ソーシャルコマースロジスティクス:市場シェア分析、産業動向、成長予測(2025~2030年)

Social - Commerce Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636225

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

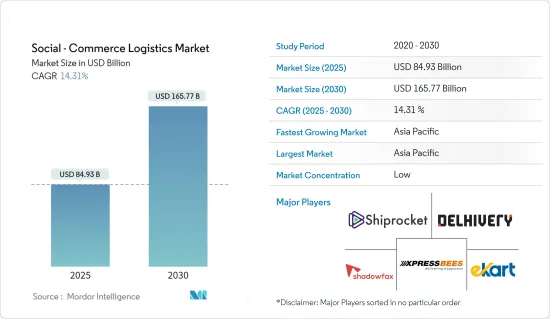

ソーシャルコマースロジスティクスの市場規模は2025年に849億3,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは14.31%で、2030年には1,657億7,000万米ドルに達すると予測されます。

主なハイライト

- eコマースとソーシャルメディアの融合であるソーシャルコマースは、世界中の小売業者と消費者との関わり方に革命をもたらしました。便利なオンラインショッピングの需要が急増する中、企業はこれらのプラットフォームを活用しています。ソーシャルメディアにより、買い物客はプラットフォームを離れることなくシームレスに商品を閲覧・購入できるようになり、購買プロセスが合理化されます。

- eコマースツールとしてのソーシャルメディアの人気は急上昇しています。2024年までに、ソーシャル・ショッピングの普及率は25.5%近くに達し、さらなる成長が予測されています。特筆すべきは、アジア市場、特にタイと中国が高い熱意を示していることで、オンライン消費者の約90%がソーシャル・ショッピングに積極的に参加しています。

- ソーシャルメディアは、消費者が買い物をする前のインスピレーションや発見の重要な情報源となっています。2023年の調査では、ソーシャルメディア・ユーザーの60%が、新しい製品やブランドを探索するためにこれらのプラットフォームを利用していることが明らかになった。2023年、フェイスブックは世界の買い物客の4分の1以上が好んで利用するソーシャルコマース・プラットフォームに浮上し、僅差で回答者の20%を集めたインスタグラムが続いた。メタが所有するフェイスブックとインスタグラムは、最も魅力的なソーシャルコマース体験を提供するソーシャルネットワークのトップです。世界中で、ソーシャルネットワーク経由で購入される最も人気のある商品カテゴリーは、アパレル、パーソナルケアアイテム、食料品、食品などです。

- ソーシャル・コマースはあらゆる年齢層で支持を集めており、中でも若い消費者が牽引役となっています。デジタル時代に育ったZ世代と、経済的自立を楽しんでいるミレニアル世代は、特にソーシャルメディア・ショッピングに熱心です。これらのグループは、動機こそ異なるもの、単なる取引よりもショッピング体験をしたいという共通の願望を持っています。このような共通の傾向から、彼らはインフルエンサーや有名人が支持する商品を非常に受け入れやすいです。2023年の調査では、プロモーションと購入プロセスの簡素化がソーシャルコマースのエンゲージメントを高める上で極めて重要であることが強調されています。

ソーシャルコマースロジスティクス市場の動向

B2Cソーシャルコマース需要の高まりが市場成長を牽引

幅広い顧客基盤、消費者エンゲージメントの機会、顧客との直接的な関係構築能力によって、B2Cセグメントはソーシャルコマースロジスティクス市場の要となっています。ソーシャル・メディアの推奨、強固な購買パターン、シームレスなモバイル・インターフェースなどの要因により、B2Cソーシャル・コマースは拡大しています。

最近では、ソーシャル・ネットワーキング・プラットフォームを利用した直接eコマース取引が急増しています。これらのプラットフォームは、企業にとって不可欠なツールへと進化し、ブランドの認知度を高めるだけでなく、直接収益を生み出すことを可能にしています。消費者がますますソーシャルメディアに集まる中、企業は膨大なオーディエンスのリーチを活用しています。フェイスブック、インスタグラム、ピンタレスト、ティックトックなどのプラットフォームは、数十億とは言わないまでも数百万人のユーザーベースを誇り、B2Cの格好の舞台となっています。

今日の消費者、特にミレニアル世代とZ世代は、即座の満足を切望しています。モバイルテクノロジーの急速な進化に伴い、彼らはデジタルでブランドと関わる斬新な方法を積極的に模索しています。特に、購買の60%以上がソーシャルメディア・プラットフォームを通じて行われており、ソーシャル・コマースにおける若年層の優位性が際立っています。

人口、デジタル決済、ソーシャルメディアの影響力が市場を独占するアジア太平洋地域

東南アジアではソーシャルメディアの利用が浸透しており、同地域の主要国での普及率は68.9%から91.7%となっています。膨大な消費者基盤だけでなく、東南アジアはソーシャルメディアへのエンゲージメントも高いです。ここでのソーシャルコマースの成功の鍵は、消費者がソーシャルプラットフォームをどのように活用するかにかかっています。東南アジアでは、ソーシャルメディアが新製品の発見、ブランドの検討、製品調査の主要な手段として君臨しています。さらに、利便性の高さが、消費者にソーシャル・コマースを受け入れさせる最大の理由となっています。

パンデミックは、東南アジアの買い物習慣に大きな変化をもたらし、オンライン・ショッピングが顕著に急増しました。アプリやウェブサイトでの購入が大幅に増加した一方で、ソーシャルコマースに初めて参入したユーザーも目立った。注目すべきは、ソーシャルコマースの普及率と市場規模が東南アジア各地で異なることです。例えば、ベトナムのソーシャルコマースロジスティクス市場は、同地域のeコマース大国であるインドネシアよりも小さいもの、地歩を固めつつあります。ベトナムはソーシャル・コマースへの関心が高いだけでなく、初めてソーシャル・コマースを利用するユーザーの割合も東南アジアで最も高いです。

アジア太平洋地域では、TikTok Shopがソーシャルコマースの分野で極めて重要なプレーヤーとして台頭しています。バイラルコンテンツ、インフルエンサーによる推薦、ライブストリーミングを通じて、ユーザーが偶然商品を見つけるというユニークなアプローチは、オンラインショッピングに革命をもたらしただけでなく、この地域のデジタル経済にも大きな影響を与えました。

インドネシア、タイ、マレーシアなどの国々では、TikTok Shopはモバイル普及率の急上昇とオンラインショッピングへの意欲の高まりを利用しています。これにより、中小企業は前例のない市場アクセスを手に入れました。同プラットフォームの際立った特徴は、クリエイターとマルチチャンネルネットワーク(MCN)を統合し、「ショッパーエンタテインメント」と呼ぶものを開拓していることです。競合他社とは異なり、TikTokの親会社であるByteDanceは、このショッピングとエンターテイメントの融合を迅速に活用し、ソーシャル・プラットフォームにおけるeコマースの新たな基準を打ち立てた。

ソーシャルコマースロジスティクス業界の概要

ソーシャルコマースロジスティクス市場は細分化されています。Shiprocket、Delhivery、Ekart、XpressBees、Shadowfax、Ecom Express、Blue Dart、Wow Express、Gati、Rivigoなどの主要企業が市場を独占しています。これらの企業は、特にソーシャルコマース企業向けに設計された物流ソリューションを専門としています。これらの企業は、効率的で信頼性の高いサービスを提供することに重点を置いており、ソーシャルメディア販売の増加傾向に対応しています。市場の競合要因としては、配送スピード、コスト効率、技術統合、一流のカスタマーサービスなどが挙げられるが、これらはすべてソーシャルコマース領域の明確なニーズに合わせたものです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 現在の市場シナリオ

- 市場力学

- 促進要因

- ソーシャルメディア・プラットフォームの増加

- オンライン購入への消費者嗜好のシフト

- 抑制要因

- 個人データの収集と利用に対するプライバシー保護への懸念

- ソーシャルコマース領域における激しい競合

- 機会

- ニッチ市場にリーチするためのインフルエンサーとのコラボレーション

- 促進要因

- バリューチェーン/サプライチェーン分析

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 技術開発

- 地政学とパンデミックが市場に与える影響

第5章 市場セグメンテーション

- ビジネスモデル別

- 企業対消費者(B2C)

- 企業対企業(B2B)

- 消費者間(C2C)

- サービス別

- 輸送

- 倉庫・在庫管理

- 付加価値サービス(ラベリングとパッケージング)

- 製品タイプ別

- パーソナル&ビューティーケア

- アパレル

- アクセサリー

- 家庭用品

- 健康補助食品

- 飲食品

- その他の製品タイプ

- 販売チャネル別

- ビデオコマース

- ソーシャル・ネットワーク主導型コマース

- ソーシャル再販

- グループ購入

- 製品レビュープラットフォーム

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米

- 欧州

- 英国

- ドイツ

- フランス

- ロシア

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- 市場集中の概要

- 企業プロファイル

- Shiprocket

- Delhivery

- Ekart

- XpressBees

- Shadowfax

- Ecom Express

- Blue Dart

- Wow Express

- Gati

- Rivigo*

- その他の企業

第7章 市場の将来

第8章 付録

目次

The Social - Commerce Logistics Market size is estimated at USD 84.93 billion in 2025, and is expected to reach USD 165.77 billion by 2030, at a CAGR of 14.31% during the forecast period (2025-2030).

Key Highlights

- Social commerce, the fusion of e-commerce and social media, has revolutionized how retailers worldwide interact with consumers. With the surge in demand for convenient online shopping, companies are capitalizing on these platforms. Social media allows shoppers to seamlessly browse and buy products without leaving the platform, streamlining the purchasing process.

- The popularity of social media as an e-commerce tool is surging. By 2024, the penetration rate of social shopping is set to hit nearly 25.5%, with further growth projected. Notably, Asian markets, especially Thailand and China, show high enthusiasm, with around 90% of online consumers actively engaging in social buying.

- Social media is a significant source of inspiration and discovery for consumers before shopping. A 2023 survey revealed that 60% of social media users utilized these platforms to explore new products and brands. In 2023, Facebook emerged as the favored social commerce platform for over a quarter of global shoppers, closely followed by Instagram, which garnered 20% of respondents' preferences. Both Facebook and Instagram, owned by Meta, are the top social networks that provide the most compelling social commerce experiences. Across the globe, the most popular product categories purchased via social networks include apparel, personal care items, groceries, and food.

- Social commerce has gained traction across all age groups, with younger consumers leading the charge. Gen Z, having grown up in the digital age, and millennials, enjoying financial independence, are particularly keen on social media shopping. While these groups differ in motivations, they share a common desire to engage in shopping experiences over mere transactions. This shared inclination makes them highly receptive to products endorsed by influencers and celebrities. A 2023 study highlighted that promotions and simplified purchase processes are pivotal in boosting social commerce engagement.

Social - Commerce Logistics Market Trends

Rising B2C Social commerce Demand Steers Market Growth

Driven by its expansive customer base, opportunities for consumer engagement, and the ability to foster direct client relationships, the B2C segment stands as the cornerstone of the social commerce logistics market. With factors such as social media recommendations, robust purchasing patterns, and a seamless mobile interface, B2C social commerce is expanding.

Recently, there has been a surge in the utilization of social networking platforms for direct e-commerce transactions. These platforms have evolved into indispensable tools for businesses, enabling them not only to enhance brand visibility but also to generate revenue directly. As consumers increasingly flock to social media, businesses are capitalizing on the vast audience reach. Platforms like Facebook, Instagram, Pinterest, and TikTok boast user bases in the millions, if not billions, making them prime B2C arenas.

Today's consumers, especially millennials and Gen Z, crave instant gratification. With the rapid evolution of mobile technology, they are actively seeking novel ways to engage with brands digitally. Notably, over 60% of purchases are transacted through social media platforms, underscoring the dominance of younger demographics in social commerce.

Asia-Pacific Dominates the Market, Fueled by Population, Digital Payments, and Social Media Influence

Social media usage is pervasive in Southeast Asia, with penetration rates ranging from 68.9% to 91.7% in the region's key countries. Beyond its vast consumer base, Southeast Asia also boasts high social media engagement. The crux of social commerce's success here hinges on how consumers leverage social platforms. In Southeast Asia, social media reigns as the primary avenue for new product discovery, brand consideration, and product research. Moreover, the convenience it offers stands out as the top reason driving consumers to embrace social commerce.

The pandemic catalyzed a significant shift in Southeast Asian shopping habits, with a notable surge in online shopping. While app and website purchases saw a substantial uptick, a noteworthy segment of users ventured into social commerce for the first time. Notably, the adoption rates and market sizes of social commerce vary across Southeast Asia. For instance, Vietnam's social commerce logistics market, though smaller than Indonesia's, the region's e-commerce giant, is gaining ground. Vietnam not only leads in social commerce interest but also boasts the highest share of first-time users in the region.

Within Asia-Pacific, TikTok Shop emerged as a pivotal player in the social commerce arena. Its unique approach, where users stumble upon products through viral content, influencer endorsements, and live streams, has not only revolutionized online shopping but also made a significant impact on the region's digital economy.

In nations like Indonesia, Thailand, and Malaysia, TikTok Shop has capitalized on the surging mobile penetration rates and the increasing appetite for online shopping. This has empowered small and medium-sized enterprises with unprecedented market access. The platform's standout feature is its integration of creators and multi-channel networks (MCNs), pioneering what it terms "shoppertainment." Unlike its competitors, ByteDance, TikTok's parent company, swiftly leveraged this fusion of shopping and entertainment, setting a new benchmark for e-commerce on social platforms.

Social - Commerce Logistics Industry Overview

The social commerce logistics market is fragmented in nature. Several key players dominate the market studied, including Shiprocket, Delhivery, Ekart, XpressBees, Shadowfax, Ecom Express, Blue Dart, Wow Express, Gati, and Rivigo. These firms specialize in logistics solutions designed specifically for social commerce enterprises. Their emphasis lies in delivering efficient and dependable services, aligning with the rising trend of social media sales. Key competitive factors in the market include delivery speed, cost efficiency, tech integration, and top-tier customer service, all tailored to the distinct needs of the social commerce realm.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Growing Number of Social Media Platforms

- 4.2.1.2 Shift in Consumer Preferences Toward Online Purchase

- 4.2.2 Restraints

- 4.2.2.1 Privacy Concerns Over Gathering and Using Personal Data

- 4.2.2.2 Intense Competition in the Social Commerce Space

- 4.2.3 Opportunities

- 4.2.3.1 Collaboration with Influencers to Reach Niche Markets

- 4.2.1 Drivers

- 4.3 Value Chain/Supply Chain Analysis

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Technological Developments

- 4.6 Impact of Geopolitics and Pandemics on the Market

5 MARKET SEGMENTATION

- 5.1 By Business Model

- 5.1.1 Business-to-consumer (B2C)

- 5.1.2 Business-to-business (B2B)

- 5.1.3 Consumer-to-consumer (C2C)

- 5.2 By Service

- 5.2.1 Transportation

- 5.2.2 Warehousing and Inventory Management

- 5.2.3 Value-added Services (Labeling and Packaging)

- 5.3 By Product Type

- 5.3.1 Personal and Beauty Care

- 5.3.2 Apparel

- 5.3.3 Accessories

- 5.3.4 Home Products

- 5.3.5 Health Supplements

- 5.3.6 Food and Beverages

- 5.3.7 Other Product Types

- 5.4 By Sales Channel

- 5.4.1 Video Commerce

- 5.4.2 Social Network-Led Commerce

- 5.4.3 Social Reselling

- 5.4.4 Group Buying

- 5.4.5 Product Review Platforms

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Italy

- 5.5.2.6 Spain

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Shiprocket

- 6.2.2 Delhivery

- 6.2.3 Ekart

- 6.2.4 XpressBees

- 6.2.5 Shadowfax

- 6.2.6 Ecom Express

- 6.2.7 Blue Dart

- 6.2.8 Wow Express

- 6.2.9 Gati

- 6.2.10 Rivigo *

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日