|

市場調査レポート

商品コード

1910864

電力:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 電力:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 260 Pages

納期: 2~3営業日

|

概要

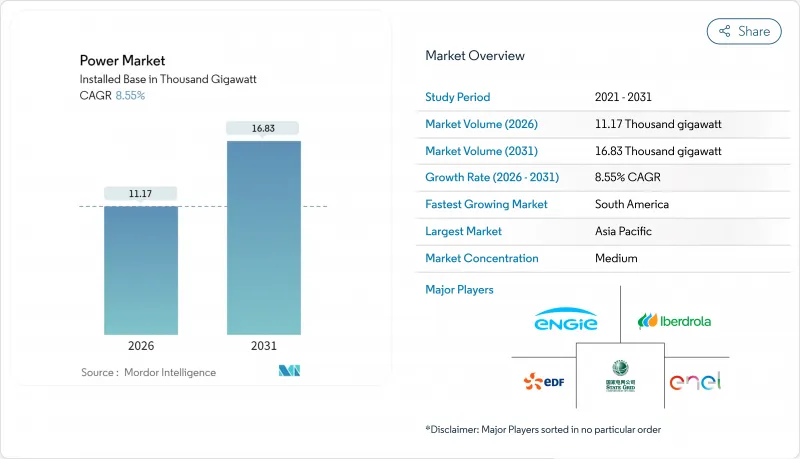

電力市場は2025年に1万290ギガワットと評価され、2026年の1万1,170ギガワットから2031年までに1万6,830ギガワットに達すると予測されています。

予測期間(2026年~2031年)におけるCAGRは8.55%と見込まれます。

容量増加の背景には、データセンターの拡張、産業の電化、グリーン水素の早期導入による電力需要の急増があります。新規容量のほぼ半分を再生可能エネルギーが占め、バッテリー貯蔵コストの急激な低下により数時間にわたる系統柔軟性が実現される恩恵を受けています。政府系ファンドや年金基金は、高電圧送電網のアップグレードに年間1,800億米ドルを継続的に投入しており、送電セグメントにおける競合を激化させています。一方で、送電網のボトルネックや許可手続きの遅延により、承認済みクリーンエネルギープロジェクトの23%が停滞する恐れがあり、発電目標とインフラ整備の間にミスマッチが生じていることが明らかになっています。

世界の電力市場の動向と洞察

爆発的に増加するデータセンターの電力需要

2024年、データセンターの電力消費量は460テラワット時(TWh)に達し、アルゼンチンの年間総消費量に匹敵し、世界の電力消費量の2%を占めました。ハイパースケール施設の平均継続電力消費量は100~200メガワット(MW)に達し、電力会社は系統連系ルールの再交渉や変電所アップグレードの迅速化を迫られています。2024年には、テクノロジー大手企業が従来の電力供給モデルを回避し、24時間365日の再生可能エネルギー確保を図る中、企業バイヤーによるクリーンエネルギー契約量は23.7ギガワットに達しました。バージニア州の「データセンター・アレイ」は既に州内発電量の25%を消費しており、規制当局は容量市場参加規則の見直しを迫られています[PJM.com]。こうした集中負荷は電圧安定性のリスクを高め、小売料金に転嫁されるプレミアム容量契約価格を押し上げています。したがって、世界の電力市場は10年前には珍しかった地域的なベースロード急増を軸に再調整が進んでいます。

産業用熱・輸送の電化

2024年には新規鉄鋼生産能力の73%を電気アーク炉が占め、欧州の産業用熱源改修では40%でヒートポンプが天然ガスに取って代わりました。モビリティ分野では、1,410万台のEVが85TWhの純需要を追加した一方で、280GWhのV2G貯蔵を提供し、夕方のピーク削減に貢献しました。北欧の送電網はこの融合を実証しています。同期化されたEV充電と産業用ヒートポンプのサイクルが時間バンドル型の消費ピークを生み出し、細分化された料金信号とAIベースのディスパッチによってバランスが取られています。アルミニウム精錬所や化学コンビナートは、安価で安定供給可能な再生可能エネルギーを確保するため、既に風力資源が豊富な地域へ移転を進めております。これにより15~20年にわたる電力購入契約が締結され、地域の送電網拡張を支えております。同様の動きが世界的に広がる中、世界の電力市場では産業用電力消費が15~20%持続的に増加すると予測され、年間450億米ドル規模の配電網強化が求められております。

送電網のボトルネックと認可遅延

送電制約により、2024年には建設準備完了済みの再生可能エネルギー127GWが保留状態となり、3,400億米ドルの投資遅延が発生しました。米国の系統連系待ち容量は2,600GWに膨れ上がり、現行送電網容量の5倍に達し、平均審査期間は5.2年に延長しています。欧州の越境送電線は風力発電が活発な時間帯に95%の稼働率を示し、特にスペインとドイツにおいて47TWhの出力抑制を余儀なくされました。政策立案者はこれに対し、EUネットゼロ産業法に基づき事前区域指定済みプロジェクトの審査期間を12ヶ月に制限する措置を講じましたが、地域住民の反対により依然として高圧直流送電設備(HVDC)建設の4件に1件が遅延しています。これらのボトルネックが解消されない場合、資本の先送りや投資家信頼の低下を招き、世界の電力市場の脱炭素化プロセスを阻害する恐れがあります。

セグメント分析

再生可能エネルギーは2025年の設備容量の47.95%を占め、2031年まで年平均CAGR13.70%で拡大しています。これは年間で過去最高の太陽光346GW、風力116GWの新規導入が支えています。洋上風力は23.10%のCAGRで成長し、浮体式基礎により深海域サイトを獲得、日本、韓国、カリフォルニアでの導入が加速しています。同時に、原子力発電所の再稼働と小型モジュール炉(SMR)の試験導入は、産業用熱供給契約を支える堅牢な低炭素電源として、初期段階ながら戦略的な選択肢を追加します。石炭・石油火力発電所は引き続き廃止または改修が進み、2024年には47GWの石炭火力発電所が水素混焼への転換を発表しましたが、商業的実現可能性は依然として炭素価格がトン当たり80米ドルを超えることが条件となります。

再生可能エネルギーの普及率上昇に伴い、計画は柔軟性資産へ重点を移します。2026年から2031年にかけて、世界中の送電網運営者は蓄電池、揚水発電、デマンドレスポンス、送電網接続設備の拡充に累計2兆8,000億米ドルの投資を必要とします。蓄電池の統合により太陽光発電の昼間過剰供給が緩和される一方、国境を越えた高圧直流送電(HVDC)リンクが余剰風力を負荷中心地へ輸送します。これらの手段が拡大するにつれ、世界の電力市場は単一燃料の支配ではなく、多様な資源構成によるレジリエンスを組み込んでいきます。したがって、再生可能エネルギーの急成長は、世界の電力システム全体における資本配分、規制枠組み、および市場価格形成を再定義するものです。

本電力市場レポートは、電源別(火力、原子力、再生可能エネルギー)、エンドユーザー別(電力会社、商業・産業、住宅)、地域別(北米、欧州、アジア太平洋、南米、中東・アフリカ)に分類されています。市場規模と予測は、設置容量(GW)単位で提供されます。

地域別分析

アジア太平洋地域は2025年に44.20%の容量シェアで世界電力市場を牽引し、中国(1,411GW)とインド(425GW)が中核をなしています。中国は年間で216GWの新規再生可能エネルギー設備を稼働させ、ドイツの既存設備総量を上回りましたが、同時にグリッド慣性を確保するため47GWの石炭火力も追加しました。一方、インドは太陽光発電の拡大目標と並行して、2026年までに50GWhの蓄電容量を目指す地域別蓄電池入札を実施しています。日本と韓国は輸入燃料依存度低減のため、洋上風力と先進的原子力発電に注力。日本は2040年までに洋上風力45GW達成を計画し、韓国は12GW規模の浮体式太陽光発電の実証を進めています。地域統合の課題は依然深刻で、中国北西部では送電網の制約により再生可能エネルギーの抑制率が8.2%を超え、省間間接送電(HVDC)ラインの緊急性を浮き彫りにしています。

南米は世界電力市場で最も急速に拡大する地域として浮上し、CAGR15.10%を記録しました。チリのグリーン水素ハブや、アルゼンチン・ブラジルにおけるリチウム電池を活用した系統連系型蓄電需要が牽引役です。ブラジルは195ギガワットの設備容量を誇り、低コストの風力・水力を活用して鉱業や農業の脱炭素化を推進しています。チリのアタカマ砂漠における太陽光発電ブームは、鉱業需要と水素輸出ターミナルの両方に電力を供給し、30米ドル/MWh未満の均等化発電原価を達成しています。再生可能エネルギーに加え、アルゼンチンのバカ・ムエルタ頁岩ガスは、変動性が高まる発電設備を安定化させる堅調な容量増加を支えています。アンデスー太平洋高圧直流送電線を含む国境を越えた連系線は、雨季と乾季における水力発電の最適化を図る地域間取引を実現しています。

欧州は2025年時点で世界の設備容量の22.80%を維持し、2022年のガス危機後、柔軟性とエネルギー安全保障の強化に注力しました。ドイツは17GWの再生可能エネルギーを導入し、周波数調整には北欧の水力発電とフランスの原子力発電の輸入に依存しました。英国は3.2GWの洋上風力を追加し、浮体式基礎技術における主導的地位を確固たるものにしました。しかし成熟した送電網は飽和状態に直面しており、電力価格がマイナスとなる時間帯が増加、蓄電の経済性が向上、卸電力市場では決済期間を5分単位に再構築する動きが急ピッチで進んでいます。北米および中東・アフリカ地域はシェアでは遅れをとっていますが、有望な成長地域として位置づけられています。米国は2024年、IRA税制優遇措置に支えられ32GWの再生可能エネルギーを導入。UAEは2071年ネットゼロ計画に5.6GWの太陽光発電を組み込みました。このように地域分散化が進むことで、世界の電力市場は特定地域における政策や資源のショックから守られるのです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3か月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- データセンターの電力需要が急増

- 産業用熱および輸送の電化

- 政府によるクリーンエネルギー補助金政策の流れ(IRA、REPowerEUなど)

- ユーティリティ規模の蓄電池における急速なコスト低下

- 国境を越えたHVDCスーパーグリッドの構築

- グリーン水素電解装置の増設がベースロード需要を押し上げる

- 市場抑制要因

- 送電網のボトルネックと許可手続きの遅延

- 重要鉱物のサプライチェーン変動性

- 飽和状態の電力網における再生可能エネルギーの抑制増加

- 気候変動による水力発電の変動性

- サプライチェーン分析

- 規制情勢

- 技術展望(スマートグリッド、BESS、AIを活用したディスパッチ)

- 再生可能エネルギー構成の概要(2024年)

- 設置済み発電容量見通し(GW)

- 発電見通し(TWh)

- 一次エネルギー消費量の動向(Mtoe)

- ポーターのファイブフォース

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 発電源別

- 火力(石炭、天然ガス、石油、ディーゼル)

- 原子力

- 再生可能エネルギー(太陽光、風力、水力、地熱、バイオマス・廃棄物、潮力)

- エンドユーザー別

- 公益事業

- 商業・産業用

- 住宅用

- 輸送・配電電圧レベル別(定性分析のみ)

- 高電圧送電(230kV以上)

- 送電網(69~161kV)

- 中電圧配電(13.2~34.5 kV)

- 低電圧配電(1kV以下)

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- 北欧諸国

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- オーストラリア

- その他アジア太平洋

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- エジプト

- その他中東・アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動き(M&A、合弁事業、資金調達、電力購入契約)

- 市場シェア分析(主要企業の市場順位・シェア)

- 企業プロファイル

- State Grid Corporation of China

- Engie SA

- Enel SpA

- Tokyo Electric Power Co. Holdings

- NTPC Ltd

- Dominion Energy

- China Huaneng Group

- Duke Energy

- E.ON SE

- Siemens Energy

- Hitachi Energy

- Electricite de France(EDF)

- Iberdrola SA

- Korea Electric Power Corp.(KEPCO)

- NextEra Energy

- Southern Company

- Exelon Corporation

- China Three Gorges Corp.

- Orsted A/S

- RWE AG

- General Electric Vernova

- Mitsubishi Electric