satellite technology have amplified the need for flexible, lightweight, and durable cables capable of supporting high-speed data transfer while maintaining operational integrity in space.

North America satellite cables and assemblies market is expected to reach USD 1 billion by 2034, with the United States at the forefront of this growth. Increased investments in space communication, exploration, and satellite-based services are driving demand for advanced cable systems that support high-performance satellite networks. U.S. government initiatives and private sector participation in satellite launches are boosting the development of innovative satellite technologies. The expansion of satellite constellations and broadband initiatives further underscores the need for reliable, efficient, and durable cables in this dynamic and rapidly evolving market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising demand for satellite broadband and communication systems

- 3.6.1.2 Increasing satellite launch activities and space exploration initiatives

- 3.6.1.3 Advancements in satellite miniaturization and cost reduction technologies

- 3.6.1.4 Growing need for high-performance, lightweight satellite cables and assemblies

- 3.6.1.5 Expanding use of satellite systems in IoT and AI applications

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High costs associated with advanced cable and assembly materials

- 3.6.2.2 Challenges in maintaining quality standards under extreme environmental conditions

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Satellite Type, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Small satellite (<500 Kg)

- 5.3 Medium satellite (501-1000 Kg)

- 5.4 Large satellite (>1000 Kg)

Chapter 6 Market Estimates & Forecast, By Conductor Material, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Metal alloys

- 6.3 Fibers

Chapter 7 Market Estimates & Forecast, By Component, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Cables

- 7.2.1 Round cables

- 7.2.2 Flat/ ribbon cables

- 7.3 Connectors

- 7.4 Others

Chapter 8 Market Estimates & Forecast, By Insulation Type, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 Thermosetting

- 8.3 Thermoplastic

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Amphenol Corporation

- 10.2 Axon' Cable SAS

- 10.3 Cicoil Flat Cables

- 10.4 Cinch Connectivity Solutions

- 10.5 Eaton Corporation

- 10.6 Huber+Suhner

- 10.7 Meggitt PLC

- 10.8 Nexans SA

- 10.9 Prysmian Group

- 10.10 Smiths Group PLC

- 10.11 TE Connectivity

- 10.12 W.L. Gore & Associates, Inc.

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日