|

市場調査レポート

商品コード

1636259

電気自動車用バッテリー電解液:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Electric Vehicle Battery Electrolyte - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 電気自動車用バッテリー電解液:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 124 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

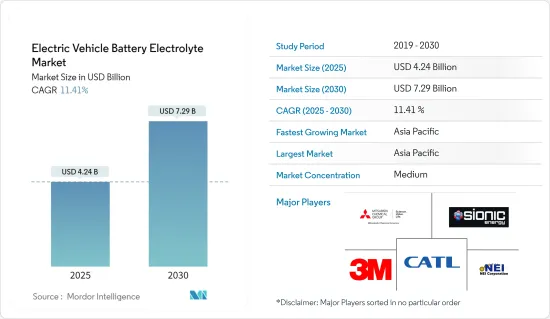

電気自動車用バッテリー電解液市場規模は2025年に42億4,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは11.41%で、2030年には72億9,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、電気自動車需要の増加や政府の支援策などの要因が、予測期間中の市場を牽引すると予想されます。

- 一方、先進電解質のコスト高と安全性への懸念が、予測期間中の市場成長の妨げになると予想されます。

- しかし、技術革新と新興バッテリー材料の拡大は、今後数年間、市場に大きな機会をもたらすと予想されます。

- アジア太平洋は、同地域のさまざまな国で電気自動車の普及率が高まっていることから、市場を独占すると推定されます。

電気自動車用バッテリー電解液の市場動向

市場を独占するリチウムイオンバッテリーセグメント

- リチウムイオンバッテリーは従来、主に携帯電話やパソコンなどの民生用電子機器に使用されてきました。しかし、環境負荷の低さから、ハイブリッド車や完全な電気自動車(EV)の動力源として再設計されるケースが増えています。EVはCO2や窒素酸化物などの温室効果ガスを一切排出しないです。

- 2023年、電気自動車(EV)用バッテリーの需要は前年比40%増と急増しました。中国はバッテリー生産、特に大型バッテリーの生産で引き続きリードしており、生産量の約12%が輸出されています。一方、欧州は大きく躍進しており、BloombergNEFの予測では、2030年までに世界のバッテリー生産に占める欧州のシェアは31%に達する可能性があります。

- 世界中で電気自動車の需要が高まるにつれ、効果的で信頼性の高いバッテリー電解液が最重要となり、電解液の配合や技術の大幅な進歩が促進されています。

- リチウムイオンバッテリー用電解液市場に影響を与える主要動向の一つは、リチウムイオンバッテリーの価格が継続的に下落していることです。例えば、リチウムイオンバッテリーの平均価格は2023年には1キロワット時(kWh)当たり約139米ドルまで下落し、2013年以来82%以上の大幅な低下となりました。予測によると、価格は2025年までに113米ドル/kWh以下に下がり、2030年には80米ドル/kWhに達する可能性があります。このような価格低下傾向は、消費者にとって電気自動車をより手頃なものにし、メーカーが新しい電解質組成を探求し、既存のものを改良してバッテリーの性能と寿命を向上させることを促します。

- 新興市場での電気自動車の普及拡大も、リチウムイオンバッテリー用電解質セグメントの成長を後押ししています。世界各国の政府は、電気自動車の普及を促進するための施策やインセンティブを実施しています。

- 米国政府は2023年、2030年までに新車販売の50%を電気自動車にするという目標を発表しました。ホワイトハウスはまた、EV Acceleration Challengeのもと、アメリカの電気自動車への歴史的移行を支援するための官民のコミットメントを発表しました。

- これは、バッテリー生産と電解液需要の急増につながります。各国が温室効果ガス排出量の削減とよりクリーンなエネルギー源への移行を優先する中、効率的なバッテリー電解液の役割は、こうした持続可能性の目標を達成する上でますます重要になっています。

- したがって、市場が発展するにつれて、持続可能性と代替技術への注目がバッテリー電解質セグメントの今後の世界の展望を形成し、より環境に優しい自動車産業に貢献すると予想されます。

アジア太平洋が市場を独占する見込み

- アジア太平洋の電気自動車(EV)用バッテリー電解液市場は、主に中国のEV生産・販売における主導的地位に牽引され、著しい成長を遂げています。世界の電気自動車販売台数は2019年の106万台から2023年には810万台に急増し、650%以上の増加となっており、中国のバッテリー電解液に対する旺盛な需要はこの拡大において極めて重要な役割を果たしています。

- 中国企業はバッテリー技術革新の最前線にあり、リチウムイオンバッテリーの性能と効率を絶えず向上させています。2024年3月には、電気自動車用リチウムイオンバッテリーの充電速度を大幅に向上させ、動作温度範囲を拡大する新しい電解質設計が調査によって発表され、大きなブレークスルーがもたらされました。この革新的な設計は、室温で10分以内の完全な充放電サイクルを可能にし、-70℃から60℃までの広い温度範囲にわたってバッテリーの可逆性を保証します。このような進歩はバッテリー効率を高め、安全性を向上させ、電気自動車用リチウムイオンバッテリーの信頼性を高めます。

- リチウムイオンバッテリーの大量生産は製造コストの低下に貢献し、電気自動車を消費者にとってより身近なものにしています。人件費の低下とメーカー間の競争激化により、全体的な収益性が向上し、より幅広い市場への参入が可能になりました。こうしたコスト効率は、より多くの消費者に電気自動車への移行を促し、それによって電解液の需要を促進する上で極めて重要です。

- 中国に加え、日本や韓国などのアジア太平洋諸国も、電気自動車用バッテリー電解質市場で大きな進歩を遂げています。日本は固体バッテリーとナトリウムイオンバッテリーの開発に重点を置いており、より低コストでより優れた性能を実現することが期待されている一方、韓国はバッテリーの生産と技術革新に多額の投資を行っています。

- 例えば、2024年4月、日本の研究者は、固体リチウムイオンバッテリーの電解質として使用するのに適した安定した高導電性材料を特定しました。この新材料は、これまで知られていた酸化物固体電解質を凌ぐイオン伝導性を誇り、広い温度範囲で効果的に作動します。

- アジア太平洋の電気自動車用バッテリー電解質市場は、技術の進歩、政府の強力な支援、コスト効率、インフラの拡大によって、継続的な成長が見込まれています。これらの要因が集約されるにつれて、この地域は電気自動車用バッテリー電解液市場における優位性を維持し、サステイナブル輸送の未来を形成すると予想されます。

電気自動車用バッテリー電解液産業概要

電気自動車用バッテリー電解液市場は半固体化しています。主要参入企業には(順不同)Mitsubishi Chemical Group、Sionic Energy、3M、Contemporary Amperex Technology Co.Limited(CATL)、NEI Corporationなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:10億米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車需要の増加

- 政府の支援策

- 抑制要因

- 先進電解質のコスト高

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- バッテリータイプ

- リチウムイオンバッテリー

- 鉛バッテリー

- その他のバッテリータイプ

- 電解質タイプ

- 液体電解質

- ゲル電解質

- 固体電解質

- 地域

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- ノルディック

- トルコ

- ロシア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- タイ

- インドネシア

- ベトナム

- マレーシア

- その他のアジア太平洋

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- エジプト

- ナイジェリア

- カタール

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Mitsubishi Chemical Group

- 3M Co.

- Contemporary Amperex Technology Co. Limited(CATL)

- NEI Corporation

- Sionic Energy

- BASF SE

- Solvay SA

- UBE Industries Ltd

- LG Chem Ltd

- Targray Industries Inc.

- 市場ランキング/シェア分析

- その他の著名な企業一覧

第7章 市場機会と今後の動向

- 新興バッテリー材料の拡大

目次

Product Code: 50003540

The Electric Vehicle Battery Electrolyte Market size is estimated at USD 4.24 billion in 2025, and is expected to reach USD 7.29 billion by 2030, at a CAGR of 11.41% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the increasing demand for electric vehicles and supportive government initiatives are expected to drive the market during the forecast period.

- On the other hand, high costs of advanced electrolytes and safety concerns are expected to hinder the market growth during the forecast period.

- However, technological innovations and expansion in emerging battery materials are expected to provide significant opportunities for the market in the coming years.

- Asia-Pacific is estimated to dominate the market due to the increasing adoption rate of electric vehicles across the various countries in the region.

Electric Vehicle Battery Electrolyte Market Trends

The Lithium-ion Batteries Segment to Dominate the Market

- Lithium-ion batteries have traditionally been used mainly in consumer electronic devices like mobile phones and personal computers. Still, due to low environmental impact, they are increasingly being redesigned as the power source of choice in hybrid and the complete electric vehicle (EV) range. EVs do not emit any CO2, nitrogen oxides, or other greenhouse gases.

- In 2023, the demand for electric vehicle (EV) batteries surged by 40% compared to the previous year, driven by rising EV sales across all markets, particularly in Europe and the United States. China continues to lead in battery production, especially for heavy-duty batteries, with approximately 12% of its production being exported. Meanwhile, Europe is making significant strides, with forecasts from BloombergNEF suggesting that its share of global battery production could reach 31% by 2030.

- As the demand for electric vehicles escalates worldwide, effective and reliable battery electrolytes have become paramount, fostering significant advancements in electrolyte formulations and technologies.

- One of the primary trends influencing the lithium-ion battery electrolyte market is the continuous decline in the price of lithium-ion batteries. For instance, the average price of lithium-ion batteries fell to around USD 139 per kilowatt-hour (kWh) in 2023, representing a significant decrease of over 82% since 2013. Projections indicate that prices could decline to below USD 113/kWh by 2025 and reach USD 80/kWh by 2030. This downward pricing trend makes electric vehicles more affordable for consumers and encourages manufacturers to explore new electrolyte compositions and improve existing ones, enhancing battery performance and longevity.

- The increasing penetration of electric vehicles in emerging markets is also driving the growth of the lithium-ion battery electrolyte segment. Governments worldwide are implementing policies and incentives to promote electric vehicle adoption.

- In 2023, the US government announced a goal to have 50% of all new vehicle sales electric by 2030. The White House also announced public and private commitments to support America's historic transition to electric vehicles under the EV Acceleration Challenge.

- This leads to a surge in battery production and electrolyte demand. As countries prioritize reducing greenhouse gas emissions and transitioning to cleaner energy sources, the role of efficient battery electrolytes becomes increasingly critical in achieving these sustainability goals.

- Hence, as the market evolves, the focus on sustainability and alternative technologies is expected to shape the future landscape of the battery electrolyte segment globally, contributing to a greener automotive industry.

Asia-Pacific is Expected to Dominate the Market

- The Asia-Pacific electric vehicle (EV) battery electrolyte market is witnessing remarkable growth, primarily driven by China's leading EV production and sales position. With global electric vehicle sales skyrocketing from 1.06 million in 2019 to 8.1 million in 2023, an increase of over 650%, China's robust demand for battery electrolytes plays a pivotal role in this expansion.

- Chinese companies are at the forefront of battery innovation, continually enhancing the performance and efficiency of lithium-ion batteries. A significant breakthrough occurred in March 2024, as researchers unveiled a new electrolyte design that greatly enhances the charging speed and expands the operational temperature range of lithium-ion batteries for electric vehicles. This innovative design allows for full charge and discharge cycles within 10 minutes at room temperature and ensures battery reversibility across a wide temperature span from -70°C to 60°C. Such advancements enhance battery efficiency and improve safety, making lithium-ion batteries more reliable for electric vehicles.

- The large-scale production of lithium-ion batteries has contributed to the decline in manufacturing costs, making electric vehicles more accessible to consumers. Lower labor costs and increased competition among manufacturers have enhanced overall profitability, enabling broader market reach. These cost efficiencies are critical in encouraging more consumers to transition to electric vehicles, thereby driving demand for electrolytes.

- In addition to China, other countries in Asia-Pacific, such as Japan and South Korea, are making significant strides in the electric vehicle battery electrolyte market. Japan's focus on developing solid-state and sodium-ion batteries promises to deliver better performance at lower costs, while South Korea is investing heavily in battery production and innovation.

- For instance, in April 2024, Japanese researchers identified a stable, highly conductive material suitable for use as an electrolyte in solid-state lithium-ion batteries. This new material boasts ionic conductivity surpassing that of any previously known oxide solid electrolytes and operates effectively over a wide temperature range.

- The Asia-Pacific electric vehicle battery electrolyte market is poised for continued growth, fueled by technological advancements, strong government support, cost efficiencies, and an expanding infrastructure. As these factors converge, the region is expected to maintain its dominance in the market for EV battery electrolytes, shaping the future of sustainable transportation.

Electric Vehicle Battery Electrolyte Industry Overview

The electric vehicle battery electrolyte market is semi-consolidated. Some of the major players include (not in particular order) Mitsubishi Chemical Group, Sionic Energy, 3M Co., Contemporary Amperex Technology Co. Limited (CATL), and NEI Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand of Electric Vehicles

- 4.5.1.2 Supportive Government Initiatives

- 4.5.2 Restraints

- 4.5.2.1 High Costs of Advanced Electrolytes

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion Batteries

- 5.1.2 Lead-acid Batteries

- 5.1.3 Other Battery Types

- 5.2 Electrolyte Type

- 5.2.1 Liquid Electrolyte

- 5.2.2 Gel Electrolyte

- 5.2.3 Solid Electrolyte

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Spain

- 5.3.2.5 NORDIC

- 5.3.2.6 Turkey

- 5.3.2.7 Russia

- 5.3.2.8 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Thailand

- 5.3.3.6 Indonesia

- 5.3.3.7 Vietnam

- 5.3.3.8 Malaysia

- 5.3.3.9 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Egypt

- 5.3.5.5 Nigeria

- 5.3.5.6 Qatar

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Mitsubishi Chemical Group

- 6.3.2 3M Co.

- 6.3.3 Contemporary Amperex Technology Co. Limited (CATL)

- 6.3.4 NEI Corporation

- 6.3.5 Sionic Energy

- 6.3.6 BASF SE

- 6.3.7 Solvay SA

- 6.3.8 UBE Industries Ltd

- 6.3.9 LG Chem Ltd

- 6.3.10 Targray Industries Inc.

- 6.4 Market Ranking/Share Analysis

- 6.5 List of Other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Expansion in Emerging Battery Materials