中東・アフリカのポリウレタン(PU)接着剤市場シェア分析、産業動向、成長予測(2025~2030年)

MEA Polyurethane (PU) Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1639433

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

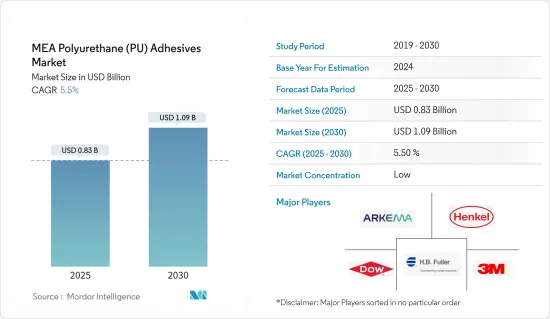

中東・アフリカのポリウレタン接着剤市場規模は2025年に8億3,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは5.5%で、2030年には10億9,000万米ドルに達すると予測されます。

COVID-19の発生は市場にマイナスの影響を与えました。いくつかの産業プロジェクトの停止や減速、移動制限、生産停止、労働力不足により、ポリウレタン(PU)接着剤市場の成長は低下しました。しかし、建築・建設、包装、医療、自動車など様々な最終用途産業からの消費増加により、2021年には大幅に回復しました。

主要ハイライト

- 短期的には、建設産業と医療インフラからの需要増加が、調査対象市場の成長を牽引する主要要因のひとつです。

- 逆に、VOC排出に関する厳しい環境規制は市場成長の妨げになると予想されます。

- しかし、バイオベースの接着剤へのシフトと軽量製品の製造への傾斜の高まりは、PU接着剤市場に機会を提供する可能性が高いです。

- サウジアラビアは中東・アフリカのPU接着剤市場を独占しており、予測期間中に最も高いCAGRを示すことになります。

中東・アフリカのポリウレタン(PU)接着剤市場動向

建築・建設産業が市場を独占

- エンドユーザー産業の中でも、建築・建設セグメントが同地域のPU接着剤消費を支配しています。

- PU接着剤には速硬化性と低強度特性があるため、木工やその他の建築用途に最適です。PU接着剤は、建設資材をつなぎ合わせるのに必要な高い強度を記載しています。

- その上、製品組立用接着剤に関しては、この材料は汎用性があります。プラスチック、ガラス、PVF、アルミニウム、ステンレス、その他の金属に適しており、接着基材の靭性に関係なく使用できます。

- サウジアラビア、クウェート、カタール、アラブ首長国連邦、エジプトなどの国々では、建設投資や建設活動の力強い成長が示されています。例えば、クウェート・ビジョン2035のサステイナブル生活環境軸には5つの柱があり、その中で最も顕著なものは、計画されたものを通じて市民に住宅ケアを提供することです。これは、約32億2,000万ウォン(105億米ドル)の5つのプロジェクトを通じて6万5,500戸の住宅供給を確保するもので、最後のプロジェクトは2029年までに終了します。

- これらのプロジェクトが実施されれば、州は現在の住宅需要91,000戸の約72%を満たすことになります。住宅ケア計画の最初のプロジェクトは、ジャベル・アル・アハマド市のクウェート2035(新クウェート)構想を中心としたもので、完成率95%を含み、2022年末に完成します。2つ目のプロジェクトはアル・ムトラアで、完成率は64%、2023年末に完成予定。

- 3つ目のプロジェクトは郊外の南アブドラ・アル・ムバラクで、完成率は72%、2025年末に完成予定。4番目のプロジェクトである南サバ・アル・アハマドの完成率は約14%で、まだ準備段階であり、2029年に完成する予定です。この南サード・アル・アブドゥラには、まだ準備段階で2029年に終了するため、完成率が13%となっています。このため、クウェートでは住宅建設が増加しており、クウェートのポリウレタン(PU)接着剤市場の需要拡大が見込まれています。

- したがって、このような国における建設産業の成長展望は、この地域におけるPU接着剤の消費を促進すると予想されます。

市場を独占するサウジアラビア

- サウジアラビアは、ポリウレタン(PU)接着剤の中東・アフリカ市場で最大のシェアを占めています。同国では、建設、医療インフラ、自動車拠点開発への投資が増加しており、ポリウレタン(PU)接着剤の需要は予測期間を通じて増加する見込みです。人口と可処分所得の増加は、より質の高い住宅建築開発への需要を増加させました。

- サウジアラビアの建設市場は、「ビジョン2030」、「NTP2020」、石油からの多角化のためのいくつかの進行中の改革により、大きな成長を示し、有利な可能性を提供すると期待されています。ビジョン2030、NTP2020、民間セクターの投資促進、進行中の改革は、予測期間中、サウジアラビアの建設産業によるポリウレタン接着剤市場の成長促進要因になると予想されます。

- さらに、「ビジョン2030」下では、2030年までにサウジアラビア全土で1万1,000室以上の豪華な客室を持つホテルが新たに80軒開業する予定です。そのため、ホテル建設への投資が増加し、ポリウレタン(PU)接着剤市場の需要が見込まれます。

- サウジアラビア経済はポスト石油時代を迎えており、現在建設中のメガシティが将来の成長をもたらすと考えられます。産業筋によると、サウジアラビアでは5,200以上の建設プロジェクトが進行中で、その総額は8,190億米ドルに上ります。これらのプロジェクトは、湾岸協力会議(GCC)全体で進行中のプロジェクト総額の約35%を占めています。

- サウジアラビアの主要な都市建設プロジェクトには、アブドラ国王警備施設(フェーズ5)やグランド・モスク(聖ハラーム・モスク拡大工事)などがあります。これらはそれぞれ213億米ドルに相当し、マッカの自治体・農村省が開発しています。

- サウジアラビアの上位建設プロジェクトには、Neom、紅海プロジェクト、Qiddiyaエンターテインメント・シティ、Amaala、Al-UlaのJean Nouvel's Sharaanリゾート、Makkah Grand Mosque-Third Expansion、Jeddah Tower、住宅省のSakani Homes、Jabal Omar、Al Widyan、Riyadh Metroなどがあります。また、リヤド高速バス輸送システム、キング・ファハド・メディカル・シティ拡大工事、キング・アブドラ・ビン・アブドゥルアジーズ・メディカル・コンプレックス、キング・サルマン・エナジー・パーク(スパーク)、Saudi Aramcoのベリとマルジャン、ハナジー・ソーラー・パーク、ドゥマット・アル・ジャンダル風力発電所、Saudi Aramco・トタールのPIB工場、パン・アジアのボトリング施設も含まれます。

- サウジアラビアの「アミッド・ビジョン2030」は、国のインフラを成長させるメガプロジェクトに支えられた重要な開発計画です。環境への取り組み、市民の生活の質の向上、強力な経済の創造に重点を置き、ビジョン2030は変革をもたらすことを目指しています。ビジョン2030とそれに対応する国家変革計画(NTP)の導入により、医療、教育、インフラなどいくつかのセグメントへの投資が拡大しました。

- サウジアラビアでは多くの住宅・商業プロジェクトが開始されており、同国の建設活動の増加が見込まれています。これらのプロジェクトの中には、5,000億米ドルを投じる未来型メガシティ「Neom」プロジェクトや、5つの島に合計3,000室を有する14の豪華・超高級ホテルを含む紅海プロジェクト・フェーズ1(2022年完成予定)などがあります。また、内陸部の2つのリゾート、Qiddi Entertainment City、豪華なウェルネス観光地Amaala、Al-Ulaにあるジャン・ヌーベルのリゾートSharaan、住宅省のSakani homes、Jeddah Towerも含まれます。

- Gulf Council Corporationによると、サウジアラビアは医療施設に664億9,000万米ドルを投資する計画で、2030年までに民間セクターの参加が65%増加すると見込まれています。

- サウジアラビアは中東における新たな自動車ハブとしての地位を確立することに注力しています。サウジアラビアは自動車と自動車部品の大規模な輸入国だが、現在、国内の自動車産業を発展させるため、OEM(相手先商標製品製造)メーカーが王国に生産工場を開設するよう誘致しようとしています。例えば、Renault、Peugeot、Volkswagenなど複数のOEMメーカーがすでにモロッコにユニットを設置しており、大手自動車メーカーはモロッコを費用対効果の高い国と見ています。

- サウジアラビアの医療産業はGCC地域で最大の支出を占めており、病院や長期ケアセンターの増加に対する需要が高まっています。サウジアラビア政府は、2030年までに民間セクターの寄与率を40%から65%に引き上げることを目指しており、290の病院と2300のプライマリーヘルスセンターの民営化を目標としています。

- したがって、こうした動向はすべて、予測期間中に同国のポリウレタン接着剤市場の消費を促進すると予想されます。

中東・アフリカのポリウレタン(PU)接着剤産業概要

中東・アフリカのポリウレタン(PU)接着剤市場は非常にセグメント化されています。同市場の主要企業には、3M、Arkema、Dow、H.B. Fuller、Henkel AG &Co.KGaAなどがあります(順不同)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 建設産業の力強い成長

- 医療インフラの成長

- その他の促進要因

- 抑制要因

- VOC排出に関する厳しい環境規制

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 樹脂タイプ

- 熱硬化性

- 熱可塑性

- 技術

- 水性

- 溶剤系

- ホットメルト

- その他

- エンドユーザー産業

- 自動車と航空宇宙

- 建築・建設

- 電気・電子

- フットウェアと皮革

- 医療

- 包装

- その他

- 地域

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- エジプト

- その他の中東・アフリカ

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア分析**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- 3M

- Arkema

- Avery Dennison Corporation

- Dow

- Dymax

- Franklin International

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- ITW Performance Polymers

- Jowat AG

- MAPEI S.p.A.

- Sika AG

- Wacker Chemie AG

第7章 市場機会と今後の動向

- バイオベース接着剤へのシフト

- 軽量製品製造への傾斜の高まり

目次

The MEA Polyurethane Adhesives Market size is estimated at USD 0.83 billion in 2025, and is expected to reach USD 1.09 billion by 2030, at a CAGR of 5.5% during the forecast period (2025-2030).

The COVID-19 outbreak negatively impacted the market. Stoppage or slowdown of several industrial projects, movement restrictions, production halts, and labour shortages led to a decline in the polyurethane (PU) adhesives market growth. However, it recovered significantly in 2021, owing to rising consumption from various end-use industries, including building and construction, packaging, healthcare, and automotive.

Key Highlights

- Over the short term, increasing demand from the construction industry and healthcare infrastructure are some of the major factors driving the studied market's growth.

- Conversely, stringent environmental regulations regarding VOC emissions are expected to hinder the studied market's growth.

- However, shifting focus towards bio-based adhesives and growing inclination towards manufacturing lightweight products will likely offer opportunities for the PU adhesives market.

- Saudi Arabia dominates the Middle East and Africa PU adhesives market and will also witness the highest CAGR during the forecast period.

MEA Polyurethane (PU) Adhesives Market Trends

Building and Construction Industry Dominates the Market

- Among end-user industries, the building and construction segment dominates the consumption of PU adhesives in the region.

- PU adhesives include rapid curing and low-strength properties, making them an excellent choice for woodworking and other construction applications. They provide the high strength required to hold construction materials together.

- Besides, this material is versatile when it comes to product assembly adhesives. It suits plastics, glass, PVFs, aluminum, stainless steel, and other metals, regardless of the toughness of bond substrates.

- Countries such as Saudi Arabia, Kuwait, Qatar, United Arab Emirates, and Egypt is witnessing strong growth in construction investments and activities. For instance, the sustainable living environment axis in Kuwait Vision 2035 includes five pillars, the most prominent of which is to provide housing care to citizens through what is planned. It is to ensure the provision of 65.5 thousand housing units through five projects costing about KWD 3.22 billion (USD 10.5 billion), the last of which ends by 2029.

- When these projects are implemented, the state will meet approximately 72% of the current housing requests, which are 91,000. The first project of the residential care plan revolves around the vision of Kuwait 2035 (New Kuwait) in the city of Jaber Al-Ahmad, which includes a completion rate of 95% and will complete at the end of 2022. The second project is in Al-Mutla'a, with a completion rate of 64%, to be completed by the end of 2023.

- The third project is in the suburb of South Abdullah Al-Mubarak, which contains a completion rate of 72% and will be completed by the end of 2025. The completion rate in the fourth project, the South Sabah Al-Ahmad, is about 14%, as it is still in the preparation stage and is expected to be completed in 2029. This south of Saad Al-Abdullah includes a completion rate of 13% as it is still in its preparatory phase and ends in 2029. Therefore, the growing residential housing construction in Kuwait is expected to create an upside demand for Kuwait's polyurethane(PU) adhesives market.

- Hence, the growth prospects for the construction industry in such countries are expected to propel the consumption of PU adhesives in the region.

Saudi Arabia to Dominate the Market

- Saudi Arabia holds the largest Middle East and African market share for polyurethane (PU) adhesives. The demand for polyurethane (PU) adhesives is expected to rise throughout the forecast period due to rising investments in construction, healthcare infrastructure, and the efforts to develop automotive hubs in the country. The rise in the population and disposable income increased the demand for better-quality residential building development.

- The Saudi Arabian construction market is expected to witness significant growth and offer lucrative potential due to its Vision 2030, NTP 2020, and several ongoing reforms to diversify away from oil. Vision 2030, NTP 2020, the private sector investment boost, and the ongoing reforms are expected to be the growth drivers for the Saudi polyurethane adhesives market from the country's construction industry during the forecasted period.

- Moreover, under Vision 2030, 80 new hotels with more than 11,000 luxurious rooms will be opened across Saudi Arabia by 2030. Therefore, increasing investments in the construction of hotels is expected to create demand for the polyurethane (PU) adhesives market.

- The country's economy is entering a post-oil era in which the kingdom's mega-cities, which are under construction, will provide future growth. According to industry sources, more than 5,200 construction projects are ongoing in Saudi Arabia at a value of USD 819 billion. These projects account for approximately 35% of the total value of active projects across the Gulf Cooperation Council (GCC).

- Some major urban construction projects in Saudi Arabia include the King Abdullah Security Compounds (Phase 5) and the Grand Mosque (Holy Haram Mosque expansion). Each of these is valued at USD 21.3 billion and developed by the Ministry of Municipalities and Rural Affairs in Makkah.

- The top construction projects in Saudi Arabia include Neom, the Red Sea Project, Qiddiya entertainment city, Amaala, Jean Nouvel's Sharaan resort in Al-Ula, Makkah Grand Mosque - Third Expansion, Jeddah Tower, Ministry of Housing's Sakani Homes, Jabal Omar, Al Widyan, and Riyadh Metro. It also includes Riyadh Rapid Bus Transit System, King Fahd Medical City Expansion, King Abdullah Bin Abdulaziz Medical Complexes, King Salman Energy Park (Spark), Saudi Aramco's Berri and Marjan, Hanergy Solar Park, Dumat Al Jandal Wind Power Plant, Saudi Aramco-Total's PIB factory, and Pan-Asia bottling facility.

- Saudi Arabia's Amid Vision 2030 is a significant development plan supported by megaprojects to grow the nation's infrastructure. With an emphasis on environmental commitments, enhancing citizen quality of life, and creating a strong economy, Vision 2030 aspires to bring about change. Investments in several fields, including healthcare, education, and infrastructure, expanded due to the introduction of Vision 2030 and the corresponding National Transformation Plan (NTP).

- Many residential and commercial projects are being launched in Saudi Arabia, which is anticipated to increase the country's construction activity. Some of these projects are the USD 500 billion futuristic mega-city "Neom" project and the Red Sea Project Phase 1 (due for completion in 2022), which includes 14 luxurious and hyper-luxury hotels that may total 3,000 rooms spread across five islands. It also includes two inland resorts, Qiddi Entertainment City, Amaala - the luxurious wellness tourism destination, Jean Nouvel's Sharaan resort in Al-Ula, the Ministry of Housing's Sakani homes, and Jeddah Tower.

- According to the Gulf Council Corporation, Saudi Arabia planned to invest USD 66.49 billion in healthcare facilities, with help from the private sector, whose participation is expected to rise by 65% by 2030.

- Saudi Arabia is focusing on establishing itself as the new automotive hub in the Middle East. Though the country is a large importer of vehicles and auto parts, it is now trying to attract original equipment manufacturers (OEMs) to open their production plants in the kingdom to develop the domestic auto industry. For instance, several OEM manufacturers such as Renault, Peugeot, and Volkswagen already set up units in Morocco, and major automotive manufacturers see Morocco as a cost-effective country.

- The healthcare industry in Saudi Arabia accounts for the largest expenditure in the GCC region, and there is a rising demand for increasing hospital and long-term care centers. Saudi Arabian Government aims to increase private sector contribution from 40% to 65% by 2030, targeting the privatization of 290 hospitals and 2,300 primary health centers.

- Hence, all such trends are expected to drive the consumption of the polyurethane adhesives market in the country during the forecast period.

MEA Polyurethane (PU) Adhesives Industry Overview

The Middle East and African polyurethane (PU) adhesives market is highly fragmented. Some of the major players in the market include 3M, Arkema, Dow, H.B. Fuller, and Henkel AG & Co. KGaA, amongst others (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Report

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Robust Growth of Construction Industry

- 4.1.2 Growing Healthcare Infrastructure

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations Regarding VOC Emissions

- 4.2.2 Other Restraints

- 4.3 Industry Value-chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Resin Type

- 5.1.1 Thermoset

- 5.1.2 Thermoplastic

- 5.2 Technology

- 5.2.1 Water Borne

- 5.2.2 Solvent-borne

- 5.2.3 Hot Melt

- 5.2.4 Other Technologies

- 5.3 End-user Industry

- 5.3.1 Automotive and Aerospace

- 5.3.2 Building and Construction

- 5.3.3 Electrical and Electronics

- 5.3.4 Footwear and Leather

- 5.3.5 Healthcare

- 5.3.6 Packaging

- 5.3.7 Other End-user Industries

- 5.4 Geography

- 5.4.1 Saudi Arabia

- 5.4.2 United Arab Emirates

- 5.4.3 Qatar

- 5.4.4 South Africa

- 5.4.5 Egypt

- 5.4.6 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Avery Dennison Corporation

- 6.4.4 Dow

- 6.4.5 Dymax

- 6.4.6 Franklin International

- 6.4.7 H.B. Fuller Company

- 6.4.8 Henkel AG & Co. KGaA

- 6.4.9 Huntsman International LLC

- 6.4.10 ITW Performance Polymers

- 6.4.11 Jowat AG

- 6.4.12 MAPEI S.p.A.

- 6.4.13 Sika AG

- 6.4.14 Wacker Chemie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Shifting Focus Towards Bio-Based Adhesives

- 7.2 Growing Inclination Towards Manufacturing of Lightweight Products

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日