|

市場調査レポート

商品コード

1636474

北米の電気自動車用バッテリー電解液:市場シェア分析、産業動向、成長予測(2025~2030年)North America Electric Vehicle Battery Electrolyte - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の電気自動車用バッテリー電解液:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

北米の電気自動車用バッテリー電解液市場規模は、2025年に1億9,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは20.12%で、2030年には4億8,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、この地域全体で電気自動車の普及とバッテリー技術の進歩が進んでおり、予測期間中の電気自動車用バッテリー電解液市場の需要を牽引すると予想されます。

- 一方、固体電解質における技術的課題は、電気自動車用バッテリー電解質市場の成長を大きく抑制する可能性があります。

- バッテリーの性能、安全性、寿命を向上させる電解液配合の技術革新は、特に高性能または長距離EV向けに、近い将来、電気自動車バッテリー電解液市場に大きな成長機会を生み出します。

- 米国は、EV普及率の上昇により、予測期間中に北米の電気自動車用バッテリー電解質市場で最も急成長する国になると予想されています。

北米の電気自動車用バッテリー電解液市場動向

リチウムイオンバッテリータイプが大きく成長

- 北米の電気自動車用バッテリー電解液市場、特にリチウムイオンバッテリーに使用される電解液市場は、電気自動車(EV)セクターの拡大とともに急成長を遂げています。この急成長の主要要因は、EVの消費者導入の増加と、温室効果ガスの排出抑制を目的とした政府の厳しい規制です。

- リチウムイオンバッテリーは、その高いエネルギー密度、サイクル寿命の延長、自己放電率の最小化により、EVにとって極めて重要です。リチウムイオンバッテリーの価格設定は電気自動車全体のコストに大きく影響し、電解液はこれらのバッテリーコストの主要な決定要因です。

- 例えば、Bloomberg NEFのレポートによると、2023年のバッテリー価格は139米ドル/kWhまで下落し、前年から13%下落しました。継続的な技術の進歩と製造の最適化により、バッテリーパック価格は2025年までに113米ドル/kWhまでさらに低下し、2030年には80米ドル/kWhに達すると予測されています。製造効率の向上、原料の大量調達、サプライチェーンの合理化によってリチウムイオンバッテリーの生産が拡大するにつれて、バッテリー電解質の単位当たりのコストは予測期間中に低下します。

- さらに、リチウムイオンバッテリーの研究開発が進んでおり、バッテリーの性能、安全性、寿命を高める新しい電解液の配合が生まれつつあります。全国の主要ラボは、リチウムイオンEVバッテリー用の先進的な電解質ソリューションを開拓しています。

- 例えば、2023年3月、米国エネルギー省傘下のArgonne National Laboratoryの研究者は、電気自動車の走行距離を大幅に延長するリチウム空気バッテリーを発表しました。この革新的なバッテリーは、従来の液体電解質のアプローチとは異なり、固体電解質を採用しています。標準的なリチウムイオンバッテリーと比較すると、この進歩によってエネルギー密度が4倍になる可能性があり、予測期間中にEVでこのような先進的なリチウムイオンバッテリーの需要が高まることを示しています。

- さらに、大手バッテリーメーカーは北米で生産能力を増強しており、電解液市場をさらに活性化しています。2023年9月、スウェーデンの著名なリチウムイオンバッテリーメーカーであるNorthvoltは、カナダのケベック州に52億米ドルのギガファクトリーを建設する計画を発表しました。この工場はバッテリーの生産だけでなく、正極活物質の生産にも力を入れます。Northvolt Six工場の建設は今年開始され、2026年の操業が予定されています。このような取り組みにより、リチウムイオンバッテリーの生産が強化され、その結果、EV用電解液の需要も今後数年間で増加する見込みです。

- 結論として、こうした取り組みや技術革新は北米におけるリチウムイオンバッテリーの生産を拡大し、予測期間中にEV用電解液の需要を急増させると考えられます。

大幅な成長を遂げる米国

- 米国は、技術革新、製造、支援施策を重視し、北米のEVバッテリー電解質市場で極めて重要な役割を果たしています。電解液は、リチウムイオンバッテリーの重要なコンポーネントとして、負極と正極の間のリチウムイオンの移動を促進し、EVのエネルギー貯蔵と放出に極めて重要です。

- 近年、米国では、消費者の需要、環境意識の高まり、税額控除やリベートといった政府の優遇措置によって、EVの販売が顕著に増加しています。このEV普及の急増は、リチウムイオン・バッテリー、ひいては高品質のバッテリー電解液の需要に直接拍車をかけています。

- 例えば、国際エネルギー機関(IEA)の報告によると、2023年のバッテリー式電気自動車の販売台数は110万台に達し、2022年から37.5%増、2019年からは3.58倍という驚異的な伸びを示しました。政府がEVの普及を促進する施策をいくつか打ち出しているため、販売台数は今後数年間で増加する見込みです。

- さらに、米国政府は電動モビリティへのシフトを支持し、炭素排出を抑制する施策を重視しています。このコミットメントが、最先端のバッテリー電解質の進歩と展開を後押ししています。

- 例えば、2024年3月、バイデン政権は、2032年までに、新たに販売される乗用車と小型トラックの大部分をすべて電気自動車にすることを義務付ける、米国で最も徹底的な気候変動規制を発表しました。このような大胆な動きは、EVの生産を早めるだけでなく、EV用バッテリー電解液の需要を今後数年間で増幅させることになります。

- 急増するEV需要に対応するため、多くのバッテリーメーカーが米国内に生産拠点を設置または拡大しています。この国内生産戦略は、輸入品への依存を抑えるだけでなく、地域固有の電解液の安定供給を保証するものでもあります。

- 例えば、LG Energy Solutionは2023年3月、北米におけるEVとESS用バッテリーの生産を強化するため、アリゾナ州に7兆2,000億ウォン(52億2,000万米ドル)を投じてバッテリー製造拠点を設立し、話題となりました。この新しい施設ではEV用バッテリーを生産することになっており、信頼性の高い電解液供給の必要性がさらに高まっています。

- これらの開発から、このような投資やプロジェクトが米国でのEV生産を強化し、EVバッテリー用電解液の需要を押し上げることは明らかです。

北米の電気自動車用バッテリー電解質産業概要

北米の電気自動車用バッテリー電解液市場は緩やかです。主要参入企業(順不同)は、3M Company、BASF Corporation、Mitsubishi Chemical Group Corporation、Targray Technology International Inc、NEI corporationなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車の普及拡大

- バッテリー技術の進歩

- 抑制要因

- 固体電解質における技術課題

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- バッテリータイプ

- リチウムイオンバッテリー

- 鉛蓄バッテリー

- その他

- 電解質タイプ

- 液体電解質

- ゲル電解質

- 固体電解質

- 地域

- 米国

- カナダ

- その他の北米地域

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- 3M Company

- BASF Corporation

- LG Chem Ltd

- Mitsubishi Chemical Group

- Panasonic Holdings Corporation

- Solvay SA

- Asahi Kasei America, Inc.

- Cabot Corporation

- Dongwha Electrolyte Co.,Ltd.

- Samsung SDI

- NEI corporation

- Targray Technology International Inc

- その他の著名な企業一覧

- 市場ランキング分析

第7章 市場機会と今後の動向

- 電解質配合の革新

目次

Product Code: 50003741

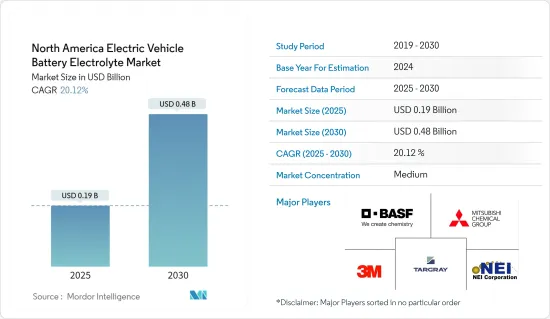

The North America Electric Vehicle Battery Electrolyte Market size is estimated at USD 0.19 billion in 2025, and is expected to reach USD 0.48 billion by 2030, at a CAGR of 20.12% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the growing adoption of electric vehicles and advancements in battery technology across the region are expected to drive the demand for the electric vehicle battery electrolyte market during the forecast period.

- On the other hand, the technological challenges in Solid-State electrolytes can significantly restrain the growth of the electric vehicle battery electrolyte market.

- Nevertheless, the innovation in electrolyte formulations that improve battery performance, safety, and lifespan, particularly for high-performance or long-range EVs creates significant growth opportunities in the electric vehicle battery electrolyte market in the near future.

- The United States is anticipated to be the fastest-growing country in the North American electric vehicle battery electrolyte market during the forecast period due to rising EV adoption.

North America Electric Vehicle Battery Electrolyte Market Trends

Lithium-Ion Batteries Type to Witness Significant Growth

- The North American market for EV battery electrolytes, especially those used in lithium-ion batteries, is experiencing rapid growth, paralleling the broader expansion of the electric vehicle (EV) sector. This surge is largely fueled by increasing consumer adoption of EVs and stringent government regulations aimed at curbing greenhouse gas emissions.

- Lithium-ion batteries are pivotal to the EV landscape, celebrated for their high energy density, extended cycle life, and minimal self-discharge rate. The pricing of lithium-ion batteries significantly influences the overall cost of electric vehicles, with electrolytes being a key determinant of these battery costs.

- For example, a Bloomberg NEF report highlighted that in 2023, battery prices fell to USD 139/kWh, marking a 13% drop from the prior year. With ongoing technological advancements and manufacturing optimizations, projections suggest battery pack prices will further decline to USD 113/kWh by 2025 and reach USD 80/kWh by 2030. As lithium-ion battery production ramps up, driven by enhanced manufacturing efficiencies, bulk raw material procurement, and streamlined supply chains, the cost per unit of battery electrolytes is set to decrease during the forecast period.

- Moreover, ongoing R&D in lithium-ion batteries is birthing new electrolyte formulations that boost battery performance, safety, and lifespan. Leading research labs nationwide are pioneering advanced electrolyte solutions for lithium-ion EV batteries.

- For instance, in March 2023, researchers from Argonne National Laboratory, under the US Department of Energy, unveiled a lithium-air battery poised to significantly extend electric vehicles' driving range. This innovative battery employs a solid electrolyte, diverging from the conventional liquid electrolyte approach. When compared to standard Li-ion batteries, this advancement could potentially quadruple energy density, signaling a heightened demand for such advanced lithium-ion batteries in EVs during the forecast period.

- Additionally, major battery manufacturers are ramping up production capacities in North America, further energizing the electrolyte market. In September 2023, Northvolt, a prominent Swedish lithium-ion battery manufacturer, unveiled plans for a USD 5.2 billion gigafactory in Quebec, Canada. This facility will not only produce batteries but also focus on cathode active material production. Construction of the Northvolt Six factory is set to kick off this year, with operations slated for 2026. Such initiatives are poised to bolster lithium-ion battery production and, consequently, the demand for EV battery electrolytes in the coming years.

- In conclusion, these initiatives and innovations are set to amplify lithium-ion battery production in North America, driving a corresponding surge in demand for EV battery electrolytes during the forecast period.

United States to Witness Significant Growth

- The United States plays a pivotal role in the North American EV battery electrolyte market, emphasizing innovation, manufacturing, and supportive policies. Electrolytes, as vital components of lithium-ion batteries, facilitate the movement of lithium ions between the anode and cathode, crucial for energy storage and release in EVs.

- In recent years, the United States has seen a notable uptick in EV sales, driven by consumer demand, heightened environmental consciousness, and government incentives like tax credits and rebates. This surge in EV adoption has directly spurred demand for lithium-ion batteries and, by extension, high-quality battery electrolytes.

- For instance, the International Energy Agency reported that in 2023, battery electric vehicle sales hit 1.1 million units, marking a 37.5% rise from 2022 and a staggering 3.58-fold increase since 2019. With the government rolling out several pro-EV adoption policies, sales are poised to climb in the coming years.

- Furthermore, the U.S. government is championing the shift to electric mobility, emphasizing policies that curb carbon emissions. This commitment is propelling the advancement and deployment of cutting-edge battery electrolytes.

- For instance, in March 2024, the Biden administration unveiled the nation's most sweeping climate regulations, mandating that by 2032, a significant majority of newly sold passenger cars and light trucks will be all-electric. Such bold moves are set to not only hasten EV production but also amplify the demand for EV battery electrolytes in the coming years.

- In response to the surging EV demand, numerous battery manufacturers are either setting up or expanding their production bases in the U.S. This domestic manufacturing strategy not only curtails dependence on imports but also guarantees a consistent supply of region-specific electrolytes.

- For instance, in March 2023, LG Energy Solution made headlines with a KRW 7.2 trillion (USD 5.22 billion) investment to establish a battery manufacturing hub in Arizona, aiming to bolster EV and ESS battery production in North America. This new facility is set to churn out EV batteries, further amplifying the need for a reliable electrolyte supply.

- Given these developments, it's evident that such investments and projects are set to bolster EV production in the United States, subsequently driving up the demand for EV battery electrolytes.

North America Electric Vehicle Battery Electrolyte Industry Overview

The North America Electric Vehicle Battery Electrolyte market is moderated. Some of the key players (not in particular order) are 3M Company, BASF Corporation, Mitsubishi Chemical Group, Targray Technology International Inc, NEI corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Adoption of Electric Vehicles

- 4.5.1.2 Advancements in Battery Technology

- 4.5.2 Restraints

- 4.5.2.1 Technological Challenges in Solid-State Electrolytes

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion Batteries

- 5.1.2 Lead-Acid Batteries

- 5.1.3 Others

- 5.2 Electrolyte Type

- 5.2.1 Liquid Electrolyte

- 5.2.2 Gel Electrolyte

- 5.2.3 Solid Electrolyte

- 5.3 Geography

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 3M Company

- 6.3.2 BASF Corporation

- 6.3.3 LG Chem Ltd

- 6.3.4 Mitsubishi Chemical Group

- 6.3.5 Panasonic Holdings Corporation

- 6.3.6 Solvay SA

- 6.3.7 Asahi Kasei America, Inc.

- 6.3.8 Cabot Corporation

- 6.3.9 Dongwha Electrolyte Co.,Ltd.

- 6.3.10 Samsung SDI

- 6.3.11 NEI corporation

- 6.3.12 Targray Technology International Inc

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Innovation in Electrolyte Formulations