|

市場調査レポート

商品コード

1636437

英国のEV用バッテリー製造:市場シェア分析、産業動向、成長予測(2025年~2030年)United Kingdom Electric Vehicle Battery Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国のEV用バッテリー製造:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

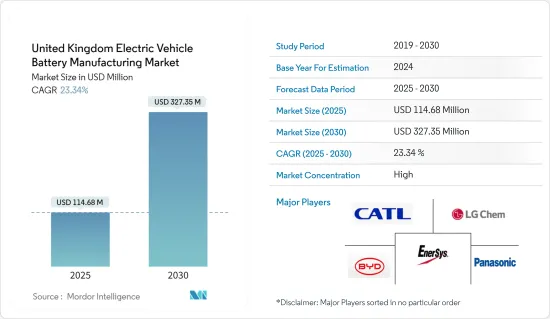

英国のEV用バッテリー製造の市場規模は、2025年に1億1,468万米ドルと推定され、予測期間(2025-2030年)のCAGRは23.34%で、2030年には3億2,735万米ドルに達すると予測されます。

主なハイライト

- 中期的には、英国のEV用バッテリー製造市場は、バッテリー生産能力増強に向けた投資によって成長する見込みです。さらに、原材料と電気自動車用電池の価格下落が、政府の支援政策と相まって、この市場をさらに後押ししています。

- 逆に、原材料の埋蔵量に限りがあることが市場拡大の課題となっています。

- しかし、電池材料の技術的進歩が続いており、英国が野心的な電気自動車の長期目標を掲げていることから、同市場のプレーヤーには大きな機会が生じています。

英国のEV用バッテリー製造市場動向

リチウムイオン電池セグメントが市場を独占

- リチウムイオン電池産業の黎明期には、コンシューマーエレクトロニクスが主要市場でした。しかし、時間の経過とともに、英国(UK)でのEV販売の急増に牽引され、電気自動車(EV)メーカーがリチウムイオン電池の主要消費者として主導権を握るようになった。

- 過去10年間、英国では主に自動車分野でリチウムイオン電池技術が急成長してきました。英国でリチウムイオン二次電池が好まれるようになったのは、容量対重量比が優れているからです。さらに、EVのリチウム電池はNOX、CO2、その他の温室効果ガスを発生させないため、従来の内燃機関(ICE)車と比べて環境負荷が大幅に低いです。こうした利点を認識し、英国をはじめとするいくつかの国は、補助金や政府のイニシアティブを通じてEVの普及と電池製造の成長を促進しています。

- 2023年、電気自動車(EV)用バッテリーパックの平均価格は139米ドル/kWhに下落し、2022年から13%下落しました。この下落は、数年前の価格上昇傾向に続くものです。継続的な技術の進歩と製造効率の向上により、バッテリーパック価格の継続的な下落が予測されており、2025年には113米ドル/kWh、2030年には80米ドル/kWhまでさらに急落すると予測されています。こうした動向は、英国におけるリチウムイオン電池製造の隆盛を後押ししています。

- 国際エネルギー機関(IEA)によると、リチウムイオン技術に90%以上依存している英国の電気自動車の販売台数は、同国のEVバッテリー製造市場の成長を反映しています。2023年の販売台数は31万台に達し、2022年の27万台から14.8%増加しました。これは、英国のEVバッテリー製造状況において、リチウムイオン電池が圧倒的な地位を占めていることを裏付けています。

- 2024年3月、リチウムイオン電気自動車用バッテリーを専門とする中国企業EVEエナジーは、12億ユーロを超える大規模な投資計画を発表しました。この投資は、英国のコベントリー郊外に570万平方フィートの広大なギガファクトリーを建設するためのもので、英国電化センターの要として構想されています。このような大規模な投資は、英国のEV用バッテリー製造市場の力強い成長軌道を示すものです。

- 2024年4月、大手自動車部品メーカーであるADVIKは、英国を拠点とする先進的なリチウムイオン電池企業であるAceleron Energy Ltd.の事業資産を買収し、大きな話題となった。この戦略的買収は、ADVIKの製品群と顧客基盤を拡大するだけでなく、次世代エネルギー貯蔵ソリューションへのコミットメントを強調するものです。ADVIKの英国部門であるADVIK Technologies Limitedが管理するこの買収により、Aceleronの最先端のリチウムイオン電池技術がADVIKのポートフォリオに統合されます。特許技術に加え、この買収によりADVIKは英国に試験・試作施設を増設し、すでに10工場からなる広範なネットワークを強化することになります。

- これらの開発から、リチウムイオン電池分野が英国市場を独占する態勢にあることは明らかです。

政府の政策とインセンティブがEV販売急増の原動力

- 英国は、温室効果ガス(GHG)、特に二酸化炭素の排出を抑制するために、いくつかの法律、政策、法律を制定しています。さらに、英国はバッテリー電気自動車に対するさまざまな優遇策を展開し、EVバッテリーメーカーにとって有利な条件を作り出しています。

- その先頭に立つのが、2022年4月に最終更新されたネットゼロ戦略(Build Back Greener)です。この戦略は、2020年11月18日に導入された「グリーン産業革命のための10項目計画」の直接的な続編であり、2050年までに政府の野心的なネットゼロ排出量目標を達成することを目的とした、政策やイニシアチブを含む包括的なロードマップを提示しています。2023年3月には、これらのイニシアチブが大幅に更新され、詳細な「パワーアップ・ブリテン」を含む広範な政策発表「パワーアップ・ブリテン」によって強調された:ネット・ゼロ成長計画

- 2023年3月、英国政府は、排出削減戦略を詳述した炭素収支計画(CBDP)を発表しました。この計画は高等法院の判決に対応するもので、ゼロ・エミッション車(ZEV)義務化法案を包含していました。

- 画期的な決定として、英国政府は2022年3月、化石燃料車を段階的に廃止し、2035年までにゼロ・エミッション車のみで構成される車両を目指す意向を発表しました。こうした動きは消費者の嗜好を変えつつあり、EVに傾倒する個人が増えています。

- さらに、政府は電気自動車充電インフラの拡大に力を入れています。国際エネルギー機関のデータでは、英国のEV充電ポイントが急増しており、2022年の36,900カ所から2023年には53,000カ所に急増しています。

- 2024年1月、英国は電気自動車移行に向けた世界で最も野心的な規制枠組みを導入しました。2024年に発効した英国のゼロ・エミッション車(ZEV)指令は、2030年までの製造業者の生産目標を示しています。2030年までに、英国で販売されるバンの新車の70%、自動車の新車の80%をゼロ・エミッション車にすることを目標としており、2035年までに完全移行することを推進しています。この軌跡は、英国のEVバッテリー製造市場が大きく成長する可能性を示唆しています。

- まとめると、電気自動車のシェアを高めるための英国政府の協調努力は、同国のバッテリー製造業界にとって良い兆しです。

英国のEV用バッテリー製造業界の概要

英国のEV用バッテリー製造市場は半固体化しています。同市場の主要企業(順不同)には、BYD Company Ltd.、Duracell Inc.、EnerSys、Panasonic Holdings Corporation、Contemporary Amperex Technology Co.Ltd.、LG Chem Ltd.などがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 市場概要

- イントロダクション

- 2029年までの市場規模および需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 電池生産能力増強のための投資

- 電池原材料コストの低下

- 有利な政府政策

- 抑制要因

- 原料備蓄の不足

- 促進要因

- サプライチェーン分析

- PESTLE分析

- 投資分析

第2章 市場セグメンテーション

- バッテリー別

- リチウムイオン

- 鉛蓄電池

- ニッケル水素電池

- その他

- 電池形状別

- 角型

- 袋型

- 円筒形

- 車両別

- 乗用車

- 商用車

- その他

- 推進別

- バッテリー電気自動車

- ハイブリッド電気自動車

- プラグインハイブリッド電気自動車

第3章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- BYD Co. Ltd

- Contemporary Amperex Technology Co. Limited

- Duracell Inc

- EnerSys

- GS Yuasa Corporation

- LG Chem Ltd

- Exide Industries

- Panasonic Corporation

- List of Other Prominent Companies

- 市場ランキング分析

第4章 市場機会と今後の動向

- 電気自動車の長期的な野心的目標

The United Kingdom Electric Vehicle Battery Manufacturing Market size is estimated at USD 114.68 million in 2025, and is expected to reach USD 327.35 million by 2030, at a CAGR of 23.34% during the forecast period (2025-2030).

Key Highlights

- In the medium term, the United Kingdom's Electric Vehicle Battery Manufacturing Market is poised for growth, driven by investments aimed at boosting battery production capacity. Additionally, a drop in the prices of raw materials and EV batteries, combined with supportive government policies, further bolsters this market.

- Conversely, a limited reserve of raw materials poses a challenge to the market's expansion.

- However, with ongoing technological advancements in battery materials and the UK's ambitious long-term electric vehicle targets, significant opportunities arise for players in the market.

United Kingdom Electric Vehicle Battery Manufacturing Market Trends

Lithium-ion Battery Segment to Dominate the Market

- In the early days of the lithium-ion battery industry, consumer electronics were the primary market. However, over time, electric vehicle (EV) manufacturers have taken the lead as the main consumers of lithium-ion batteries, driven by a surge in EV sales in the United Kingdom (UK).

- Over the past decade, the United Kingdom has seen a meteoric rise in lithium-ion battery technology, predominantly in the automotive sector. The growing preference for lithium-ion rechargeable batteries in the UK can be attributed to their superior capacity-to-weight ratio. Furthermore, lithium batteries in EVs produce no NOX, CO2, or other greenhouse gases, resulting in a significantly lower environmental impact compared to traditional internal combustion engine (ICE) vehicles. Recognizing these advantages, the UK and several other nations are promoting EV adoption and battery manufacturing growth through subsidies and government initiatives.

- In 2023, average battery pack prices for electric vehicles (EVs) fell to USD 139/kWh, a notable 13% drop from 2022. This decline followed a trend of rising prices in the years prior. With ongoing technological advancements and improved manufacturing efficiencies, projections indicate a continued decrease in battery pack prices, forecasting USD 113/kWh by 2025 and an even steeper drop to USD 80/kWh by 2030. Such trends bolster the prominence of lithium-ion battery manufacturing in the UK.

- According to the International Energy Agency (IEA), sales of electric vehicles in the United Kingdom, which are over 90% reliant on lithium-ion technology, mirrored the growth of the country's EV battery manufacturing market. In 2023, sales reached 310,000 vehicles, up from 270,000 in 2022, marking a notable 14.8% increase. This underscores the dominant position of lithium-ion batteries in the UK's EV battery manufacturing landscape.

- In March 2024, EVE Energy, a Chinese firm specializing in lithium-ion electric vehicle batteries, unveiled plans for a significant investment exceeding EUR 1.2 billion. The investment is set to fund a sprawling 5.7 million square feet gigafactory on the outskirts of Coventry, United Kingdom, envisioned as a cornerstone of the United Kingdom Centre for Electrification. Such substantial investments signal a robust growth trajectory for the UK's electric vehicle battery manufacturing market.

- In April 2024, ADVIK, a leading automotive component manufacturer, made headlines by acquiring the business assets of Aceleron Energy Ltd., an advanced lithium-ion battery firm based in the UK. This strategic acquisition not only expands ADVIK's product range and customer base but also emphasizes its commitment to next-generation energy storage solutions. Managed by ADVIK Technologies Limited, the company's British division, the acquisition integrates Aceleron's state-of-the-art lithium-ion battery technology into ADVIK's portfolio. In addition to the patented technology, the deal enhances ADVIK's capabilities with extra testing and prototyping facilities in the UK, strengthening its already extensive network of ten plants.

- Given these developments, it's evident that the lithium-ion battery segment is poised to dominate the market in the United Kingdom.

Policies and incentives of the Government are driving the Surge in EV Sales

- The United Kingdom has enacted several legislations, policies, and acts to curb greenhouse gas (GHG) emissions, particularly carbon dioxide. Additionally, the United Kingdom (UK) has rolled out various incentives for battery-electric vehicles, creating favorable conditions for EV battery manufacturers.

- Leading the charge is the Net Zero Strategy (Build Back Greener), which was last updated in April 2022. This strategy, a direct continuation of the Ten-point plan for a green industrial revolution introduced on November 18, 2020, lays out a comprehensive roadmap with policies and initiatives aimed at achieving the government's ambitious net-zero emissions target by 2050. March 2023 saw a significant update to these initiatives, underscored by the extensive policy release, Powering Up Britain, which included the detailed Powering Up Britain: Net Zero Growth Plan.

- In March 2023, the UK government unveiled its Carbon Budget Delivery Plan (CBDP), detailing its emission reduction strategy. This plan was a response to a High Court ruling and encompassed the Zero Emission Vehicle (ZEV) mandate legislation.

- In a landmark decision, the UK government, in March 2022, announced its intent to phase out fossil fuel vehicles, aiming for a fleet exclusively made up of zero-emission vehicles by 2035. These moves are reshaping consumer preferences, with a growing number of individuals gravitating towards EVs.

- Moreover, the government is intensifying its focus on expanding electric vehicle charging infrastructure. Data from the International Energy Agency reveals a surge in the UK's EV charging points, jumping from 36,900 in 2022 to 53,000 in 2023, which notably includes 10,000 Superfast EV charging stations.

- In January 2024, the UK rolled out the globe's most ambitious regulatory framework for the electric vehicle transition. Effective in 2024, the UK's zero-emission vehicle (ZEV) mandate outlines production targets for manufacturers up to 2030. By 2030, the mandate aims for 70% of new vans and 80% of new cars sold in Great Britain to be zero-emission, pushing for a complete transition by 2035. This trajectory hints at significant growth prospects for the UK's EV battery manufacturing market.

- In summary, the UK government's concerted efforts to boost the share of electric vehicles bode well for the country's battery manufacturing industry.

United Kingdom Electric Vehicle Battery Manufacturing Industry Overview

The United Kingdom Electric Vehicle Battery Manufacturing Market is semi-consolidated. Some of the major players in the market (in no particular order) include BYD Company Ltd, Duracell Inc., EnerSys, Panasonic Holdings Corporation, Contemporary Amperex Technology Co. Limited, and LG Chem Ltd among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 MARKET OVERVIEW

- 1.1 Introduction

- 1.2 Market Size and Demand Forecast in USD, till 2029

- 1.3 Recent Trends and Developments

- 1.4 Government Policies and Regulations

- 1.5 Market Dynamics

- 1.5.1 Drivers

- 1.5.1.1 Investments to Enhance the battery production capacity

- 1.5.1.2 Decline in cost of battery raw materials

- 1.5.1.3 Favorable Government Policies

- 1.5.2 Restraints

- 1.5.2.1 Lack of Raw Material Reserves

- 1.5.1 Drivers

- 1.6 Supply Chain Analysis

- 1.7 PESTLE ANALYSIS

- 1.8 Investment Analysis

2 MARKET SEGMENTATION

- 2.1 Battery

- 2.1.1 Lithium-ion

- 2.1.2 Lead-Acid

- 2.1.3 Nickel Metal Hydride Battery

- 2.1.4 Others

- 2.2 Battery Form

- 2.2.1 Prismatic

- 2.2.2 Pouch

- 2.2.3 Cylindrical

- 2.3 Vehicle

- 2.3.1 Passenger Cars

- 2.3.2 Commercial Vehicles

- 2.3.3 Others

- 2.4 Propulsion

- 2.4.1 Battery Electric Vehicle

- 2.4.2 Hybrid Electric Vehicle

- 2.4.3 Plug-in Hybrid Electric Vehicle

3 COMPETITIVE LANDSCAPE

- 3.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 3.2 Strategies Adopted by Leading Players

- 3.3 Company Profiles

- 3.3.1 BYD Co. Ltd

- 3.3.2 Contemporary Amperex Technology Co. Limited

- 3.3.3 Duracell Inc

- 3.3.4 EnerSys

- 3.3.5 GS Yuasa Corporation

- 3.3.6 LG Chem Ltd

- 3.3.7 Exide Industries

- 3.3.8 Panasonic Corporation

- 3.4 List of Other Prominent Companies

- 3.5 Market Ranking Analysis

4 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 4.1 Long-term ambitious targets for electric vehicles