|

市場調査レポート

商品コード

1636253

ダイレクト・トゥ・カスタマー・アウトソーシング・フルフィルメント:市場シェア分析、産業動向、成長予測(2025年~2030年)Direct To Customer Outsourced Fulfillment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ダイレクト・トゥ・カスタマー・アウトソーシング・フルフィルメント:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

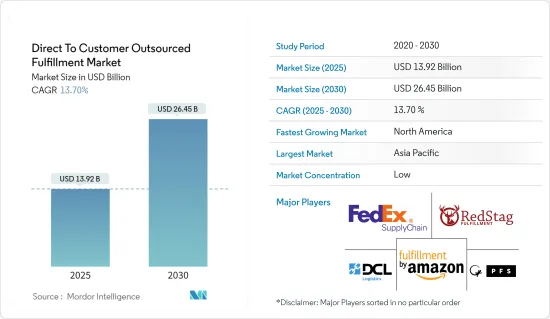

ダイレクト・トゥ・カスタマー・アウトソーシング・フルフィルメント市場規模は2025年に139億2,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは13.7%で、2030年には264億5,000万米ドルに達すると予測されます。

企業はD2C注文を処理するための重要な戦略として、フルフィルメントのアウトソーシングに目を向けることが多いです。このアプローチでは、倉庫、在庫、出荷業務を監督する第三者物流業者(3PL)を雇うことになります。フルフィルメントのアウトソーシングは、これらの業務を管理するための社内リソースや専門知識を持たない企業にとって魅力的です。3PLと提携することで、企業は3PLの専門知識とインフラを活用し、フルフィルメントプロセスを合理化することができます。この戦略は、倉庫の設置や人員配置に関連するような固定費の削減に役立つ一方で、企業はコアコンピタンスに集中することができます。しかし、フルフィルメントプロセスのコントロールを放棄することは、顧客体験全体に影響を与える可能性があります。

2024年1月、Apollo Groupのロジスティクス部門であるApollo Supply Chainは、D2Cブランド向けにカスタマイズ型、包括的なeコマース・フルフィルメントと発送の新サービスを発表しました。産業関係者は、すでに賑わいを見せているインドのD2Cは、2027年までに600億米ドルの産業に急成長すると予測しています。

さらに、2023年6月には、欧州で著名なeコマース・フルフィルメント企業であるAlaikoが、英国に進出するという戦略的な動きを見せた。Alaikoはロンドン北部にある最先端のフルフィルメントセンターと提携し、地元市場に対応します。他とは一線を画し、Alaikoは技術中心のフルフィルメントサービスであることを誇りとしています。同社独自のプラットフォームであるAlaiko Logistics Operating Systemは、先進的な倉庫技術とロボット工学と相まって、eコマース業務をシームレスに処理する力を企業に与えます。

この動きは英国のeコマース・ベンチャーに独特なフルフィルメント手段を提供し、国内及び欧州全域でのスムーズなスケーラビリティを可能にします。アライコを選択することは、欧州全域に広がるフルフィルメント・ハブのネットワークにより、より迅速な配送と簡素化された返品を意味します。欧州連合内で商品を保管し、直送を促進することにより、Alaikoは、潜在的な税関のハードルを回避し、迅速な国内配送と国境を越えた配送を保証します。

D2Cフルフィルメント市場は、多数のプロバイダーが競争しており、各プロバイダーは独自のサービス品質、価格体系、専門知識を誇り、多くの場合、ファッション、エレクトロニクス、健康と美容のようなニッチな製品カテゴリーに特化しています。

ダイレクト・トゥ・カスタマー・アウトソーシング・フルフィルメント市場動向

倉庫・保管部門が近い将来の市場成長を牽引

- オンラインショッピングの急増は、倉庫の運営方法に変化をもたらしています。オンラインショッピングが消費者に支持されるにつれ、eコマース企業は在庫を最適化し、注文を効率的に処理するという課題をますます抱えるようになっています。このため、倉庫スペースの需要が大幅に増加しています。2024年までに、世界の小売eコマース売上高は6兆3,000億米ドルを超えると予測されており、その後もさらなる成長が見込まれています。

- 効率的な在庫管理の必要性は、eコマース時代における倉庫需要の主要原動力のひとつです。eコマース事業者は、顧客の需要に応えるため、大量かつ多様な在庫を維持しなければならないです。倉庫は、これらの在庫を保管、整理、処理するための中心的な拠点であり、タイムリーな注文の履行を保証します。

- 消費者直接販売(D2C)ブランドの成長も、倉庫需要の急増に寄与しています。従来の小売チャネルをバイパスして顧客に直接販売するD2Cブランドは、製品を保管し、注文に効率的に対応するために専用の倉庫スペースを必要としています。

北米が市場シェアでトップに

- フルフィルメントサービスの北米市場は、eコマースと消費者直接販売(DTC)ビジネスモデルの急増に後押しされ、力強い成長を遂げています。北米のeコマース売上は右肩上がりで、合理化されたフルフィルメントソリューションへの需要が高まっている

- 米国のオンライン売上高は、2022年の1兆400億米ドルから2023年には約1兆1,190億米ドルに達し、成長率は7.6%に達します。これに対し、米国の小売総売上高は、2022年の約4兆9,040億米ドルから2023年には約5兆880億米ドルに増加し、成長率は約3.8%です。

- 米国商務省が報告したように、すべての小売業と外食産業の売上高を考慮すると、米国のeコマースは2023年第4四半期の売上高全体の15.6%を占めました。調整前の数字では、米国のeコマース売上は全体の17.1%を占めていました。商務省の推定によると、米国の年間eコマース売上高は1兆1,180億米ドルを超えました。

- 米国では、進化する消費者行動と技術の進歩により、倉庫の大型化が顕著な動向となっています。eコマース大手からサードパーティロジスティクス企業に至るまで、企業は倉庫の設置面積を大幅に拡大しています。こうした力学を理解し、戦略を市場の需要に合わせることは、企業にとってますます重要になってきています。

- 自動化のような先進技術を採用する企業が増えるにつれ、フルフィルメントプロセスの状況は進化しています。大規模倉庫へのシフトは、商品の保管、輸送、フルフィルメントの方法の変化を反映し、現代のサプライチェーン・マネジメントが機敏かつ効率的であることの必要性を強調しています。

ダイレクト・トゥ・カスタマー・アウトソーシング・フルフィルメント産業概要

ダイレクト・トゥ・カスタマー・アウトソーシング・フルフィルメント市場は、FedEx Fulfillment、Red Stag Fulfillment、PFS Commerce、FBA(Fulfillment by Amazon)、DCL Logisticsなどの主要企業を擁し、多様で激しい競合情勢を誇っています。これらの産業大手は、合併、買収、提携、事業拡大を活用して市場での存在感を高め、サービスポートフォリオを拡大してきました。

Amazonは、その強固なロジスティクスと膨大な顧客基盤により、市場の巨大企業として際立っています。一方、Walmart Fulfillmentはeコマースとオムニチャネルの領域で重要なパートナーシップを結び、戦略的にサービスを強化しています。

FedExは2024年1月、データ中心のコマースプラットフォームの先駆けである「fdx」を発表しました。この革新的なツールは、カスタマーの旅のすべてのステップをシームレスにつなぎ、需要の向上、転換率の向上、フルファッションの精度向上、返品の簡素化を実現する。特にFedExは、統一されたプラットフォームであらゆる規模の企業に対応する包括的なeコマースソリューションを提供する唯一のロジスティクス企業として際立っています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提

- 市場の定義

- 調査範囲

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場洞察

- 現在の市場シナリオ

- 技術動向

- 政府の取り組み

- バリューチェーンとサプライチェーン分析

- 返品処理に関する洞察

- 外注フルフィルメント価格の注目点

- COVID-19とその他の地政学的イベントが市場に与える影響

第5章 市場力学

- 市場促進要因

- eコマースの世界の急拡大が市場を牽引

- 倉庫の自動化と在庫管理における技術進歩の増加

- 市場抑制要因/課題

- 運用の複雑さが市場の抑制要因

- 市場に影響を与える規制

- 市場機会

- 新市場への進出が市場を牽引

- 持続可能性への取り組みが市場を牽引

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

第6章 市場セグメンテーション

- サービス別

- 倉庫・保管

- 流通

- 付加価値サービス

- 用途別

- ファッション・アパレル

- 民生用電子機器製品

- 民生用電子機器製品

- 家具

- 美容・パーソナルケア製品

- その他の用途(玩具、食品など)

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- シンガポール

- その他のアジア太平洋

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- オマーン

- エジプト

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- メキシコ

- その他の南米

- 北米

第7章 競合情勢

- Market Concentration

- 企業プロファイル

- FedEx Fulfillment

- Red Stag Fulfillment

- PFS Commerce

- FBA(Fulfillment by Amazon)

- DCL Logistics

- Sekel Tech

- WareIQ

- Ship Network(旧Rakuten Super Logistics)

- DHL Fulfillment

- ShipMonk

- Whiplash(A Part of Ryder System Inc.)*

- その他の企業

第8章 市場の将来

第9章 付録

- マクロ経済指標

- 資本フロー洞察(運輸・倉庫部門への投資)

- eコマースと消費関連統計

- 対外貿易統計

The Direct To Customer Outsourced Fulfillment Market size is estimated at USD 13.92 billion in 2025, and is expected to reach USD 26.45 billion by 2030, at a CAGR of 13.7% during the forecast period (2025-2030).

Companies often turn to outsourcing fulfillment as a key strategy for handling D2C orders. This approach entails enlisting a third-party logistics provider (3PL) to oversee warehouse, inventory, and shipping tasks. Outsourcing fulfillment appeals to firms lacking the in-house resources or expertise to manage these operations. By partnering with a 3PL, companies tap into their expertise and infrastructure, streamlining the fulfillment process. While this strategy helps cut fixed costs-like those associated with setting up and staffing a warehouse-it also allows companies to sharpen their focus on core competencies. Yet, relinquishing some control over the fulfillment process can potentially impact the overall customer experience.

In January 2024, Apollo Supply Chain, the logistics arm of Apollo Group, unveiled a new, all-encompassing e-commerce fulfillment and shipping service tailored for D2C brands. Industry insiders predict that India's D2C landscape, already bustling, could burgeon into a USD 60 billion industry by 2027.

Moreover, in June 2023, Alaiko, a prominent direct-to-consumer e-commerce fulfillment entity in Europe, made a strategic move by venturing into the United Kingdom. Alaiko forged a partnership with a cutting-edge fulfillment center in the north of London to cater to the local market. Setting itself apart, Alaiko prides itself on being a technology-centric fulfillment service. Its proprietary platform, Alaiko Logistics Operating System, coupled with advanced warehouse tech and robotics, empowers businesses to handle their e-commerce operations seamlessly.

This move offers UK e-commerce ventures a distinctive fulfillment avenue and positions them for smooth scalability domestically and across Europe. Opting for Alaiko translates to swifter deliveries and simplified returns, thanks to its expanding network of fulfillment hubs across Europe. By storing products within the European Union and facilitating direct shipping, Alaiko ensures rapid national and cross-border deliveries, sidestepping potential customs hurdles.

The D2C outsourced fulfillment market teems with competition as a multitude of providers vies, each boasting distinct service quality, pricing structures, and expertise, often specializing in niche product categories like fashion, electronics, or health and beauty.

Direct To Customer Outsourced Fulfillment Market Trends

Warehousing and Storage Segment to Drive Market Growth in the Near Future

- The surge in online shopping is transforming how warehouses operate. As online shopping gains traction among consumers, e-commerce companies are increasingly challenged to optimize inventory and fulfill orders efficiently. This has led to a significant uptick in demand for warehouse space. By 2024, global retail e-commerce sales were projected to surpass USD 6.3 trillion, with further growth anticipated in the subsequent years.

- The need for efficient inventory management is one of the primary drivers of demand for warehousing in the e-commerce era. E-commerce businesses must maintain large and diverse inventories to cater to customer demands. Warehouses are the central hubs for storing, organizing, and processing these inventories, ensuring timely order fulfillment.

- The growth of direct-to-consumer (D2C) brands has also contributed to the surge in warehousing demand. D2C brands bypassing traditional retail channels and selling directly to customers require dedicated warehousing space to store their products and fulfill orders efficiently.

North America is Set to Lead in Market Share

- The North American market for outsourced fulfillment services is witnessing robust growth, propelled by the surge in e-commerce and direct-to-consumer (DTC) business models. With e-commerce sales in North America on a steady rise, the demand for streamlined fulfillment solutions is escalating.

- US online sales hit approximately USD 1.119 trillion in 2023, up from USD 1.040 trillion in 2022, marking a growth rate of 7.6%. In comparison, total retail sales in the United States climbed to about USD 5.088 trillion in 2023 from roughly USD 4.904 trillion in 2022, reflecting a growth rate of about 3.8%.

- Factoring in all retail and food-service sales, US e-commerce made up 15.6% of the total sales in Q4 2023, as reported by the Commerce Department. The unadjusted figures revealed that US e-commerce sales represented 17.1% of the total sales. The Commerce Department's estimates suggested that the total US e-commerce sales for the year surpassed USD 1.118 trillion.

- There is a noticeable trend toward larger warehouses in the United States driven by evolving consumer behaviors and technological advancements. Businesses - from e-commerce giants to third-party logistics firms - are significantly expanding their warehouse footprints. Understanding these dynamics and aligning strategies with market demands is becoming increasingly crucial for businesses.

- With businesses increasingly adopting advanced technologies like automation, the landscape of fulfillment processes is evolving. The shift toward larger warehouses underscores the necessity for modern supply chain management to be agile and efficient, reflecting changes in how goods are stored, transported, and fulfilled.

Direct To Customer Outsourced Fulfillment Industry Overview

The direct-to-customer (D2C) outsourced fulfillment market boasts a diverse and fiercely competitive landscape, featuring key players like FedEx Fulfillment, Red Stag Fulfillment, PFS Commerce, FBA (Fulfillment by Amazon), and DCL Logistics. These industry leaders have leveraged mergers, acquisitions, partnerships, and expansions to bolster their market presence and broaden their service portfolios.

Amazon stands out as a market behemoth, credited to its robust logistics and vast customer base. On the other hand, Walmart Fulfillment has been strategically enhancing its offerings through key partnerships in the e-commerce and omnichannel realm.

In January 2024, FedEx Corp. unveiled 'fdx,' a pioneering data-centric commerce platform. This innovative tool seamlessly links every step of the customer's journey, empowering businesses to boost demand, enhance conversion rates, fine-tune fulfillment, and simplify returns. Notably, FedEx stands out as the sole logistics firm providing comprehensive e-commerce solutions, catering to businesses of all scales, all within a unified platform.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption

- 1.2 Market Definition

- 1.3 Scope of the Study

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Technological Trends

- 4.3 Government Initiatives

- 4.4 Value Chain and Supply Chain Analysis

- 4.5 Insights on Returns Processing

- 4.6 Spotlight on Outsourced Fulfillment Prices

- 4.7 Impact on COVID-19 and Other Geopolitical Events on The Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 The rapid expansion of e-commerce globally driving the market

- 5.1.2 Increasing technological advancements in warehousing automation and inventory management

- 5.2 Market Restraints/Challenges

- 5.2.1 Operational complexity hindering the market

- 5.2.2 Regulatory compliances affecting the market

- 5.3 Market Opportunities

- 5.3.1 Expansions into New Markets driving the market

- 5.3.2 Sustainability Initiatives driving the market

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Consumers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitutes Products and Services

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Service

- 6.1.1 Warehousing and Storage

- 6.1.2 Distribution

- 6.1.3 Value-Added Services

- 6.2 By Application

- 6.2.1 Fashion and Apparel

- 6.2.2 Consumer Electronics

- 6.2.3 Home Appliances

- 6.2.4 Furniture

- 6.2.5 Beauty and Personal Care Products

- 6.2.6 Other Applications (Toys, Food Products, Etc.)

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Spain

- 6.3.2.5 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 Japan

- 6.3.3.4 Singapore

- 6.3.3.5 Rest of Asia-Pacific

- 6.3.4 Middle East and Africa

- 6.3.4.1 Saudi Arabia

- 6.3.4.2 United Arab Emirates

- 6.3.4.3 Oman

- 6.3.4.4 Egypt

- 6.3.4.5 South Africa

- 6.3.4.6 Rest of Middle East and Africa

- 6.3.5 South America

- 6.3.5.1 Brazil

- 6.3.5.2 Mexico

- 6.3.5.3 Rest of South America

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration

- 7.2 Company profiles

- 7.2.1 FedEx Fulfillment

- 7.2.2 Red Stag Fulfillment

- 7.2.3 PFS Commerce

- 7.2.4 FBA (Fulfillment by Amazon)

- 7.2.5 DCL Logistics

- 7.2.6 Sekel Tech

- 7.2.7 WareIQ

- 7.2.8 Ship Network (Formerly Rakuten Super Logistics)

- 7.2.9 DHL Fulfillment

- 7.2.10 ShipMonk

- 7.2.11 Whiplash (A Part of Ryder System Inc.)*

- 7.3 Other companies

8 FUTURE OF THE MARKET

9 APPENDIX

- 9.1 Macroeconomic Indicators

- 9.2 Insight Into Capital Flows (Investments In Transport and Storage Sector)

- 9.3 E-commerce and Consumer Spending-related Statistics

- 9.4 External Trade Statistics