ポリウレタン接着剤とシーラント:市場シェア分析、産業動向、成長予測(2025~2030年)

Polyurethane Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1641901

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

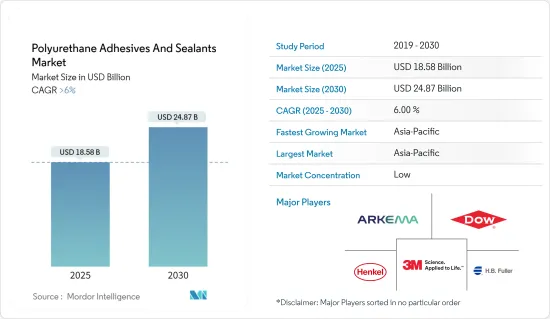

ポリウレタン接着剤とシーラント市場規模は2025年に185億8,000万米ドルと推定・予測され、2030年には248億7,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは6%を超えると予測されます。

COVID-19パンデミックは世界のポリウレタン(PU)接着剤とシーラント市場に大きな影響を与えました。ロックダウンや渡航制限が原料や完成品のサプライチェーンに混乱を引き起こし、供給不足と価格上昇を招いた。政府や企業はパンデミックの間、医療やその他の必要不可欠なセグメントを優先し、これらの製品に大きく依存する建設、自動車、その他の産業への投資の減少につながりました。しかし、市場はCOVID-19の最初の影響から回復し、長期的には緩やかなペースで成長を続けています。

主要ハイライト

- アジア地域では、都市化とインフラ整備に伴う建設活動の増加と包装産業の成長が、接着剤とシーラントの需要を押し上げると予想されます。

- しかし、揮発性有機化合物の使用に関する政府の厳しい環境規制が、市場拡大の妨げになると予想されます。

- バイオベースのポリウレタン(PU)ホットメルト接着剤に対する需要は、広範なPU接着剤とシーラント市場の中で着実に高まっており、世界市場に有利な成長機会を生み出すと予想されます。

- アジア太平洋は最大の市場であり、予測期間中に最も急成長する市場となる見込みです。これは、中国、インド、ASEAN諸国からの消費の増加によるものです。

ポリウレタン接着剤とシーラントの市場動向

建築・建設産業が市場を独占

- 接着剤とシーラントの消費量が最も多いのは建設部門です。ポリウレタン接着剤とシーラントは、その弾性と構造的特性により、コンクリート、木材、プラスチック、ガラスなど多くの基材に良好な接着性を発揮します。継続的な技術的進歩とともに、これらの特性は、住宅建設におけるポリウレタン接着剤とシーラントの使用を増加させています。

- アジア太平洋の建設部門は世界最大です。同地域の人口増加、中間所得層の増加、都市化により、同部門は健全な成長率を示しています。

- 中国政府は、第14次5ヵ年計画期間中(2021~2025年)に建設部門の包括的な開発計画を導入しました。この計画は、この極めて重要な産業を、より環境に配慮し、技術的に先進的で安全な軌道へと導くことを目的としています。住宅・都市・農村開発省がまとめたガイドラインによると、建設産業は2025年、国内総生産(GDP)の6%という貢献度を維持する見込みです。

- 中国の建設部門は世界最大の建設産業であり、5,300万人以上を雇用しています。国家統計局によると、中国の建設部門の生産高は、2021年の29兆3,100億人民元(約4兆2,900億米ドル)に対し、2022年には31兆2,000億人民元(約4兆5,700億米ドル)となり、6%の成長を記録しました。中国の建設産業は2022年のGDPに約6.9%寄与しました。

- 住宅・都市・農村開発省の予測によると、中国の建設部門は2025年以降もGDPの6%を維持すると予想されています。

- 国際貿易機関によると、中国は世界最大の建設市場であり、世界で最も都市化率が高いです。米国建築家協会(AIA)上海支部のデータによると、中国は2025年までに、1990年代以降、ニューヨークの10個分に相当する都市を建設するといいます。

- 中国は2030年までに約13兆米ドルを建築物に投じると予想されており、市場には明るい展望が開けています。同国は世界最大の建設市場であり、世界全体の建設投資の20%を占めています。

- 北米では、米国国勢調査によると、2022年に約1兆7,929億米ドルが建設に費やされ、これは2021年の年間建設支出額を10%上回るかなりの額です。これは、同地域の建築・建設が上昇傾向にあることを示しています。

- さらに、Eurostatによると、EU復興基金からの新規投資により、2022年の欧州の建設部門は2.5%成長しました。2022年の主要建設プロジェクトは、非住宅建設(オフィス、病院、ホテル、学校、工業用建物)が全体の31.3%を占めます。

- これらのことから、今後数年間はポリウレタン接着剤とシーリング材を購入したいと考える人が増えると考えられます。

アジア太平洋が市場を独占する

- アジア太平洋が世界市場を独占しています。中国、インド、日本などの国々における包装、建設、自動車、医療などの産業からの需要の増加が、調査された市場を牽引しています。

- 中国は、現在進行中の都市化傾向を積極的に推進・維持しており、2030年までに70%の都市化を目指しています。その結果、中国のような国々における建設活動の活発化が、この地域における接着剤産業の成長を促進すると予想されます。これらの要因は総体的に、地域全体の接着剤需要の高まりに寄与しています。

- Invest Indiaによると、インドの建設産業は2025年までに1兆4,000億米ドルに達すると予想され、インドの建設産業は、セクター間の連携とPMAY-Uの技術サブミッションの下で識別された54以上の世界の革新的な建設技術で250のサブセクターにわたって動作し、インドの建設セクターの新時代を開始します。

- ポリウレタン(PU)接着剤とシーラントは、靴の耐久性、快適性、美観を確保するために、靴産業において重要な役割を果たしています。アッパーとソールの接着から縫い目のシール、装飾品の取り付けまで、靴製造の様々な段階で使用されています。

- 中国は世界最大のPU消費国であり、世界最大の靴生産国でもあります。中国は世界最大のフットウェア製造・輸出国であり、世界を席巻しています。中国は2022年に130億足以上の靴とブーツを出荷しました。

- 一方、中国は世界最大の自動車生産・購入国です。OICAによると、中国は世界最大の自動車生産拠点であり、2022年の自動車総生産台数は2,702万台で、昨年の2,608万台に比べて3%の増加を記録します。

- したがって、このような市場動向は、予測期間中、同地域の接着剤とシーラント市場の成長に大きな影響を与えると予想されます。

ポリウレタン接着剤とシーラント産業概要

ポリウレタン接着剤とシーラント市場は細分化されています。主要企業(順不同)には、3M、H.B. Fuller Company、Arkema(Bostik)、Dow、Henkel AG &Co.KGaAなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- アジア地域における建設産業の需要増加

- 包装産業の成長

- その他の促進要因

- 抑制要因

- 有害物質に関する規制強化と環境問題

- 原料価格の変動

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- 技術

- 水ベース

- 溶剤ベース

- ホットメルト

- その他の技術(バイオベース、ナノPU接着剤など)

- エンドユーザー産業

- 建築・建設

- 医療

- 自動車・輸送

- 包装

- フットウェア皮革

- 電気・電子

- その他のエンドユーザー産業(木工・家具、消費財など)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- インドネシア

- マレーシア

- タイ

- ベトナム

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- トルコ

- 北欧諸国

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- カタール

- アラブ首長国連邦

- エジプト

- アルジェリア

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- 3M

- Arkema

- Beijing Comens New materials Co. Ltd

- Dow

- H.B.Fuller Company

- Henkel AG & Co.KGaA

- Hubei Huitian New Materials Co. Ltd

- Huntsman International LLC

- Jowat SE

- Kangada New Materials(Group)Co. Ltd

- MAPEI SpA

- NANPAO RESINS CHEMICAL GROUP

- Pidilite Industries Ltd

- Sika AG

- Soudal Holding NV

第7章 市場機会と今後の動向

- バイオベースPUホットメルト接着剤に対する需要の高まり

目次

The Polyurethane Adhesives And Sealants Market size is estimated at USD 18.58 billion in 2025, and is expected to reach USD 24.87 billion by 2030, at a CAGR of greater than 6% during the forecast period (2025-2030).

The COVID-19 pandemic had a significant impact on the global polyurethane (PU) adhesives and sealants market. Lockdowns and travel restrictions caused disruptions in the supply chain for raw materials and finished products, leading to shortages and price increases. Governments and businesses prioritized healthcare and other essential sectors during the pandemic, leading to reduced investment in construction, automotive, and other industries that rely heavily on these products. However, the market has recovered from the initial impact of COVID-19 and continues to grow at a moderate pace in the long run.

Key Highlights

- Increased construction activities in the Asian region, driven by urbanization and infrastructure development, along with the growth in the packaging industry, are expected to propel the demand for adhesives and sealants.

- However, strict environmental regulations set by the government on the use of volatile organic compounds are anticipated to hamper the expansion of the market studied.

- The demand for bio-based polyurethane (PU) hot-melt adhesives is steadily rising within the broader PU adhesives and sealants market, which is expected to create lucrative growth opportunities in the global market.

- The Asia-Pacific region represents the largest market and is also expected to be the fastest growing market over the forecast period. This is due to the increase in consumption from China, India, and ASEAN Countries.

Polyurethane Adhesives And Sealants Market Trends

Building and Construction Industry to Dominate the Market

- The construction sector has the highest consumption of adhesives and sealants. Polyurethane adhesives and sealants offer good adhesion to numerous substrates, such as concrete, wood, plastic, and glass, due to their elasticity and structural properties. Together with ongoing technical advancement, these characteristics have increased the use of polyurethane adhesive and sealant in residential construction.

- The construction sector in the Asia-Pacific region is the largest in the world. The sector is growing at a healthy rate due to the region's rising population, increase in middle-class incomes, and urbanization.

- As per the Government of China, China introduced a comprehensive development blueprint for its construction sector during the 14th Five-Year Plan period (2021-2025). This plan aims to steer the pivotal industry towards a more environmentally responsible, technologically advanced, and safer trajectory. As per the guidelines outlined by the Ministry of Housing and Urban-Rural Development, the construction industry is expected to uphold its contribution at 6 percent of the nation's GDP through 2025.

- China's construction sector is the largest construction industry in the world, employing more than 53 million people. According to the National Bureau of Statistics, the Chinese construction sector output was CNY 31.20 trillion (~USD 4.57 trillion) in 2022, compared to CNY 29.31 trillion (~USD 4.29 trillion) in 2021, registering a 6% growth. China's construction industry contributed around 6.9% to its GDP in 2022.

- As per the Ministry of Housing and Urban-Rural Development forecast, China's construction sector is expected to maintain a 6% share of the country's GDP moving into 2025.

- According to the International Trade Organization, China is the world's largest construction market, with the highest urbanization rate globally. According to data from the American Institute of Architects (AIA) Shanghai, by 2025, China will have built a city equivalent to 10 in New York since the 1990s.

- China is expected to spend nearly USD 13 trillion on buildings by 2030, creating a positive outlook for the market. The country has the largest construction market in the world, encompassing 20% of all construction investments globally.

- In North America, according to the US Census, around USD 1,792.9 billion was spent on construction in 2022, a considerable amount and 10% higher than the annual spending on construction in 2021. This indicates an upward trend for buildings and construction in the region.

- Furthermore, according to Eurostat, the European construction sector grew by 2.5% in 2022 due to new investments from the EU Recovery Fund. The major construction projects in 2022 accounted for non-residential construction (offices, hospitals, hotels, schools, and industrial buildings), accounting for 31.3% of total activity.

- All of these things are likely to make more people want to buy polyurethane adhesives and sealants over the next few years.

Asia-Pacific to Dominate the Market

- The Asia-Pacific region dominated the global market. The increasing demand from industries such as packaging, construction, automotive, healthcare, etc., in countries such as China, India, and Japan is driving the market studied.

- China is actively promoting and sustaining an ongoing urbanization trend, aiming for an anticipated rate of 70% by the year 2030. Consequently, the heightened construction activities in countries such as China are expected to propel growth in the adhesive industry within the region. These factors collectively contribute to an elevated demand for adhesives across the region.

- As per Invest India, the Indian construction industry is expected to reach USD 1.4 trillion by 2025, and the construction industry in India works across 250 sub-sectors with linkages across sectors and over 54 global innovative construction technologies identified under a Technology Sub-Mission of PMAY-U to start a new era in the Indian construction sector.

- Polyurethane (PU) adhesives and sealants play a crucial role in the footwear industry, ensuring the durability, comfort, and aesthetic appeal of shoes. They are used in various stages of shoe manufacturing, from bonding the upper to the sole to sealing seams and attaching embellishments.

- China is the largest consumer of PU and the largest producer of footwear globally. China is the world's largest footwear manufacturer and exporter, dominating worldwide. China shipped more than 13 billion pairs of shoes and boots in 2022.

- On the other hand, China is the world's greatest producer and purchaser of automobiles. According to OICA, China has the largest automotive production base in the world, with a total vehicle production of 27.02 million units in 2022, registering an increase of 3% compared to 26.08 million units produced last year.

- Hence, such market trends are expected to significantly impact the growth of the adhesives and sealants market in the region during the forecast period.

Polyurethane Adhesives and Sealants Industry Overview

The polyurethane adhesives and sealants market is fragmented in nature. The major players (not in any particular order) include 3M, H.B. Fuller Company, Arkema (Bostik), Dow, and Henkel AG & Co. KGaA, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Demand from the Construction Industry in the Asian Region

- 4.1.2 Growth in the Packaging Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stricter Regulations on Hazardous Materials and Environmental Concerns

- 4.2.2 Fluctuating Raw Material Prices

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Technology

- 5.1.1 Water-based

- 5.1.2 Solvent-based

- 5.1.3 Hot-melt

- 5.1.4 Other Technologies (Bio-based, Nano-PU adhesives, etc.)

- 5.2 End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Healthcare

- 5.2.3 Automotive and Transportation

- 5.2.4 Packaging

- 5.2.5 Footwear and Leather

- 5.2.6 Electrical and Electronics

- 5.2.7 Other End-user Industries (Woodworking and Furniture, Consumer Goods, etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Indonesia

- 5.3.1.6 Malaysia

- 5.3.1.7 Thailand

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Turkey

- 5.3.3.8 NORDIC Countries

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Qatar

- 5.3.5.4 United Arab Emirates

- 5.3.5.5 Egypt

- 5.3.5.6 Algeria

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Beijing Comens New materials Co. Ltd

- 6.4.4 Dow

- 6.4.5 H.B.Fuller Company

- 6.4.6 Henkel AG & Co.KGaA

- 6.4.7 Hubei Huitian New Materials Co. Ltd

- 6.4.8 Huntsman International LLC

- 6.4.9 Jowat SE

- 6.4.10 Kangada New Materials (Group) Co. Ltd

- 6.4.11 MAPEI SpA

- 6.4.12 NANPAO RESINS CHEMICAL GROUP

- 6.4.13 Pidilite Industries Ltd

- 6.4.14 Sika AG

- 6.4.15 Soudal Holding NV

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Demand for Bio-based PU Hot-melt Adhesives

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日