中国の電気自動車用電池製造:市場シェア分析、産業動向・統計、成長予測(2025~2030年)

China Electric Vehicle Battery Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 95 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636467

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

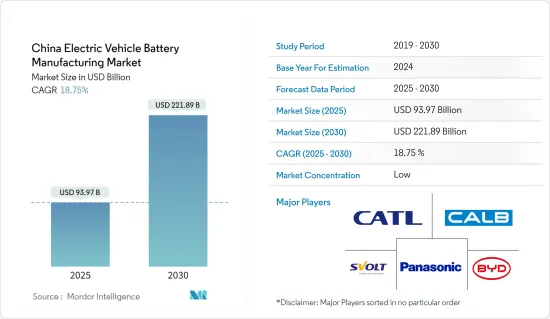

中国の電気自動車用電池製造市場規模は2025年に939億7,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは18.75%で、2030年には2,218億9,000万米ドルに達すると予測されます。

主要ハイライト

- 長期的には、電池生産能力増強のための投資や電池原料コストの低下といった要因が、予測期間中の中国の電気自動車電池製造市場の最も大きな促進要因のひとつになると予想されます。

- その一方で、主要電池原料の輸入依存度は、産業を価格変動や不均衡な開発の影響を受けやすくしています。これは予測期間中、中国の電気自動車用電池製造市場にとって脅威となります。

- 電気自動車に対する長期的な野心的目標は継続しています。この要因は、将来的に市場にいくつかの機会を生み出すと予想されます。

中国の電気自動車電池製造市場動向

市場を独占するリチウムイオン電池タイプ

- 高いエネルギー密度と長いライフサイクルで知られるリチウムイオン電池は、電気自動車メーカーにとって有力な選択肢となっています。この技術は、効率的な電気自動車の生産を保証するだけでなく、消費者の期待と産業のベンチマークの両方を満たしています。

- EVの普及と電池の国内生産を強化するため、中国政府は一連の強力な施策を展開してきました。新エネルギー自動車(NEV)義務化のようなイニシアチブは、補助金や税制優遇措置と並んで、EVセクターの急速な拡大に拍車をかけています。さらに、「メイド・イン・チャイナ2025」イニシアチブは、先進製造業の世界的フロントランナーとしての地位を確固たるものにしようという中国の野心を強調しています。

- 二酸化炭素排出量の削減と大気汚染への取り組みを推進する中国の動きは、EV市場の活況を支える極めて重要な力となっています。クリーンエネルギー自動車を支持する施策により、内燃機関から電気モビリティへの移行が急速に進んでいます。世界最大のEV市場である中国の需要急増を後押ししているのは、都市化、環境意識の高まり、厳しい自動車排ガス規制であり、これらすべてが国産電池の必要性を高めています。

- 2024年5月、中国は電気自動車(EV)用の次世代電池技術の開拓に約60億人民元(8億4,500万米ドル)を投入する予定です。全固体電池(ASSB)は、従来のリチウムイオン電池(LIB)を超える最先端の進歩であり、固体導電性電解質を利用して安全性とエネルギー密度を高めています。EV用電池の大手であるCATLは、その可能性を認識し、この技術的飛躍のために政府の支援を受ける態勢を整えています。

- 中国の大規模な充電インフラ開発は、同国の電気自動車普及にとって極めて重要です。この戦略的投資は、EVユーザーに効率的な充電ソリューションへの容易なアクセスを保証し、EV電池の需要をさらに拡大します。同時に、中国企業は研究開発に資源を投入し、電池技術の改良と生産コストの削減を目指しています。国際的なハイテク企業や研究機関とのコラボレーションが、電池製造におけるイノベーションの起爆剤となっています。

- 例えば、2024年5月、国有企業の上海汽車は、2025年までに完全固体電池をEVブランドに統合し、2026年に量産する計画を発表しました。400Wh/kgを超えるエネルギー密度を誇るこの電池は、少なくとも1,000kmの航続距離を約束します。昨年6月には、国内EVメーカーのニオが、エネルギー密度360Wh/kg、航続距離1,044kmという驚異的な記録を達成した固体電池のテストに成功しています。さらに、SAICが一部を所有するIM Motorsは、4月にIM L6 EVモデルを発表しました。このモデルは、130kWhの電力を持つ超急速充電ソリッドステート・電池を搭載し、1,000kmの航続距離と900Vの超急速充電機能をサポートしています。

- 中国は、900ギガワット時近い製造能力を誇り、世界全体の77%という圧倒的なシェアを誇る。さらに、世界の電池メーカー上位10社のうち6社は中国が占めています。この優位性は、金属採掘から車両生産まで、EVのサプライチェーン全体を中国が包括的に支配していることでさらに強化されています。世界の電気自動車保有台数の半分以上が中国にあり、2023年に1705GWhと記録された中国のリチウムイオン電池セル製造能力は、2027年までに6197GWhに急増すると予測されています。

- このような開発と投資を考えると、今後数年間はリチウムイオン電池の需要拡大とともに、この地域全体でEV用電池の生産が急増すると予想されます。

電池生産能力強化のための投資

- 中国は、電気自動車(EV)の需要急増に対応するため、戦略的に電池生産能力を増強しています。補助金や投資優遇措置などの政府の取り組みが、国内企業の生産能力強化に拍車をかけています。この協調的な取り組みにより、中国はEV用電池製造の世界のトップランナーとしての地位を固め、拡大するEV市場向けにプレミアム電池の安定供給を保証しようとしています。

- 中国全土に新しい電池生産工場が設立され、EV電池製造市場を後押ししています。CATLやBYDのような産業大手は、生産を拡大するために最新鋭の設備を導入しています。先進技術を導入したこれらの最新鋭工場は、生産量と効率の向上を約束し、急増する国内外のEV電池需要を満たす重要な要素となっています。

- スラリーミキサーの浮動入札は、電池生産プロセスを改良する上で極めて重要な役割を果たします。これらのミキサーは、電池材料の配合の均一性を確保し、リチウムイオン電池の品質と性能に直接影響します。このような重要なミキサーの入札を募集することで、中国は電池製造技術を強化するだけでなく、EV電池市場全体の成長と効率を強化し、産業の迅速な拡大を後押ししています。

- 例えば、2024年6月、中国の電池セルメーカーであるGotion High-techは、10分以下で充電できる画期的な電気自動車用電池を発表し、世界的リーダーであるCATLの強力な競争相手として位置づけた。この急速充電イノベーションは、充電時間に関する消費者の懸念に直接対応するものです。ゴティオンは、長距離ハイブリッド車向けのG-Current電池の量産を開始しました。一方、電気自動車用電池の生産ラインも建設中で、年内に量産を開始する予定です。

- 中国政府はEVセクターへの支援を堅持しており、税制優遇措置、メーカーと消費者への補助金、充電インフラの強化などの施策を展開しています。こうしたイニシアチブは、EVの手頃な価格と利便性を向上させ、普及率を高め、ひいては電池材料の需要を増幅させることを目的としています。電池技術の革新もまた、EVの状況を変えつつあります。例えば、BYDはリン酸鉄リチウム(LFP)電池のような新しい化学品を開拓しており、従来のリチウムイオン電池よりもエネルギー密度はわずかに低いもの、より安全で経済的です。こうしたブレークスルーは、EVをより広範な市場に普及させる上で極めて重要です。

- 今後を展望すると、中国のEV用電池製造市場は強気の軌道に乗る態勢を整えています。揺るぎない政府のバックアップ、技術的な進歩、戦略的な産業協力により、中国は世界のEVセグメントで優位性を維持することになります。大手電池メーカーによる生産能力の絶え間ない拡大は、サステイナブルプラクティスへの注力と相まって、必要不可欠な材料への安定した需要をもたらし、EV電池製造セクターの急速な上昇を後押ししています。

- 中国のリチウムイオン電池生産能力は驚異的な1.2テラワット時(TWh)に達し、世界の76%のシェアを占めています。世界の電気自動車の半数以上が中国の道路を走っていることから、この生産能力は2030年までに4.65TWhに急増すると予測されています。

- このような投資と生産拡大は、リチウムイオン電池容量の需要を増幅させると考えられます。

中国の電気自動車用電池製造産業概要

中国の電気自動車用電池製造市場は半分断されています。この市場の主要企業(順不同)は、BYD、Contemporary Amperex Technology Co.Limited、Panasonic Corporation、CALB(China Aviation Lithium Battery)、SVOLT Energy Technologyです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電池生産能力増強のための投資

- 電池原料コストの低下

- 抑制要因

- 主要電池材料の輸入依存

- 促進要因

- サプライチェーン分析

- PESTLE分析

- 投資分析

第5章 市場セグメンテーション

- 電池

- リチウムイオン

- 鉛-酸

- ニッケル水素電池

- その他

- 電池形態

- 角型

- 袋型

- 円筒形

- 車両

- 乗用車

- 商用車

- その他

- 推進

- 電池電気自動車

- ハイブリッド電気自動車

- プラグインハイブリッド電気自動車

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- BYD Co. Ltd

- Contemporary Amperex Technology Co. Limited

- EnerSys

- GS Yuasa Corporation

- LG Chem Ltd

- Exide Industries

- Panasonic Corporation

- CALB(China Aviation Lithium Battery)

- SVOLT Energy Technology

- EVE Energy

- その他の著名な企業一覧

- 市場ランキング分析

第7章 市場機会と今後の動向

- 電気自動車の長期的な野心的目標

目次

The China Electric Vehicle Battery Manufacturing Market size is estimated at USD 93.97 billion in 2025, and is expected to reach USD 221.89 billion by 2030, at a CAGR of 18.75% during the forecast period (2025-2030).

Key Highlights

- Over the long term, factors such as investments to enhance the battery production capacity and a decline in the cost of battery raw materials are expected to be among the most significant drivers for the China Electric Vehicle Battery Manufacturing Market during the forecast period.

- On the other hand, import dependency for key battery materials leaves the industry vulnerable to price fluctuations and imbalanced development. This poses a threat to the China Electric Vehicle Battery Manufacturing Market during the forecast period.

- Nevertheless, continued Long-term ambitious targets for electric vehicles. This factor is expected to create several opportunities for the market in the future.

China Electric Vehicle Battery Manufacturing Market Trends

Lithium-ion Battery Type to Dominate the Market

- Li-ion batteries, known for their high energy density and long life cycles, have become the go-to choice for EV manufacturers. This technology not only ensures the production of efficient electric vehicles but also meets both consumer expectations and industry benchmarks.

- To bolster EV adoption and domestic battery production, the Chinese government has rolled out a series of robust policies. Initiatives like the New Energy Vehicle (NEV) mandate, alongside subsidies and tax incentives, are fueling the rapid expansion of the EV sector. Furthermore, the "Made in China 2025" initiative underscores China's ambition to cement its status as a global frontrunner in advanced manufacturing.

- China's drive to cut carbon emissions and tackle air pollution is a pivotal force behind its booming EV market. With policies championing clean energy vehicles, the nation is witnessing a swift transition from internal combustion engines to electric mobility. As the globe's largest EV market, China's surging demand is propelled by urbanization, heightened environmental consciousness, and stringent vehicle emission regulations, all of which amplify the need for domestically produced batteries.

- In May 2024, China is set to channel approximately CNY 6 billion (USD 845 million) into pioneering next-generation battery technologies for electric vehicles (EVs). All Solid State Batteries (ASSBs), a cutting-edge advancement over traditional lithium-ion batteries (LIBs), utilize a solid conductive electrolyte, enhancing safety and energy density. Recognizing their potential, EV battery titan CATL is poised to receive government backing for this technological leap.

- China's expansive charging infrastructure development is pivotal for the country's electric vehicle adoption. This strategic investment guarantees EV users easy access to efficient charging solutions, further amplifying the demand for EV batteries. Concurrently, Chinese firms are pouring resources into R&D, aiming to refine battery technologies and curtail production costs. Collaborations with international tech giants and research entities are catalyzing innovations in battery manufacturing.

- For example, in May 2024, state-owned SAIC announced plans to integrate full solid-state batteries into its EV brands by 2025, with mass production slated for 2026. Boasting an energy density exceeding 400Wh/kg, this battery promises a driving range of at least 1,000km. Last June, domestic EV maker Nio successfully tested a solid-state battery achieving a 360Wh/kg energy density and a remarkable 1,044km range. Additionally, IM Motors, partially owned by SAIC, revealed in April its IM L6 EV model, featuring an ultra-fast charging solid-state battery with 130kWh power, supporting a 1,000km range and 900V ultra-fast charging capability.

- China dominates the global battery landscape, boasting a manufacturing capacity nearing 900 gigawatt-hours, which translates to a commanding 77% share of the worldwide total. Furthermore, six of the top ten battery manufacturers globally hail from China. This dominance is further reinforced by China's holistic control over the entire EV supply chain, from metal mining to vehicle production. With more than half of the world's electric vehicle fleet residing in China, the nation's lithium-ion battery cell manufacturing capacity, recorded at 1705 GWh in 2023, is projected to skyrocket to 6197 GWh by 2027.

- Given these developments and investments, a surge in EV battery production across the region is anticipated, alongside a growing demand for lithium-ion batteries in the coming years.

Investments to Enhance the Battery Production Capacity

- China is strategically ramping up its battery manufacturing capacity to cater to the surging demand for electric vehicles (EVs). Government initiatives, including subsidies and investment incentives, are spurring domestic companies to bolster their production capabilities. This concerted effort seeks to cement China's status as a global frontrunner in EV battery manufacturing, guaranteeing a consistent supply of premium batteries for the expanding EV market.

- The establishment of new battery production plants throughout China is propelling the EV battery manufacturing market. Industry giants like CATL and BYD are rolling out cutting-edge facilities to amplify their production. These state-of-the-art plants, outfitted with advanced technologies, promise heightened output and efficiency-key factors in satisfying the surging domestic and international appetite for EV batteries.

- Floating tenders for slurry mixers play a pivotal role in refining the battery production process. These mixers ensure uniformity in battery material blending, directly influencing the quality and performance of lithium-ion batteries. By soliciting tenders for these crucial mixers, China is not only enhancing its battery manufacturing technology but also bolstering the overall growth and efficiency of the EV battery market, fueling the industry's swift expansion.

- For example, in June 2024, Gotion High-tech, a Chinese battery cell manufacturer, unveiled a groundbreaking electric vehicle battery capable of charging in under 10 minutes, positioning it as a formidable competitor to global leader CATL. This swift-charging innovation directly addresses consumer concerns about charging durations. Gotion has commenced mass production of its G-Current batteries, tailored for extended-range hybrids. Meanwhile, production lines for all-electric vehicle batteries are under construction, with mass production slated to kick off by year's end.

- China's government remains steadfast in its support for the EV sector, rolling out measures like tax incentives, subsidies for manufacturers and consumers, and bolstering charging infrastructure. Such initiatives aim to enhance the affordability and convenience of EVs, driving up adoption rates and, in turn, amplifying the demand for battery materials. Battery technology innovations are also reshaping the landscape. For instance, BYD is pioneering new chemistries like lithium iron phosphate (LFP) batteries-safer and more economical, albeit with a marginally lower energy density than conventional lithium-ion counterparts. These breakthroughs are pivotal in making EVs more accessible to the broader market.

- Looking ahead, China's EV battery manufacturing market is poised for a bullish trajectory. With unwavering government backing, technological strides, and strategic industry collaborations, China is set to uphold its dominance in the global EV arena. The relentless expansion of production capacities by leading battery manufacturers, coupled with a focus on sustainable practices, bodes well for a consistent demand for essential materials, propelling the swift ascent of the EV battery manufacturing sector.

- China's lithium-ion battery manufacturing capacity stands at a staggering 1.2 terawatt hours (TWh), commanding a robust 76 percent share of the global landscape. With more than half of the world's electric vehicles gracing Chinese roads, projections indicate this capacity will surge to 4.65 TWh by 2030.

- Such investments and production expansions are set to amplify the demand for lithium-ion battery capacity.

China Electric Vehicle Battery Manufacturing Industry Overview

The China Electric Vehicle Battery Manufacturing Market is semi-fragmented. Some of the key players in this market (in no particular order) are BYD Co. Ltd., Contemporary Amperex Technology Co. Limited, Panasonic Corporation, CALB (China Aviation Lithium Battery), and SVOLT Energy Technology.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Investments to Enhance the battery production capacity

- 4.5.1.2 Decline in cost of battery raw materials

- 4.5.2 Restraints

- 4.5.2.1 Import Dependency for Key Battery Material

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE ANALYSIS

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery

- 5.1.1 Lithium-ion

- 5.1.2 Lead-Acid

- 5.1.3 Nickel Metal Hydride Battery

- 5.1.4 Others

- 5.2 Battery Form

- 5.2.1 Prismatic

- 5.2.2 Pouch

- 5.2.3 Cylindrical

- 5.3 Vehicle

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.3.3 Others

- 5.4 Propulsion

- 5.4.1 Battery Electric Vehicle

- 5.4.2 Hybrid Electric Vehicle

- 5.4.3 Plug-in Hybrid Electric Vehicle

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BYD Co. Ltd

- 6.3.2 Contemporary Amperex Technology Co. Limited

- 6.3.3 EnerSys

- 6.3.4 GS Yuasa Corporation

- 6.3.5 LG Chem Ltd

- 6.3.6 Exide Industries

- 6.3.7 Panasonic Corporation

- 6.3.8 CALB (China Aviation Lithium Battery)

- 6.3.9 SVOLT Energy Technology

- 6.3.10 EVE Energy

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Long-term ambitious targets for electric vehicles

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 95 Pages

- 納期

- 2~3営業日