|

市場調査レポート

商品コード

1851776

サービスデリバリプラットフォーム:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Service Delivery Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| サービスデリバリプラットフォーム:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月17日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

概要

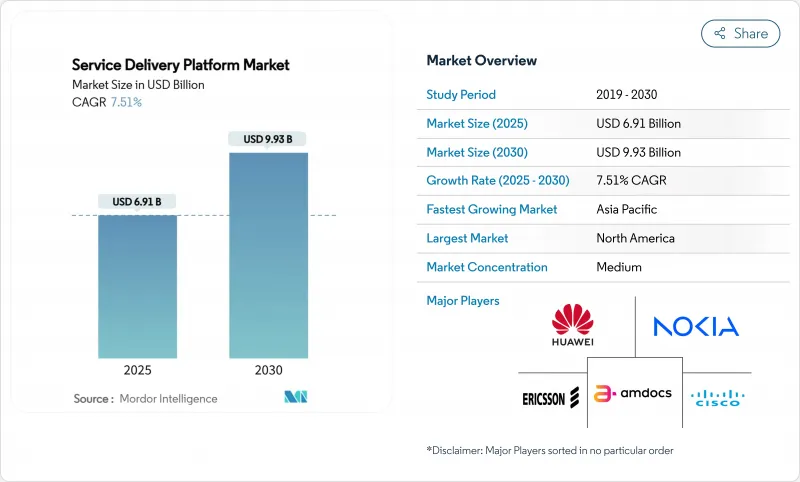

サービスデリバリプラットフォームの市場規模は2025年に69億1,000万米ドル、2030年には93億3,000万米ドルに拡大すると予測され、この期間のCAGRは7.51%です。

5Gのスタンドアロン展開、クラウドネイティブの変革戦略、レガシーOSS/BSSスタックの緊急リプレースなどが相まって、資本はプラットフォームの近代化に向かっています。通信事業者は、リリースサイクルを短縮し、ネットワークのスライシングを可能にし、低遅延の企業ユースケースを収益化するマイクロサービスアーキテクチャに投資しています。ソフトウェア定義の俊敏性は、産業キャンパスにおけるプライベート5Gの採用や、超パーソナライズされた消費者向け提案に対する需要の高まりによって、さらに増幅されています。ハイパースケールなクラウドプロバイダー、従来のネットワークベンダー、ニッチなソフトウェアスペシャリストが同じビジネスチャンスに集中し、統合、パートナーシップ、オープンAPI戦略を余儀なくされているため、競合の激しさは増しています。

世界のサービスデリバリープラットフォーム市場の動向と洞察

柔軟なサービス・オーケストレーションを推進する5Gの展開

5Gの単体構築では、事業者はミリ秒単位でネットワークリソースを割り当て、オープンAPIを通じて機能を公開するオーケストレーションレイヤーを採用する必要があります。エリクソンは、ネットワーク・スライシングだけで2,000億米ドルの新たな価値を解き放つことができると見積もっており、シングテルが2024年にプレミアム5G+層を構築するためにコンシューマー向けスライシングを商用化した理由を強調しています。キャリアがワークロードをクラウドネイティブコアに移行したため、世界のモバイルコアへの支出は2025年第1四半期に前年同期比で32%急増しました。サービスベースのアーキテクチャは本質的にマイクロサービスに適しており、プラットフォームベンダーは遅延、帯域幅、セキュリティ保証を収益化するポリシーエンジンを組み込んでいます。そのため、サービスデリバリープラットフォーム市場は、5G無線リソースを企業のSLAにリンクさせるインテントベースのオーケストレーションに対する需要を捉えています。ヘルスケア、ロジスティクス、メディアでより多くのスライスが稼動するにつれ、収益機会は増大し、プラットフォームの拡張性が競争力を左右するようになると思われます。

通信事業者のクラウドネイティブ化

ハイパースケール・アライアンスは、通信事業者のITロードマップを再構築しています。VodafoneとMicrosoftの10年にわたる15億米ドルの契約は、欧州とアフリカ全体で3億人の加入者を対象としており、ワークロードをAzureに移行し、リリースサイクルを数ヶ月から数週間に短縮するDevOpsのプラクティスを組み込んでいます。Telefonicaドイツは、4,500万人のユーザーをクラウドネイティブな5Gコアに移行させ、サービスを中断させることなく、コンテナ化されたネットワーク機能の成熟度を証明しました。現在では、継続的インテグレーションと自動化されたテストが迅速な機能の有効化を支えており、動的なリソースのスケーリングがコスト規律を向上させています。ベンダーはSaaSデリバリーモデルと従量課金ライセンスで対応し、対応可能なサービスデリバリープラットフォーム市場を拡大しています。長期的には、クラウドファースト戦略により、通信事業者は専有ハードウェアへの依存度を下げ、業界横断的な提案をより機敏に開始できるようになると思われます。

レガシーOSS/BSSを近代化するための高額なCAPEX

メインフレーム時代のスタックをリプレースするための先行投資は、多くの中堅・新興市場の通信事業者が本格的なデジタル化を躊躇する要因となっています。エアテル・スリランカ(Airtel Sri Lanka)の変革では、営業IT費用を80%削減したが、段階的な資本注入と専門家によるコンサルティング・サポートが必要でした。小規模な通信事業者は、コアのサイロをそのまま残すオーバーレイ・アプローチに頼ることが多く、当面のプラットフォーム収益を抑制しています。クラウドのサブスクリプション・モデルはバランスシートへのプレッシャーを和らげるが、統合の複雑さは依然としてプロフェッショナル・サービスの予算を大きく左右します。その結果、短期的な導入曲線は平坦化し、サービスデリバリープラットフォーム市場全体のCAGRは、推定でマイナス1.2%ポイント鈍化する可能性があります。

セグメント分析

サービスデリバリープラットフォーム市場のソフトウェア売上はCAGR 11.7%で上昇しており、事業者が独自のアプライアンスからAPI中心のオーケストレーションスイートへ移行するにつれて、ヘッドラインの成長率を上回っています。統合、移行、マネージド・オペレーションに対する継続的な需要を反映して、2024年の売上高の60.3%は依然としてサービスが占めています。ベンダーは、AI、アナリティクス、ローコードツールなど、サービスイノベーションのタイムラインを短縮するために、大幅なR&Dを割り当てている(ファーウェイだけでも2024年に248億米ドルを費やしている)。

プラットフォーム・ソフトウェアは、ネットワークの複雑性を抽象化し、パートナーのオンボーディングを促進するコンポーザブル・マイクロサービスを可能にします。Nexignのフレームワークのようなプロジェクトは、統合期間を3ヶ月から4週間に短縮し、メガフォンが170以上のサービスを迅速に展開できるようにしました。レガシーのカットオーバーフェーズやDevOpsの実現には、プロフェッショナルサービスが不可欠です。これらを総合すると、ソフトウェアの増加により、サービス・デリバリー・プラットフォームの市場シェアは、モジュール型のライセンスベース製品のシェアを着実に引き上げると思われます。

クラウド実装は2024年の世界売上高の63.1%を占め、通信事業者が資本コミットメントのリスクを回避し、弾力的なスケーリングを追求するにつれて、CAGR 14.2%で増加しています。クラウドファーストの流れは、T-MobileがプリペイドBSSをAWSに移行してハードウェアのオーバーヘッドを削減し、稼働時間を向上させていることからも明らかです。

ハイブリッド設計図は、データレジデンシー規則によりオンプレミスのコントロールプレーンが義務付けられている金融サービスや公共セクターで出現しています。ベンダーのツールキットは現在、CI/CDパイプラインを自動化し、ゼロタッチでネットワーク機能をアップグレードできるようになっており、クラウドへの選好をさらに高めています。その結果、クラウド導入に起因するサービスデリバリプラットフォームの市場規模は、2030年までに50億米ドルを超えると予想されています。

地域分析

北米は2024年に売上高の31.6%を占め、積極的な5Gの展開スケジュール、周波数政策、クラウドに関する深い専門知識によって支えられています。ベライゾンによる200億米ドルのフロンティア買収やチャーターによる345億米ドルのコックス買収などの大規模合併は、光ファイバーのフットプリントを拡大し、エンド・ツー・エンドのプラットフォーム統合を刺激します。TモバイルのKKRとの合弁によるメトロネットの買収は、統合された固定ワイヤレス提案を加速させる。サプライチェーンのセキュリティと海底ケーブルの監視に対する規制の焦点は、並行してコンプライアンス・コンサルティング需要を生み出し、この地域のベンダー・サービス・ポートフォリオを形成しています。

アジア太平洋地域のCAGRは14.1%と世界最速と予測されるが、これは通信事業者がすでに2024年上半期の売上高の19.9%を占めているコネクティビティ以外の収益に軸足を移しているためです。チャイナ・モバイルとチャイナ・ユニコムは、クラウド、ビデオ、産業用デジタル・サービスに規模の優位性を活かしています。StarHubのCloud Infinityプログラムは、AWS、Google Cloud、Nokiaとのマルチクラウド・オーケストレーションを活用し、企業ワークロードに10ミリ秒以下のレイテンシーを実現するもので、アーキテクチャの革新性を示しています。各国のデジタルエコノミー政策は、民間の5Gやスマート製造業の展開にインセンティブを与え、地域の勢いを強めています。

欧州は成熟した規制の多い環境であり、EUのAI法やデータ主権指令がアーキテクチャの選択に影響を与えています。VodafoneのAzureパートナーシップは、複数の国市場におけるクラウドネイティブな変革への長期的な資本コミットメントを例示しています。英国のテレコム・セキュリティ法は、Tier1事業者に258のサイバーセキュリティ管理の実施を義務付け、プラットフォームのアップグレードを加速させています。南米と中東・アフリカは低いベースラインからスタートするが、モバイル普及率の上昇と政府のデジタル化計画は、俊敏なサービス・デリバリー・フレームワークに対する将来の需要が旺盛であることを示しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

よくあるご質問

目次

第1章 イントロダクション

- 市場の定義と調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 柔軟なサービス・オーケストレーションを推進する5Gの展開

- 通信事業者のクラウドネイティブ化

- デジタルBSSと超パーソナライズド・サービスへの需要

- スケーラブルなサービス管理が求められるIoTの普及

- マイクロサービスとコンテナ化の採用

- ネットワークスライシングとプライベート5Gの収益化

- 市場抑制要因

- レガシーOSS/BSSを近代化するための高CAPEX

- サイバーセキュリティとデータプライバシーへの懸念

- クラウド-SDPエコシステムにおけるベンダーのロックイン

- DevOps/クラウドネイティブ人材の不足

- バリューチェーン分析

- 重要な規制枠組みの評価

- 主要利害関係者の影響評価

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- マクロ経済要因の影響

第5章 市場規模と成長予測

- タイプ別

- ソフトウェア

- サービス

- 展開モード別

- オンプレミス

- クラウド

- 用途別

- 通信事業者

- BFSI

- メディアとエンターテイメント

- ヘルスケア

- 小売とeコマース

- 政府および公共部門

- その他

- ネットワークタイプ別

- ワイヤレス

- ワイヤライン

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリアおよびニュージーランド

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- エジプト

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Huawei Technologies Co., Ltd.

- HCL Technologies Limited

- Fujitsu Limited

- Accenture plc

- Telenity, Inc.

- Nokia Corporation

- Ericsson AB

- Cisco Systems, Inc.

- Amdocs Limited

- Oracle Corporation

- ZTE Corporation

- Hewlett Packard Enterprise Company

- Tata Consultancy Services Limited

- NEC Corporation

- IBM Corporation

- CSG Systems International, Inc.

- Comarch SA

- Tech Mahindra Limited

- Openet(Amdocs)

- Qvantel Oy

第7章 市場機会と今後の動向

- ホワイトスペースとアンメットニーズ評価