中国の発電:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

China Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 95 Pages

- 納期

- 2~3営業日

- 商品コード

- 1637883

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

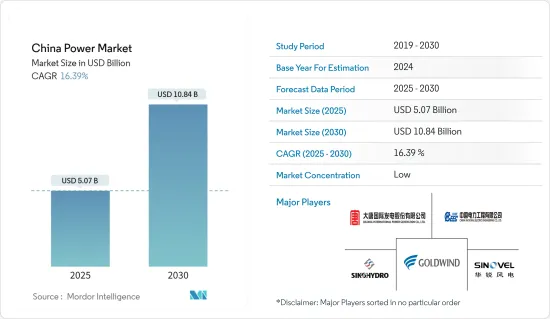

中国の発電市場規模は2025年に50億7,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは16.39%で、2030年には108億4,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、今後の投資の増加や製造業の成長といった要因が、予測期間中の中国の発電市場を牽引すると考えられます。

- その一方で、中国の発電量の大部分を占める石炭ベースの発電所の段階的廃止は、発電市場の成長を妨げると予想されます。

- 中国政府は2030年までに再生可能エネルギーの導入量を1200GWまで増やすと発表しました。これは、予測期間中、中国の発電市場にいくつかの機会をもたらすと考えられます。

中国の発電市場の動向

再生可能エネルギーセグメントが市場を独占する見込み

- 中国政府は、補助金、減税、規制など様々な施策とインセンティブを通じて、再生可能エネルギー開発を積極的に推進しています。こうした政府の支援は再生可能エネルギーセグメントの成長を後押しし、今後も続くと予想されます。

- さらに、中国はエネルギー需要を満たすために輸入化石燃料に大きく依存しています。そのため、価格変動や供給途絶の影響を受けやすいです。再生可能エネルギーに投資することで、中国は外国のエネルギー源への依存を減らし、エネルギー安全保障を高めることができます。

- さらに、再生可能エネルギーのコストは近年急速に低下しており、化石燃料との競合はますます激しくなっています。場合によっては、再生可能エネルギーはすでに石炭火力発電所よりも安くなっています。このコスト競合は、エネルギーコストの削減を目指す中国にとって、再生可能エネルギーを魅力的な選択肢にしています。

- 2022年、中国の再生可能エネルギー発電量は約1367TWhでした。2021年と比較して19%の増加です。予測期間中も同様の傾向が続くと予想されます。

- 例えば、2022年3月、中国政府はゴビ砂漠などの砂漠地帯に450GWの太陽光・風力発電容量を建設する意向であると発表しました。現在、約100GWの太陽光発電容量がすでに建設中です。

- 国家エネルギー局(NEA)によると、中国は2022年に3,260万kWの陸上風力発電容量を接続し、総設備容量を3億3,398万kWに引き上げます。さらに、中国の陸上風力発電市場は、国内市場向けと国際輸出向けの主要部品や材料のニーズが高まっており、今後数年間は安定した成長が見込まれています。また、中国では発電量の70%近くが火力発電です。火力発電による公害が増加する中、同国は発電におけるよりクリーンで再生可能な電源の割合を増やすことに注力しています。

今後の投資計画の増加が市場を牽引

- 世界第2位の経済大国である中国のエネルギー需要は、経済開発目標を達成するために急成長しました。人口の増加、都市化、工業化がこの需要に貢献し、発電能力の必要性が高まっている

- 2022年、中国の総発電量は8,848.7TWhとなり、2021年比で約3.6%増加しました。この傾向は、中国が再生可能エネルギー容量を増やすにつれて続くと予想されます。それは発電能力の増加を助けると考えられます。

- さらに、世界原子力協会によると、中国には現在55基の稼働中の原子炉があり、さらに22基が建設中または開発中です。中国政府は、石炭火力発電所による汚染への懸念もあり、エネルギー需要を満たすため、長期的に閉鎖サイクル原子力の利用を増やすことを目指しています。

- 2022年4月、中国国務院は6基の新規原子力発電所建設にゴーサインを出し、三門、海陽、禄豊の各原子力発電所敷地内に2基の原子炉を追加建設する計画を示しました。建設が承認されたのは、三門の3号機と4号機、海陽の3号機と4号機、禄豊の5号機と6号機です。この動きにより、中国の原子力発電設備容量は2025年までに70GWeに増加すると予想されます。

- さらに、ロシア・ウクライナ戦争のような最近の地政学的動向により、中国政府はエネルギー安全保障の強化に重点を移しました。ロシアとウクライナの戦争のような最近の地政学的な動きにより、中国政府はエネルギー安全保障の強化に重点を置くようになりました。石油・ガスの供給は世界的に影響を受け、中国の発電セクターも影響を受けました。

- 中国は、発電セクターの他のセグメントのアップグレードにも多額の投資を行っています。これには、再生可能な発電を小規模な発電事業から需要センターまで輸送するための主要なHVDCとUHVDCプロジェクトにおける送電と配電インフラ、送電網を安定させながら余剰の再生可能エネルギー発電を貯蔵するためのバッテリー貯蔵容量が含まれます。

- 例えば、2022年7月に白河灘-江蘇800kV超高圧(UHV)直流送電プロジェクトが商業運転を開始したが、これは大規模な西から東への送電計画における主要プロジェクトの一つです。このような開発は、大規模ソーラーパークからの配電に役立つと期待されています。

- したがって、上記のような点から、中国政府は同国のエネルギー部門への投資を増やし、同国の発電市場を拡大することが期待されます。

中国の発電産業概要

中国の発電市場は細分化されています。同市場の主要企業(順不同)には、Datang International Power Generation Company Limited、China National Electric Engineering、Xinjiang Goldwind Science &Technology、Sinohydro Corporation、Sinovel Wind Groupなどが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 中国の発電量と2028年までの予測(単位:テラワット)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 再生可能エネルギーセグメントへの投資の増加

- 製造業の成長による発電需要の増加

- 抑制要因

- 石炭発電所の段階的廃止の増加

- 促進要因

- サプライチェーン分析

- PESTLE分析

第5章 市場セグメンテーション

- 発電源

- 火力

- 水力発電

- 原子力

- 再生可能エネルギー

- その他の発電源

- 送配電(T&D)

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Datang International Power Generation Company Limited

- China National Electric Engineering Co. Ltd

- Xinjiang Goldwind Science & Technology Co. Ltd

- Sinohydro Corporation

- Sinovel Wind Group Co. Ltd.

- Wuxi Suntech Power Co. Ltd.

- China Yangtze Power Co., Ltd.

- China National Electric Wire & Cable I/E Corp.

- State Grid Corporation of China

- Shandong energy group co. Ltd.

第7章 市場機会と今後の動向

- 再生可能エネルギー発電を支援する政府目標の存在

目次

The China Power Market size is estimated at USD 5.07 billion in 2025, and is expected to reach USD 10.84 billion by 2030, at a CAGR of 16.39% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the increasing upcoming investments and the growing manufacturing sector will likely drive the Chinese power market during the forecast period.

- On the other hand, phasing out coal-based power plants, which account for a major share of power generation in China, is expected to hinder the growth of the power market.

- Nevertheless, the Chinese government announced increasing its installation of renewable energy sources to 1200 GW by 2030. It will likely create several opportunities for the Chinese power market in the forecast period.

China Power Market Trends

The Renewable Energy Segment Expected to Dominate the Market

- The Chinese government actively promoted renewable energy development through various policies and incentives, such as subsidies, tax breaks, and regulations. This government support helped to drive growth in the renewable energy sector and is expected to continue in the coming years.

- Moreover, China heavily relies on imported fossil fuels to meet its energy needs. It makes the country vulnerable to price fluctuations and supply disruptions. By investing in renewable energy, China can reduce its dependence on foreign energy sources and increase its energy security.

- Additionally, the cost of renewable energy has decreased rapidly in recent years, making it increasingly competitive with fossil fuels. In some cases, renewable energy is already cheaper than coal-fired power plants. This cost competitiveness makes renewable energy an attractive option for China, which aims to reduce its energy costs.

- In 2022, the electricity generated through renewable energy in China was around 1367 TWh. It is an increase of 19% compared to 2021. A similar trend is expected to be followed during the forecasted period.

- For instance, in March 2022, it was announced by the Chinese government that they intend to construct solar and wind power generation capacity of 450 GW in desert regions such as the Gobi desert. Currently, around 100 GW of solar power capacity is already under construction.

- According to the National Energy Administration (NEA), China connected 32.6 GW of onshore wind capacity in 2022, boosting its total installations to 333.98 GW. Further, the Chinese onshore wind market is expected to grow steadily in the coming years, with rising needs for key components and materials for the national market and international exports. Besides, in China, nearly 70% of the electricity produced is from thermal energy sources. With increasing pollution from thermal sources, the country focuses on increasing the share of cleaner and renewable sources in power generation.

Increasing Upcoming Investment Plans to Drive the Market

- As the world's second-largest economy, China's energy demand grew rapidly to meet its economic development goals. A growing population, urbanization, and industrialization contributed to this demand, increasing the need for electricity generation capacity.

- In 2022, the total electricity generated in China was 8848.7 TWh, an increase of almost 3.6% compared to 2021. This trend is expected to continue as China increases its renewable energy capacity. It will aid in increasing electricity generation capacity.

- Moreover, according to the World Nuclear Association, China currently contains 55 operational nuclear power reactors, with 22 more under construction or development. The Chinese government aims to increase its use of closed-cycle nuclear power in the long term to meet its energy demands, partly due to concerns over the pollution caused by coal-fired power plants.

- In April 2022, China's State Council gave the green light to construct six new nuclear power plants, with plans to build two additional reactors at the Sanmen, Haiyang, and Lufeng nuclear power plant sites. The approved construction involves units 3 and 4 at Sanmen, 3 and 4 at Haiyang, and 5 and 6 at Lufeng. This move is expected to increase China's installed nuclear-generating capacity to 70 GWe by 2025.

- Additionally, the Chinese government shifted its focus on increasing energy security due to recent geopolitical developments like the Russia-Ukraine war. It affected the oil and gas supply globally and China's electricity sector, as the country heavily relies on imported fossil fuels for power generation.

- China is also investing heavily in upgrading other segments of its power sector. It includes transmission and distribution infrastructure in major HVDC and UHVDC projects for transporting renewable electricity from small utility-scale energy projects to demand centers and battery storage capacity to store excess renewable generation while stabilizing the grid.

- For instance, in July 2022, the Baihetan-Jiangsu 800 kV ultra-high-voltage (UHV) direct current power transmission project entered commercial operation, one of the key projects in the larger West-to-East power transmission program. Such developments are expected to help the electricity distribution from utility-scale solar parks.

- Therefore, due to the points mentioned above, the government of China is expected to increase investment in the country's energy sector, which will increase the country's power market.

China Power Industry Overview

The Chinese power market is fragmented. The key players in the market (in no particular order) include Datang International Power Generation Company Limited, China National Electric Engineering Co. Ltd, Xinjiang Goldwind Science & Technology Co. Ltd, Sinohydro Corporation, and Sinovel Wind Group Co. Ltd, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 China Power Generation and Forecast, in Terawatt, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Upcoming Investments in Renewable Energy Sector

- 4.5.1.2 Growing Manufacturing Sector Increases Demand For Power

- 4.5.2 Restraints

- 4.5.2.1 Rising Phase Out of Coal-based Power Plants

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

5 MARKET SEGMENTATION

- 5.1 Power Generation Source

- 5.1.1 Thermal

- 5.1.2 Hydroelectric

- 5.1.3 Nuclear

- 5.1.4 Renewable

- 5.1.5 Other Power Generation Sources

- 5.2 Power Transmission and Distribution (T&D)

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Datang International Power Generation Company Limited

- 6.3.2 China National Electric Engineering Co. Ltd

- 6.3.3 Xinjiang Goldwind Science & Technology Co. Ltd

- 6.3.4 Sinohydro Corporation

- 6.3.5 Sinovel Wind Group Co. Ltd.

- 6.3.6 Wuxi Suntech Power Co. Ltd.

- 6.3.7 China Yangtze Power Co., Ltd.

- 6.3.8 China National Electric Wire & Cable I/E Corp.

- 6.3.9 State Grid Corporation of China

- 6.3.10 Shandong energy group co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Presence of Government Targets to Support Renewable Energy Generation

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 95 Pages

- 納期

- 2~3営業日