|

市場調査レポート

商品コード

1636487

中東・アフリカの電気自動車用バッテリー電解液の市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Middle East And Africa Electric Vehicle Battery Electrolyte - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東・アフリカの電気自動車用バッテリー電解液の市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

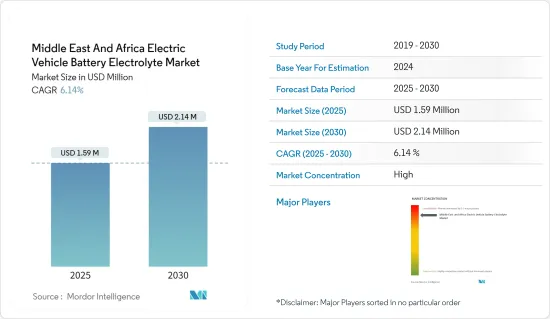

中東・アフリカの電気自動車用バッテリー電解液市場規模は、2025年に159万米ドルと推定され、予測期間(2025~2030年)のCAGRは6.14%で、2030年には214万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、中東地域では政府の施策や関連投資により電気自動車の普及が進んでおり、市場を牽引するとみられます。

- 一方、電気自動車用バッテリーや原料の輸入依存度が高いことが市場成長の妨げになる可能性が高いです。

- セパレーター材料の継続的な研究開発は、市場に将来の成長機会をもたらすと予想されます。

- 調査期間中、中東・アフリカ電気自動車用バッテリー電解液の最大市場は南アフリカになると予想されます。

中東・アフリカの電気自動車用バッテリー電解液市場動向

リチウムイオンバッテリーセグメントが大きなシェアを占める

- リチウムは電気自動車(EV)用バッテリーの製造において重要な役割を果たしています。充電可能なリチウムイオンバッテリーの主要成分であるリチウムの高いエネルギー密度は、走行距離の延長を容易にします。最近、中東・アフリカではリチウムイオンバッテリーの製造と研究が急増しており、電解液などのバッテリー部品への関心が高まっている

- 例えば、2023年7月、カタール大学の先端材料センター(CAM)は、有名な世界的機関と協力して、海水からのリチウム抽出に革命を起こしました。この画期的な技術は、クリーンエネルギーに対する需要の高まりに対応し、持続可能性を促進することを約束するものです。

- 2024年7月、エジプトのRaya Autoは、バッテリー生産と車両電化に特化した新興企業であるシフトEVと戦略的提携を結びました。この提携の下、シフトEVはRaya Autoの軽電動車シリーズに電力を供給するため、現地製のリチウムイオンバッテリーを供給します。このような取り組みは、中東全域で予想されるリチウムバッテリーの需要増に合わせて、電解液市場を強化する構えです。

- 同様に、中東・アフリカでリチウムイオン探査プロジェクトが拡大するにつれて、バッテリー生産における電解液の需要も増加します。2024年6月、EV Metals Group plcは、サウジアラビアのバルサガ・リチウムプロジェクトでの探鉱を終了しました。ジッダの東450km、アラビアン・シールド南東部に位置するこのプロジェクトは、1,200平方キロメートルに及ぶ13の鉱区にまたがっています。これにより、サウジアラビアのリチウムバッテリー製造の展望が強化され、電解液需要が増加し、予測期間中の市場成長に影響を与える可能性が高いです。

- 歴史的に、リチウムイオンバッテリーの価格は急落しており、電解液のような関連部品の需要に拍車をかけています。Bloomberg NEFによると、2023年のリチウムイオンバッテリーの平均価格は139米ドル/kWhで、2014年から5倍下落しました。したがって、価格下落に伴いリチウムイオンバッテリーの採用が急増すれば、電解液市場は利益を得ることになります。

- 前述のようなリチウムイオンバッテリーと電解液生産の動向を踏まえると、中東・アフリカの電気自動車用バッテリー電解液市場は成長が見込まれます。

南アフリカが市場を独占する可能性が高い

- 2023年12月、南アフリカ政府は国内の自動車部門が2026年までに電気自動車(EV)をデビューさせる計画を発表しました。低炭素で気候変動に強い経済の育成を目指す南アフリカのJust Energy Transition(JET)戦略の中心は、輸送の電化に重点を置くことです。JETの枠組みでは、2023~2027年までの期間に約68億4,000万米ドルという多額の投資が必要とされています。

- 2024年2月、南アフリカ政府は国内のEV生産を強化するための税制優遇措置を打ち出しました。この優遇措置は、製造企業に対して150%の税額控除を提供するものです。このような優遇措置は、EV生産の拡大に熱心なFord Motor CompanyやVolkswagenAGのような産業大手に特に有利です。その結果、EVの生産台数は増加し、南アフリカではEV用バッテリーや関連部品(特に電解液)の需要が高まっている

- 2024年7月、中国の著名な電気自動車メーカーであるBYDは、公共交通の電化という世界のビジョンに沿って、南アフリカで電気バスの初受注を確保しました。163年の歴史を持つ南アフリカのバス運行会社、Golden Arrowは、この新エネルギー車(NEV)メーカーと協力し、120台の電気バスを発注しました。南アフリカが電気バスを採用するにつれて、この勢いは市場の予測期間中、バッテリー製造に不可欠な電解液の生産を増加させると予想されます。

- さらに、南アフリカでは近年、電気自動車の導入が顕著に増加しています。国際エネルギー機関のデータによると、インドの電気自動車販売台数は2023年に1,080台に達し、前年比74%増という驚異的な急増を記録しました。このような軌跡を踏まえると、南アフリカの電気自動車需要は回復基調にあり、電解液市場をさらに活性化させると考えられます。

- このような動向を踏まえると、電気自動車とそのバッテリーの採用が増加し、電解液の製造が強化されることになります。このように、中東・アフリカの電気自動車用バッテリー電解液市場は、今後数年間で大きく成長する展望です。

中東・アフリカの電気自動車用バッテリー電解液産業概要

中東・アフリカの電気自動車用バッテリー電解液市場は集中しており、参入企業は少数です。主要参入企業(順不同)には、Dubi Chem、Oasis Chemical Materials Trading Co、Targray Technology International, Inc、Andrea FZCO、Rekoserなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:10億米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車の導入を支援する政府の施策

- リチウムイオンバッテリーの価格低下

- 抑制要因

- 輸入バッテリーと原料への依存度の高さ

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- バッテリータイプ

- 鉛蓄バッテリー

- リチウムイオンバッテリー

- その他

- 電解質タイプ

- 液体電解質

- ゲル電解質

- 固体電解質

- 地域

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- エジプト

- カタール

- ナイジェリア

- その他の中東・アフリカ

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Dubi Chem

- Oasis Chemical Materials Trading Co

- Targray Technology International, Inc.

- Andrea FZCO

- Rekoser

- その他の著名な企業一覧

- 市場ランキング分析

第7章 市場機会と今後の動向

- 電解質材料の研究開発

The Middle East And Africa Electric Vehicle Battery Electrolyte Market size is estimated at USD 1.59 million in 2025, and is expected to reach USD 2.14 million by 2030, at a CAGR of 6.14% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the increasing adoption of electric vehicles in the Middle East region due to government policies and associated investments in them is likely to drive the market.

- On the other hand, high dependency on imported electric vehicle batteries and raw materials are likely to hinder the market growth.

- Continuous research and development in separator material is expected to provide future growth opportunities for the market.

- The South Africa is expected to be the largest market for the Middle East and Africa Electric Vehicle Battery Electrolyte during the study period.

Middle East And Africa Electric Vehicle Battery Electrolyte Market Trends

Lithium-ion Battery Segment to Hold Significant Share

- Lithium plays a crucial role in manufacturing batteries for electric vehicles (EVs). As the key ingredient in rechargeable lithium-ion batteries, lithium's high energy density facilitates extended driving ranges. Recently, the Middle East and Africa have seen a surge in lithium-ion manufacturing and research, heightening interest in battery components like electrolytes.

- For example, in July 2023, Qatar University's Center for Advanced Materials (CAM) collaborated with renowned global institutions to revolutionize lithium extraction from seawater. This breakthrough promises to address the escalating demand for clean energy and promote sustainability.

- In July 2024, Raya Auto in Egypt entered a strategic partnership with Shift EV, a startup focused on battery production and fleet electrification. Under this alliance, Shift EV will supply locally made lithium-ion batteries to power Raya Auto's light e-mobility range. Such initiatives are poised to bolster the electrolyte market, aligning with the anticipated rise in lithium battery demand across the Middle East.

- Similarly, as lithium-ion exploration projects expand in the Middle East and Africa, the demand for electrolytes in battery production is set to grow. In June 2024, EV Metals Group plc wrapped up its exploration at the Balthaga Lithium Project in Saudi Arabia. Located 450km east of Jeddah, within the Arabian Shield's southeastern area, the project spans 13 tenements over 1,200 square kilometers. This bolsters Saudi Arabia's lithium battery manufacturing prospects, likely driving up electrolyte demand and influencing market growth during the forecast period.

- Historically, lithium-ion battery prices have plummeted, spurring demand for related components like electrolytes. Bloomberg NEF reported that in 2023, the average price of lithium-ion batteries was USD 139 USD/kWh, marking a fivefold drop since 2014. Thus, as lithium-ion battery adoption surges with falling prices, the electrolyte market stands to gain.

- Given the aforementioned trends in lithium-ion batteries and electrolyte production, the electric vehicle battery electrolyte market in the Middle East and Africa is poised for growth.

South Africa is Likely to Dominate the Market

- In December 2023, South Africa's government announced plans for the nation's automotive sector to debut its electric vehicles (EVs) by 2026. Central to South Africa's Just Energy Transition (JET) strategy, which aims to cultivate a low-carbon and climate-resilient economy, is the emphasis on transport electrification. The JET framework highlights a significant investment requirement of approximately USD 6.84 billion, slated for the period from 2023 to 2027.

- In February 2024, the South African government rolled out a tax incentive to bolster domestic EV production. This initiative offers manufacturing companies a generous 150% tax deduction. Such incentives particularly benefit industry titans like Ford Motor Company and Volkswagen AG, both eager to amplify their EV output. Consequently, this uptick in EV production is set to escalate the demand for EV batteries and associated components, notably electrolytes, within the South African landscape.

- In July 2024, BYD Company, a prominent Chinese electric vehicle manufacturer, secured its inaugural order for electric buses in South Africa, aligning with its global vision to electrify public transport. Golden Arrow, a 163-year-old South African bus operator, has collaborated with the new energy vehicle (NEV) maker, placing an order for 120 electric buses. As South Africa embraces electric buses, this momentum is expected to amplify the production of electrolytes vital for battery manufacturing during the market's forecast period.

- Furthermore, South Africa has seen a notable uptick in electric vehicle adoption in recent years. Data from the International Energy Agency reveals that electric car sales in India reached 1,080 units in 2023, marking a staggering 74% surge from the prior year. Given this trajectory, South Africa's demand for electric vehicles is poised for a rebound, further energizing the electrolyte market.

- Given these trends, the rising adoption of electric vehicles and their batteries is set to bolster electrolyte manufacturing. Thus, the electric vehicle battery electrolyte market in the Middle East and Africa is poised for significant growth in the coming years.

Middle East And Africa Electric Vehicle Battery Electrolyte Industry Overview

The Middle East and Africa Electric Vehicle battery Elecrolytr market is concentrated, with few players. Some of the major players (not in particular order) include Dubi Chem, Oasis Chemical Materials Trading Co, Targray Technology International, Inc., Andrea FZCO, and Rekoser.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Government policies supporting adoption of electric vehicles

- 4.5.1.2 Declining Lithium-ion Battery Prices

- 4.5.2 Restraints

- 4.5.2.1 High dependecy on imported batteries and raw materials

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lead Acid Batteries

- 5.1.2 Lithium-ion Batteries

- 5.1.3 Other Battery Types

- 5.2 Electrolyte Type

- 5.2.1 Liquid Electrolyte

- 5.2.2 Gel Electrolyte

- 5.2.3 Solid Electrolyte

- 5.3 Geography

- 5.3.1 Saudi Arabia

- 5.3.2 South Africa

- 5.3.3 United Arab Emirates

- 5.3.4 Egypt

- 5.3.5 Qatar

- 5.3.6 Nigeria

- 5.3.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Dubi Chem

- 6.3.2 Oasis Chemical Materials Trading Co

- 6.3.3 Targray Technology International, Inc.

- 6.3.4 Andrea FZCO

- 6.3.5 Rekoser

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Research & Development in Electrolyte material