|

市場調査レポート

商品コード

1693417

欧州のポリウレタン接着剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Polyurethane Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のポリウレタン接着剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 202 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

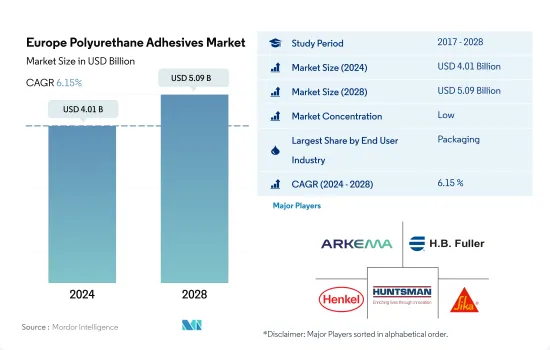

欧州のポリウレタン接着剤市場規模は2024年に40億1,000万米ドルと推定され、2028年には50億9,000万米ドルに達すると予測され、予測期間中(2024-2028年)のCAGRは6.15%で成長すると予測されます。

新興の建設・包装最終用途部門が欧州のポリウレタン接着剤消費を押し上げる見込み

- ポリウレタン接着剤は、飲食品包装、容器包装、機能的バリア用途の最終包装、金属包装などの包装業界で広く使用されています。英国は同国最大の包装市場のひとつです。同国の設計改善と技術革新は、包装用リサイクル可能材料の使用へのシフトと相まって、市場成長のための数多くの機会を提供すると期待されており、その結果、市場に新製品を投入する機会を生み出しています。英国の包装製造業は110億英ポンドの年間売上高を記録しており、これが同地域の包装用接着剤市場を牽引していると思われます。

- 2020年のCOVID-19パンデミックによる景気減速後の欧州連合委員会の復興計画、例えば欧州の建物を環境に優しいものにし、資源の浪費を減らすために建設部門に資金が割り当てられたNext Generation EUなどにより、建設業界におけるポリウレタン接着剤の需要は2021年に飛躍的に伸びた。ポリウレタン建築用接着剤の全体的な需要の伸びは、デンマークなどの北欧諸国が建設生産高で17.8%の伸びを示したため、その他欧州の地域セグメントで2021年に最も高くなりました。

- 欧州では、ドイツが最大のヘルスケア産業を占めています。同国の健康に対する年間支出は、フィットネスとウェルネスを除いて3,750億ユーロ以上と推定されます。人口動態の変化とデジタル化の動向により、ヘルスケア支出は増加を続け、予測期間中、同地域のポリウレタン接着剤市場を牽引すると予想されます。

欧州では建設、包装、自動車産業が増加し、ポリウレタン接着剤の需要を将来的に促進する可能性が高い

- 2017年から2021年の期間において、欧州地域から生み出された需要は全地域の中で2位にランクされました。この地域の自動車、航空宇宙、建築・建設などのエンドユーザー産業の製造能力が高いため、この地域の接着剤需要のシェアは一貫して世界需要の24~25%を占めています。同地域では、ホットメルトや水溶性技術を用いたポリウレタン接着剤が需要の大半を生み出しています。

- 2017年から2019年にかけて、この地域の接着剤需要はCAGR 1.85%で増加しました。ポリウレタン接着剤需要の伸びの鈍化は、この地域における建設活動の伸びの鈍化と自動車生産の減少に起因しています。これらのエンドユーザー産業からの需要は、この期間にそれぞれCAGR 0.44%と-0.50%で減少しました。

- 2020年には、操業、労働力、原材料、サプライチェーン、その他の分野での制約により、地域全体のすべてのエンドユーザーからの需要が減少しました。この地域のすべての国のすべての産業の中で、ドイツの履物産業とフランスの自動車産業が最も大きな打撃を受け、前年同期比数量ベースでそれぞれ37.89%と35.94%減少しました。

- 2021年には、この地域のすべての国からポリウレタン接着剤の需要が回復し始め、2022年には流行前の需要量を上回ると予想されます。イタリアの需要は数量ベースで前年比8.38%増と最も高い伸びを示しました。この成長動向は予測期間中も続くと予想されます。欧州地域全体の需要は、予測期間中にCAGR 3.83%で増加すると予想されます。

欧州のポリウレタン接着剤市場動向

欧州における飲食品産業の著しい成長により包装産業が拡大

- 包装は欧州地域の主要分野の一つです。同地域は世界第2位の包装製品生産国で、アジア太平洋地域に次いで世界の包装生産量の約24%を占めています。ドイツ、ロシア、スペイン、英国は欧州における包装製品の主要生産国です。COVID-19パンデミックの影響により、2020年の包装生産は2019年に比べ7.14%減少したと見られます。この年、いくつかの国によって全国的な封鎖が行われ、この地域の生産設備は3~4ヶ月間停止しました。

- ロシアは包装製品の主要生産国で、2021年には2億1,380万トンを生産し、これは欧州で最高です。ロシアの包装産業は、近年の飲食品産業の急成長によって大きく牽引されてきました。ロシアは世界の食品の主要輸出国であり、様々な最終用途産業にわたる洗練されたパッケージングへのニーズを満たすために、パッケージング販売にさらなる影響を与えています。

- ドイツは欧州におけるプラスチック包装の主要生産国です。プラスチック包装は2021年に生産される包装の約79%を占める。プラスチック包装産業は、主に国内の飲食品産業の急成長によって牽引されています。同地域では、より多忙なライフスタイル、より大きな消費力、および関連要因の増加に伴い、素早く持ち運べるパッケージ製品の需要が増加しています。この動向は、今後数年間、欧州の包装製品で高まると思われます。

新築の急増と改築ニーズの高まりが業界を牽引する

- 2020年の建設業全体の収益は、COVID-19によるパンデミック状況の影響により急減しました。

- 欧州の建設セクター全体の売上高は驚異的な伸びを示し、2021年の前年比成長率は2020年に比べて最も高くなりました。これは、「次世代EU」と名付けられたCOVID復興計画の下、全セクターに7,500億ユーロを投入するなどのEU委員会の取り組みや対策が奏功したためです。ネクストジェネレーションEU計画では、建築物のグリーン化とデジタル化という欧州の目標が既存の建築物や構造物の年間改修率の増加につながったため、建設部門が最大の投資を受けました。

- EUROCONSTRUCTの報告書によると、EUの政治的地域に基づくセグメントのうち、中東欧のCAGRは6.4%、次いで西欧のCAGRは6.1%と予想されています。

- 欧州連合(EU)および国家レベルの政策立案者は、「建物のエネルギー性能に関する指令(Energy Performance of Buildings Directive)」をはじめとするさまざまな政策を通じて、新しい建物の建設や既存の建物のエネルギー効率化を優先しています。こうした政策により、予測期間中の建設全体の収益が増加することになります。

欧州のポリウレタン接着剤産業の概要

欧州のポリウレタン接着剤市場は細分化されており、上位5社で25.72%を占めています。この市場の主要企業は以下の通り。 Arkema Group, H.B. Fuller Company, Henkel AG & Co. KGaA, Huntsman International LLC and Sika AG(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 履物・皮革

- 包装

- 木工・建具

- 規制の枠組み

- EU

- ロシア

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- 履物・皮革

- ヘルスケア

- 包装

- 木工・建具

- その他のエンドユーザー産業

- テクノロジー

- ホットメルト

- 反応性

- 溶剤系

- UV硬化型接着剤

- 水系

- 国名

- フランス

- ドイツ

- イタリア

- ロシア

- スペイン

- 英国

- その他欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- 3M

- Arkema Group

- Beardow Adams

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Jowat SE

- MAPEI S.p.A.

- Sika AG

- Soudal Holding N.V.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の接着剤とシーラント産業の概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、抑制要因、機会

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 92476

The Europe Polyurethane Adhesives Market size is estimated at 4.01 billion USD in 2024, and is expected to reach 5.09 billion USD by 2028, growing at a CAGR of 6.15% during the forecast period (2024-2028).

Emerging construction and packaging end-use sector expected to boost the consumption of polyurethane adhesives in Europe

- Polyurethane adhesives are widely used in the packaging industry for food and beverage packaging, container packaging, end-of-line packaging for functional barrier applications, and metal packaging. The United Kingdom is one of the largest packaging markets in the country. The country's designed improvements and innovation, combined with a shifting focus toward the usage of recyclable materials for packaging, are expected to offer numerous opportunities for market growth, thus, creating opportunities for the launch of new products into the market. The UK packaging manufacturing industry records annual sales of GBP 11 billion, which is likely to drive the market for packaging adhesives in the region.

- The demand for polyurethane adhesives in the construction industry grew tremendously in 2021 because of the European Union's Commission's recovery plan post an economic slowdown due to the COVID-19 pandemic in 2020, such as Next Generation EU in which a fund has been allocated for the construction sector to make European buildings environmentally benign and reduce the wastage of resources. The overall growth in demand for polyurethane construction adhesives was the highest in 2021 for the Rest of Europe regional segment because of the Nordic countries, such as Denmark, which witnessed a 17.8% growth in their construction output.

- In Europe, Germany accounts for the largest healthcare industry. The annual expenditure on health in the country is estimated to be more than EUR 375 billion, excluding fitness and wellness. Owing to its demographic changes and digitalization trends, healthcare expenditure is expected to continue rising and drive the polyurethane adhesives market in the region over the forecast period.

Rising construction, packaging and automotive industries in Europe likely to propel the demand for polyurethane adhesives in the future

- In the period 2017 to 2021, the demand generated from the Europe region ranked 2rd among all regions. The share of adhesive demand from this region has consistently occupied 24-25% of the global demand because of the high manufacturing capacity of end-user industries, like automotive, aerospace, building and construction, and other industries in the region. Polyurethane adhesives with hot melt and water-borne technologies generate most of the demand in the region.

- From 2017 to 2019, the demand for adhesives from this region increased with a CAGR of 1.85%. The slow growth in the demand for polyurethane adhesives has resulted in slow growth in construction activities and a decrease in Automotive production in the region. The demand from these end-user industries declined with a CAGR of 0.44% and -0.50%, respectively, during this period.

- In 2020, due to constraints in operations, labor, raw material, supply chain, and other areas, the demand from all end users across the region declined. Among all Industries from all countries in the region, the footwear industry in Germany and the automotive industry in France took the worst hit, declining by 37.89% and 35.94%, respectively, in Y-o-Y volume terms.

- In 2021, the demand for polyurethane adhesives started to recover from all countries in the region and is expected to outgrow pre-pandemic demand volume by 2022. The demand from Italy has witnessed the highest Y-o-Y growth of 8.38% in volume terms. This growth trend is expected to continue during the forecast period. The overall demand from the Europe region is expected to increase with a CAGR of 3.83% during the forecast period.

Europe Polyurethane Adhesives Market Trends

Significant growth of food & beverage industry in Europe to escalate packaging industry

- Packaging is one of the major sectors of Europe region. The region is the second-largest producer of packaging products in the world, which holds about 24% of global packaging production after the Asia-Pacific region. Germany, Russia, Spain, and the United Kingdom are major producers of packaging products in Europe. It is seen that packaging production reduced by 7.14% in 2020 compared to 2019 due to the impact of the COVID-19 pandemic. During the year, a nationwide lockdown imposed by several countries halted the production facilities for three to four months in the region.

- Russia is a leading producer of packaging products producing 213.8 million tons in 2021, which is the highest in Europe. The Russian packaging industry has majorly been driven by the rapid growth of the food and beverages industry in recent years. Russia is a major exporter of food products worldwide, which further influences packaging sales to meet the need for sophisticated packaging across various-end use industries.

- Germany is the major producer of plastic packaging in Europe. Plastic packaging which nearly accounts for around 79% of the packaging produced in 2021. The plastic packaging industry is majorly driven by the rapid growth of the food and beverages industry in the country. With the rise in busier lifestyles, greater spending power, and related factors in the region, the demand for quick and on-the-go packaged products is increasing. This trend will rise in packaging products in the coming years in Europe.

Rapid growth of new construction along with rising need for renovation activities will drive the industry

- The overall revenue of construction showed a steep decrement in 2020 because of the impact of the pandemic situation due to COVID-19, which led to an overall recovery slowdown and social distancing measures on work sites.

- The overall revenue of the construction sector in Europe grew tremendously, with the highest year-on-year growth in 2021 compared to that of 2020 because of the initiatives and measures taken by the EU Commission, such as the infusion of EUR 750 billion for all sectors under the COVID recovery plan named Next Generation EU. Under the Next Generation EU plan, the construction sector received the maximum investment because of the European objective of green and digital transition in buildings which led to growth in the annual renovation rate of existing buildings and structures.

- As per the EUROCONSTRUCT report, among the segments of the European Union based on political geography, Central and Eastern Europe are expected to register a CAGR of 6.4%, followed by Western Europe at a CAGR of 6.1% in 2022-2024.

- The policymakers at European Union and national level are prioritizing the construction of new buildings and conversion of existing buildings to be energy efficient through various policies including Energy Performance of Buildings Directive and others. These policies will lead to an increase in overall revenue for construction in the forecast period.

Europe Polyurethane Adhesives Industry Overview

The Europe Polyurethane Adhesives Market is fragmented, with the top five companies occupying 25.72%. The major players in this market are Arkema Group, H.B. Fuller Company, Henkel AG & Co. KGaA, Huntsman International LLC and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Footwear and Leather

- 4.1.5 Packaging

- 4.1.6 Woodworking and Joinery

- 4.2 Regulatory Framework

- 4.2.1 EU

- 4.2.2 Russia

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Packaging

- 5.1.7 Woodworking and Joinery

- 5.1.8 Other End-user Industries

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Solvent-borne

- 5.2.4 UV Cured Adhesives

- 5.2.5 Water-borne

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Russia

- 5.3.5 Spain

- 5.3.6 United Kingdom

- 5.3.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 Beardow Adams

- 6.4.4 H.B. Fuller Company

- 6.4.5 Henkel AG & Co. KGaA

- 6.4.6 Huntsman International LLC

- 6.4.7 Jowat SE

- 6.4.8 MAPEI S.p.A.

- 6.4.9 Sika AG

- 6.4.10 Soudal Holding N.V.

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms